About the use of inclusive language in this publication

The use of language that does not discriminate and that makes all gender identities visible is an institutional commitment of the Central Bank of the Argentine Republic. This publication recognizes the influence of language on ideas, feelings, ways of thinking and evaluation schemes.

This document has sought to avoid sexist and binary language. However, for ease of reading, resources such as “@” or “x” are not included.

Executive summary

• In November, the financial system continued to develop its financial intermediation activity and the provision of means of payment, preserving high margins of solvency, liquidity and forecasts. The sector’s performance has been underpinned by the various measures adopted by the BCRA in order to contribute to greater access to credit, the safeguarding of savings in national currency and increasing efficiency in the operations of the payment system, preserving the conditions for financial stability.

• In November, the balance of credit to the private sector in pesos increased slightly in real terms compared to the previous month, increasing nominally by just over 3.2%. With this performance, credit to the private sector in pesos accumulated a real year-on-year growth (y.a.) of 10.9%, highlighting financing through documents and credit cards.

• Within the framework of the new Financing scheme for Productive Investment of MSMEs, until the end of January 2021, the set of entities disbursed $221,280 million, reaching 65,772 companies. Going forward, this institution will continue to promote measures to deepen the credit channel in order to meet the financing needs of the private sector (mainly MSMEs, either through working capital or for investment projects).

• In a context in which the modification of the parameters for classifying debtors and the possibility of transferring unpaid installments at the end of the life of the loan are still in force, in November the ratio of irregularity of credit to the private sector fell slightly to 4.1%. In the month, the relative level of forecasting of the aggregate financial system remained high compared to what has been observed in the last 15 years, representing 5.8% of total credit to the private sector and 139.9% of the portfolio in an irregular situation.

• The balance of deposits in pesos of the private sector in real terms fell in November, although it accumulated a growth of 37.8% y.o.y. (87.2% y.o.y. nominal) driven by both the term and demand segments.

• The financial institutions as a whole continued to exhibit high levels of liquidity. In November, liquid assets totaled 64% of deposits at the systemic level, with no changes in magnitude compared to last month and 6.7 p.p. above the level of November 2019.

• The solvency indicators of all financial institutions increased in the month. The capital integration (RPC) of the financial system reached 23.2% of risk-weighted assets (RWA) in November, 0.2 p.p. more than last month. The capital position (integration minus capital requirement) of the institutions as a whole stood at 175% of the regulatory requirement in November, 6.7 p.p. more than in October.

• In relation to the profitability indicators in real terms of the system at the aggregate level, positive levels are maintained with a pattern of gradual decline. In the 11 months of 2020 as a whole, the entities as a whole accrued comprehensive results in homogeneous currency equivalent to 2.2% annualized (y.) of assets (ROA) and 14.7% y. of equity (ROE). Particularly in the month of November, ROA reached 1.8% y/y and ROE 11.9%y/y, both records being lower than the annual cumulative.

I. Financial intermediation activity

According to the estimated flow of funds on items in national currency1, at the aggregate level it was observed that in November the decrease in liquidity in the broad sense was the main source of resources for all financial institutions. Meanwhile, the reduction in private and public sector deposits was the most prominent fund application in month2.

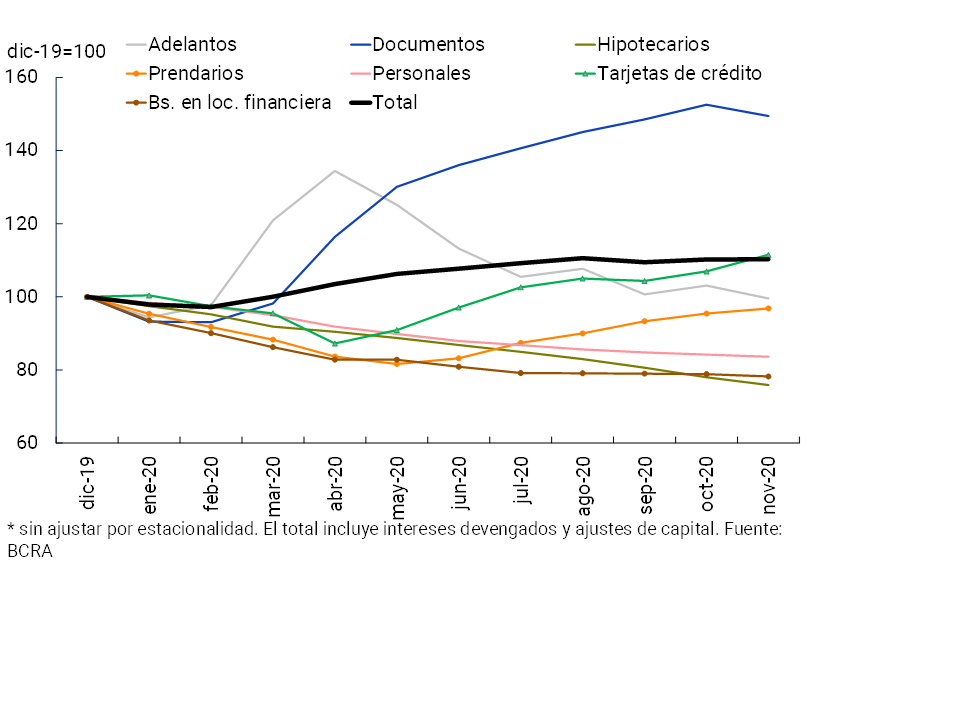

In November, the real balance of credit to the private sector in national currency increased slightly compared to the previous month (+0.1%; +3.2% nominal) (see Chart 1)3. Within the segment in pesos, there was a heterogeneous behavior in the period, with increases in cards and pledges and decreases in the rest of the credit lines. It should be noted that based on the measures promoted by the BCRA in order to promote financing in pesos, during 2020 an outstanding performance was observed in loans instrumented via documents, with a real growth of more than 52% between March and November and, to a lesser extent, in credit cards. With regard to the evolution by group of entities, in the month the financing channeled by public financial institutions and by non-banking financial institutions (NFFIs) showed a real increase, while in the rest of the groups of entities they fell4.

Graph 1 | Credit balance to the private sector in pesos

In real terms*

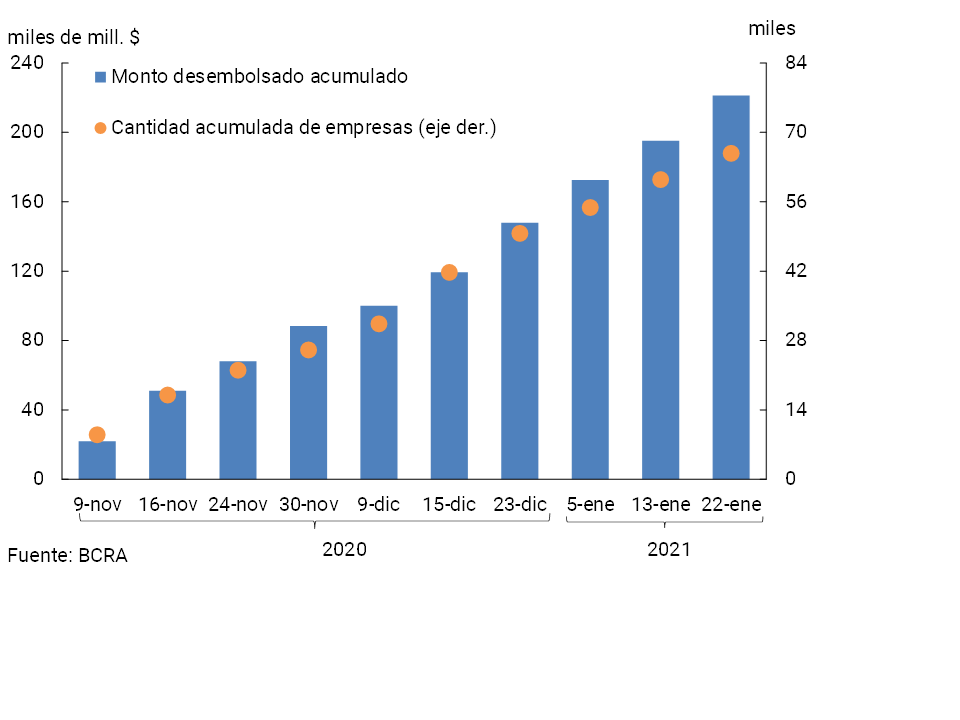

Within the framework of the new Financing for Productive Investment of MSMEs5 scheme, from its entry into force until the end of January 2021, $221,280 million were disbursed (of which $37,753 million correspond to investment projects), distributed among 65,772 companies (see Graph 2)6. Distinguishing by group of financial institutions, those with national private capital accounted for 38% of the total disbursements, public ones accounted for 34% and foreign private ones accounted for 28%. It should be noted that, within the framework of what is mentioned in the objectives and plans for 2021 recently published by the BCRA7, this Institution will continue to deepen the credit channel, in order to continue meeting the financing needs of the private sector (mainly MSMEs, either through working capital or for investment projects).

Graph 2 | Financing line for productive investment of MSMEs

Additionally, through the line of financing at subsidized interest rates for companies enrolled in the “Emergency Assistance Program for Work and Production” (ATP)8, until the end of January 2021, $12,931 million were granted, channeling more than 550,600 workers.

For its part, within the framework of the credit lines aimed at single-tax and self-employed persons, through the Zero Rate Credit Line9 until the end of January, 561,931 loans were granted for a total equivalent to $66,474 million (99.5% already disbursed). The implementation of this line influenced the issuance of 249,316 new credit cards and the opening of 777 demand accounts for the accreditation of these credits. In addition, through the Cultura10 Zero-Rate Credit line, $304 million (93.3% already credited) were granted through 2,902 loans.

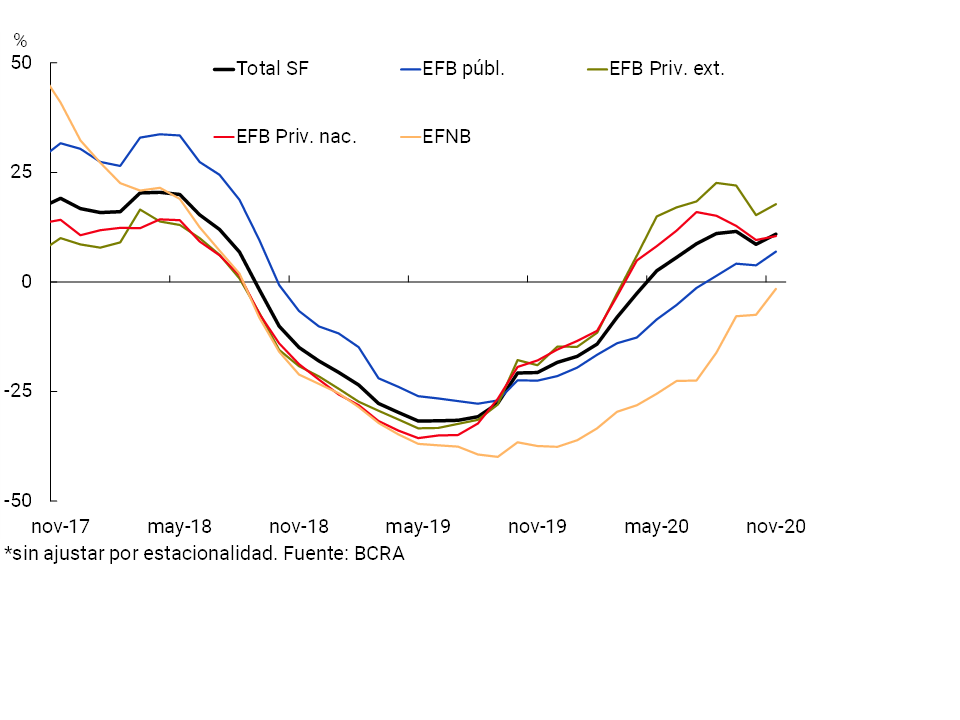

Financing in pesos to the private sector increased 10.9% YoY in real terms in November, thus registering seven consecutive months with positive year-on-year variations. Loans channeled by private entities verified the largest relative year-on-year increases in the period (see Graph 3).

Graph 3 | Credit balance to the private sector in pesos

By group of financial institutions – Var. % real a.y.*

For its part, in November the balance of credit in foreign currency to the private sector decreased 2.5% – in source currency – compared to October. Thus, total financing to the private sector (in domestic and foreign currency) fell 0.2% in real terms in the month and 4.5% YoY in real terms.

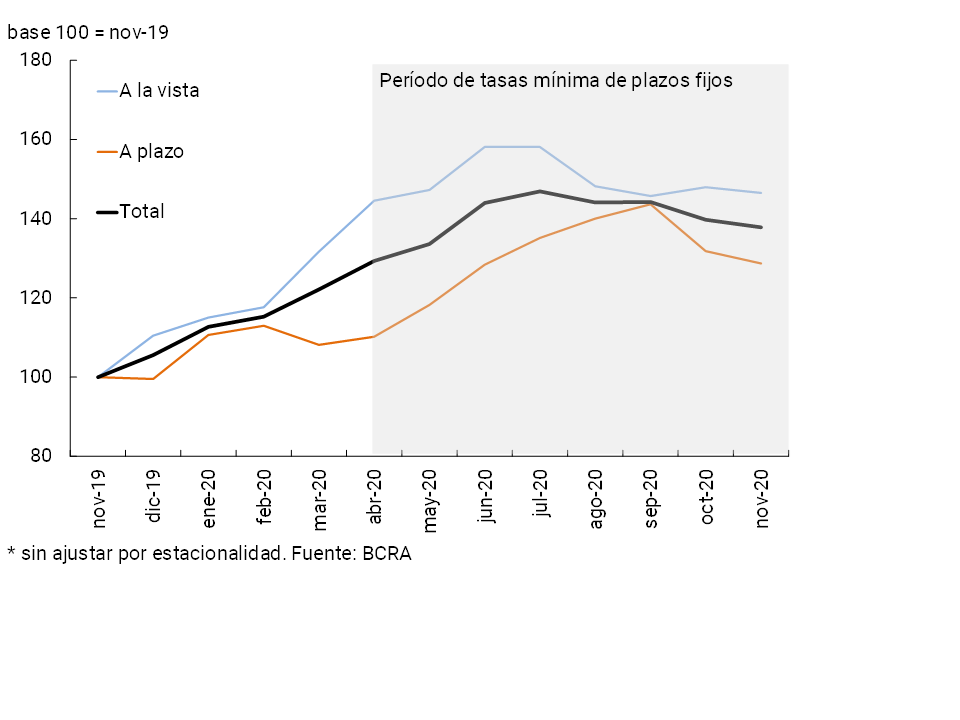

On the funding side of the aggregate financial system, the balance of deposits in pesos of the private sector fell by 1.4% in real terms in November (+1.7% nominal) (see Chart 4). Time deposits in pesos decreased 2.3% in real terms compared to October (+0.7% nominal), while demand accounts fell 1% in real terms (+2.2% nominal).

Figure 4 |Balance of private sector deposits in pesos

In real terms*

Meanwhile, the balance of deposits in foreign currency of the private sector remained without significant changes compared to October —in currency of origin—. In this context, the real balance of total private sector deposits (in domestic and foreign currency) fell 1% in the month and accumulated a real increase of 20.5% in year-on-year terms.

For their part, public sector deposits in national currency decreased 5.4% in real terms in the month (-2.4% nominal). Thus, total deposits in pesos (from the public and private sectors) fell 2.2% in real terms compared to October (0.9% nominal).

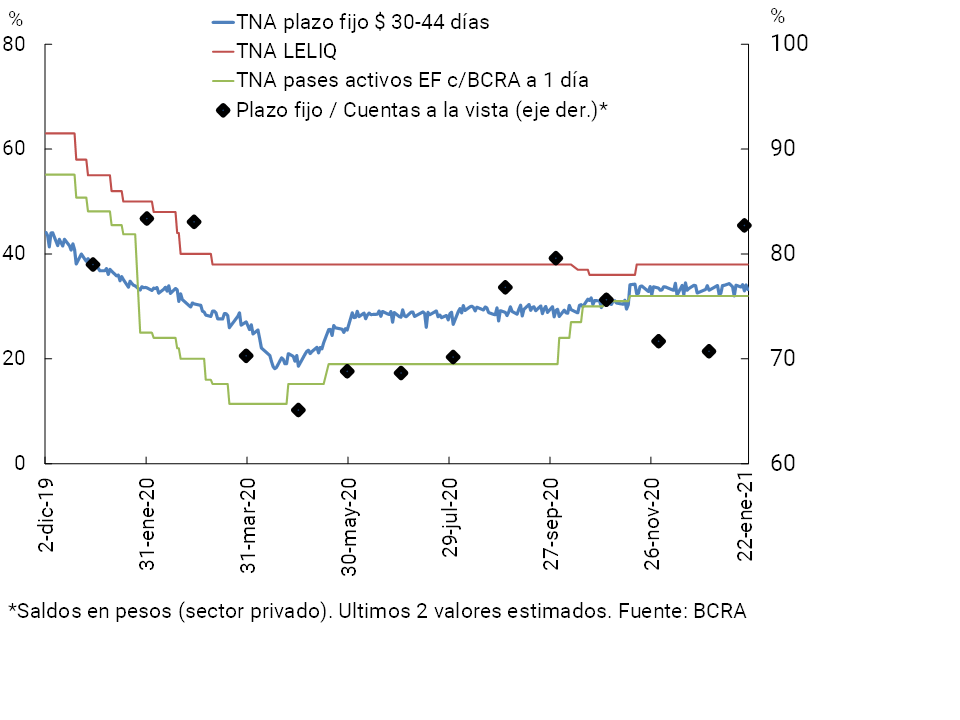

Throughout November, the BCRA continued to carry out a progressive harmonization of interest rates on monetary policy instruments (see Chart 5). In the month, the interest rate on passive passes for the BCRA (assets for financial institutions) was raised to one and seven days, and the interest rate on LELIQ was increased. At the same time, in order to promote returns in line with inflation levels and to encourage savings in pesos, the minimum guaranteed interest rate on fixed-term deposits in pesos was increased during the period (37% nominal annual rate for those of up to $1 million constituted by individuals and 34% nominal annual rate for the rest)11.

Graph 5 | Interest rates and deposits in pesos*

In year-on-year terms, in November private sector deposits in pesos accumulated a growth of 37.8% in real terms (87.2 nominal y.o.y.), a variation similar to that observed in public sector deposits in the same denomination. As a result, the balance of total deposits (public and private sector) in pesos increased by 36% YoY in real terms (84.7% YoY nominal).

II. Aggregate composition of the balance sheet

The assets of the financial system fell in real terms by 0.6% in November, mainly due to the performance of public financial institutions (see Chart 6). It is worth mentioning that since the middle of the year the dynamism of the total assets of the aggregate financial system decreased, in line with the lower monetary issuance needs generated from a certain morigeration of the extraordinary measures promoted by the National Government to assist families and companies, in a context of normalization of certain economic activities – although still heterogeneous. In this sense, the sterilization needs were limited, and consequently the holding of LELIQ in the portfolio of financial institutions ceased to increase.

Graph 6 | Total Asset Balance

In real terms

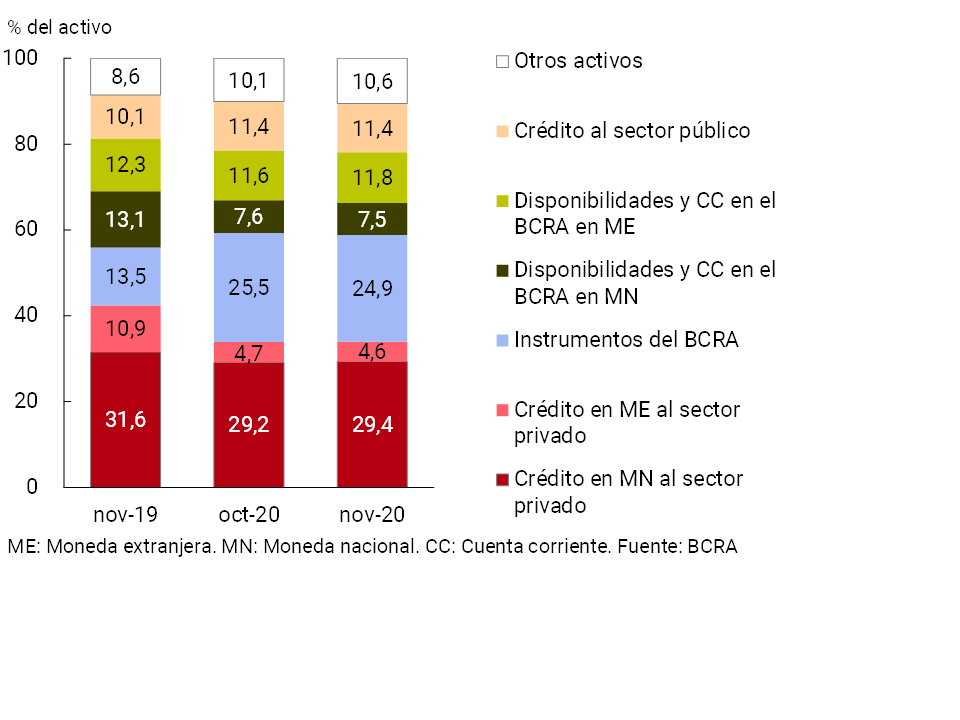

In relation to the composition of the assets of the financial system, in November the relevance of credit to the private sector in pesos increased slightly (to a total of 29.4%), while the balance of LELIQ (holdings and passes with the BCRA) decreased its relative weight (to represent 24.9%, see Graph 7). With respect to items in foreign currency, it was observed that credit to the private sector decreased its relative importance in the month and that of the most liquid assets increased.

Figure 7 | Composition of total assets

Financial system – Share %

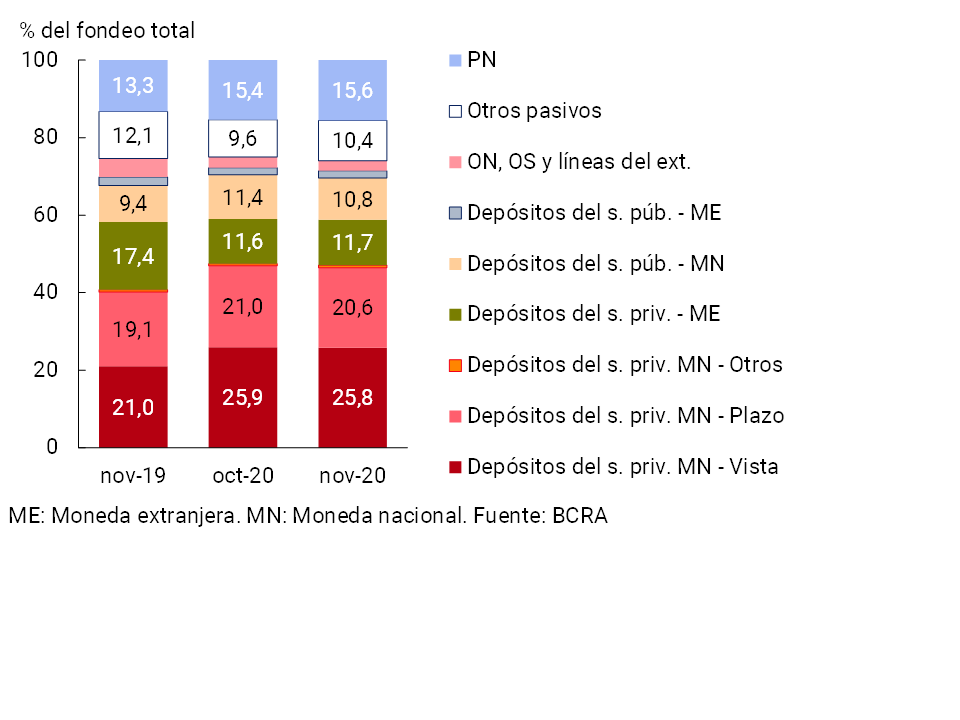

With regard to bank funding, in November the share of public sector deposits in national currency fell (to 10.8%) and private sector time deposits (to 20.6%, see Chart 8).

Figure 8 | Total system funding composition

In % of total funding (liabilities + equity)

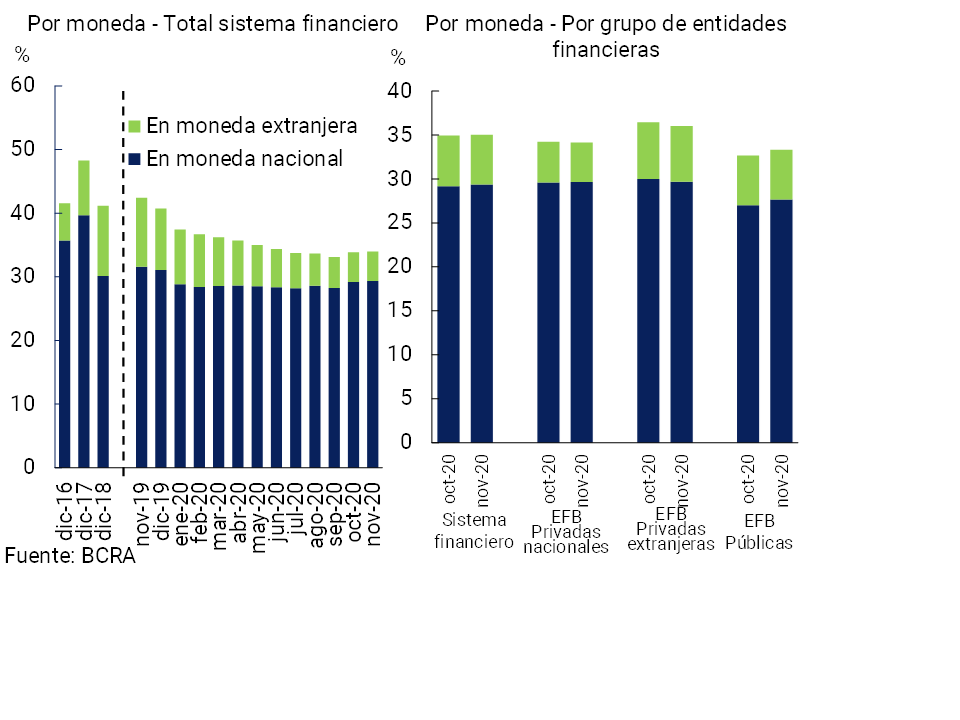

When considering the balance sheet items of the financial system denominated in foreign currency, as of November the corresponding asset accounts maintained their weighting in the total compared to last month (standing at 19.1%), while on the liability side they slightly increased their participation in total funding in the same period (+0.2 p.p. to 17.2%). However, this monthly performance, in year-on-year terms, there was a reduction of 7.7 p.p. in the share of assets in foreign currency over total assets and of 8 p.p. in the case of the ratio that considers liabilities. In November, the spread between assets and liabilities in foreign currency, plus the net balance of forward purchase/sale transactions of foreign currency, totaled 13.8% of regulatory capital, 0.7 p.p. less than in October and 1.9 p.p. more than in the same month of 2019 (see Chart 9).

Figure 9 | EM Assets – EM Liabilities + EM Forward Position (Financial System)

III. Portfolio quality

The total credit balance to the private sector (including domestic and foreign currency) stood at 34% of the assets of the financial system in November. This level was higher than in the previous month as mentioned in the previous section, thus verifying an increase in the gross exposure of the financial system to the private sector for the second consecutive month. Considering only the balance of financing in pesos, this ratio increased 0.2 p.p. compared to October (see Chart 10), a movement led by national public and private entities.

Figure 10 | Credit balance to the Private Sector / Assets

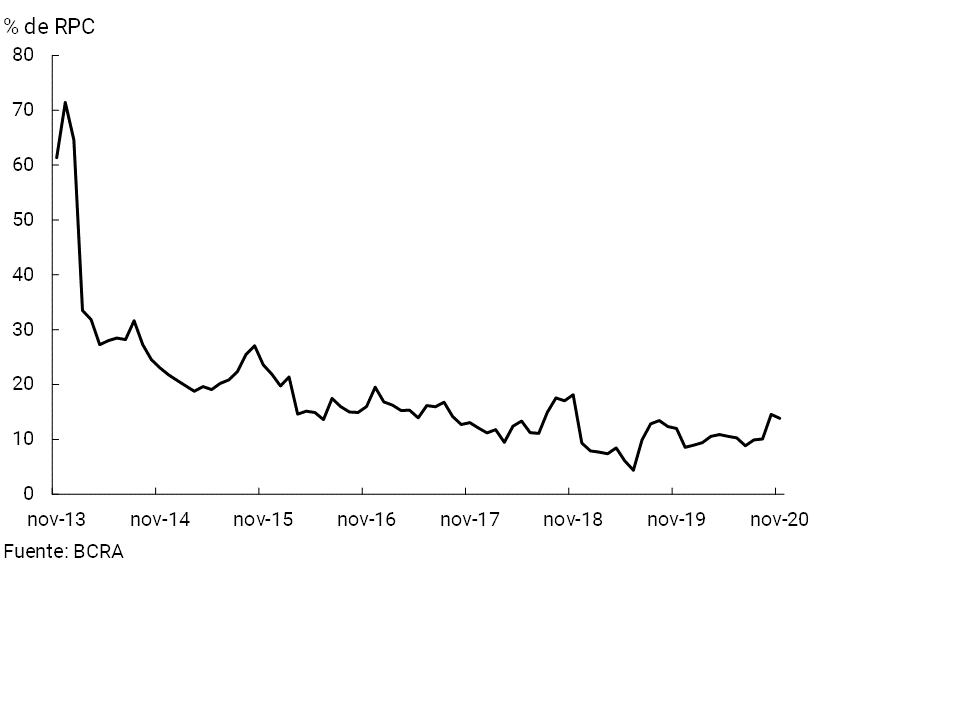

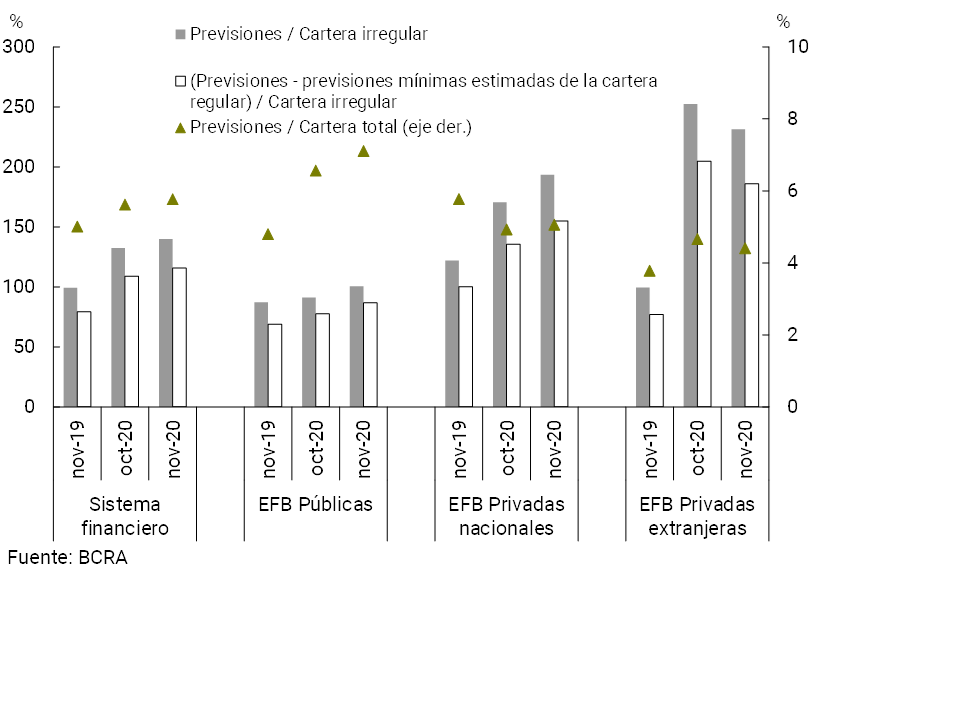

In a scenario in which the modification of the parameters for classifying debtors and the possibility of transferring unpaid installments at the end of the life of the credit – accruing onlycompensatory interest 12 – remain in force, the ratio of irregularity of credit to the private sector continued to decrease. Thus, as of November, the NPL indicator totaled 4.1%, slightly lower than in the previous month (see Graph 11). This fall was verified in all groups of financial institutions with the exception of foreign private ones.

Figure 11 | Irregularity of credit to the private sector

Irregular financing / Total financing (%)

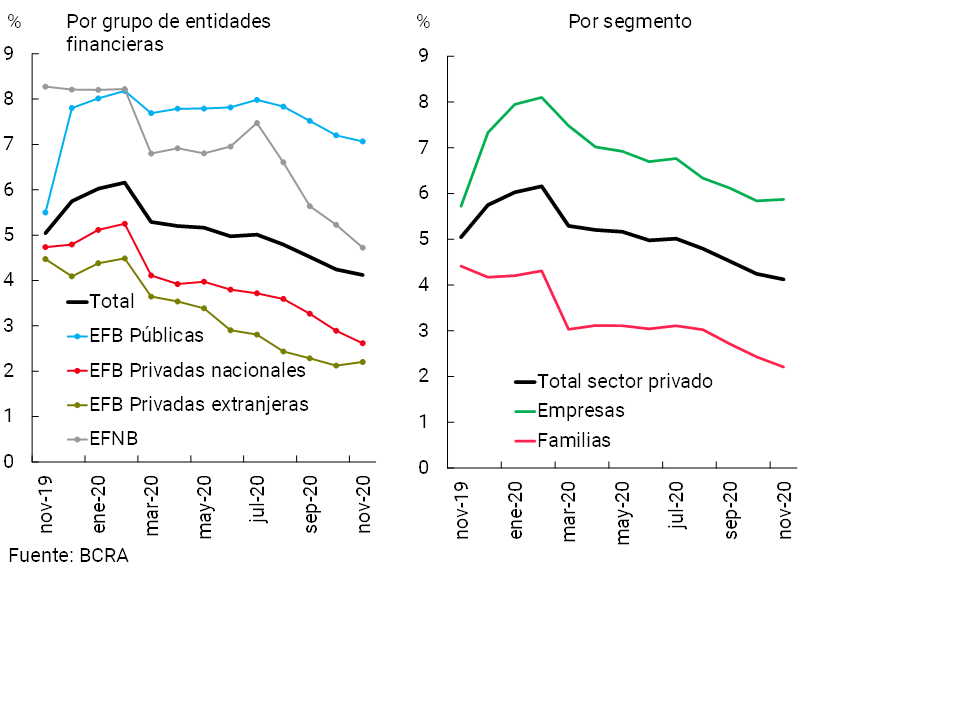

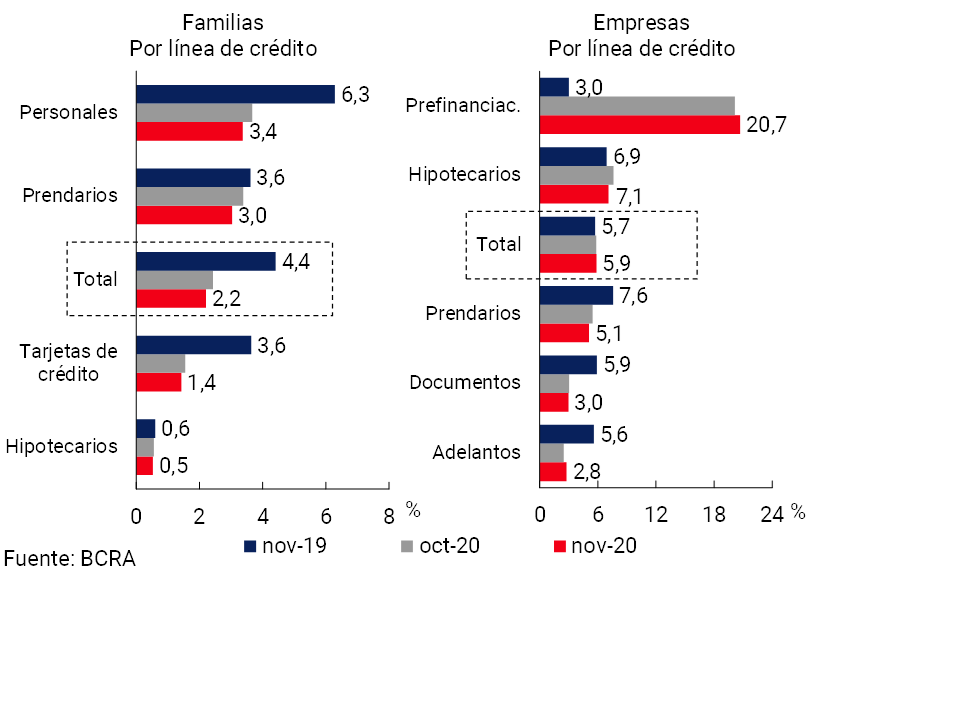

When analyzing by type of debtor, the monthly performance was explained by the credit destined to families. The non-performing loan ratio of these loans stood at 2.2%, down 0.2 p.p. compared to October. This decrease was generalized among the different lines, with the behavior of collateral and personal loans standing out (see Graph 12). As for credit to companies, the irregularity remained stable in November, at around 5.9%, presenting a disparate behavior between the lines: an increase in loans via advances and pre-financing to exports13 and a reduction in loans with real guarantees.

Figure 12 | Irregularity of credit to the private sector

Irregular financing / Total financing (%)

In November, the financial system as a whole continued to present comfortable levels of forecasting. At the aggregate level, the forecasts represented 5.8% of total credit to the private sector, 0.1 p.p. more than in the previous month and 0.8 p.p. above the level of a year ago (see Chart 13). The balance of total accounting forecasts represented 139.9% of the balance of credit to the private sector in an irregular situation, increasing 7.4 p.p. compared to October and 40.6 p.p. y.o.y. On the other hand, the balance of regulatory forecasts attributable to the non-performing portfolio (following the criteria of the minimum regulatory forecasts for uncollectibility risk) totaled 115.7% of said portfolio in November

Figure 13 | Credit to the private sector and forecasts

By Entity Group

IV. Liquidity and solvency

The financial system as a whole continued to exhibit relatively high liquidity and solvency margins, in particular exceeding international standards.

During November, the verified levels in liquidity ratios that are in line with the Basel Committee’s recommendations – Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) – for the group of entities obliged to comply with these requirements (Group A) continued to practically double the minimum required at the local level14, Question 15.

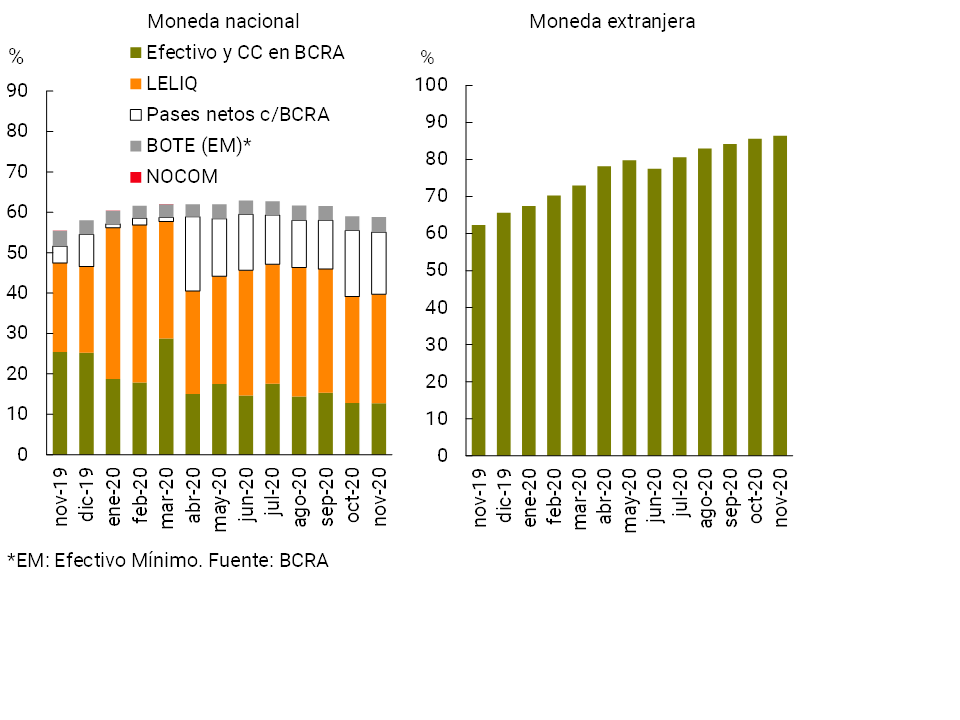

In November, the balance of the set of liquid assets in the broad sense for the aggregate of financial institutions16 represented 64% of total deposits (58.8% for the segment in pesos and 86.4% for items in foreign currency), with smaller changes in the month (-0.2 p.p. and +0.8 p.p. for items in local currency and in foreign currency, respectively) (see Figure 14). Within the segment in pesos, in the month the composition of liquid assets turned towards a greater share of LELIQ’s holdings, and a reduction in net passes against the BCRA and the balance in the current accounts held by the entities in this Institution17, 18. In a year-on-year comparison, the broad liquidity indicator increased 6.7 p.p. of deposits, a performance that was mainly explained by liquidity in foreign currency.

Figure 14 | Liquidity of the financial system

In % of deposits

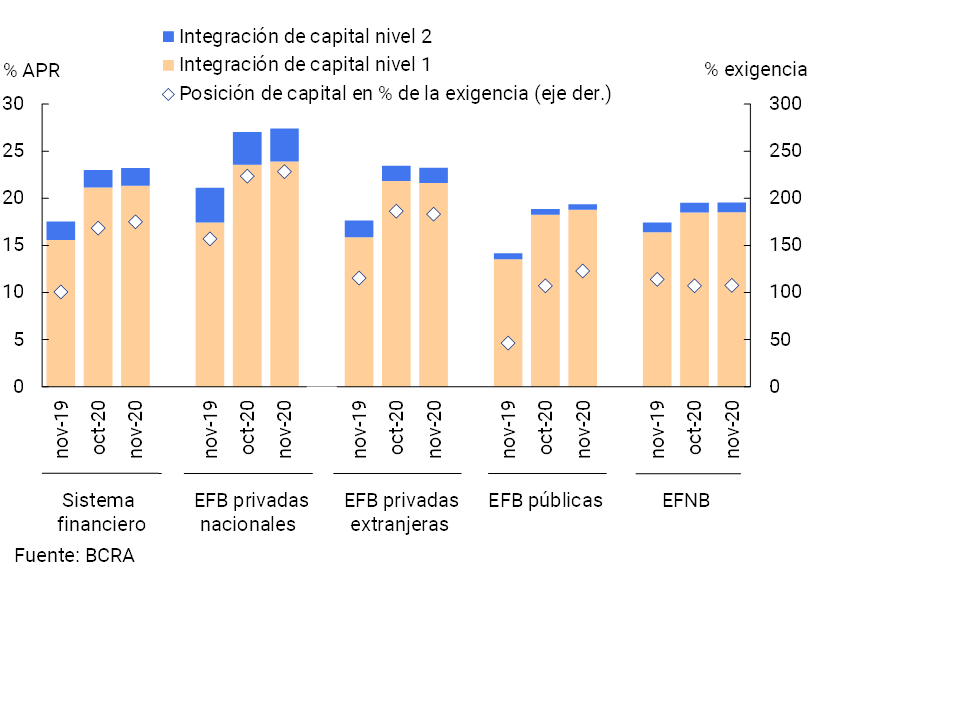

In terms of the sector’s solvency indicators, capital integration (RPC) in relation to risk-weighted assets (RWA) increased in November. This ratio stood at 23.2% at the systemic level in the month, 0.2 p.p. above the October figure (+0.1 p.p. to 25.3% for private banks and +0.5 p.p. to 19.4% for public banks, see Chart 15). The capital position (integration minus capital requirement) of the aggregate of financial institutions stood at 175% of the regulatory requirement in November (206% for private banks and 123% for public banks). It should be recalled that the increase in the solvency indicators of the financial system as a whole is generated within the framework of the macroprudential measures that this Institution adopted in a timely manner, in particular the suspension until the end of the first quarter of 2021 of the possibility of distributing dividends.

Figure 15 | Integration of regulatory capital

By financial institution group

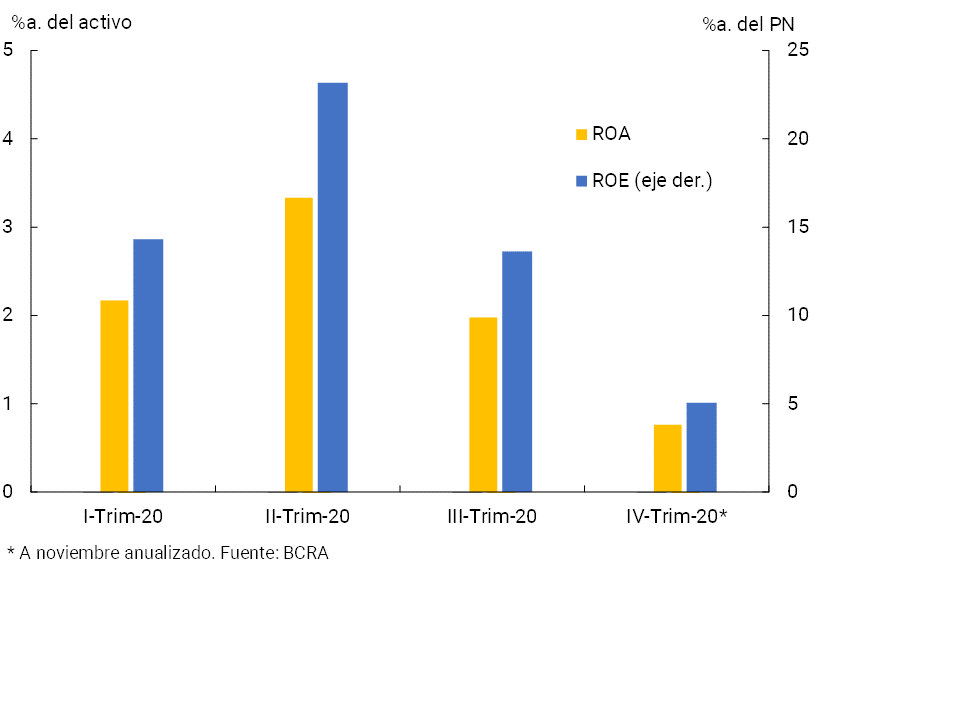

In relation to the profitability indicators in real terms of the sector, a pattern of gradual decline is maintained. In the 11 months of 2020 as a whole, the entities as a whole accrued comprehensive results in homogeneous currency equivalent to 2.2% annualized (y.) of assets (ROA) and 14.7% y. of equity (ROE). Particularly in November, ROA reached 1.8%yA and ROE 11.9%YoY, both records being lower than the annual cumulative. Thus, so far in the fourth quarter of 2020, ROA totaled 0.8%y/y, 1.2 p.p. and 2.6 p.p. below the previous two quarters (see Chart 16).

Figure 16 | Comprehensive total profit in homogeneous currency of the financial system

In the cumulative period between January and November 2020, the financial margin of the aggregate of entities totaled 11% of assets. Interest income was the most relevant source of income (8.5% y/y of assets) in the period, followed by results from securities (8.1% y/y of assets). On the other hand, interest paid was the main disbursement of the financial margin so far this year (8.8% y/y of assets). Among the non-financial items in the profitability table, in 2020, net income from services (1.9% y/y of assets) stood out as a source of results and administrative expenses (6.6% y/y of assets) and charges for uncollectibility (1.5% y/y of assets) as the main expenses.

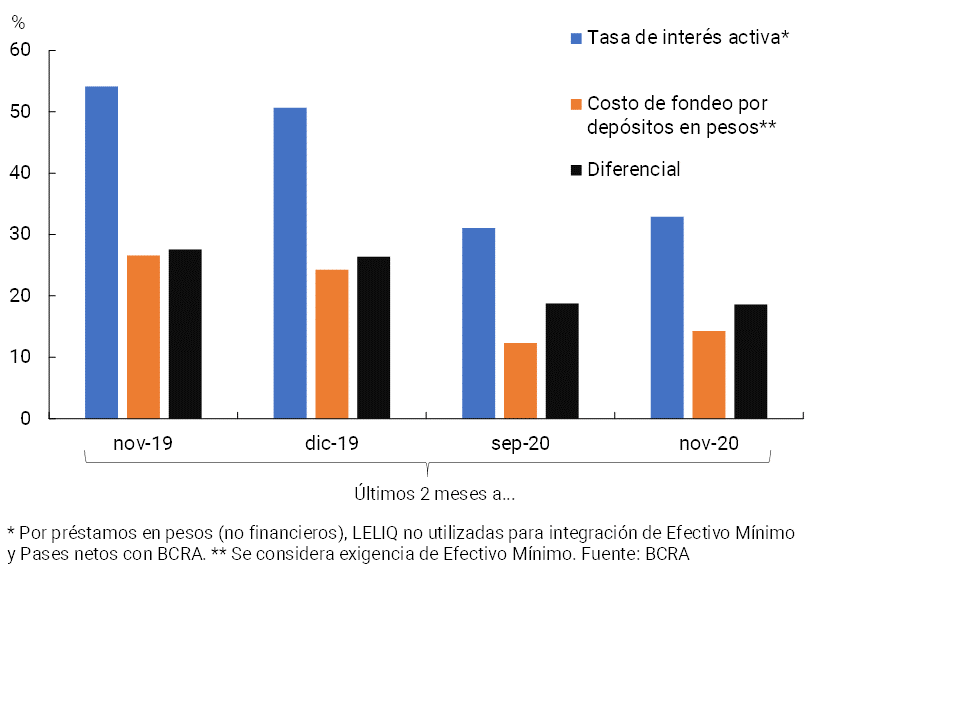

The monitoring of implicit interest rates helps to monitor the main sources of financial income and expenditure in national currency of the group of entities for each peso allocated to financial intermediation19. It is estimated that in the last two months to November, the nominal implicit active interest rate increased slightly lower than that recorded in the implicit funding cost for deposits in national currency in the same period (see Chart 17).20 Therefore, the differential between both estimated concepts decreased slightly in the last two months. It should also be noted that the inflation recorded in the last two months to November was higher than that corresponding to the previous two-month period. Therefore, it is estimated that, when considering the effect of inflation, the differential between implied interest rates would have been reduced even more, in line with the lower levels of financial margin and real profitability that the sector has been verifying.

Figure 17 | Estimated (annualized) implied nominal interest rates for the financial system

V. Payment system

Payment system transactions continued to be carried out within the framework of the health measures adopted to deal with the pandemic, some of which were gradually made more flexible. In this scenario, the BCRA continues to actively promote measures in order to minimize risks and stimulate the use of digital payment channels.

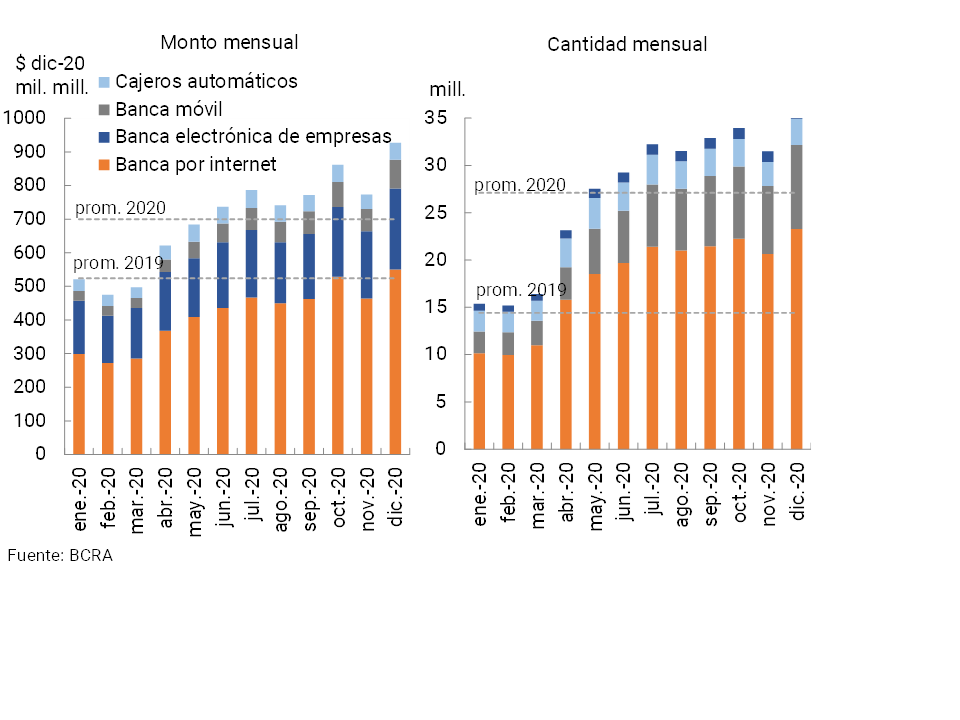

As usual for this time of year, total immediate transfers made during December (latest available information) increased compared to last month, registering monthly growth of 15% in quantities and 15.4% in real amounts (see Graph 18), expanding 103.2% year-on-year in number and 52% in amounts. Thus, immediate transfers made in the last month of the year remained above the annual average: +33.7% in amounts and +24.7% in real terms. Operations carried out through mobile banking and electronic business banking were the channels with the best relative performance in the month.

Figure 18 | Immediate transfers in pesos

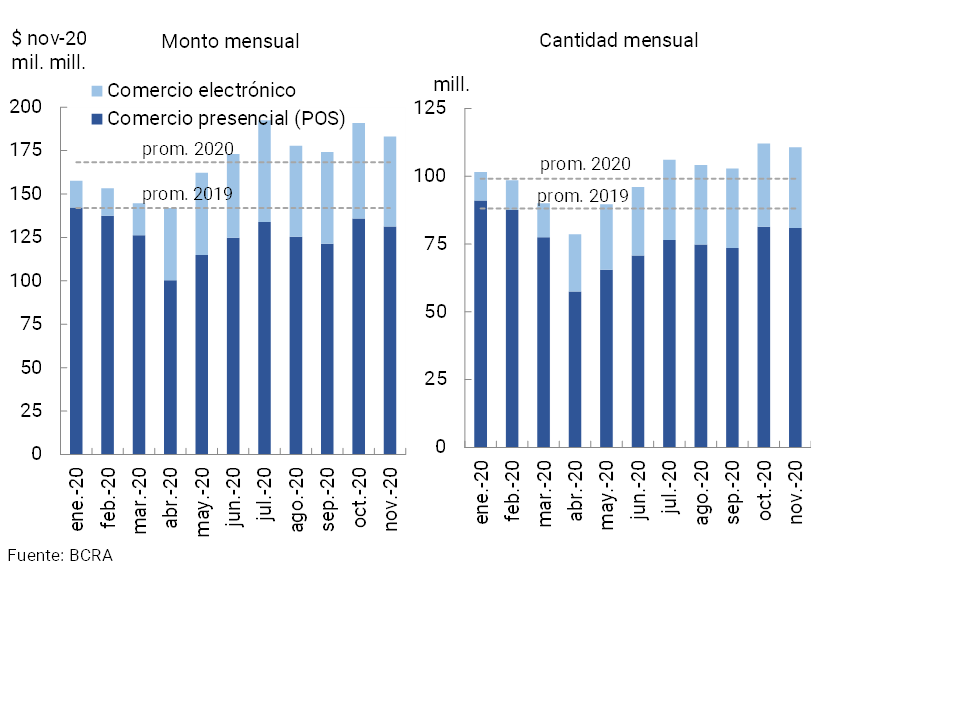

Regarding debit card transactions, in November (latest available information) there was a certain decrease (-1.2% in amounts and -4.1% in real amounts), although they continued to be above the annual average for 2020 (+11.7% and +8.8% in real terms of amounts and amounts respectively, see Chart 19). Compared to the same month of the previous year, debit card operations increased in amounts (18.5%) and in real amounts (29.8%). In the last year, operations in electronic format became especially relevant, increasing 227% in quantities (to represent 27% of the total in November) and 304% in real amounts (reaching 28% of the total in the period).

Figure 19 | Debit card transactions

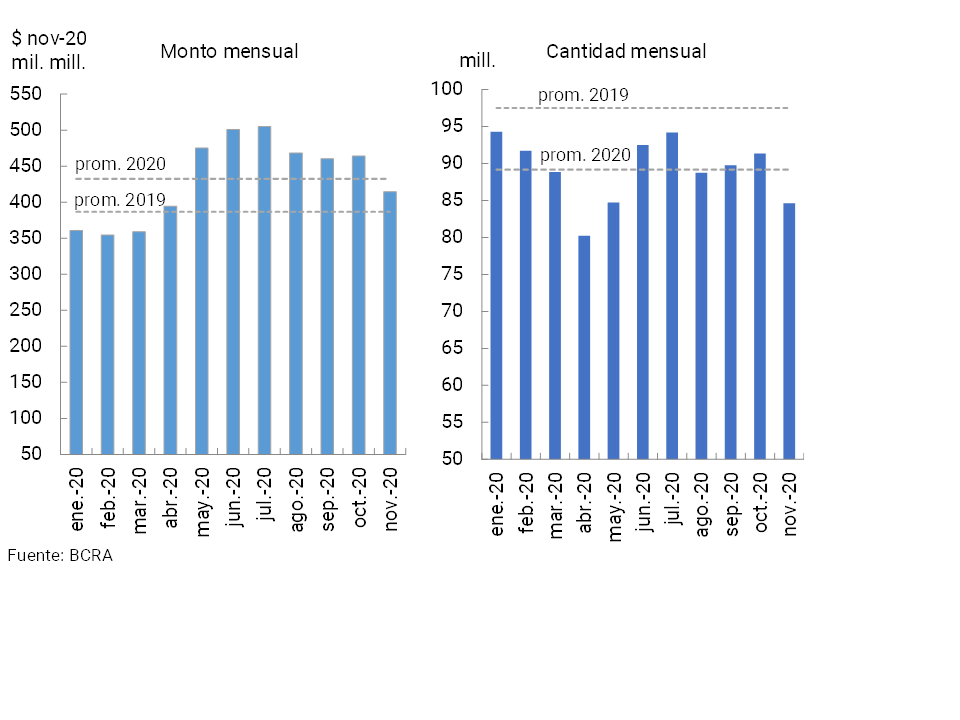

Regarding the use of ATMs, in November the number and amount of withdrawals fell compared to the previous month (-7.3% for the number of operations and -10.6% in real terms for the amounts withdrawn, see Chart 20). Compared to the same month of the previous year, cash withdrawals via ATMs decreased in amounts (-14.6%) and increased in real amounts (13.3%), thus increasing the average amount of each withdrawal measured in constant currency (+$1,206, to almost $4,900 per withdrawal at November 2020 prices).

Figure 20 | Cash withdrawals

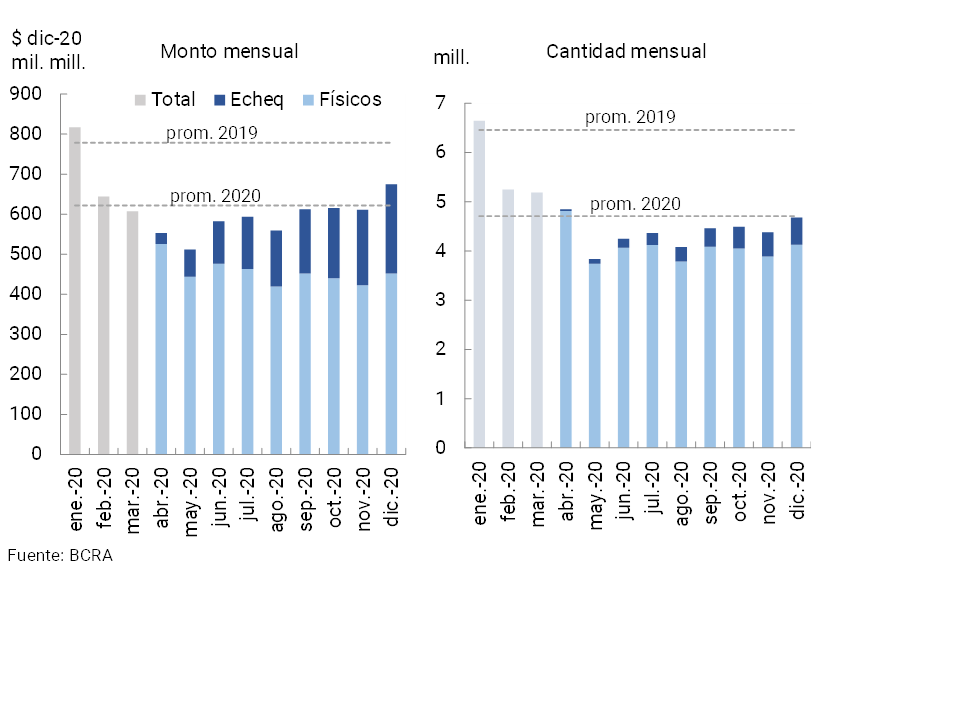

In relation to check operations, during December (latest available information) total compensation increased compared to the previous month: 6.8% in amounts and 10.5% in real terms in amounts (see Graph 21). The number of checks cleared in the month was in line with the annual average, while the amounts were above that average (measured in homogeneous currency). The monthly compensation increased compared to November both in its physical format (6.2% and 6.9% in real amounts and amounts, respectively), and in its electronic version (ECHEQs grew 11.7% in quantities and 18.4% in real amounts). Thus, since April, the relative participation of operations with ECHEQs has increased significantly, to 11.8% in terms of the number of operations and 33.1% in terms of the amounts. On the other hand, compared to the same month of the previous year, the clearing of checks decreased in amounts (-26.6%) and in real amounts (-13.3%).

Figure 21 | Check clearing

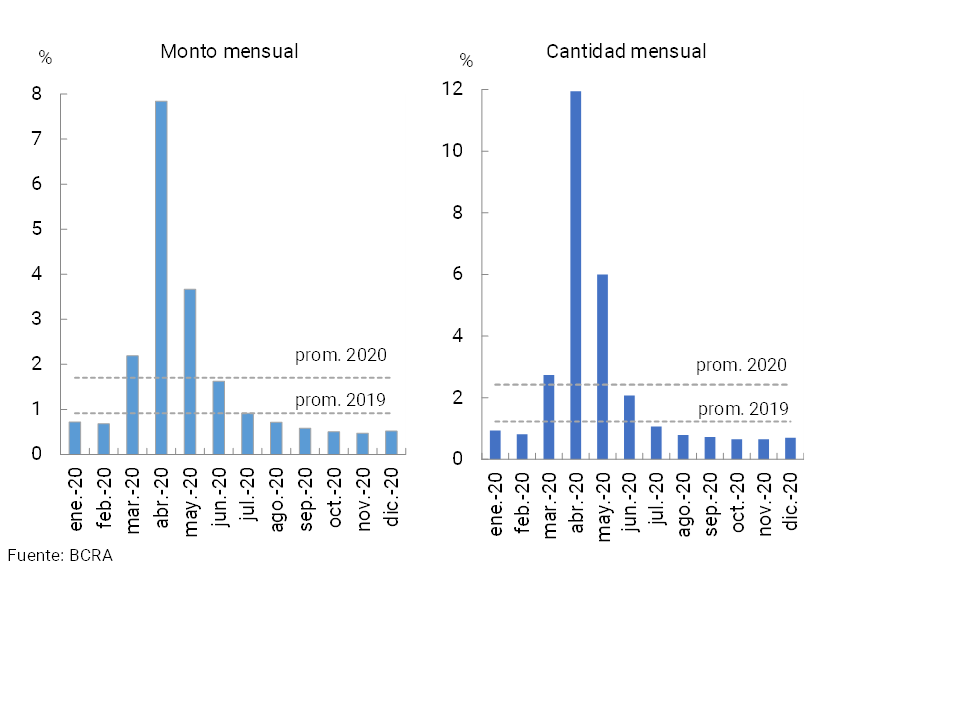

The rejection of checks due to lack of funds in terms of the total compensated increased slightly in December compared to the previous month, totaling 0.7% and 0.52% for amounts and amounts respectively. In this way, the ratio of check rejection due to lack of funds remains below the 2020 average, both in terms of amounts and amounts (see Graph 22). Compared to the same month of the previous year, the rejection ratio decreased in quantities (-0.28 p.p.) and in amounts (-0.27 p.p.), even below the monthly average of 2019.

Figure 22 | Bounce checks due to insufficient funds

Rejects / Total Offset

References

1 Differences in balance sheet balances expressed in homogeneous currency.

2 Considering the segment of items in foreign currency —in the currency of origin—, in November the decrease in financing to the private sector and the public sector were the most prominent sources of funds for the system. Meanwhile, the reduction of foreign loan lines, negotiable and subordinated obligations and the increase in liquidity were the main applications of resources in the period.

3 Includes principal adjustments and accrued interest.

4 Throughout the Report, when reference is made to groups of private (national and/or foreign) and public financial institutions, it corresponds to banking entities. Non-bank entities will be referred to as “EFNBs”.

5 See Communication “A” “7140” and amendments.

6 Within the framework of this new line, recently through Communication “A” “7160”: a) financing alternatives were expanded and b) an additional regulatory benefit was incorporated in terms of Minimum Cash for financing for investment projects (with maximum interest rates of 30% TNA).

7 See “Objectives and plans regarding the development of monetary, financial, credit and exchange policies for the year 2021”.

8 See communication “A” “7082” and communication “A” “7102”.

9 See Communication “A” “6993”.

10 See Communication “A” “7082”.

11 See Communication “A” “7160”.

12 Communication “A” “6938”, Communication “A” “7107”, Communication “A” “7181” and Point 2.1.1. of the Ordered Text “Financial Services in the Framework of the Health Emergency Provided for by Decree No. 260/2020 CORONAVIRUS (COVID-19)”.

13 This monthly behavior was recorded throughout the year and had more to do with a decrease in the denominator than with an increase in the numerator, which was effectively verified towards the end of 2019 in a small group of companies.

14 The LCR considers the liquidity available to deal with a potential outflow of funds in the event of a possible stress scenario in the short term. See Ordered Text —TO— “Liquidity Coverage Ratio”.

15 The NSFR takes into account the availability of stable funding of the entities, in line with the terms of the businesses to which it applies. See TO “Stable Net Funding Ratio”.

16 Considers availability, integration of minimum cash and BCRA instruments, in national and foreign currency.

17 Towards the end of November, the BOTE 2020 – used by institutions for the integration of minimum cash – expired and a tender for BOTE 2022 was held, resulting in a slight increase in these holdings in terms of deposits (+0.2 p.p.).

18 In November, the percentages of financing admitted as minimum cash deductions under the “Subsidized Rate Loans for Companies” program were established based on the interest rate of such financing. In addition, the possibility of imputing as a deduction of the requirement to financing MSMEs intended for the payment of salaries for up to 120% of the Minimum Living and Mobile Wage included in the ATP Program (see Communication “A” “7157”) was annulled. In turn, effective from the beginning of the month, the minimum cash requirement was reduced by an amount equivalent to 14% of the capital investment financing agreed within the framework of the LFIP to an APR of up to 30% (see Communication “A” “7161”).

19 These calculations do not consider concepts such as administrative expenses, tax expenditures, cost of capital or other components associated with risks assumed by the entities.

20 Implied interest rates are estimated by accumulating flows over the last 2 months and annualized, for more detail see previous editions of the Bank Report.

Share on