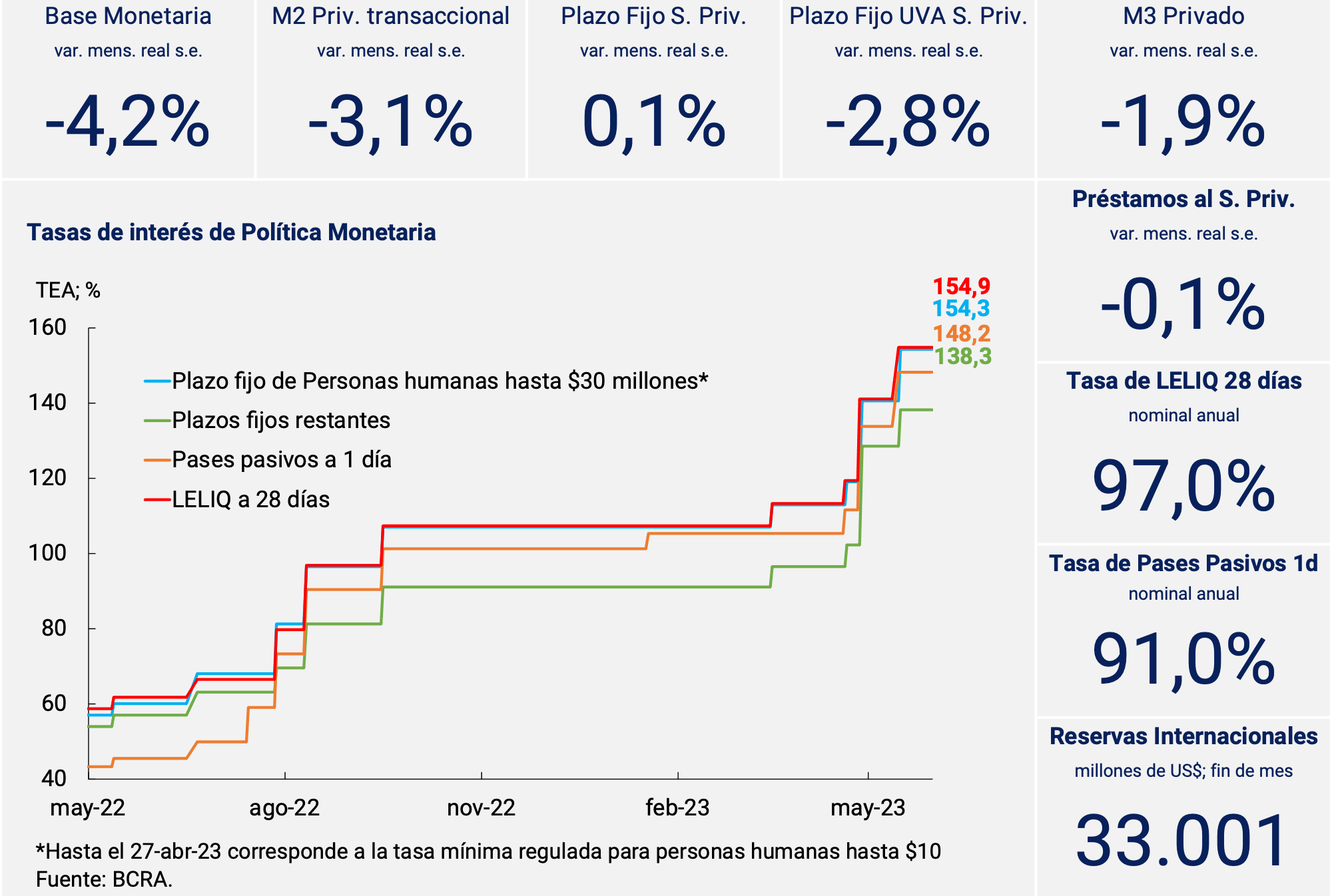

1. Executive Summary

In mid-May, the BCRA raised the monetary policy interest rate (LELIQ 28 days) by 6 percentage points (p.p.), bringing it to 97% n.a. (154.9% y.a.). It also raised interest rates on the rest of the monetary regulation instruments and the minimum regulated interest rates on deposits. Given that the rise occurred in the middle of the month, it has not yet fully impacted the dynamics of deposits. In May, fixed-term placements in pesos by the private sector remained unchanged. In this way, they persist around the maximum values of recent decades, both at constant prices and as a percentage of Output.

On the other hand, transactional means of payment continued to decline and, contrary to what happened with savings instruments in pesos, the transactional private M2 in terms of GDP continued to be at the lowest levels in the last 20 years.

In a context in which time deposits remained unchanged and in which means of payment contracted, the broad monetary aggregate (private M3) at constant prices and without seasonality would have registered a contraction in the fifth month of the year.

Loans for the productive activity of MSMEs, instrumented through documents, were the most dynamic, with the Financing for Productive Investment (LFIP) line being the main tool used to channel this type of credit.

Finally, it should be noted that in May the third edition of the Export Increase Program for the soybean complex ended, although it still continues for regional economies. The program allowed the BCRA, until June 2, to buy foreign currency for a total of US$5,112.5 million, a record that was in line with the forecasts made at the launch of the program that anticipated liquidations of around US$5,000 million.

2. Payment methods

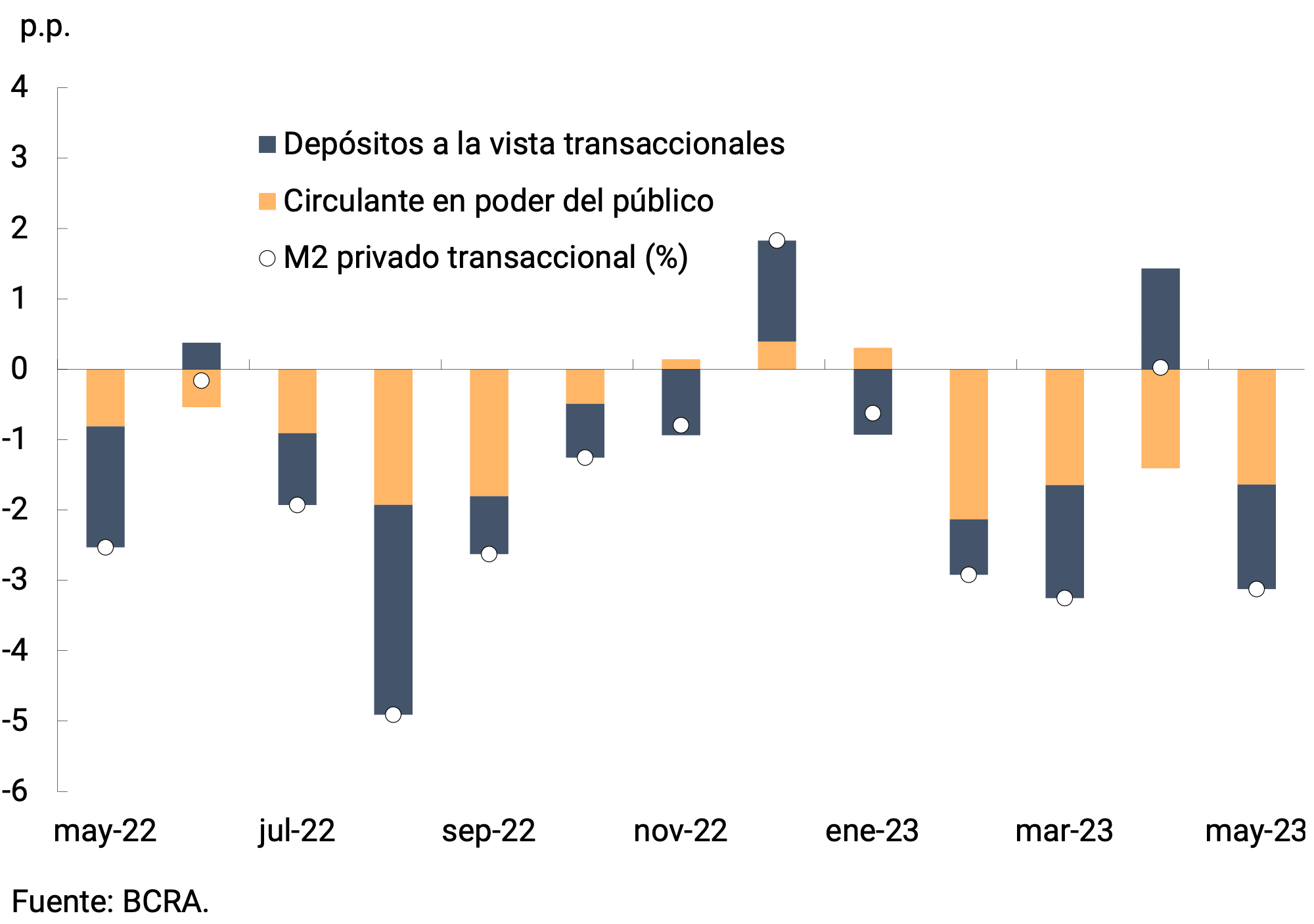

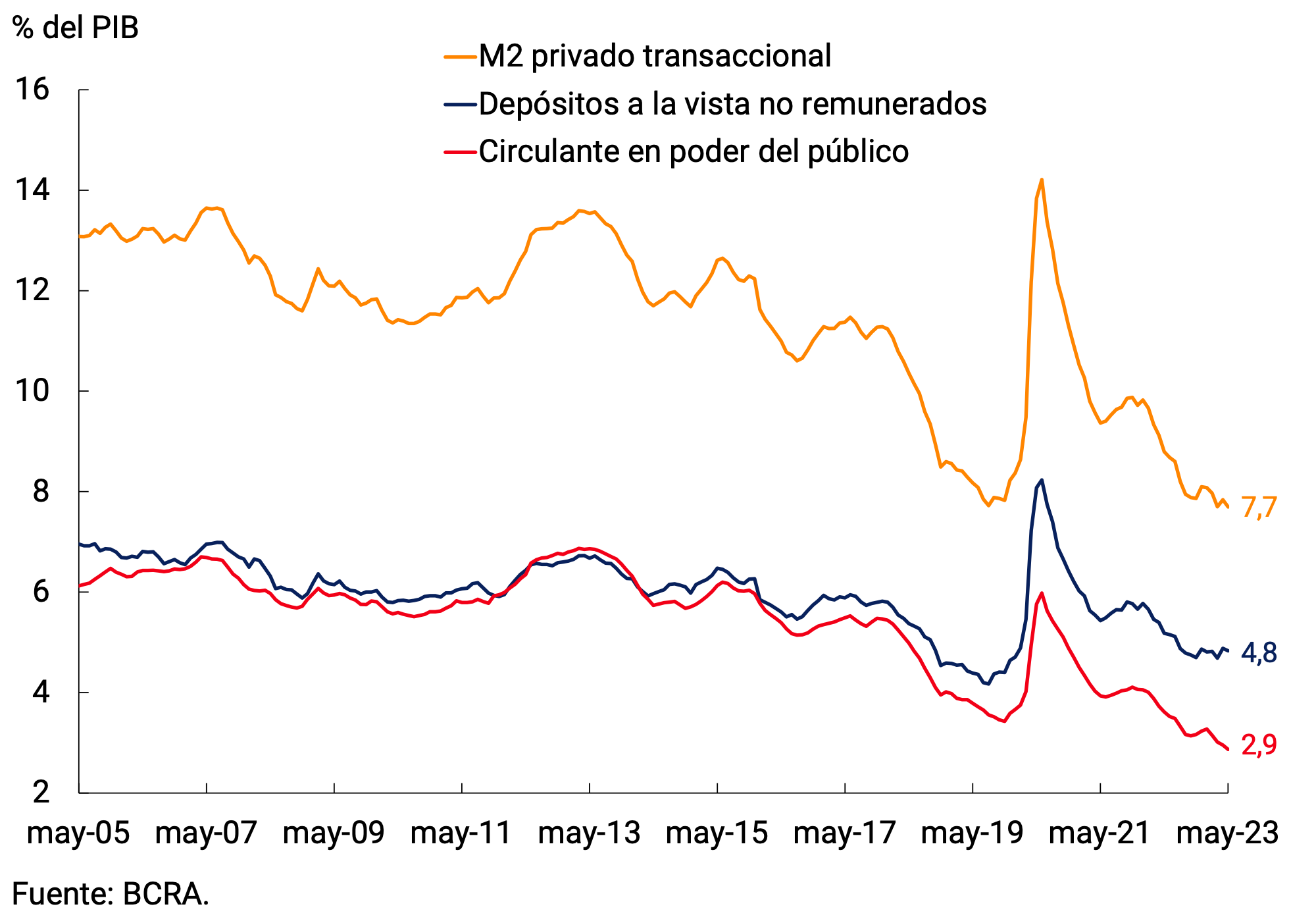

In real and seasonally adjusted terms (s.e.), means of payment (private transactional M21) would have registered a contraction of 3.1% in May. The dynamics of the month responded, in similar proportions, to both the behavior of working capital held by the public and of non-interest-bearing demand deposits (see Figure 2.1). Thus, in year-on-year terms and at constant prices, private transactional M2 would be 18.7% below the level of May 2022. As a proportion of GDP, means of payment would have represented 7.7%, showing a slight decrease (0.1 p.p.) compared to the previous month and around their lowest values of the last 20 years (see Figure 2.2).

Figure 2.1 | Private transactional M2 at constant

prices Contribution by component to the monthly vari. s.e.

Figure 2.2 | Private transactional M2

3. Savings instruments in pesos

The Board of Directors of the BCRA decided to increase the minimum guaranteed interest rates on fixed-term deposits in the fifth month of the year, with the aim of maintaining the incentive to save in domestic currency and contributing to the financial and exchange rate balance2. Specifically, the monetary authority raised the minimum guaranteed interest rate on fixed-term loans for individuals from 91% n.a. to 97% n.a. (154.3% y.a.). Meanwhile, for the rest of the depositors in the financial system, the minimum guaranteed interest rate rose from 85.5% n.a. to 90% n.a. (138.3% n.a.3).

Given that the new rate was only in force for 15 days in May, the effect on the average monthly variation was limited. Thus, the private sector’s fixed-term deposits in pesos would have kept their balance stable at constant prices and, thus, remained close to the highest levels recorded in recent decades. In terms of Output, this type of deposits would have stood at 7.7% in May.

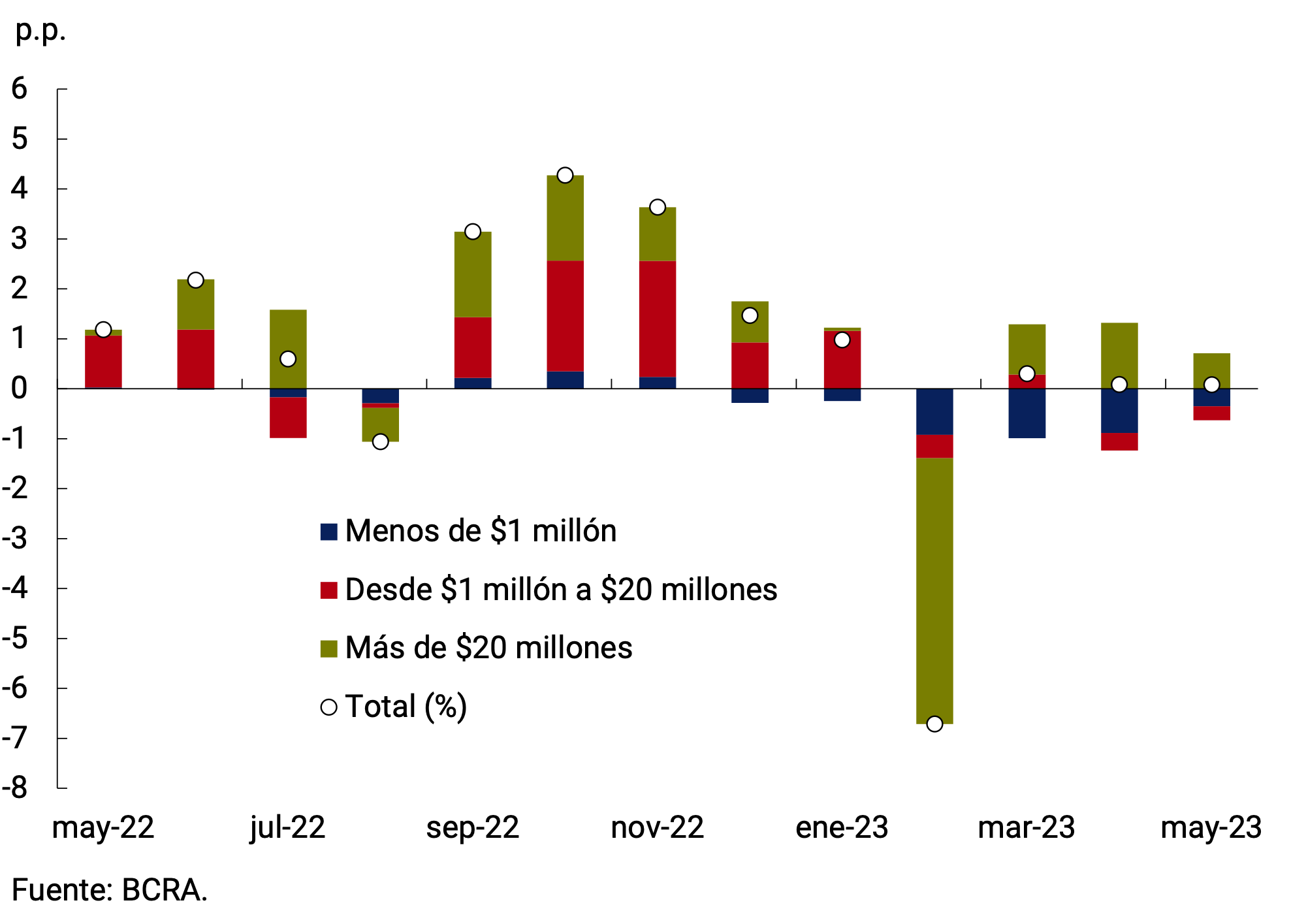

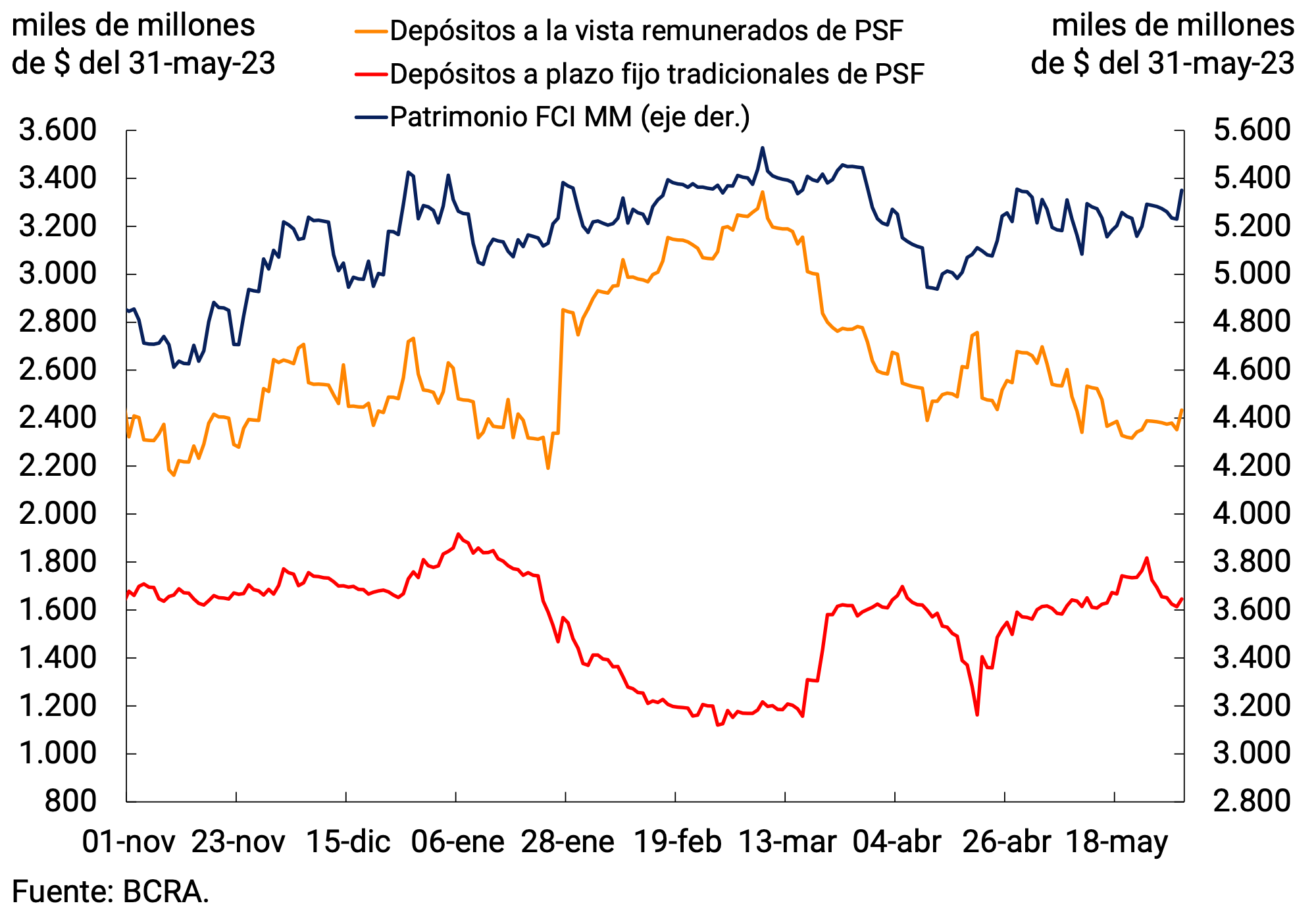

Analyzing term placements by strata of amount, wholesale deposits (more than $20 million) showed an increase on average in the month (see Figure 3.1). The dynamics of the wholesale segment were explained by the higher holdings of Financial Services Providers, whose main players are the Money Market Mutual Funds (MM FCI). These agents rebalanced their portfolio in favor of traditional fixed-term placements and to the detriment of interest-bearing demand deposits. In fact, on average for the month, paid pay registered a contraction of 2.4% at constant prices and without seasonality. This change in the composition of MM’s CRF portfolio occurred in a context of relative stability of its assets measured at constant prices4 (see Figure 3.2). The dynamics of the wholesale segment were offset by the behavior of retail deposits (up to $1 million) and those from $1 to $20 million, which experienced declines in real terms. Finally, Investments with early cancellation option, which cannot be classified by type of holder, showed an increase in the month.

Figure 3.1 | Private Sector Deposits in PesosContribution to Real Monthly Growth by Amount Layer

Figure 3.2 | Deposits of more than $20 million

Balance at constant prices

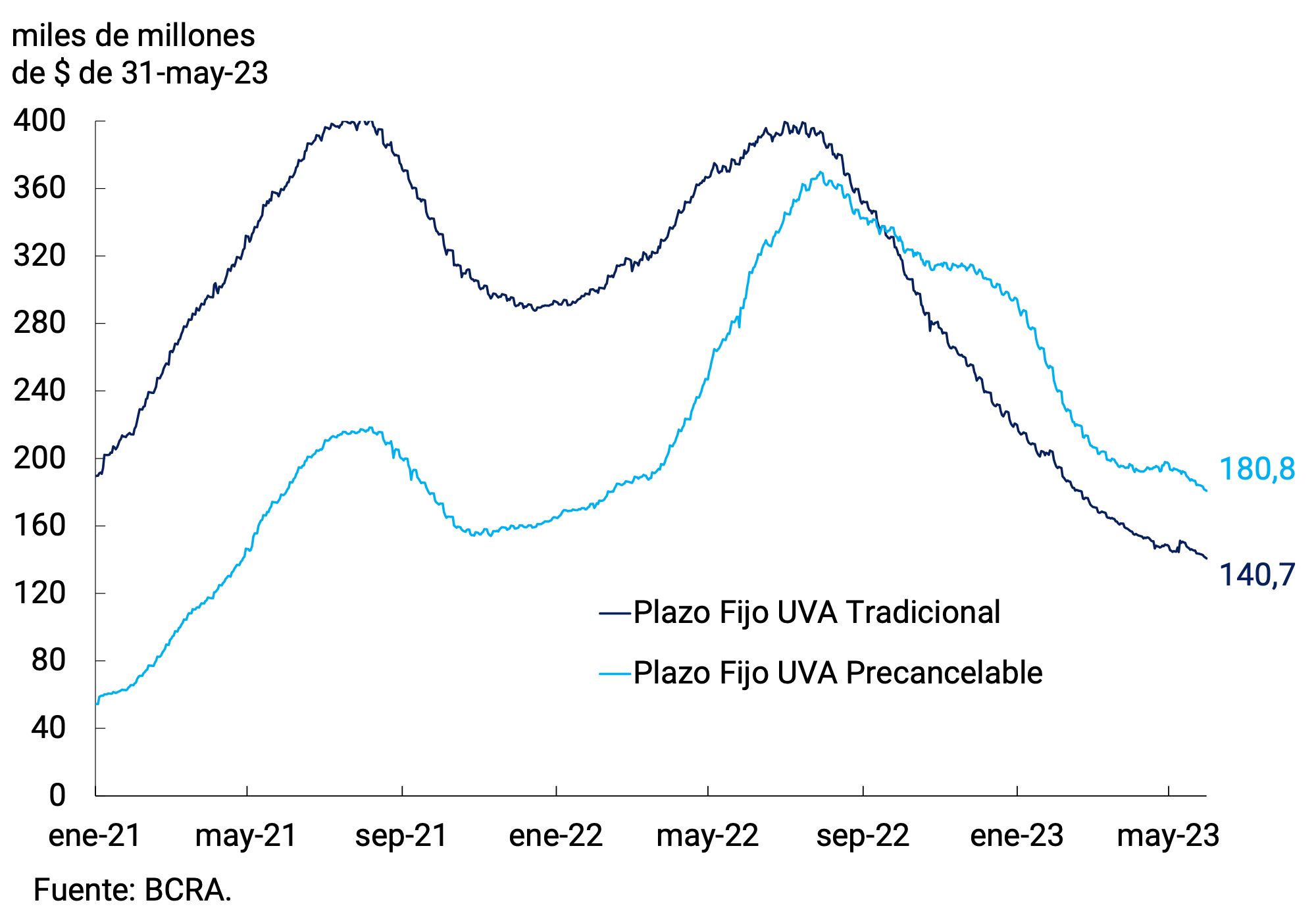

The segment of fixed-term deposits adjustable by CER continued to experience a contraction in real terms, accumulating ten consecutive months of decline. However, they moderated their rate of decline compared to previous months. The decrease was verified in both traditional and pre-cancellable UVA placements, whose monthly rates of change were -3.3% s.e. and -2.3% s.e. respectively (see Figure 3.3). Distinguishing by type of holder, the decrease was mainly due to the dynamics of placements by individuals, which represent approximately 85% of the total. All in all, the balance of deposits in UVA reached $321,500 million at the end of May, which is equivalent to 2.9% of the total of term instruments denominated in domestic currency.

Figure 3.3 | Fixed-term deposits in UVA of the private

sector Balance at constant prices by type of instrument

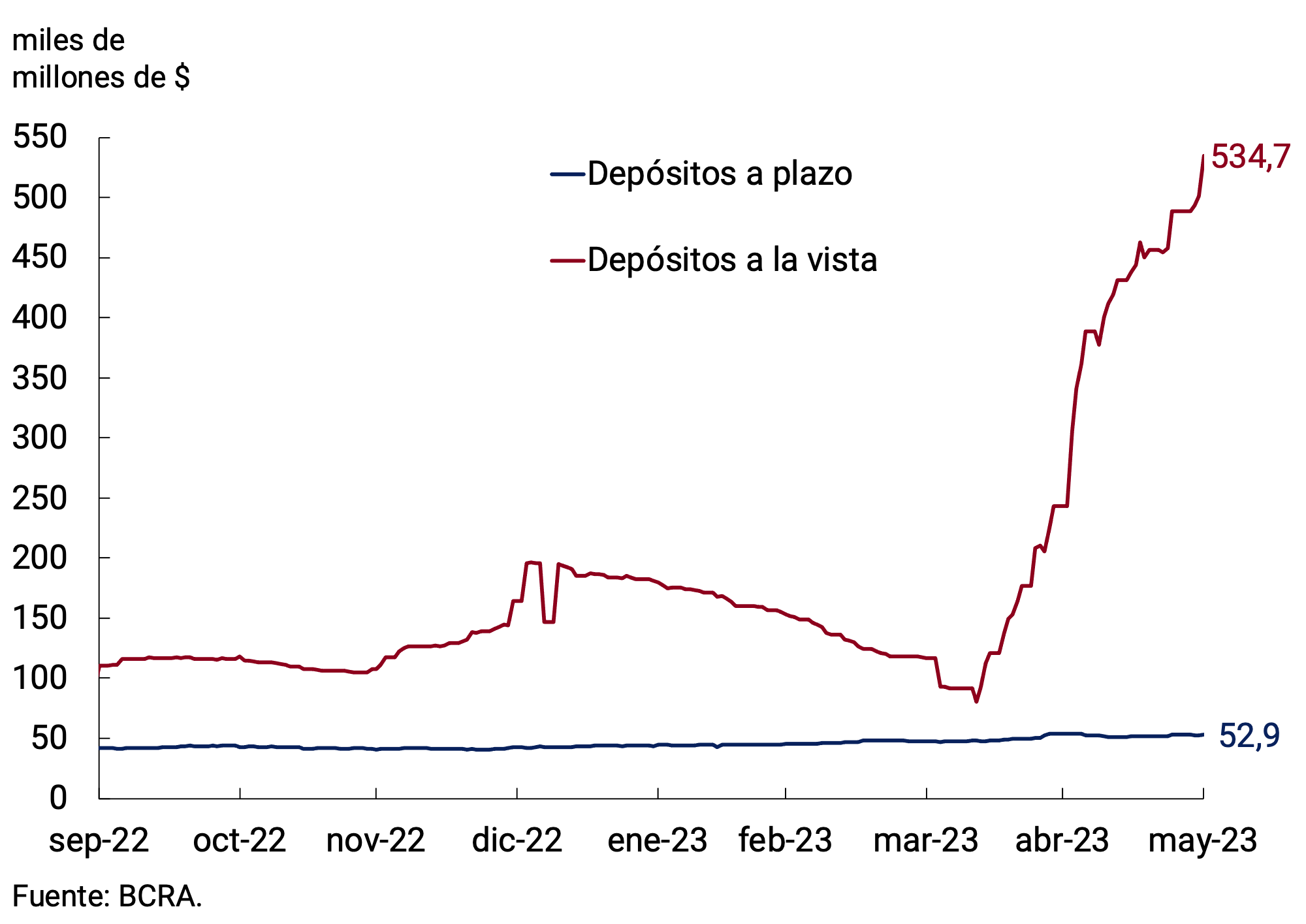

Figure 3.4 | Deposits adjustable by exchange

rate Balance at current prices

On the other hand, deposits adjusted for the value of the reference exchange rate experienced an increase in the fifth month of the year. Currently, there are two types of deposits with exchange rate coverage: a demand account and term investments, the latter called DIVA dollar5. Demand deposits adjusted for exchange rates experienced a variation at the end of the month of 119.6% at current prices, reaching a balance of $534,700 million at the end of May. It should be remembered that the origin of these funds are the operations carried out under the “Export Increase Program” (PIE). Meanwhile, the DIVA dollar reached a balance of $52,900 million at the end of the month, which implied an average monthly expansion of 5.8% at current prices (see Chart 3.4). To cover the exchange rate risk of these deposits, financial institutions have at their disposal the Bills with adjustment according to the value of the dollar (LEDIV).

However, the broad monetary aggregate, private M3, at constant prices and adjusted for seasonality, would have exhibited a monthly fall of 1.9% in May6. In the year-on-year comparison, this aggregate would have experienced a decrease of 4%. As a proportion of GDP, it would have stood at 17.5%, exhibiting a decrease (0.1 p.p.) compared to last month and persisting in line with the average of the 2010-2019 period.

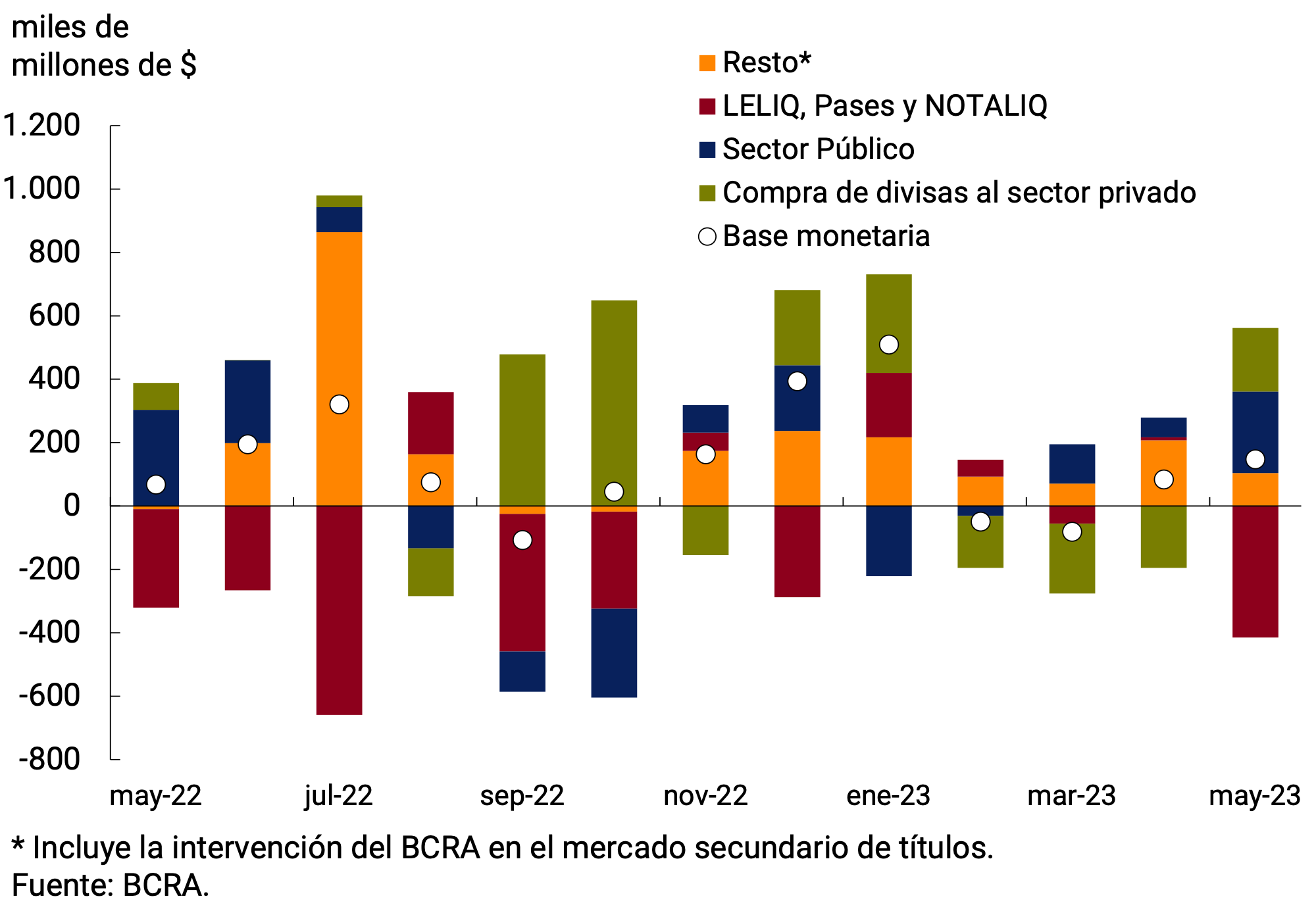

4. Monetary base

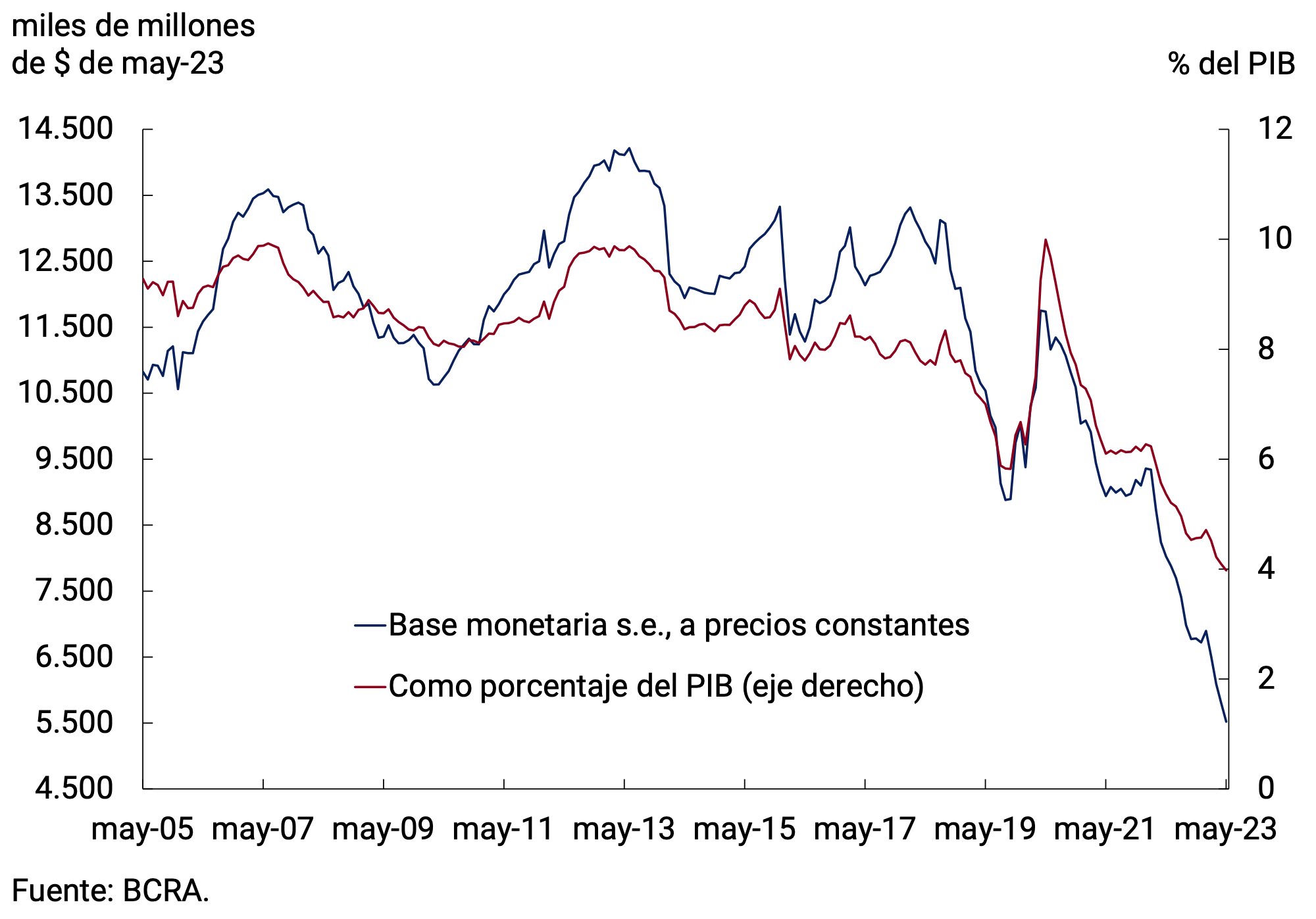

The Monetary Base stood at an average of $5,392.8 billion in May, which implied a monthly expansion of 2.8% (+$147,443 million) at current prices. Adjusted for seasonality and at constant prices, it would have exhibited a decrease of 4.2%, accumulating a drop of 30.7% in the last twelve months. In terms of GDP, the Monetary Base would stand at 4%, 0.1 p.p. below the value recorded the previous month and around the lowest values since the exit from convertibility (see Chart 4.1).

Figure 4.1 | Monetary base

Figure 4.2 | Factors explaining the Monetary Base

Average monthly change

On the supply side, the main factors of expansion of the monetary base were public sector operations and the net purchase of foreign currency from the private sector that prompted the reopening of the “Export Increase Program”. Another factor in the expansion of liquidity was the purchase of public securities in the secondary market, with the aim of limiting excessive financial volatility. These effects, taken together, were partially sterilized through monetary regulation instruments and, to a lesser extent, by the effect of collateral integrations of futures positions (see Figure 4.2).

In mid-May, the BCRA decided to raise the interest rate of the LELIQ by 6 p.p. to 28 days, bringing it to 97.0% n.a. (154.9% y.a.). The interest rate of the LELIQ with a 180-day term was increased by the same magnitude and stood at 105.5% n.a. (133.8% y.a.). As for shorter-term instruments, the interest rate on 1-day pass-by-passes increased from 85% n.a. to 91% n.a. (148.2% y.a.); while the interest rate on 1-day active passes was set at 116% n.a. (218.4% y.a.). Finally, the spread of the NOTALIQ was 8.5 p.p. in the last auction, the same value it has registered since September last year. The monetary authority’s decision was based on the need to tend towards positive real returns on investments in local currency and to prevent financial volatility from impacting inflation expectations. Likewise, this decision is consistent with the level of short-term interest rates on National Treasury debt instruments.

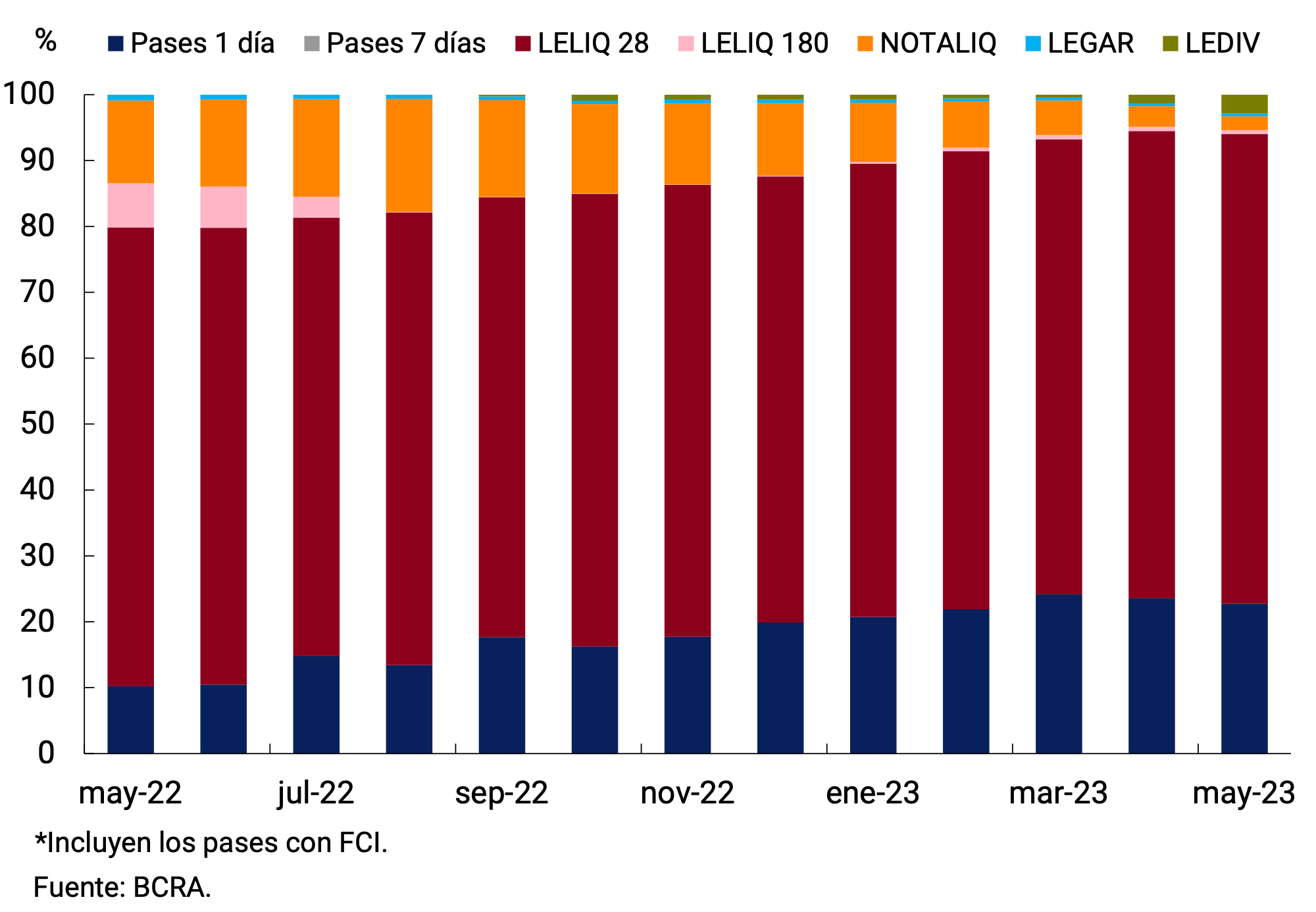

With the current configuration of instruments, in May interest-bearing liabilities were composed, on average, of 71.3% by LELIQ with a 28-day term. Longer-term species, mainly concentrated in NOTALIQ, accounted for 2.7% of the total. On the other hand, 1-day pass-throughs decreased their share of total instruments, representing 22.7% of the total. The rest was made up of LEDIV and LEGAR, increasing their share by 1.5 p.p. compared to the previous month (see Figure 4.3).

Figure 4.3 | Composition of Interest-Bearing Liabilities of the BCRA

Monthly Average

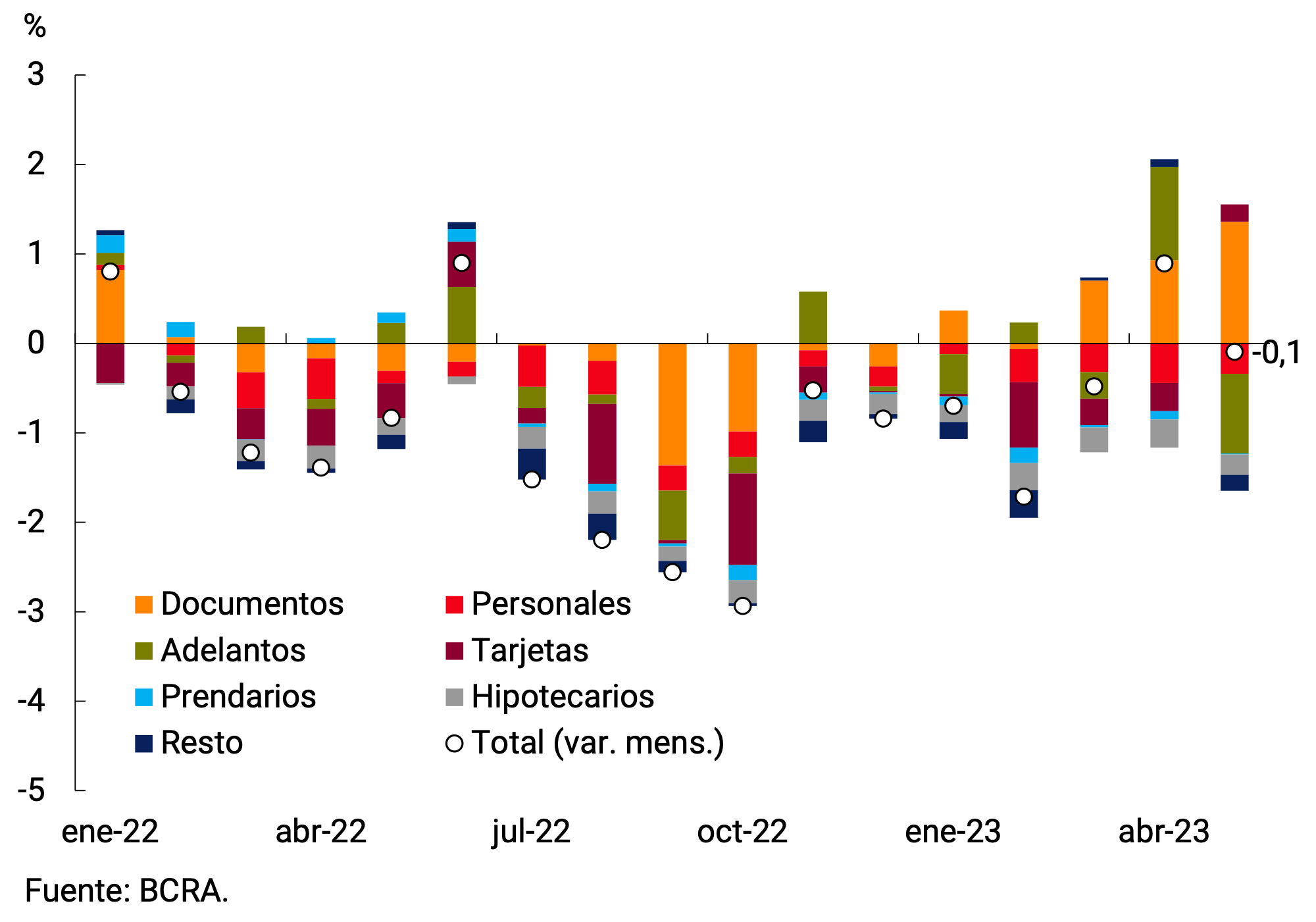

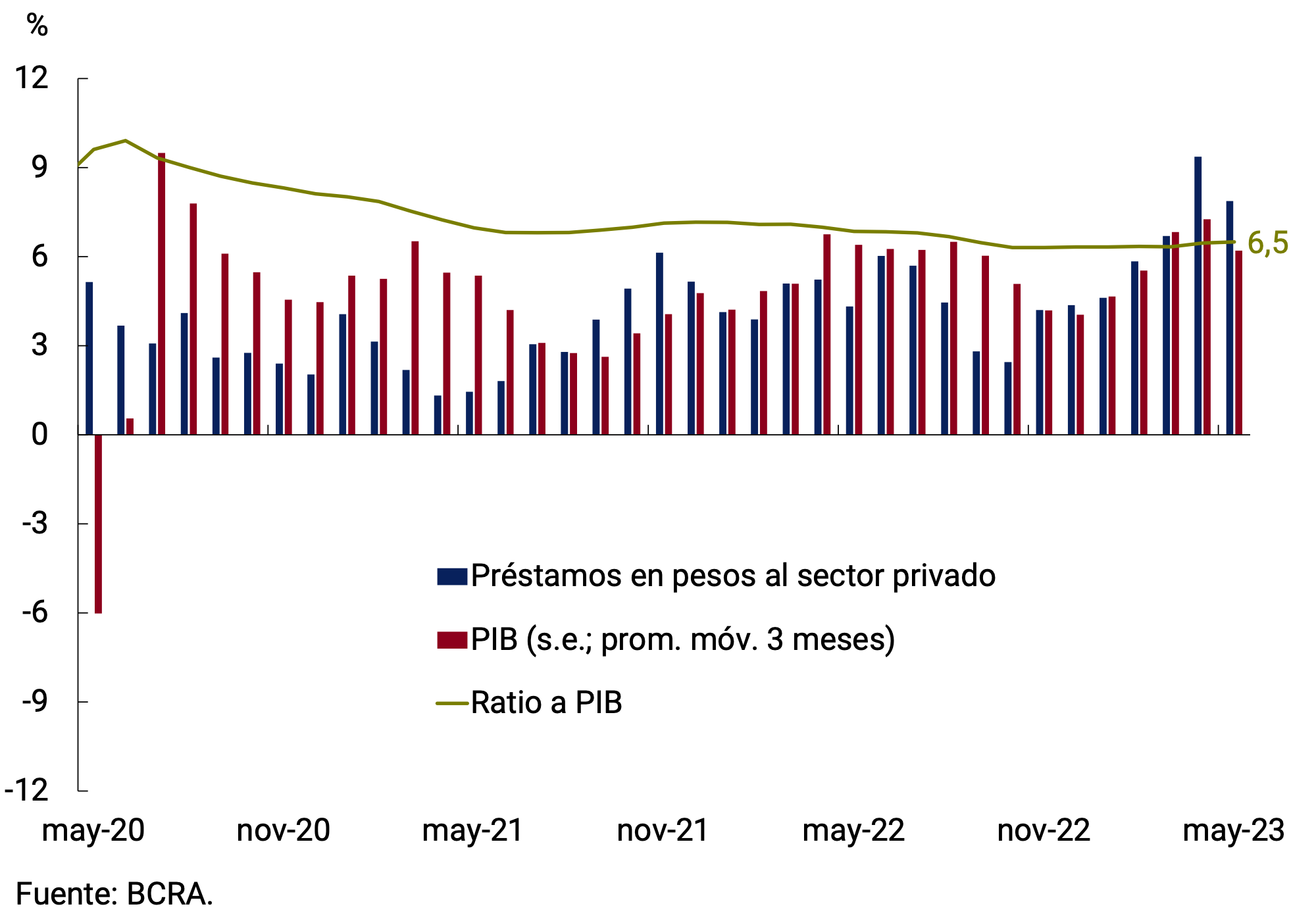

5. Loans to the private sector

In May, loans in pesos to the private sector in real terms and without seasonality would have registered a monthly fall of 0.1% and accumulate in the last 12 months a decrease of 11.2%. The decrease occurred in virtually all funding lines with the exception of documents (see Figure 5.1). As a percentage of current GDP, loans in pesos to the private sector grew slightly in the month and stood at 6.5% (see Figure 5.2).

Figure 5.1 | Loans in pesos to the private

sector Real without seasonality; contribution to monthly growth

Figure 5.2 | Loans in pesos to the private

sector In terms of GDP

By type of financing, lines mainly for commercial purposes grew 0.7% in real terms, with heterogeneous behaviors at the level of loans instrumented through documents and current account advances. In fact, loans granted through documents would have exhibited an increase of 4.9% s.e. in real terms, reaching a balance similar to that of May 2022. The boost came from both discounted documents (6.0% s.e. monthly), and single-signature documents, which also grew in real terms in real terms in the month (4.0% s.e.). On the other hand, advances would have registered a drop at constant prices of 7.2% s.e., the highest in the last two years, standing 2.3% below the level of a year ago.

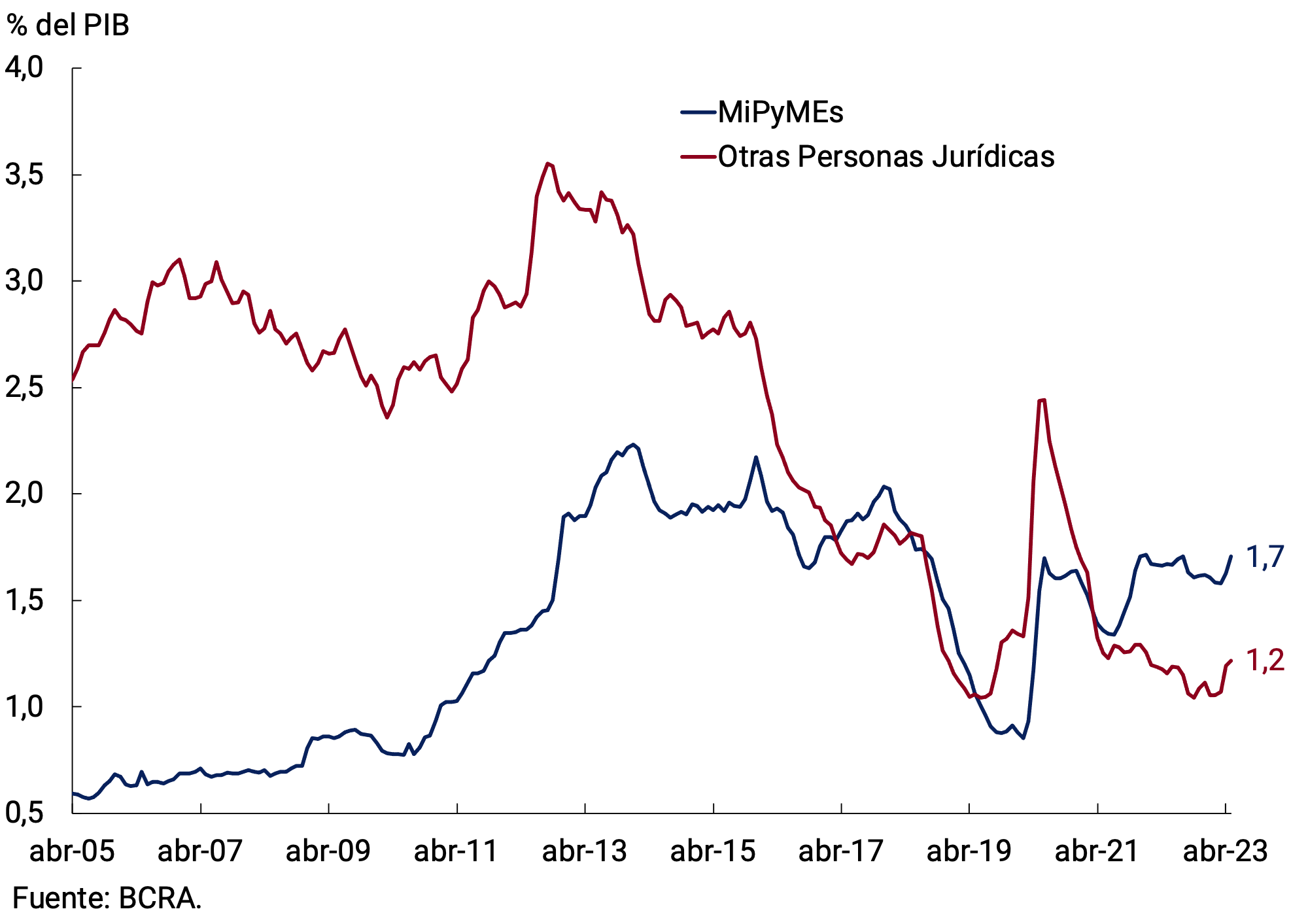

When analyzing the evolution of commercial credit by type of debtor, financing to MSMEs would have grown at constant prices (1.7% s.e.), while credit to large companies would have registered a slight monthly contraction. In terms of GDP, credit to relatively smaller companies was above the pre-pandemic record and above its historical average. On the other hand, in the case of large companies, although it has increased in the last two months, the credit-to-GDP ratio is around the lowest in historical terms (see Figure 5.3).

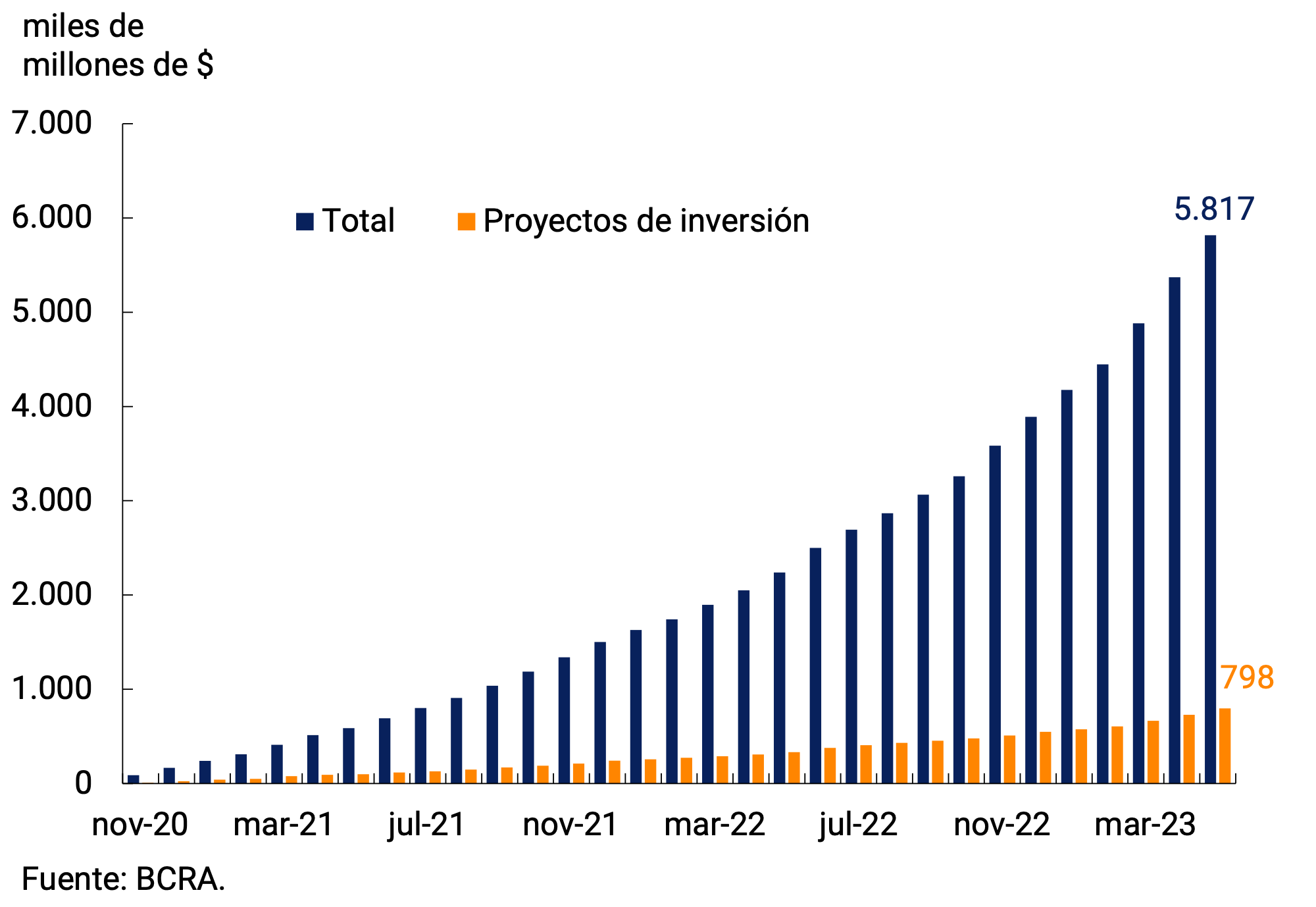

From this it can be deduced that the credit was mainly aimed at the productive activity of Micro, Small and Medium-sized Enterprises (MSMEs), in this sense, the Financing Line for Productive Investment (LFIP) continued to be the main tool used to channel this type of credit. At the end of May, loans granted under the LFIP accumulated approximately $5,817 billion since its launch, an increase of 8.3% compared to last month (see Figure 5.4). Of the total financing granted through the LFIP, 13.7% corresponds to investment projects and the rest to working capital. It should be noted that the average balance of financing granted through the LFIP reached approximately $1,566 billion in April (latest available information), which represents about 18.7% of total loans and 42.7% of total commercial loans.

Figure 5.3 | Commercial Loans by Type of Debtor

As a Percentage of GDP

Figure 5.4 | Financing granted through the Productive Investment Financing Line (LFIP)

Accumulated disbursed amounts; data at the end of the month

Consumer loans would have fallen 0.3% s.e. at constant prices during the month and would accumulate a reduction of 13.9% in the last 12 months. Within these lines, credit card financing would have shown an increase in real terms of 0.7% s.e. in May (-10.0% y.o.y.). For their part, personal loans would have exhibited a fall of 2.2% per month and would be about 20.0% below the level recorded a year ago.

With regard to lines with real collateral, in real terms, collateral loans would have registered a decrease of 0.2% s.e. and are 9.5% below the level of a year ago. For its part, the balance of mortgage loans would have shown a monthly contraction of 4.9% s.e. at constant prices, accumulating a fall of 39.1% in the last twelve months.

6. Liquidity in pesos of financial institutions

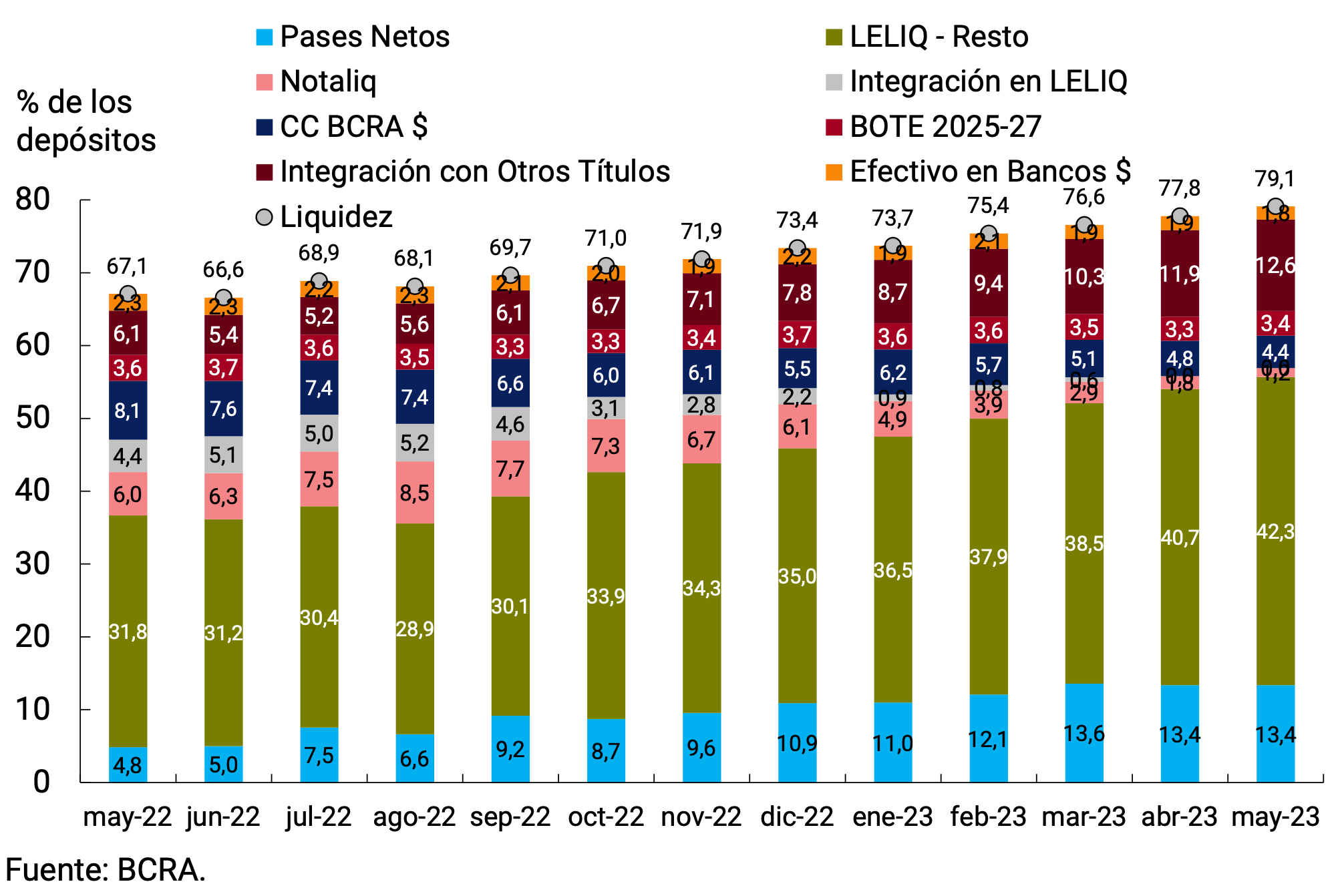

In May, ample bank liquidity in local currency7 showed a further increase of 1.3 p.p. compared to April, averaging 79.1% of deposits (see Figure 6.1). In this way, it remained at historically high levels. The increase was mainly explained by the LELIQ and the integration with public securities, partially offset by the NOTALIQ and the current accounts at the Central Bank.

With respect to regulatory changes with a potential impact on bank liquidity, firstly, it is worth mentioning that as of May 15, the minimum cash requirement that can be integrated with BOTE 2027 (maturing on 05/23/2027 and 11/23/2027) may also be integrated with the new National Treasury Bond in pesos maturing on August 23, 20258. This bond was issued at the end of May, so the full impact on integration will be observed as of June.

Second, with regard to the public securities admitted for minimum cash integration, the maximum residual term was extended to 760 days for all admitted species9. Thirdly, it was provided that financial institutions may compute as a deduction of the minimum cash requirement the financing to MSMEs instrumented through the purchase of Electronic Credit Invoices for MSMEs (FCEM) accepted by companies that meet certain conditions contemplated in regulation10.

Figure 6.1 | Liquidity in pesos of financial institutions

7. Foreign currency

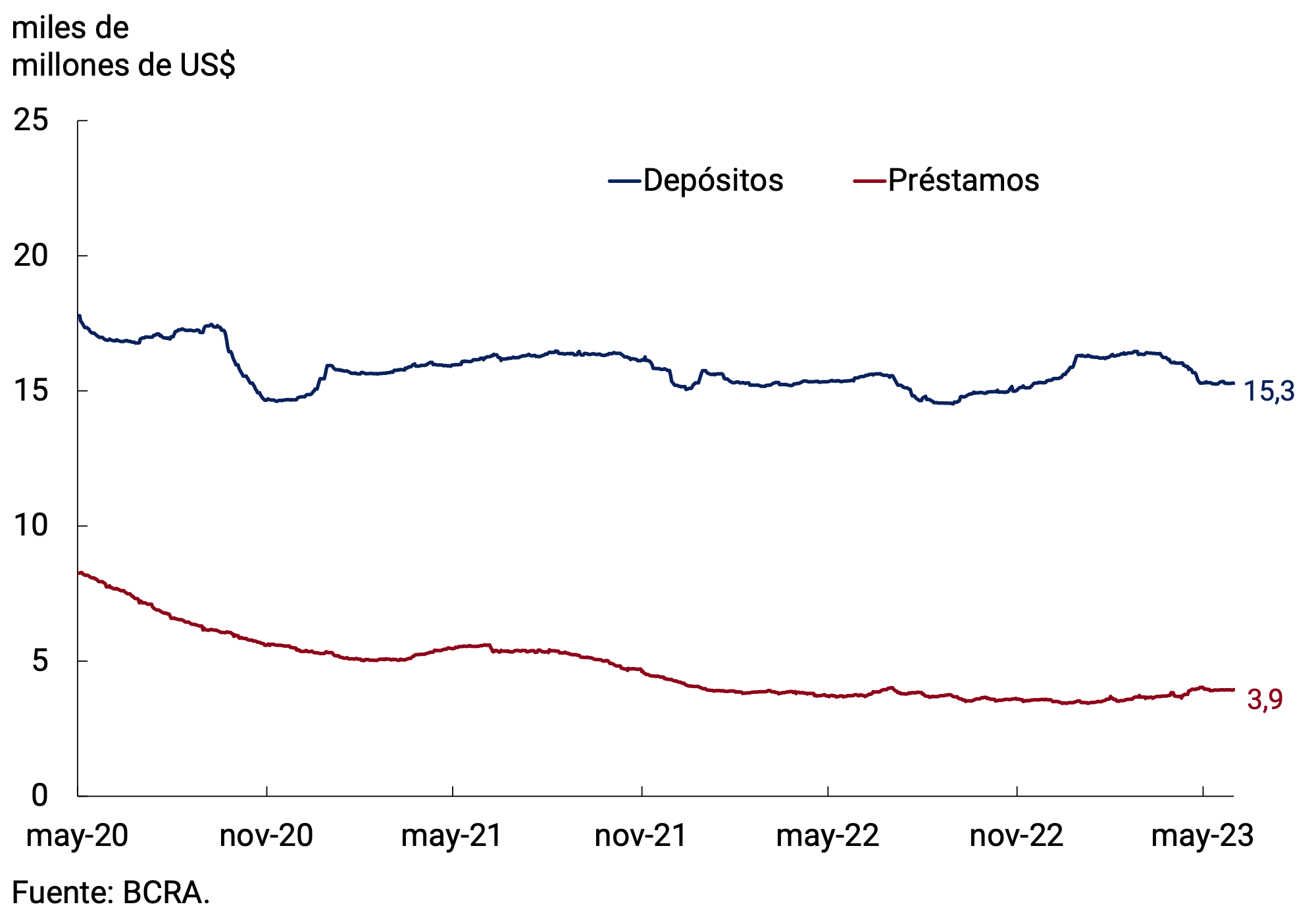

In the foreign currency segment, the main assets and liabilities of financial institutions had limited variations. On the one hand, at the end of the month, the balance of private sector deposits was US$15,282 million, so it registered practically no changes compared to the end of April. Inside, however, there are increases in deposits of legal entities and falls in those of individuals. On the other hand, the balance of loans to the private sector fell by US$80 million and ended the month at US$3,946 million (see Figure 7.1).

Figure 7.1 | Balance of private sector foreign currency deposits and loans

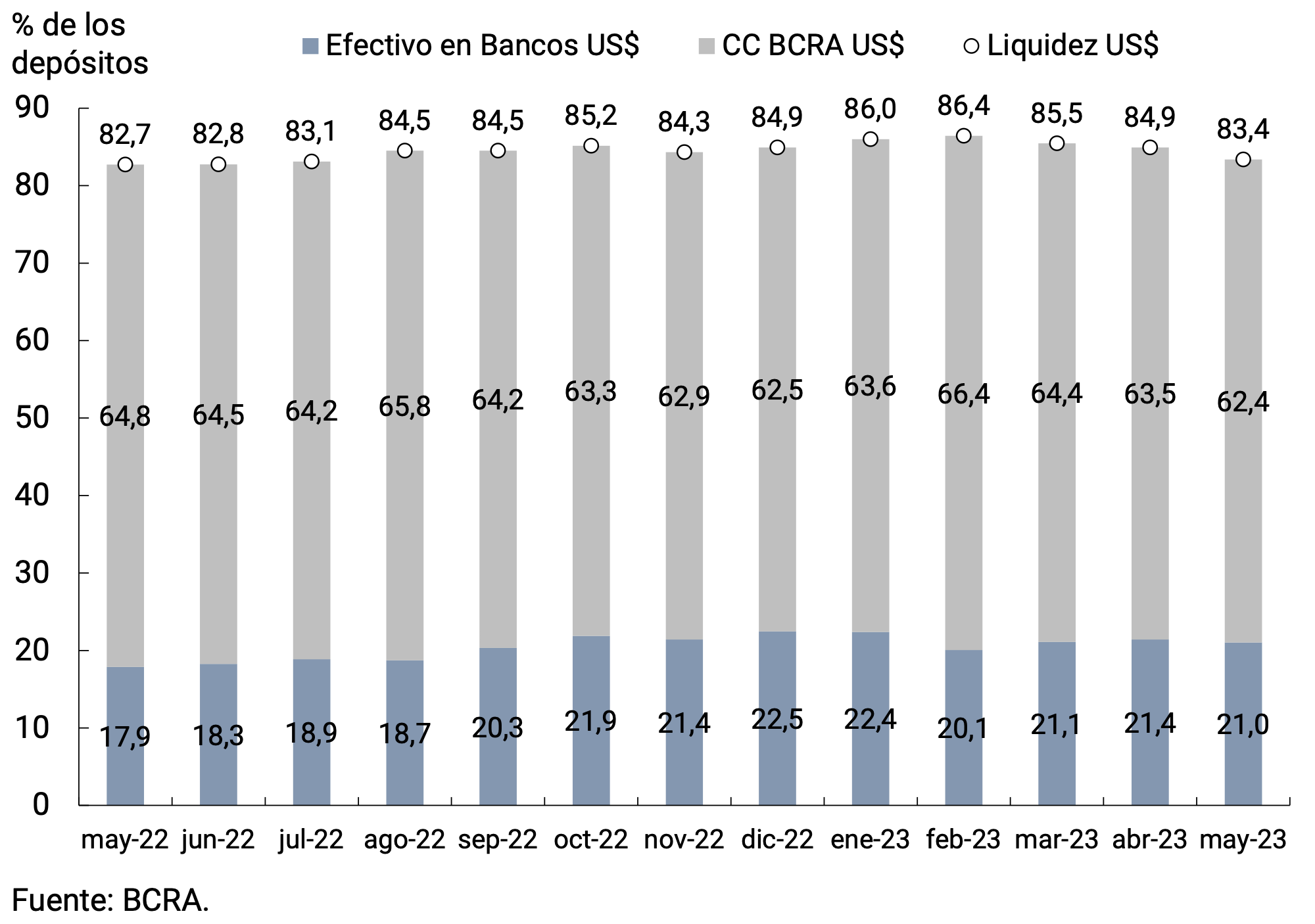

Figure 7.2 | Liquidity in foreign currency of financial institutions

The liquidity of financial institutions in the foreign currency segment experienced a fall of 1.5 p.p. compared to the April average, standing at 83.4% of deposits. In any case, it remains at historically high levels. The movement was explained by current accounts at the BCRA, partially offset by an increase in cash in banks (see Figure 7.2).

During May, a series of regulatory modifications were made in foreign exchange matters, aimed at favoring an efficient allocation of International Reserves. First, it was established that the consumption of foreign tourists made through electronic wallets that involve a debit in their bank or virtual accounts as well They may be settled at an exchange rate that has financial dollars as a reference11. In turn, the same regulation provided that when the currency indicated in the SIRA or SIRASE declaration is the currency of a country with which the BCRA has a Bilateral Currency Pass Agreement in force, The payment must be made in the same currency as that shown in the corresponding declaration. On the other hand, It was decided to apply the export pre-financing system to the payment of imports12. This system allows companies that act as both importers and exporters to finance the purchase of inputs with their own suppliers or with international lines of credit, from foreign or local banks. Finally, new conditions were established to grant access to the foreign exchange market for the payment of imports13, to carry out operations with securities14 and payments abroad with credit cards15.

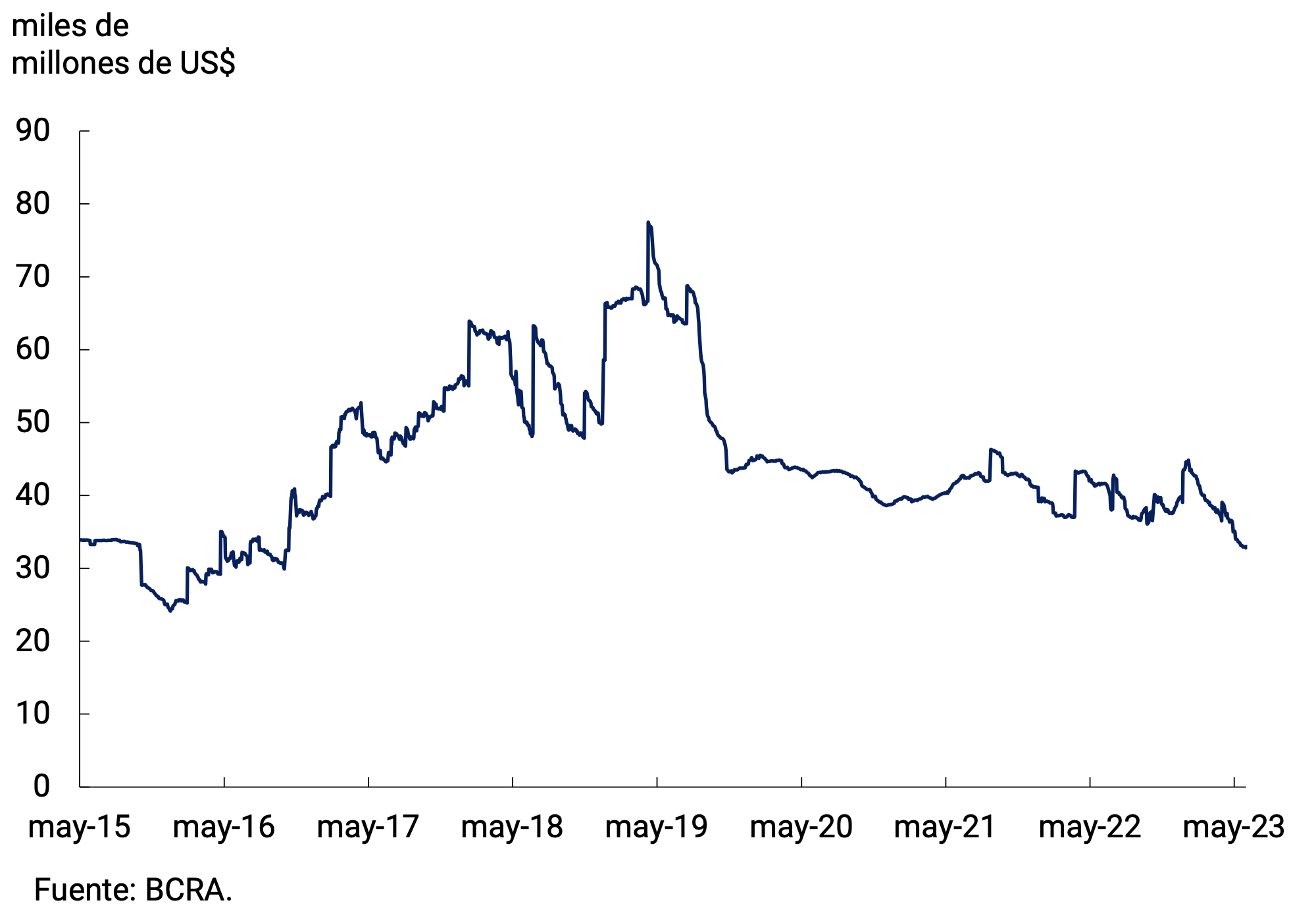

The BCRA’s International Reserves ended May with a balance of US$33,001 million, registering a decrease of US$2,000 million compared to the end of April. This drop was mainly explained by payments to international organizations, including payments to the International Monetary Fund for US$800 million and by losses on the valuation of net foreign assets. On the other hand, foreign currency purchases under the Export Increase Program totaled US$3,205 million in the month, although they were partially offset by net sales made outside the program (see Figure 7.3). It should be noted that, until June 2, for the third edition of the Export Increase Program, the BCRA bought foreign currency for US$5,112.5 million.

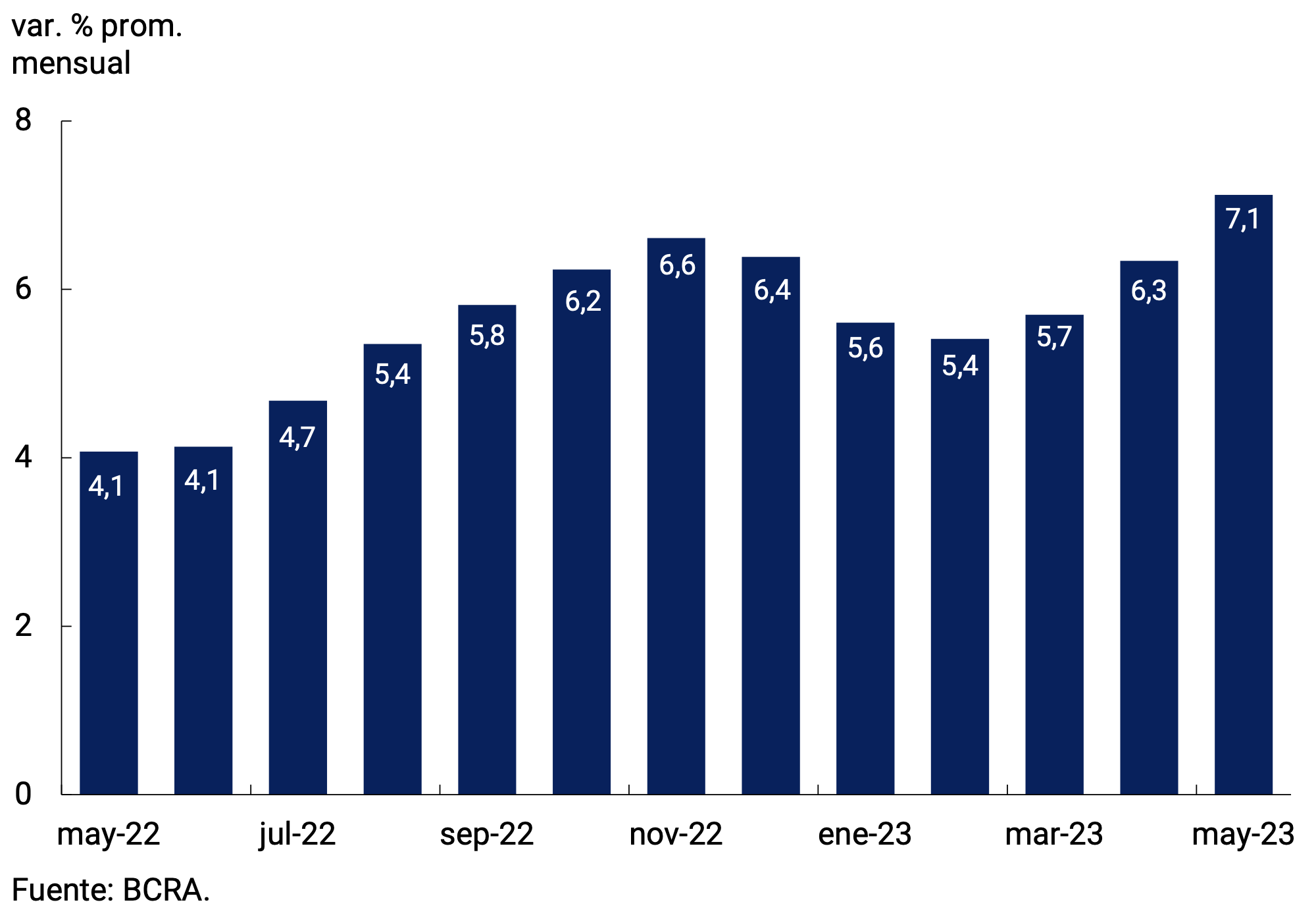

Finally, the bilateral nominal exchange rate (TCN) against the U.S. dollar increased by 7.1% in May, a higher increase than in the previous month (see Figure 7.4). Thus, it stood at an average of $231.14/US$.

Figure 7.3 | International Reserve Balance

Figure 7.4 | Variation in the bilateral nominal exchange rate with the United States

Glossary

ANSES: National Social Security Administration.

AFIP: Federal Administration of Public Revenues.

BADLAR: Interest rate on fixed-term deposits for amounts greater than one million pesos and a term of 30 to 35 days.

BCRA: Central Bank of the Argentine Republic.

BM: Monetary Base, includes monetary circulation plus deposits in pesos in current account at the BCRA.

CC BCRA: Current account deposits at the BCRA.

CER: Reference Stabilization Coefficient.

NVC: National Securities Commission.

SDR: Special Drawing Rights.

EFNB: Non-Banking Financial Institutions.

EM: Minimum Cash.

FCI: Common Investment Fund.

A.I.: Year-on-year .

IAMC: Argentine Institute of Capital Markets

CPI: Consumer Price Index.

ITCNM: Multilateral Nominal Exchange Rate Index

ITCRM: Multilateral Real Exchange Rate Index

LEBAC: Central Bank bills.

LELIQ: Liquidity Bills of the BCRA.

LFIP: Financing Line for Productive Investment.

M2 Total: Means of payment, which includes working capital held by the public, cancelling cheques in pesos and demand deposits in pesos from the public and non-financial private sector.

Private M2: Means of payment, includes working capital held by the public, cancelling cheques in pesos and demand deposits in pesos from the non-financial private sector.

Private transactional M2: Means of payment, includes working capital held by the public, cancelling cheques in pesos and non-remunerated demand deposits in pesos from the non-financial private sector.

M3 Total: Broad aggregate in pesos, includes the current currency held by the public, cancelling checks in pesos and the total deposits in pesos of the public and non-financial private sector.

Private M3: Broad aggregate in pesos, includes the working capital held by the public, cancelling checks in pesos and the total deposits in pesos of the non-financial private sector.

MERVAL: Buenos Aires Stock Market.

MM: Money Market.

N.A.: Annual nominal.

E.A.: Effective Annual.

NOCOM: Cash Clearing Notes.

ON: Negotiable Obligation.

GDP: Gross Domestic Product.

P.B.: basis points.

PSP.: Payment Service Provider.

p.p.: percentage points.

MSMEs: Micro, Small and Medium Enterprises.

ROFEX: Rosario Term Market.

S.E.: No seasonality

SISCEN: Centralized System of Information Requirements of the BCRA.

SIMPES: Comprehensive System for Monitoring Payments of Services Abroad.

TCN: Nominal Exchange Rate

IRR: Internal Rate of Return.

TM20: Interest rate on fixed-term deposits for amounts greater than 20 million pesos and a term of 30 to 35 days.

TNA: Annual Nominal Rate.

UVA: Unit of Purchasing Value

References

1 Corresponds to private M2 excluding interest-bearing demand deposits from companies and financial service providers. This component was excluded since it is more similar to a savings instrument than to a means of payment.

2 The interest rates currently in force are those established by communication “A” 7726.

3 The rest of the depositors are made up of Legal Entities and Individuals with deposits of more than $10 million.

4 Although on average the assets of the FCI MM grew by 2.2% s.e. in real terms, this increase was mainly due to the carry-over effect of the previous month.

5 This type of accounts is not available to all agents. Demand accounts adjusted for the exchange rate can only be subscribed by 1) holders with agricultural activity (who participated in the Export Increase Program -PIE- and exporters from regional economies) and 2) special accounts for exporters. The latter includes exporters of goods under certain requirements and entities that receive financial assistance and/or non-refundable contributions from international organizations. On the other hand, time deposits with adjustment for exchange rates are only for agents with agricultural activity.

6 The private M3 includes the working capital held by the public and the deposits in pesos of the non-financial private sector (demand, time and others).

7 Includes current accounts at the BCRA, cash in banks, balances of net passes arranged with the BCRA, holdings of LELIQ and NOTALIQ, and public bonds eligible for reserve requirements.

8 Communication “A” 7767

9 Communication “A” 7775

10 Communication “A” 7758

11 Communication “A” 7762.

12 Communication “A” 7770.

13 Communications “A” 7763, “A” 7766 and “A” 7771.

14 Communication “A” 7772.

15 Communication “A” 7766.

Share on