Executive summary

• The intermediation activity of the financial system with the private sector in foreign currency continued to grow in April, while the slowdown in the monthly rate of reduction of the segment in pesos was accentuated. In an operational context where the size of the balance sheet of the financial system did not present any major changes, in April the group of entities continued to present comfortable levels of liquidity and solvency.

• The balance of bank credit to the private sector in foreign currency grew 17.3% in the month (in currency of origin), accumulating a year-on-year expansion (YoY) of 40.1%. For its part, the balance of financing to the private sector in pesos fell 1% in real terms in April, being the smallest decrease in the last 6 months. Among credit assistance in pesos, in April consumer lines increased in real terms (4.3% personal and 1.8% cards), as well as advances (1.7%), while the rest continued to decrease. In year-on-year terms, the balance of credit to the private sector in pesos fell 33.6%.

• In April, the quality of the total portfolio of loans to the private sector of the aggregate financial system remained without significant changes. The non-performing loan ratio for loans to the private sector remained at 1.8% (-1.2 p.p. y.o.y.). The NPL ratio for the loan portfolio for households stood at 2.6% (-0.7 p.p. y.o.y.) and 1.3% for the corporate financing segment (-1.7 p.p. y.o.y.). The accounting forecasts represented 167.4% of the portfolio in an irregular situation at the aggregate level in the period.

• The balance of deposits in foreign currency of the private sector grew 2.3% in the month (in currency of origin), limiting the year-on-year reduction (-12.8%). In April, the real balance of private sector deposits in national currency fell by 1.4% (-38% YoY), a performance mainly explained by demand accounts (-4.8%), with a preponderance of the interest-bearing segment. For its part, the dynamics of previous months continued, the balance of time deposits in pesos grew 3.2% in April.

• In the month, the broad liquidity indicator for the financial system grew 1.3 p.p. of total deposits to 79.3%. The monthly performance was driven by items in pesos (+3.1 p.p. to 80.2%); The ratio for the foreign currency segment fell (-5.4 p.p. to 75.7%), in the context of the increase in credit to the private sector in this denomination.

• Regulatory capital integration (RPC) stood at 40.3% of risk-weighted assets (RWA) for all entities in the month (+0.9 p.p. monthly and +10.2 p.p. y.o.y.). In this context, the regulatory capital position – regulatory capital net of the regulatory requirement – maintained a significant level of slack, reaching 405% of the requirement at the systemic level.

• The performance of solvency levels has been driven by the positive results obtained in the period. The total comprehensive results in homogeneous currency that the sector accumulated in the last 12 months were equivalent to 6.8% of assets (ROA) and 31.1% of equity (ROE), being levels higher than those recorded in a year-on-year comparison.

• In April, the main means of electronic payment continued to show a positive performance. The amount of immediate transfers grew 6.4% in real terms in the month (+20.1% real YoY) and that of cleared electronic checks (ECHEQs) 24.5% in real terms (+10% real YoY).

I. Financial intermediation activity

In April, financial intermediation with the private sector – in real terms – fell slightly for the segment in pesos, with a marked slowdown in the monthly rate of reduction. For their part, private sector loans and deposits arranged in foreign currency maintained their growth pattern throughout the month.

Taking into account the variations (in constant currency) of the most relevant items of the balance sheet in pesos of the financial system, in April credit to the private sector and the balance of passes with the BCRA (sources of funds) decreased. Meanwhile, in the month, the real balance of financing to the public sector, the real balance in the current account at the BCRA and the real balance of private sector deposits (applications of funds) decreased. In relation to the changes in equity of the main foreign currency items, credit to the private sector increased in April, offset by a decrease in liquidity and an increase in private sector deposits1.

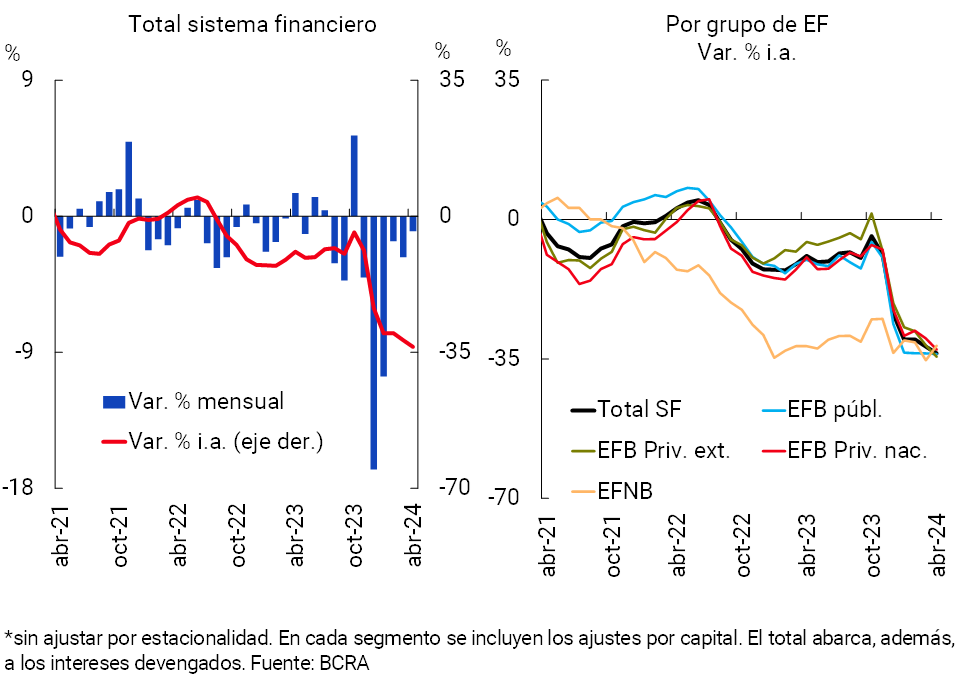

The balance of financing to households and companies in national currency fell by 1% in real terms between the peak of the month (+7.7% nominal)2, a variation that has been narrowing in recent months (see Graph 1). The monthly performance was heterogeneous among credit assistance, with increases in real terms in consumer lines (4.3% personal and 1.8% cards), as well as in advances (1.7%), and reductions in the rest. The balance of credit to the private sector in pesos increased in real terms in the group of public banks, while it fell in private banks. In year-on-year terms, the balance of credit to the private sector fell 33.6% at the systemic level.

Graph 1 | Credit balance to the private sector in pesos

In real terms*

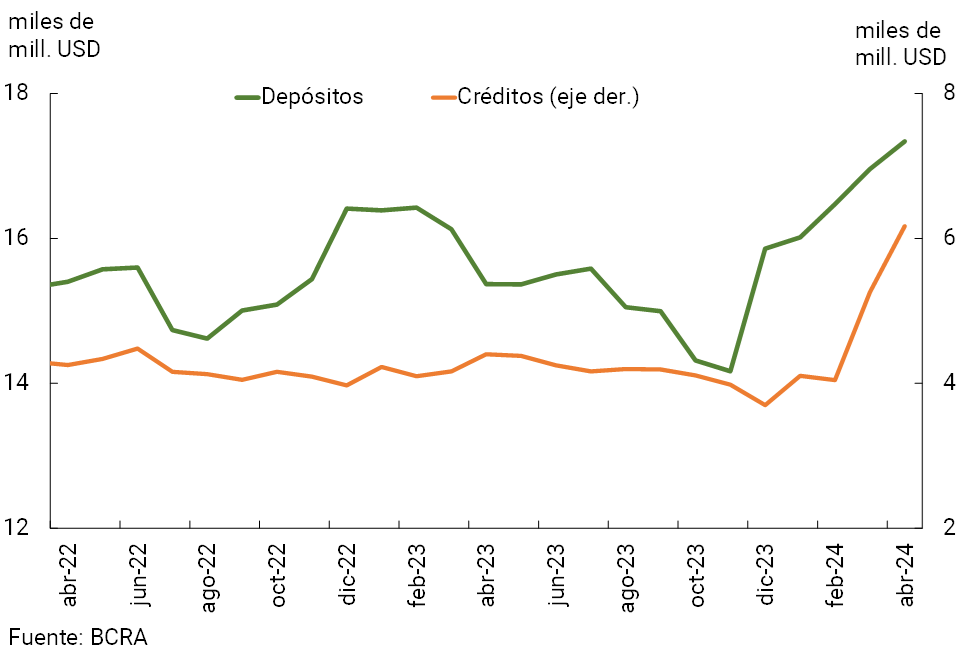

Credit to the private sector in foreign currency grew significantly (see Chart 2) and across the board among groups of entities during April. At the aggregate level, in the month credit to the private sector in foreign currency increased 17.3%; 29.6% in national private banks; 19.8% in public and 10.5% in foreign private ones (in all cases, in currency of origin). The monthly performance was explained by loans instrumented via documents and pre-financing for exports. Thus, the balance of loans to the private sector in foreign currency of the group of entities grew 40.1% compared to April 2023, a dynamism driven by private banks. When considering all bank financing to the private sector (national and foreign currency), between the end of the month the real balance remained unchanged in magnitude, accumulating a decrease of 10.1% compared to the same period in 2023.

Graph 2 | Financial intermediation in foreign currency with the private

sector – Financial system

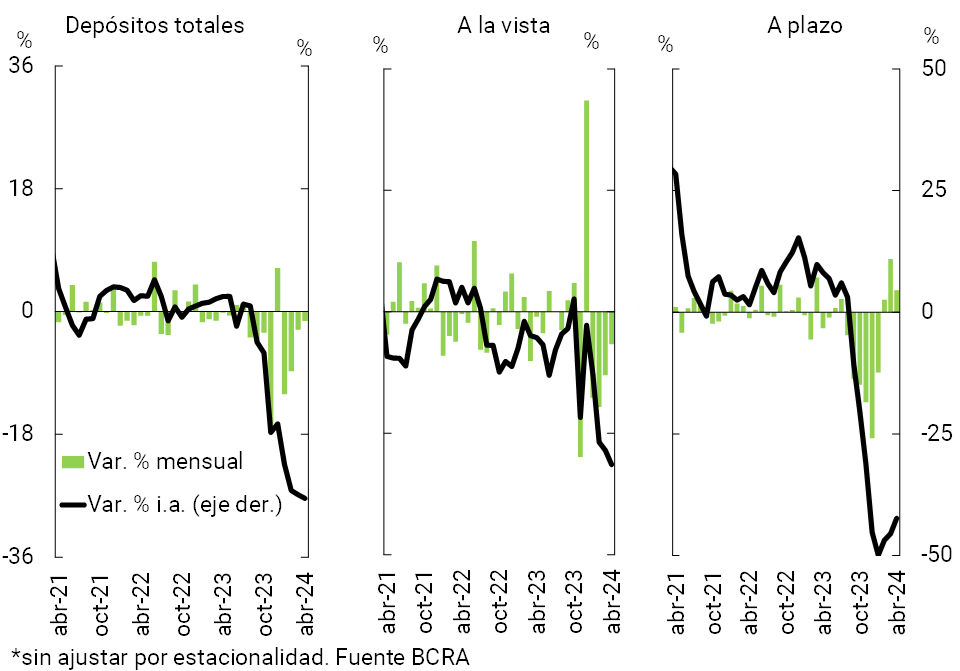

Regarding the sector’s funding, in April the real balance of private sector deposits in national currency fell by 1.4% (see Graph 3), mainly explained by the performance of demand accounts (-4.8% in real terms), with a preponderance of the interest-bearing segment. On the other hand, in line with the dynamics reflected in previous months, time deposits in pesos of households and companies expanded 3.2% in real terms in the period (generalized behavior among the different groups of entities). This increase was mainly explained by fixed-term deposits from legal entities providing financial services3. In year-on-year terms, the real balance of private sector deposits in national currency decreased by 38% (-42.3% for time deposits and -31.5% for demand).

Graph 3 | Balance of private sector deposits in pesos

In real terms* – Sistema financiero

In April, foreign currency deposits of the private sector grew again – in source currency – (+2.3% monthly, see Chart 2). Compared to the same period in 2023, the balance fell 12.8% at the systemic level. Thus, when considering all currencies and sectors, total deposits in the sector fell by 24.7% YoY.

II. Evolution and aggregate composition of the balance sheet

In April, the size of the balance sheet of the financial system, measured in terms of total assets in real terms, did not show any changes in magnitude compared to last month. In the last 12 months, the total assets of all entities accumulated a decrease of 10.1% at constant prices, a generalized performance among the different groups of financial institutions.

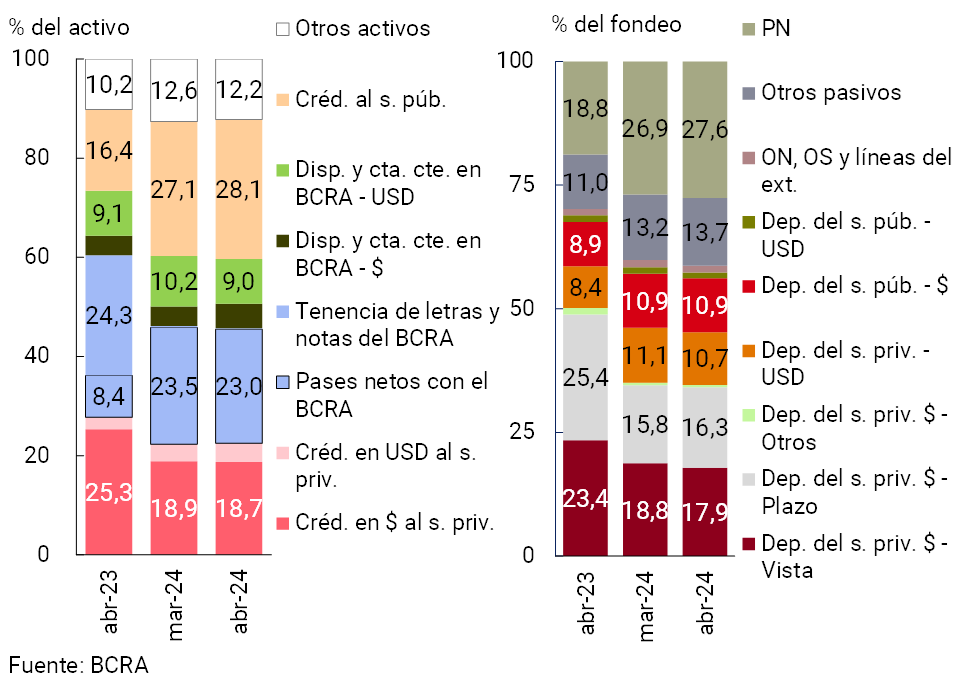

With respect to the components of the sector’s total assets, in April the relative weight of net passes with the BCRA and of availabilities and current accounts in this institution in foreign currency decreased, while financing to the non-financial public sector and availabilities and current accounts in the BCRA in pesos increased their weighting (see Graph 4). Regarding the composition of total funding, in the month the private sector’s demand accounts in pesos and deposits in foreign currency in the same sector reduced their relative importance, while the net worth and time placements of the private sector in pesos increased their share of the total4.

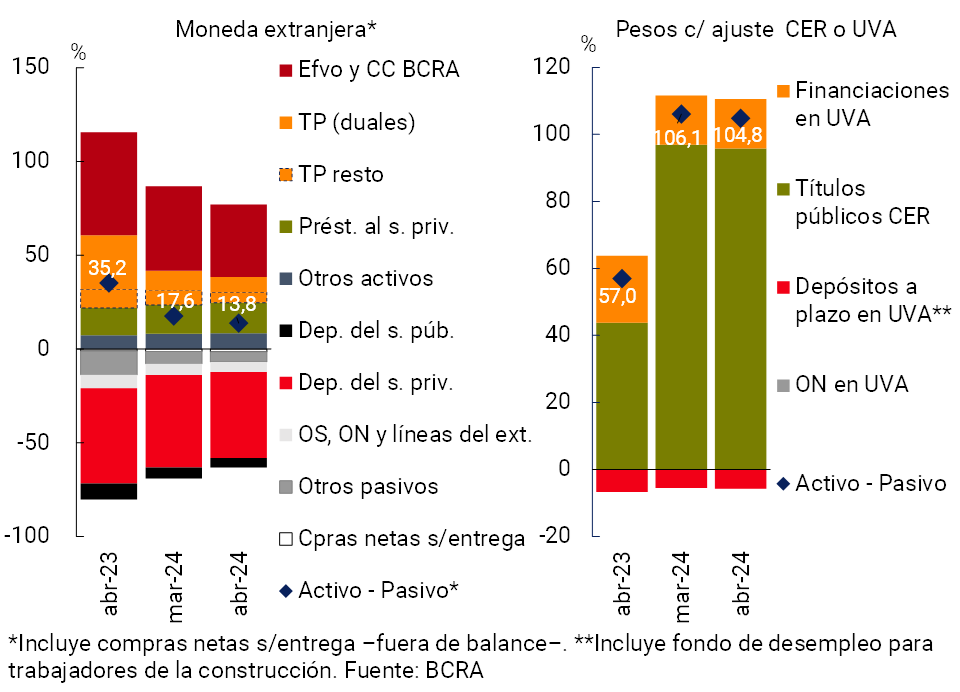

The estimated spread between assets and liabilities in foreign currency5 of the financial system stood at 13.8% of regulatory capital in April, 3.8 p.p. below the previous month’s record (-21.4 p.p. y.o.y.) (see Graph 5). In turn, the estimated spread between assets and liabilities in pesos with capital adjustment by CER (or agreed in UVA) totaled 104.8% of the RPC at the aggregate level, 1.3 p.p. less than the March level (+47.8 p.p. y.o.y.).

Figure 4 | Composition of assets and funding Financial

system – Participation %

Graph 5 | Spread between assets and liabilities

In % of PRC

III. Portfolio quality

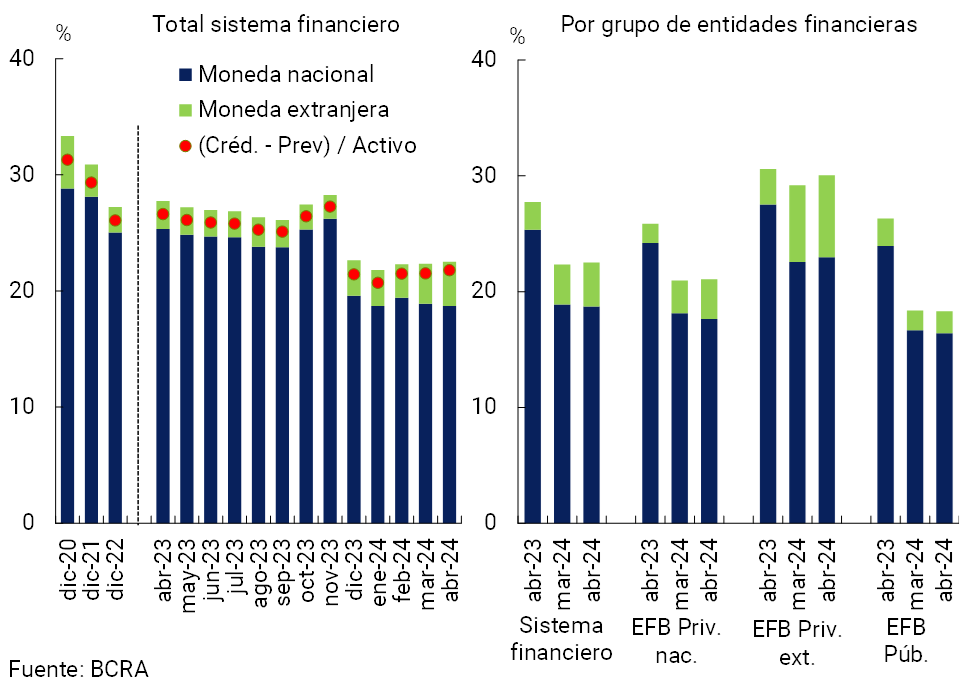

The gross exposure of the financial system to the private sector (including domestic and foreign currency) stood at 22.5% of total assets in April (see Chart 6), slightly above the previous month’s figure (+0.2 p.p., although -5.2 p.p. y.o.y.). The monthly dynamics were mainly driven by the performance of foreign private banking financial institutions. Regarding the credit segment in pesos, this ratio totaled 18.7% (-0.2 p.p. monthly and -6.6 p.p. y.o.y.), while it reached 3.8% of assets in items denominated in foreign currency (+0.4 p.p. monthly and +1.4 p.p. y.o.y.). The balance of credit to the private sector net of forecasts was equivalent to 21.8% of assets in the period, increasing 0.3 p.p. compared to March (-4.8 p.p. y.o.y.).

Graph 6 | Credit balance to the private sector in terms of assets

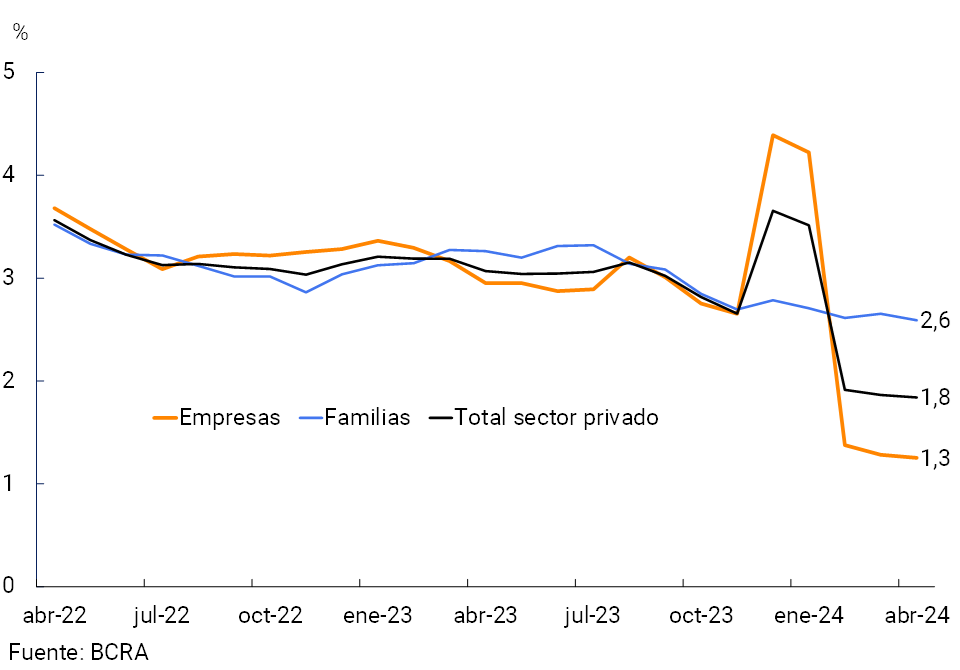

In April, the non-performing loan ratio to the private sector stood at 1.8%, without significant changes compared to last month (-1.2 p.p. y.o.y.; see Figure 7). When distinguishing by type of debtor, the NPL indicator for credit to households stood at 2.6% (-0.7 p.p. y.o.y.), while the NPL ratio for loans to companies totaled 1.3% (-1.7 p.p. y.o.y.).

Figure 7 | Private Sector Credit Irregularity Ratio – Financial System

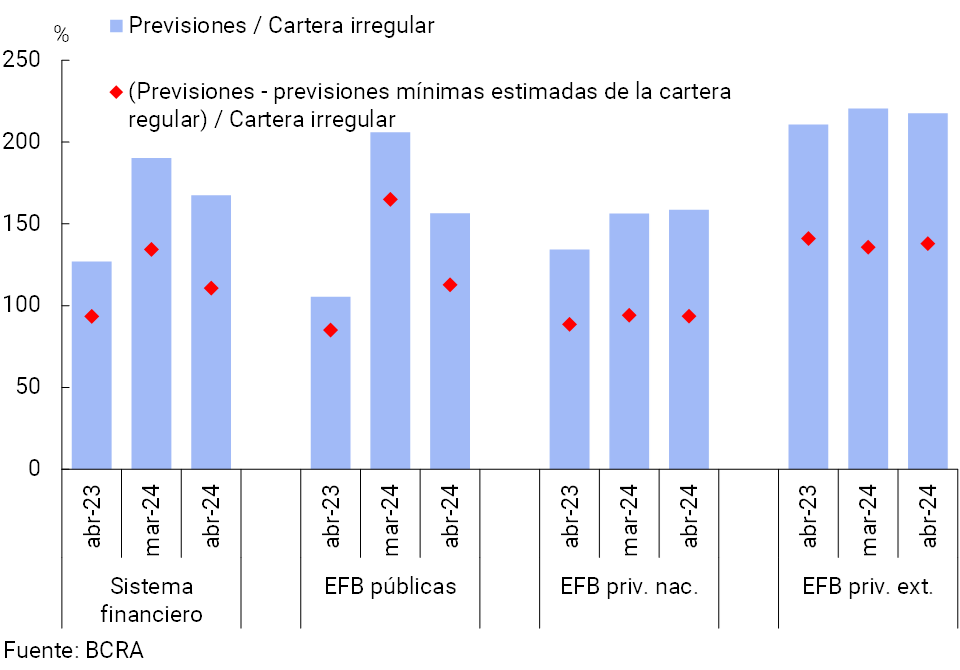

Figure 8 | Forecast balance (private sector) – By group of financial institutions

The financial system continued to exhibit comfortable levels of forecasting in April (see Chart 8). The accounting forecasts represented 167.4% of the portfolio in an irregular situation at the aggregate level, reducing 22.8 p.p. in the month, although they exceeded the level of the same month last year by 40.4 p.p.6. In the period, the balance of forecasts attributable to the portfolio in an irregular situation continued to exceed the total of said portfolio at the aggregate level, standing at 110.7% (-23.7 p.p. monthly and +17.2 p.p. y.o.y.)7.

IV. Liquidity and solvency

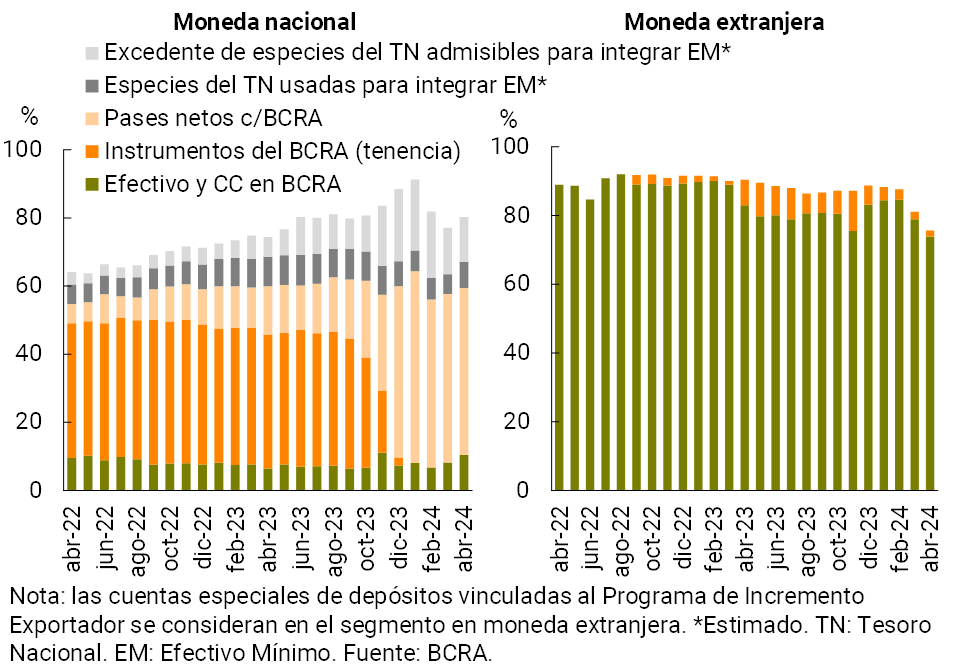

In April, the broad liquidity indicator8 for the financial system grew 1.3 p.p. of total deposits to 79.3% (+2.4 p.p. y.o.y.) (see Graph 9). The monthly performance was driven by items in pesos (+3.1 p.p. to 80.2%); the ratio for the foreign currency segment fell (-5.4 p.p. to 75.7%), in the context of the increase in credit to the private sector in this denomination (see Section 1). Regarding the composition of liquidity in pesos, the relevance of the accounts that entities have in the BCRA9 and of the National Treasury species admissible for integration of Minimum Cash increased during the month, partially offset by a reduction in passes with this Institution.

Figure 9 | Liquidity of the financial

system As a % of deposits

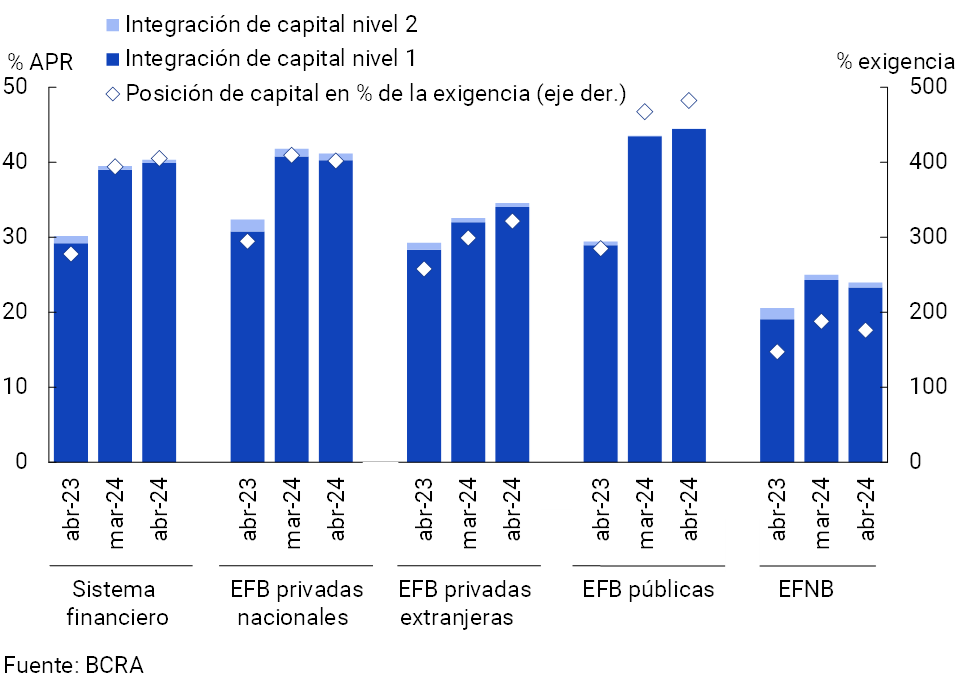

Regulatory capital integration (RPC) stood at 40.3% of risk-weighted assets (RWA) for all entities, 0.9 p.p. above the previous month’s level and 10.2 p.p. compared to April 2023 (see Chart 10). The monthly increase in this ratio occurred within the framework of a 3.6% real increase in the PRC (+26.8% real y.o.y.) that exceeded the 1.4% real increase in RWAs (-5.1% real y.o.y.). The capital position – regulatory capital net of the regulatory requirement – totaled 405% of the requirement at the systemic level and 82.1% of the balance of credit to the private sector net of provisions, well above the average of the last 10 years (23.6%).

Figure 10 | Capital Integration (RPC)

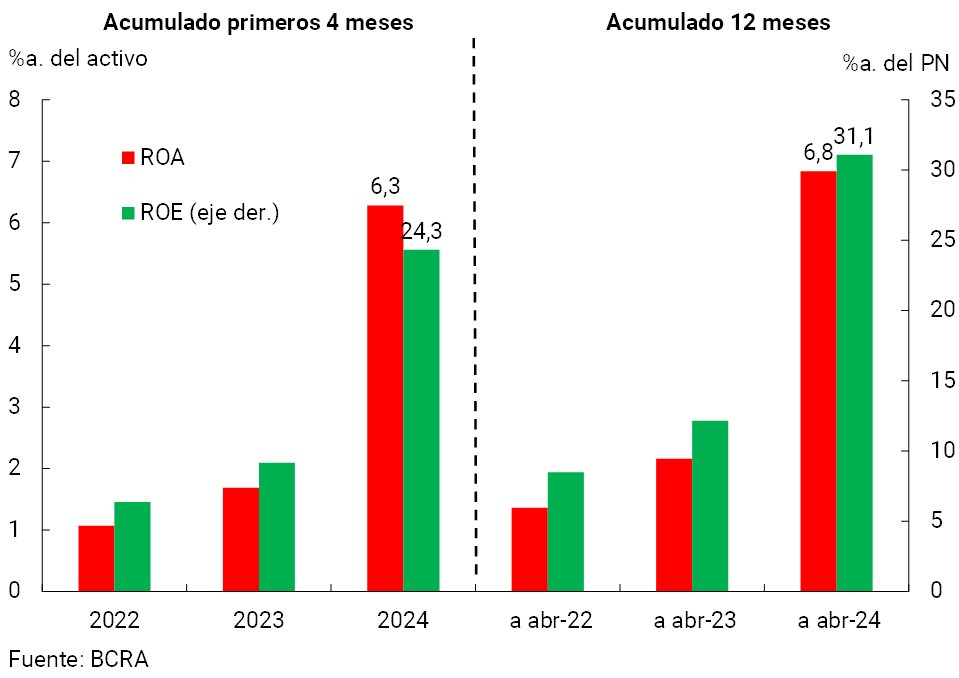

At the level of the aggregate financial system, the performance of capital levels has been driven mainly by the positive results obtained, in a framework in which the regulations on profit distribution are gradually being readjusted10. In relation to profitability, in the last 12 months the financial system had comprehensive total results in homogeneous currency equivalent to 6.8% of assets (ROA) and 31.1% of equity (ROE) (see Chart 11). The sector’s cumulative profitability increased in a year-on-year comparison, mainly due to a higher financial margin (increase in premiums for passes, CER adjustments, differences in share prices and results for securities, tempered by higher interest expenses), an effect partially offset by an increase in losses due to exposure to currency items and tax expenses. among other concepts.

Figure 11 | Comprehensive total profit in homogeneous currency of the financial system

V. Payment system

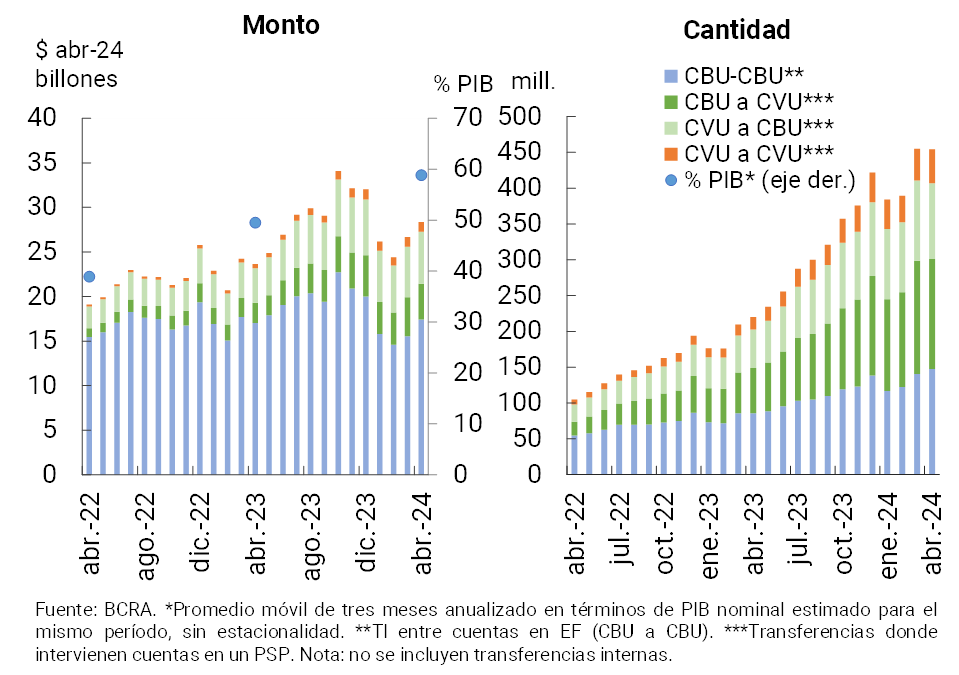

In April, immediate transfers (TI) increased in real amounts (+6.4%) compared to March, and did not show any changes in magnitude in the amounts traded (see Graph 12)11. In year-on-year terms, IT more than doubled in quantity (+106.4%) and increased 20.1% in real terms in amounts, a dynamism mainly explained by transactions involving the interaction between accounts in financial institutions (FIs) and payment service providers (PSPs), as well as the segment exclusively of accounts in PSPs12 13. It is estimated that the amount traded in the aggregate set of IT in the last three months (annualized) represented approximately 58.9% of GDP, 9.4 p.p. more than compared to the same month of the previous year.

Figure 12 | Instant Transfers (TI)

Payments by Transfer (PCT) by QR code decreased slightly in the month, although they continued to show significant growth compared to April 2023, with increases of 278% and 190% in real amounts and amounts, respectively (see Chart 13)14. This reflects the positive impact of the measures opportunely implemented by the BCRA to promote the adoption of payments through any digital wallet15.

Figure 13 | Payments with transfer (PCT) through interoperable QR codes

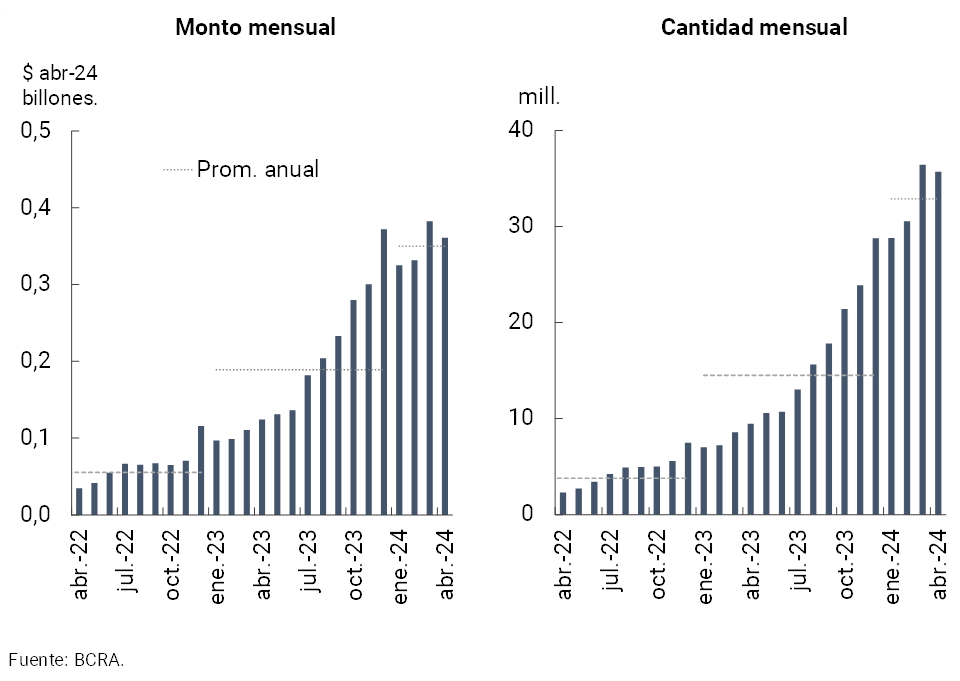

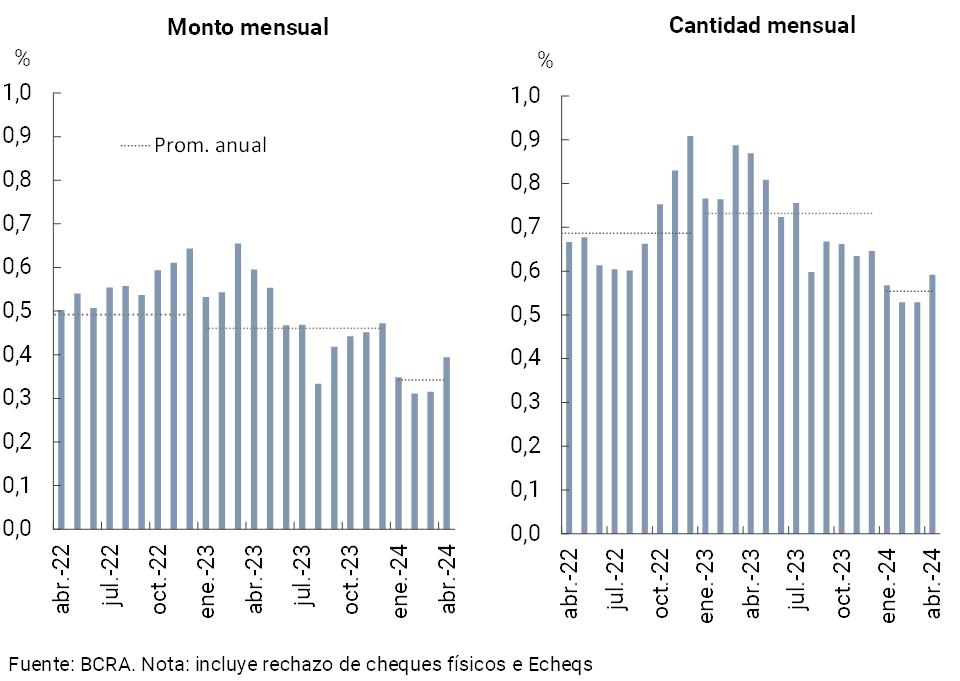

In April, check clearing increased significantly, with greater relative dynamism in operations through Echeqs (+24% in real amounts and amounts)16. The monthly dynamics were reflected in both physical and electronic operations (Echeqs). In this way, electronic clearing accounted for 71% and 46% of the total operations in the month, in terms of amounts and amounts, respectively. On the other hand, the rejection of checks due to lack of funds in relation to the total compensated increased slightly in April, however, it is lower in a year-on-year comparison (see Graph 14).

Figure 14 | Bounce rate for non-funded checks – In terms of total compensated

References

1 During the month, the balance of public securities denominated in foreign currency also fell, within the framework of the substitution by specie in pesos that has been taking place since the beginning of the year.

2 Includes principal adjustments and accrued interest.

3 It should be noted that during April it was established that the demand balances of the Money Market Mutual Funds in the entities must include a minimum cash requirement of 10% (Communication A 7988).

4 As mentioned in the previous section, the performance of private sector deposits in pesos in the month was influenced by the dynamics of placements by Money Market Mutual Funds.

5 Includes off-balance sheet foreign currency forward purchase and sale transactions. Liabilities include deposits that have variable remuneration depending on the evolution of the exchange rate – associated with the Export Increase Programme – and LEDIV are included in assets.

6 The monthly reduction was mainly explained by a one-off operation by a financial institution of magnitude within the framework of adjustments in its expected loss models.

7 Corresponds to the balance of total net forecasts of the minimum regulatory forecasts for debtors in situations 1 and 2, following the criteria of the minimum regulatory forecasts for risk of uncollectibility.

8 Considers availabilities, BCRA instruments in national and foreign currency, and all public securities authorized to be used as an integration of the requirement that arises in the Minimum Cash standard.

9 Part of this increase occurred within the framework of the regulatory changes that the BCRA has been implementing. In particular, since mid-April, Communication A 7988 has been in force, which increases, from 0% to 10%, the minimum cash requirement that financial institutions must apply to deposits in demand pesos that constitute the credit of Money Market Mutual Funds.

10 Communication A 7997establishes that financial institutions that decide to distribute results may do so in 3 equal monthly and consecutive installments. In the case of non-resident shareholders, financial institutions must grant them the option of receiving their dividends – in whole or in part – in a single cash installment provided that these funds are applied directly to the primary subscription of Bonds for the Reconstruction of a Free Argentina (BOPREAL).

11 In the month, IT from CBU to CVU accounted for 34% of the total amount of IT (14.5% of the total amount), from CVU to CBU they accounted for 23.3% of the amount of IT (21.1% of the total amount), between CVU (not including those made between accounts of the same PSP) they accounted for 10.4% of the IT (3.9% of the total amount) and finally those that originate from and reach CBU accounts (excluding those made between accounts of the same PSP) same financial institution) represented 32.3% of the total in quantity (60.4% in amount) in the month.

12 Compared to the same period in 2023, the number of transfers from CBU to CBU grew 72.2% (+1.7% in real amounts), +142.3% from CBU to CVU (77.5% in real amounts), +97.2% from CVU to CBU (50.3% in real amounts) and +170.1% between CVU (139% in real amounts).

13 In March, the value of IT averaged approximately $61,084 ($114,338 for IT between CBU, $23,041 for IT between CVU, $26,111 for CBU to CVU, and $55,325 between CVU and CBU).

14 In May, interoperable QR transactions averaged about $10,112.

15 The BCRA promotes the interoperability of QR codes for credit card payments. The QR codes displayed by merchants to charge with credit cards must accept that customers can make payments with any digital wallet (bank or payment service provider), regardless of whether there is a brand match with the QR (see Press Release of April 30, 2024).

16 In the month, the average amount of cleared checks was $2,011,635 ($1,051,210 in the physical format and $3,151,391 in ECHEQs).

Share on