I. Financial intermediation activity

In March, the financial intermediation of all entities with the private sector had a weak performance. According to the most relevant movements in the balance sheet of the aggregate financial system for items in pesos – in homogeneous currency – liquidity in the broad sense and financing fell in the month, mainly to the public sector. These variations were mainly offset by a real decrease in deposits. When considering the segment of items in foreign currency, deposits and liquidity decreased in the period, while there was an increase in financing, mainly to the public sector.

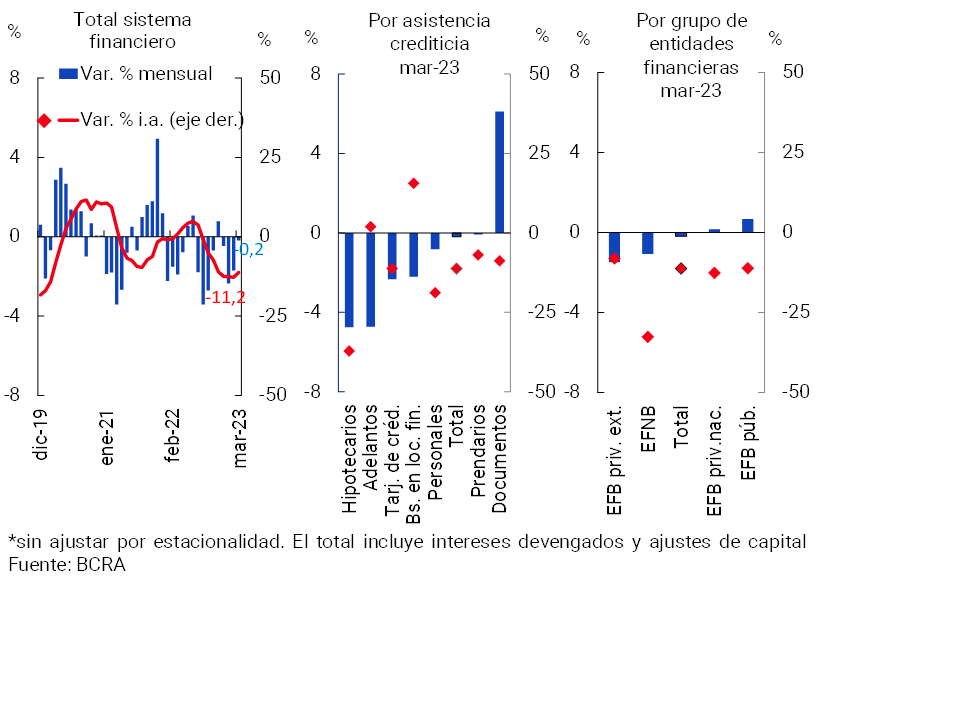

The real balance of credit in national currency to the private sector did not show any changes in magnitude with respect to February (-0.2%, see Graph 1)1. In March, there was a significant real increase in documents, which practically compensated for the reduction in the rest of the assistance. The year-on-year variation of the financing balance in pesos continued at negative levels.

Graph 1 | Credit balance to the private sector in pesos

In real terms*

Part of the positive monthly dynamics of the documents was driven by the Financing Line for Productive Investment of MSMEs (LFIP). Through this tool, almost $5.4 billion has been disbursed since its launch until the end of April 2023, covering more than 424,200 companies. The estimated balance of the LFIP totaled $1.4 trillion as of March. It is estimated that the LFIP accounted for 13.4% of total credit to the private sector (+1.5 p.p. y.o.y.), with 43.8% allocated to investment projects2.

In order to expand financing alternatives for MSMEs, the BCRA recently regulated the Open Circulation System (SCA) of Electronic Credit Invoices for MSMEs through financial institutions and established regulatory incentives associated with them. Through this system, MSMEs can transmit free of charge and discount the FCEM from their account3.

In March, the balance of credit to the private sector in foreign currency increased by 1.4%4. The total financing balance (in domestic and foreign currency) to the private sector did not show significant variations in the period (-0.2% in real terms), accumulating a fall of 11.2% in real terms year-on-year.

According to the latest results of the latest Credit Conditions Survey (CCS) corresponding to the first quarter of year5, the aggregate of participating entities indicated that, on the side of financing to companies, the credit supply would have remained unchanged. For its part, demand would have grown slightly at the beginning of 2023. In terms of financing to families, neutrality was also observed in terms of supply, along with a certain increase in demand for consumer and pledge lines.

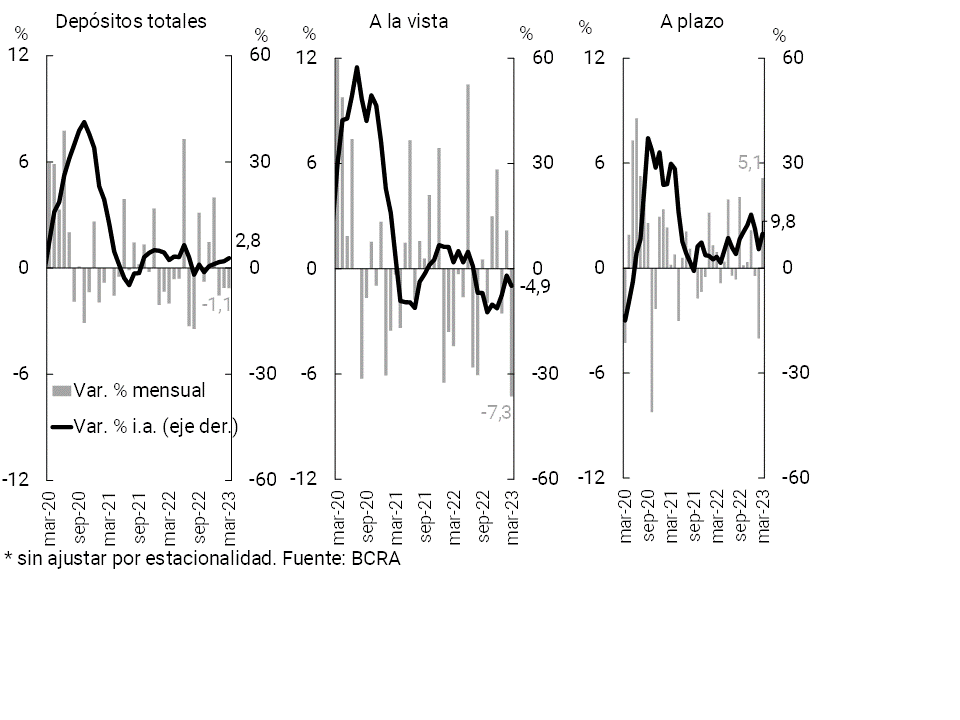

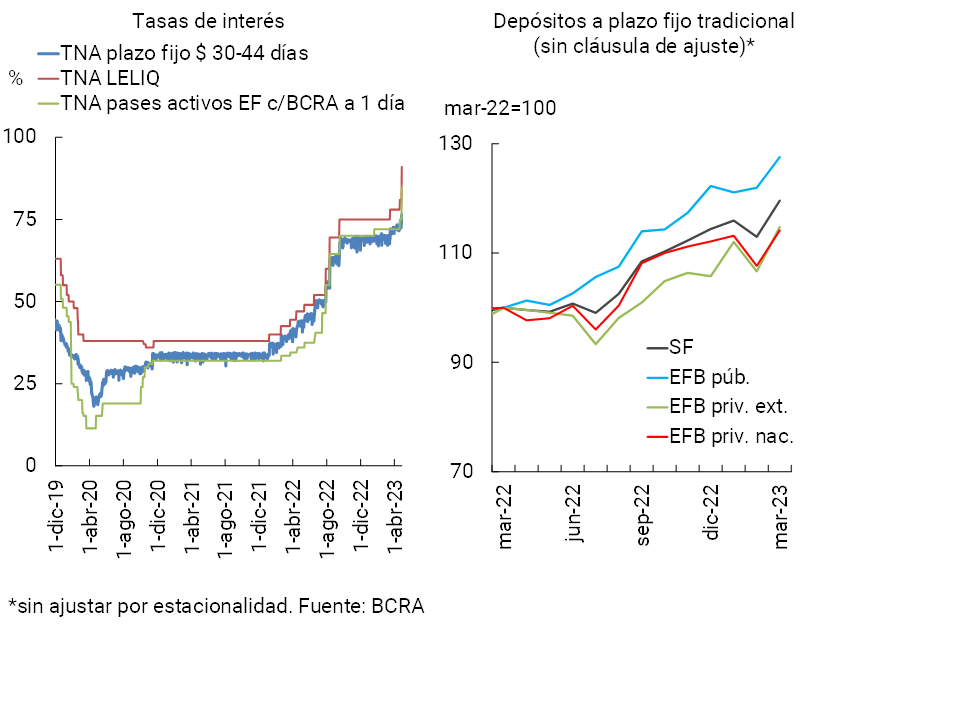

On the funding side of the group of entities, the real balance of deposits in pesos of the private sector decreased monthly in March (see Graph 2), a performance explained by demand accounts, while time deposits increased. This performance was partly explained by the rotation towards time deposits to the detriment of demand deposits by some institutional investors, reversing the behavior of the previous month. In addition, the increase in time deposits in the month was in line with the increase in minimum nominal interest rates (see Chart 3).

Graph 2 | Balance of private sector deposits in pesos

In real terms* – Financial system

Graph 3 | Interest rates and fixed-term deposits

In mid-May, the BCRA ordered a new increase in the interest rate of the 28-day LELIQ and the minimum interest rate for time deposits in pesos of up to $30 million of individuals, bringing them to 97% TNA (90% minimum TNA for the rest of the fixed terms). In addition, it was decided to reduce the interest rate for the financing of unpaid balances of credit cards for individuals: from June it will drop from 88% to 86% TNA, when the amount financed, considering each credit card account, does not exceed $200,0006.

The balance of private sector deposits in foreign currency decreased 1.8% in source currency in March. Thus, the balance of total private sector deposits (in domestic and foreign currency) fell by 1.5% in real terms in the period.

In year-on-year terms, the balance of deposits in pesos of the private sector increased by 2.8% in real terms. In this context, the real balance of total deposits (all currencies and sectors) remained unchanged in magnitude from the level of a year ago.

II. Evolution and aggregate composition of the balance sheet

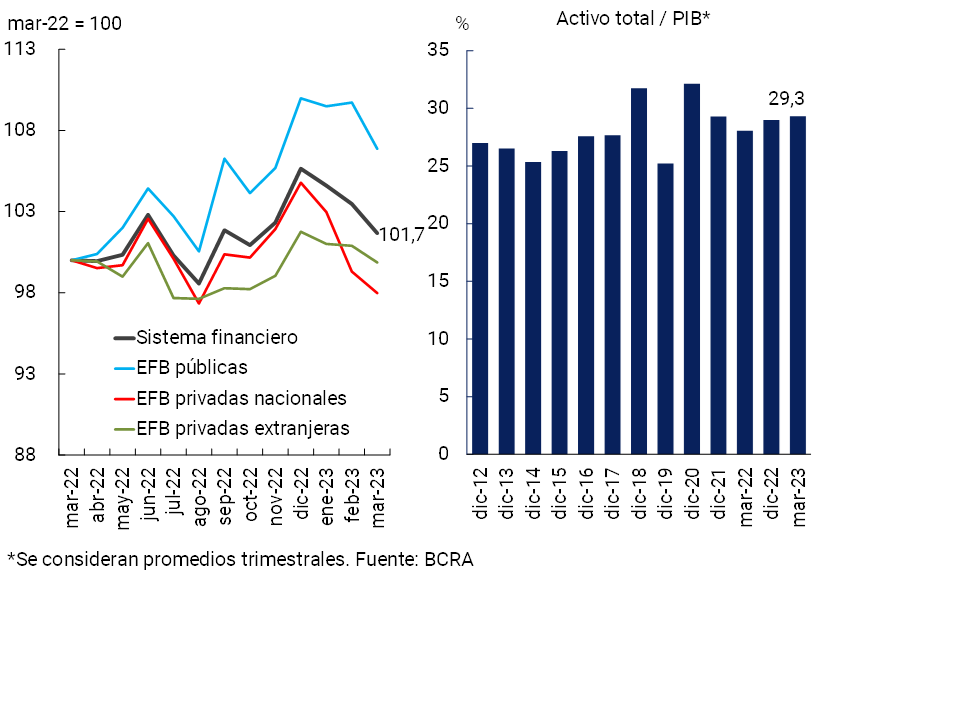

In March, the total assets of all financial institutions fell by 1.7% in real terms, above the level of a year ago (see Chart 4). The monthly decrease in assets was verified in all groups of financial institutions. It is estimated that the aggregate assets of the financial system represented 29.3% of GDP at the end of the first quarter of the year, exceeding both the level of March 2022, and the average of the last 10 years (of 28.2%).

Figure 4 | Total assets in real terms

Financial system

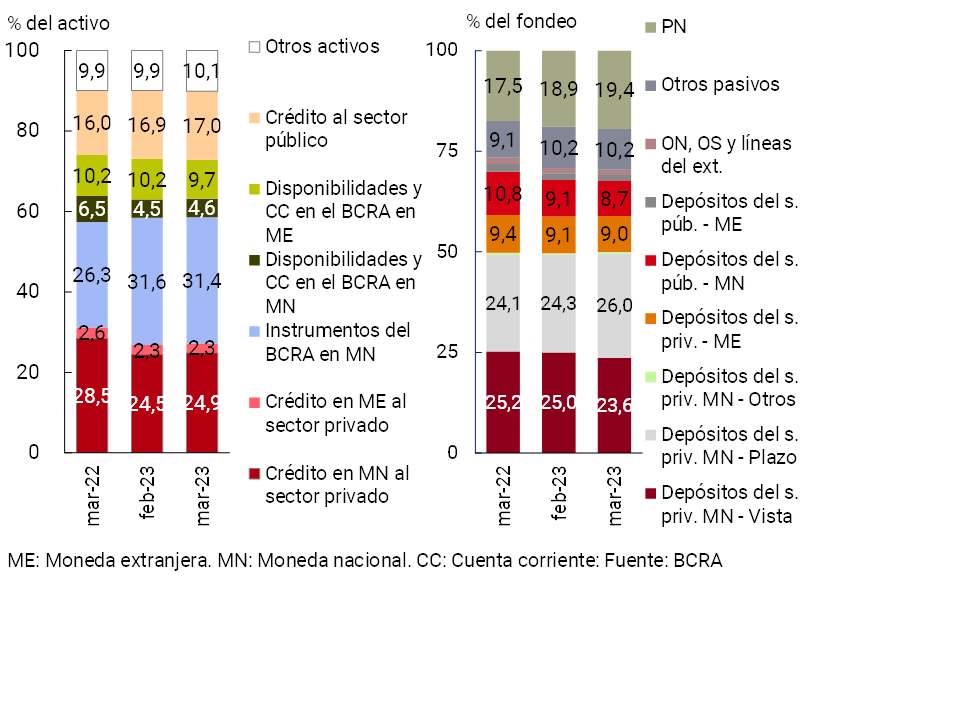

With respect to the composition of the sector’s total assets, in March the weighting of the balance of availabilities and current accounts in the BCRA decreased, while the relative importance of credit in pesos to the private sector increased (see Chart 5). On the side of total funding, in March the demand accounts in pesos of the private sector and the deposits of the public sector in the same denomination reduced their relevance. On the other hand, term placements in pesos from the private sector and net worth increased their weighting in total funding in the period (see Chart 5).

Graph 5 | Composition of assets and total funding

Financial system – Share %

In the month, the estimated spread between assets and liabilities of the financial system in foreign currency increased by 1.5 p.p. of regulatory capital (RPC) to 32.2% (+22.2 p.p. y.o.y.)7. With regard to items adjusted for CER (or UVA), the estimated spread between assets and liabilities stood at 57.8% of the PRC in the period for all entities, 14.3 p.p. more than in February (-14.5 p.p. y.o.y.)8.

III. Portfolio quality

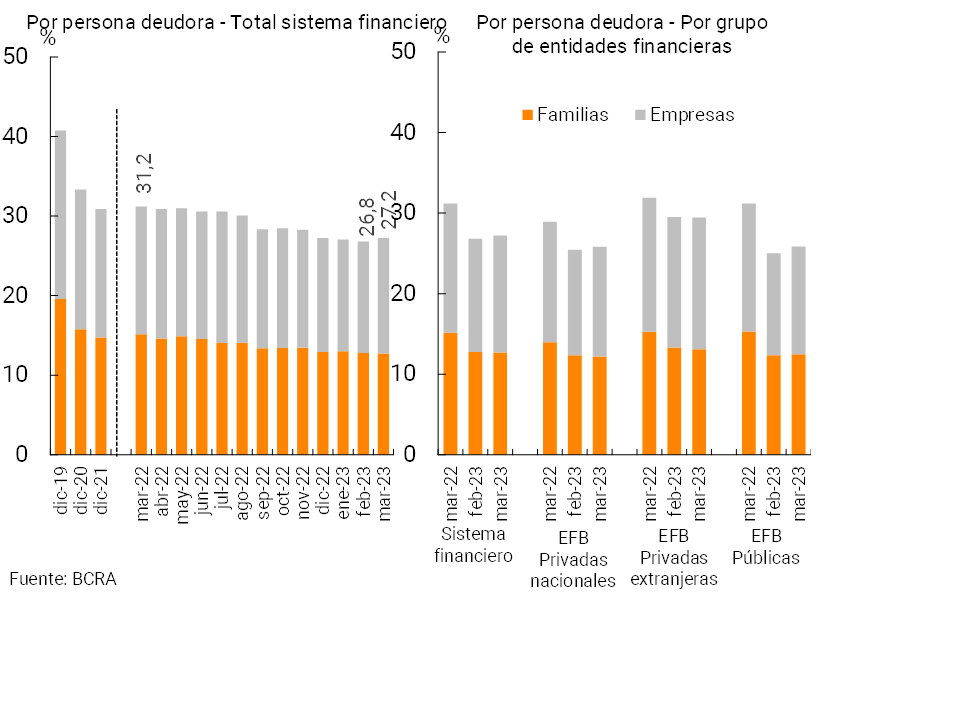

The weighting of total credit to the private sector in the assets (gross exposure) of all financial institutions totaled 27.2% in March, increasing slightly in month9 (-3.9 p.p. y.o.y.). The monthly dynamics responded to the corporate financing segment, which slightly increased its relative weight to 14.5% of assets, while credit for households slightly decreased its weighting to 12.7% of assets (see Graph 6)10. If the balance of forecasts is deducted, exposure to the private sector reached 26.1% of assets at the end of the first quarter for the financial system as a whole.

Graph 6 | Private Sector Credit Balance / Assets

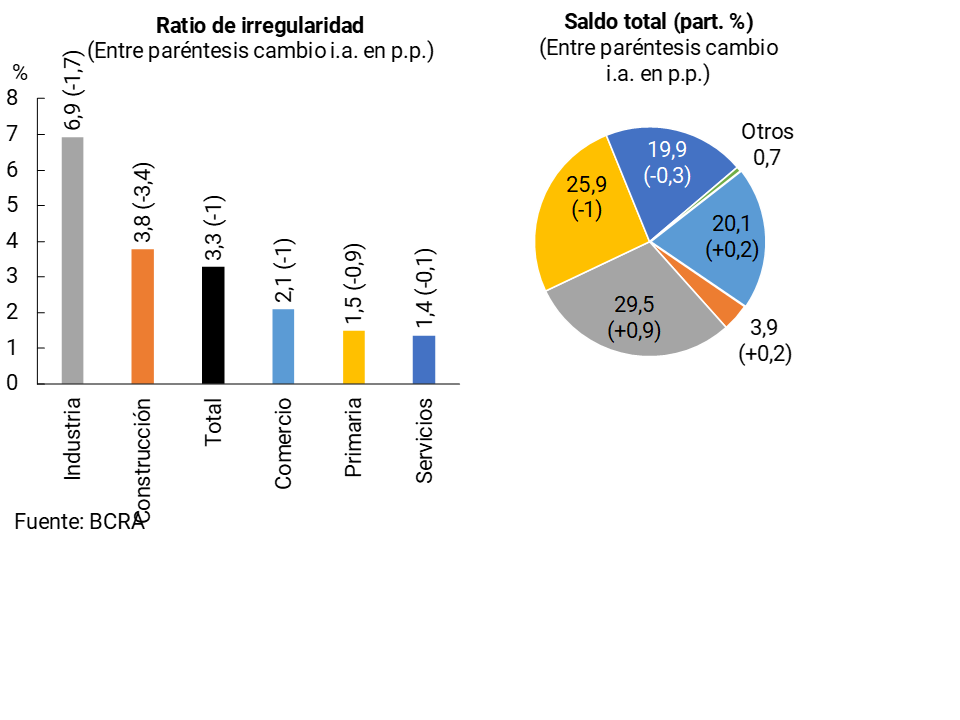

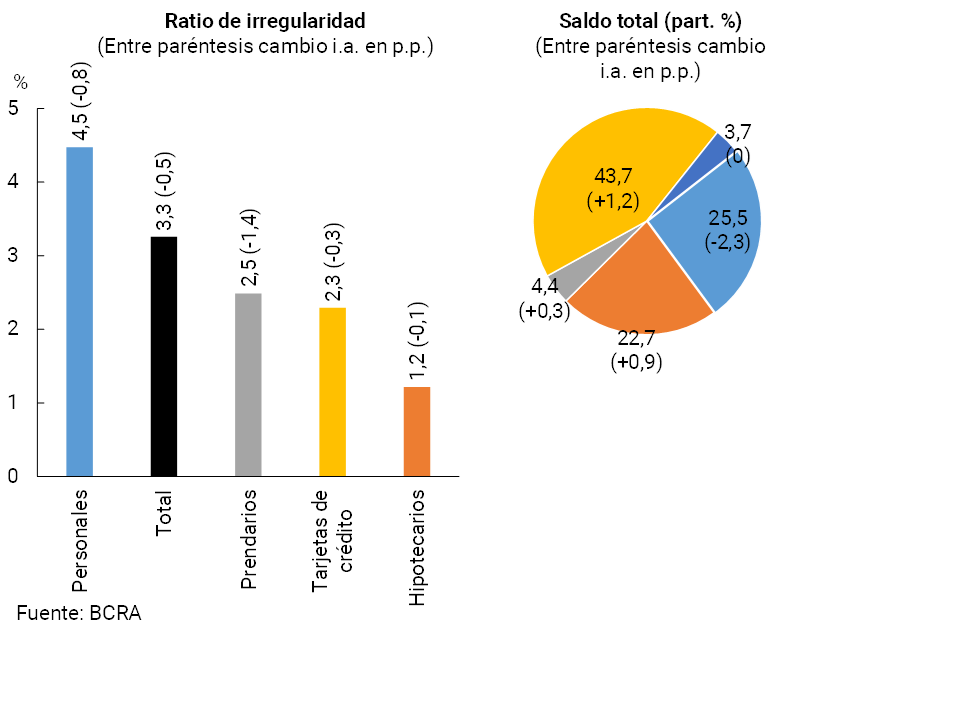

In March, the irregularity of credit to the private sector remained at around 3.2% of the total portfolio of this sector, falling 0.7 p.p. in year-on-year terms. When distinguishing by credit segment, in the month the non-performing loan indicator for loans to companies decreased slightly to 3.2%, thus being 0.9 p.p. lower than the level of a year ago. This year-on-year dynamic was widespread among the different sectors of economic activity (greater falls in the irregularity ratio of loans to companies in industry and construction, see Graph 7). For its part, in the month the indicator of irregularity of loans to households increased slightly to 3.3%, accumulating a year-on-year decrease of 0.5 p.p. The year-on-year performance of the NPL indicator for loans to families was reflected in all assistance (with greater falls in collateral and personal loans, see Chart 8).

Figure 7 | Irregularity ratio for credit to companies as of March 2023 – Sistema financiero

Figure 8 | Irregularity ratio for credit to households as of March 2023 – Sistema financiero

Forecast levels remained relatively high in March. The forecasts accounted for by the aggregate financial system stood at 4% of total credit to the private sector in March (no significant changes in the month and -0.5 p.p. y.o.y.) and at 126.1% of the non-performing portfolio (-1.2 p.p. compared to February and +9.8 p.p. y.o.y.). In the period, the balance of forecasts attributable to the irregular situationportfolio 11 totaled 93.9% of said portfolio at the aggregate level (+3.7 p.p. y.a.).

IV. Liquidity and solvency

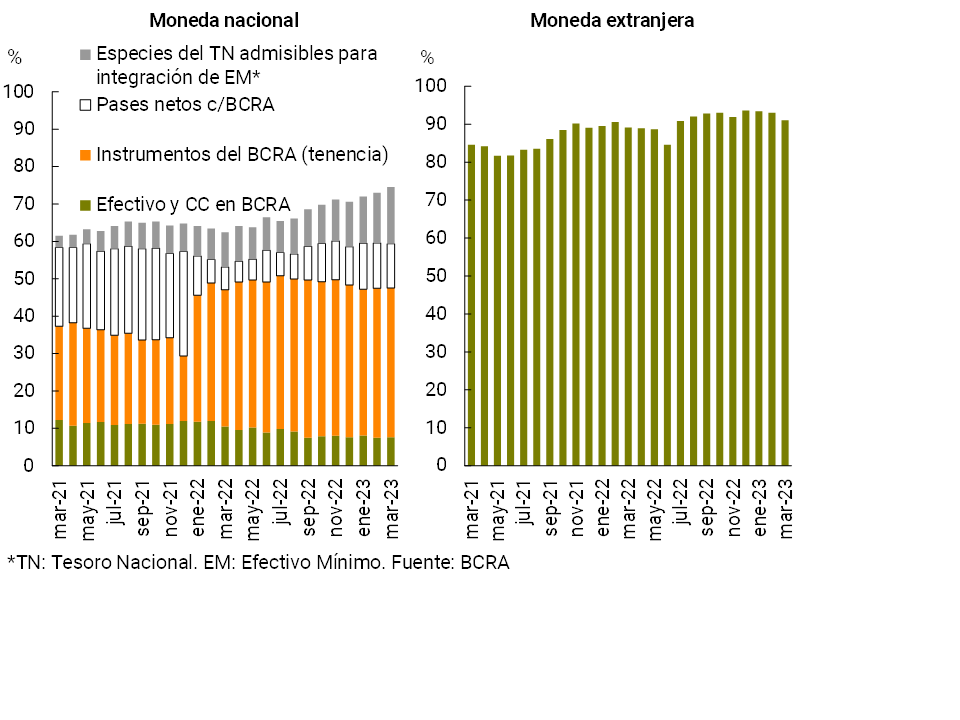

In March, the12th broad liquid assets of the financial system amounted to 77.2% of deposits, slightly increasing compared to February. The indicator for items in pesos stood at 74.6% and 92.2% for those in foreign currency (see Graph 9). In relation to the composition of liquidity in national currency, between the end of the month the participation of the National Treasury species eligible for the integration of Minimum Cash increased, while that of the BCRA instruments -holdings and passes- decreased. In a year-on-year comparison, ample liquidity (in pesos and in foreign currency) increased 10.5 p.p. of total deposits.

Graph 9 | Liquidity of the financial system

In % of deposits

The sector’s solvency indicators increased slightly in the month. The integration of regulatory capital (RPC) of the aggregate of entities stood at 31.4% of risk-weighted assets (RWA), 0.3 p.p. above the February figure (+3.8 p.p. y.o.y.). 96.8% of the PRC was accounted for by Tier 1 capital, which has a greater capacity to absorb potential losses. In March, the capital position – regulatory capital net of the minimum regulatory requirement – totaled 292.6% of the requirement at the systemic level (+47.3 p.p. y.o.y.) and 47.1% of the balance of credit to the private sector net of forecasts, above the average of the last 10 years (18.5%).

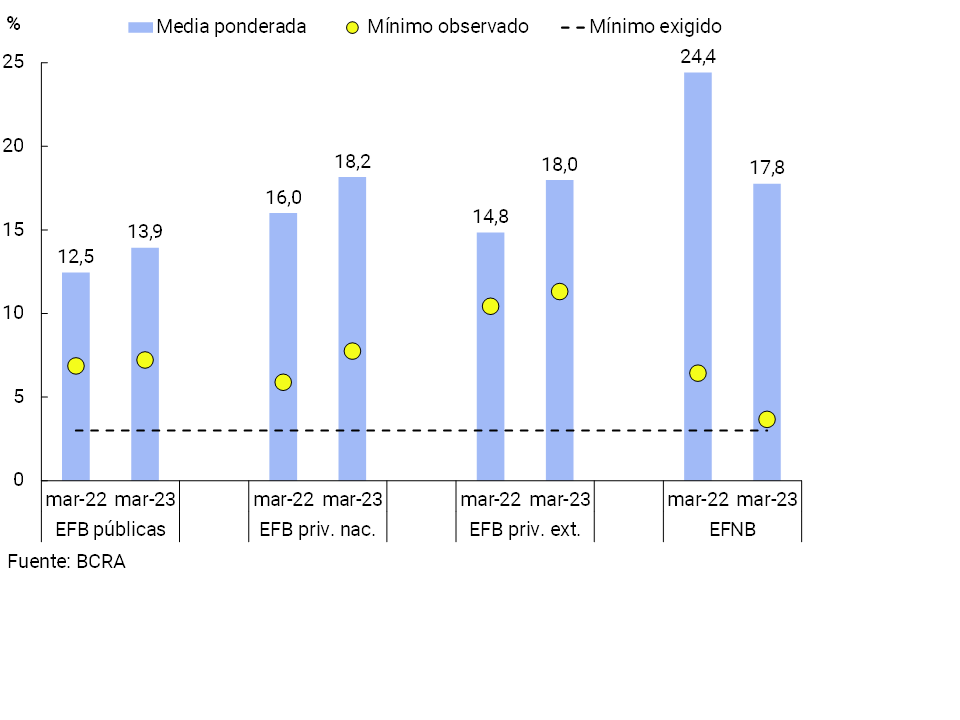

The leverage ratio (as measured by the Basel Committee: Tier 1 capital in terms of a broad measure of exposures) increased year-on-year across all groups of banks (EFNBs decrease, see Chart 10). As of March, the leverage ratio reached 16.3% at the aggregate level, increasing 2 p.p. y.o.y., well above the regulatory minimum (3%). All entities verified a level higher than the regulatory minimum.

Figure 10 | Leverage ratio

Tier 1 capital in terms of a broad measure of exposure

With regard to the sector’s internal capital generation, in the first quarter of the year the financial system recorded a positive comprehensive total result (in homogeneous currency) which, in terms of assets (ROA), was similar to that verified in the last 12 months. The IT-23 ROA for the aggregate of financial institutions was lower than that of the IVT-22, mainly due to higher negative monetary results, an effect partially offset by the decrease in other expenditures (tax and administrative)13.

V. Payment system

In the first quarter, the main retail electronic payment methods continued to expand and gain relevance in the economy, reflecting the effect of growing demand from users, as well as the stimuli promoted by the BCRA and the adoption by businesses, financial institutions and payment service providers (PSPs)14.

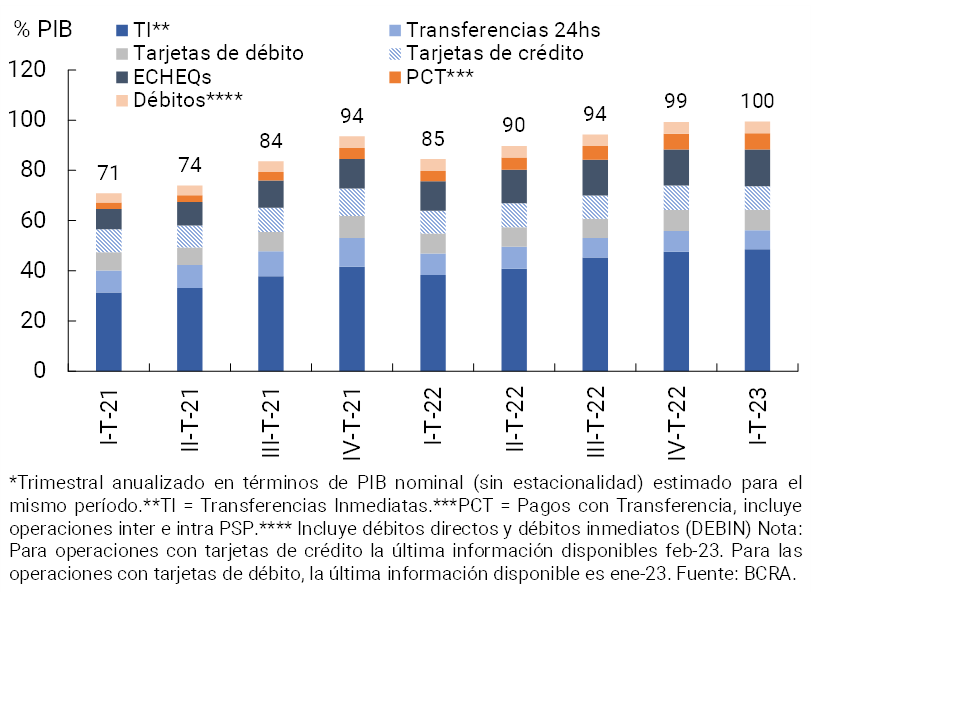

Within the framework of seasonal factors, the volume of the most relevant electronic means of payment increasedin March 15. In this context, it is estimated that the amounts traded in this set of payment instruments reached an amount equivalent to almost 100% of GDP at the end of the first quarter, a level higher than that evidenced both one and two years ago (see Graph 11).

Figure 11 | Main Retail Electronic Payment Methods – Estimated Amounts Traded as % of GDP

Payments by transfer (PCT), electronic checks (ECHEQs) and immediate transfers (TI) were the instruments that gained the highest share, both in the margin and in a year-on-year comparison. In this way, ITs and ECHEQs are consolidated as the instruments with the greatest relative weight (48.6% and 14.6% of GDP, respectively), while PCTs are gradually gaining prominence (6.5% of GDP)16.

Finally, in March, the ratio of rejection of checks due to lack of funds in terms of the total compensated rose slightly in amounts (value of 0.89%) and in terms of amounts traded (value of 0.65%). The current levels of this indicator were slightly above those recorded in the same period of the previous year (+0.18 p.p. and +0.13 p.p. in terms of quantity and actual amounts, respectively).

Back to top

References

1 Includes principal adjustments and accrued interest.

2 Within the framework of the LFIP, as of mid-May, it was established that financing of investment projects will have a maximum interest rate of 76% TNA and 88% TNA for all other financing.

3 See “Press Release” of 4/5/23 and Communication “A” “7758”. In addition, financial institutions may deduct from the minimum cash requirement in pesos the financing of customers who meet the condition of MSMEs instrumented through the purchase of FCEM.

4 Expressed in currency of origin.

5 For more information see “Credit Conditions Survey (ECC)”.

6 See Communication “A” “7767”.

7 Includes forward purchase and sale transactions of foreign currency classified off-balance sheet. Liabilities include deposits in the agricultural sector that have variable remuneration depending on the evolution of the exchange rate.

8 It should be noted that during March the National Government exchanged bonds and bills, delivering mostly specie in pesos with CER adjustment in exchange for specie in pesos at a fixed rate.

9 This monthly increase occurred in a context in which assets fell in real terms relatively more than credit to the private sector (–1.7% vs. –0.2%, respectively, see Sections of the Report above).

10 Considering exclusively financing in pesos, the ratio between credit to the entire private sector and assets stood at 24.9% in the period (+0.4 p.p. monthly and -3.6 p.p. y.o.y.), while the indicator for foreign currency items stood at 2.3% of assets (unchanged in the month and -0.3 p.p. y.o.y.).

11 Total net forecasts of the minimum regulatory forecasts for debtors in situations 1 and 2, according to the criteria of the minimum regulatory forecasts for risk of uncollectibility.

12 Considers availabilities, BCRA instruments in national and foreign currency, and all public securities authorized to be used as minimum cash integration.

13 IT-23 ROA was higher than in the same period of 2022, mainly due to the increase in financial margin (results from securities and interest income from loans, partially offset by higher interest expenses paid), which was tempered by higher losses due to exposure to currency items.

14 Recently, the BCRA provided that PSPs that offer payment accounts (PSPCPs) may not carry out or facilitate their customers to carry out transactions with digital assets – including cryptoassets and those whose yields are determined based on the variations that they register – that are not authorized by a competent national regulatory authority or by this Institution. The measure seeks to mitigate the risks that operations with these assets could generate for users of financial services and the national payment system. This standard equates the rules that PSPCPs and financial institutions must comply with (“Communication “A” 7506″). For more details, see “Press Release” and “Communication “A” 7759″.

15 In the month, Immediate Transfers (TI) had a significant increase of 18.8% in amounts and 16.8% in real amounts. Within IT among CBUs, a significant increase was observed in the use of electronic business banking, with an increase of 24.6% in quantities and 15.6% in real amounts. The use of interoperable QR codes also had a significant increase of 19% in quantities and 12.4% in real amounts. Finally, ECHEQs increased by 14.5% in quantities and 13.7% in real amounts.

16 Within the framework of retail digital operations, the BCRA provided that tourists will be able to pay with electronic wallets with debit in accounts of non-residents abroad at an exchange rate that will have financial dollars as a reference (see “Press Release” and “Communication “A” 7762″).

Share on