1. Executive Summary

In real and seasonally adjusted terms, means of payment (private transactional M2) would have remained stable in September, a dynamic that responded to both the behavior of transactional demand deposits and working capital deposits held by the public.

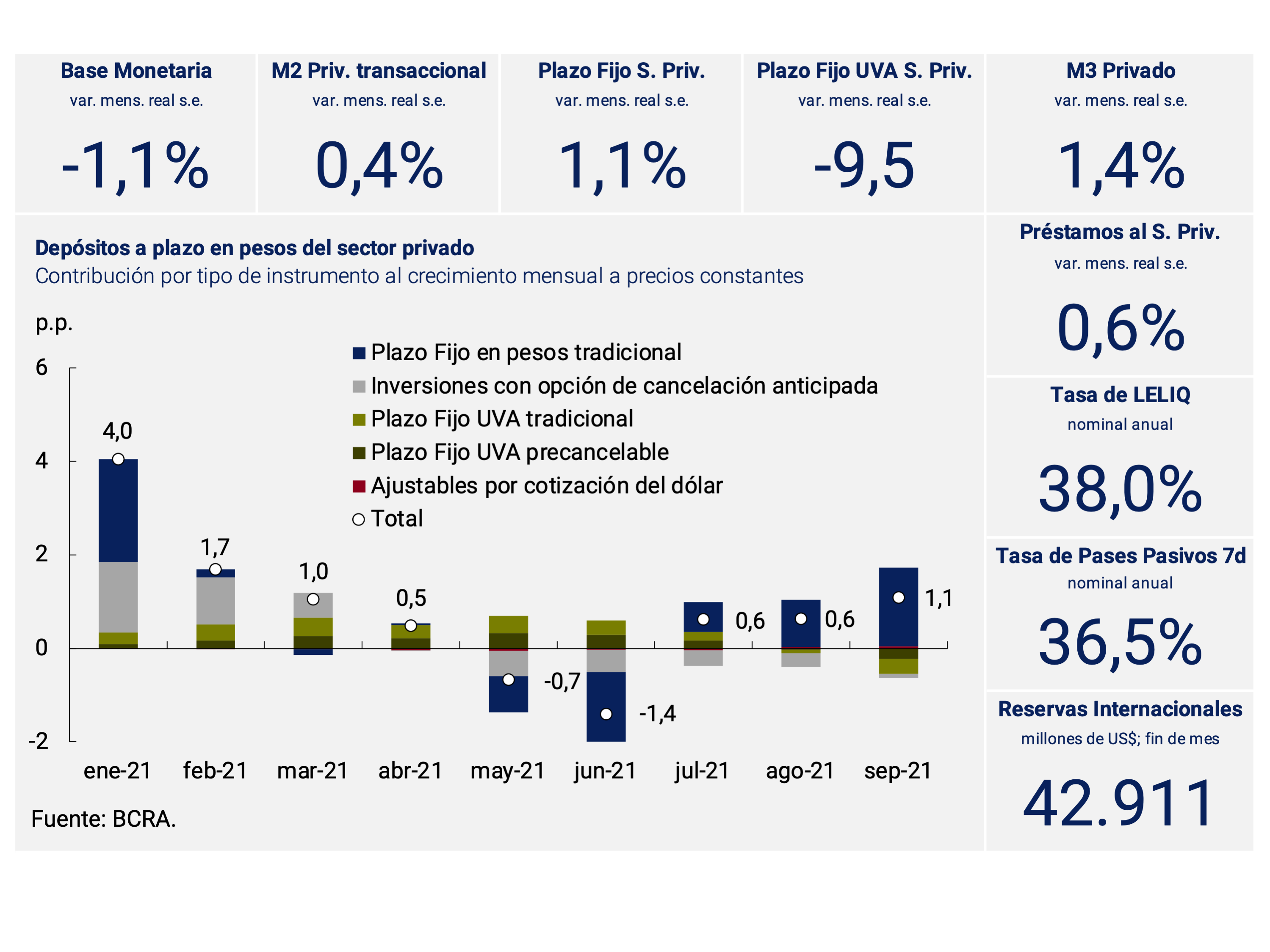

Fixed-term deposits in pesos of the private sector would have grown for the third consecutive month at constant prices. By instrument, the largest contribution continued to come from fixed-term placements in traditional pesos. Meanwhile, UVA deposits contributed negatively to the month’s expansion. Growth was concentrated in the wholesale segment and was driven by company placements. Financial Services Providers (FSPs) showed a greater preference for shorter-term assets, leading to an increase in interest-bearing demand deposits and a relative stability of traditional fixed-term placements.

Loans in pesos to the non-financial private sector would have grown in the month at constant prices. The increase was explained by documents, loans with collateral and personal lines. Recently, the BCRA extended the validity of the LFIP until March 2022. The line was expanded to small agricultural producers, provided that the funds are intended to increase the productive capacity of beef and/or bovine milk. The gastronomy, hotel, cultural and leisure services sectors will also be able to access the working capital line, with a grace period of 6 months.

2. Payment methods

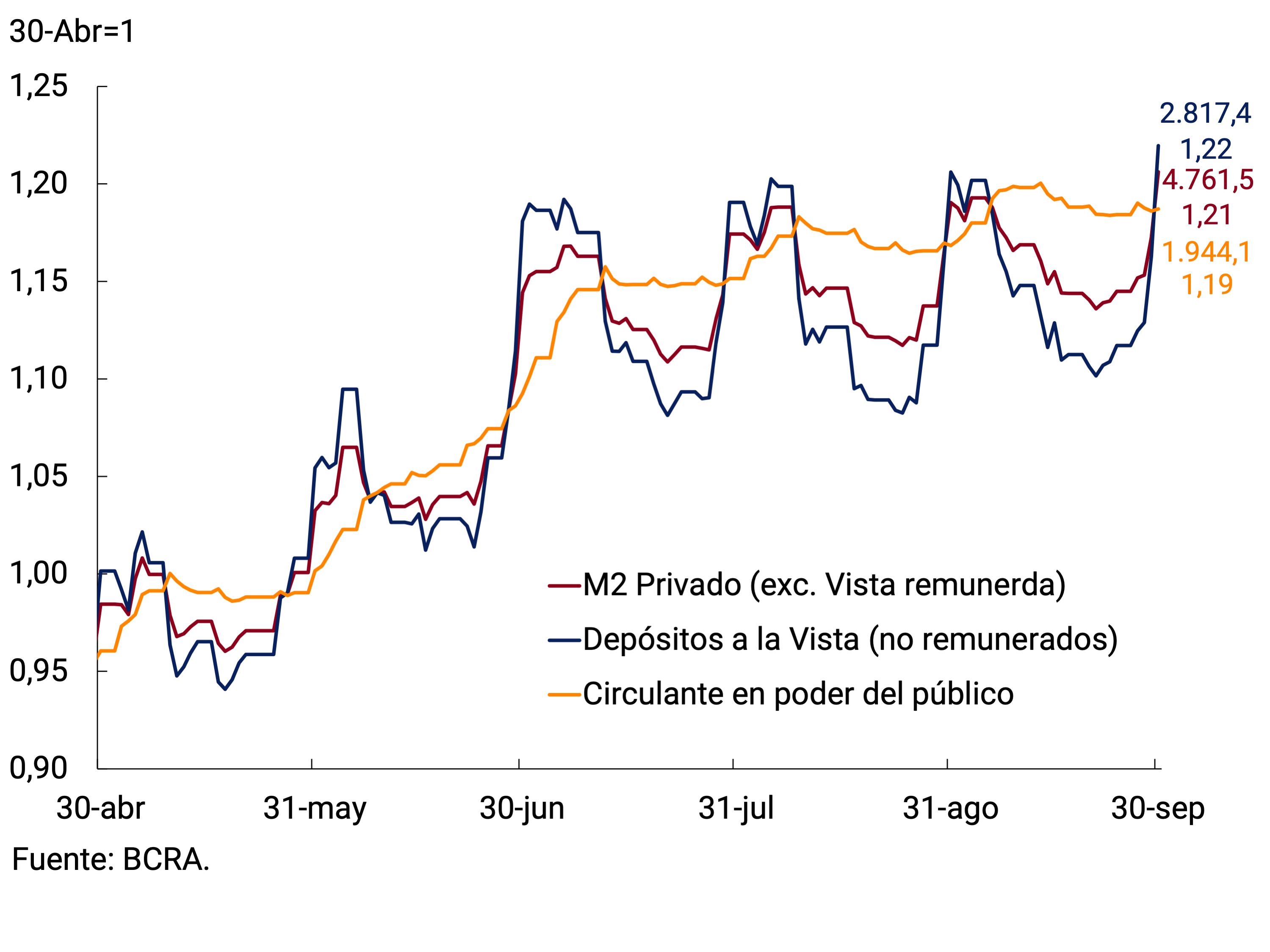

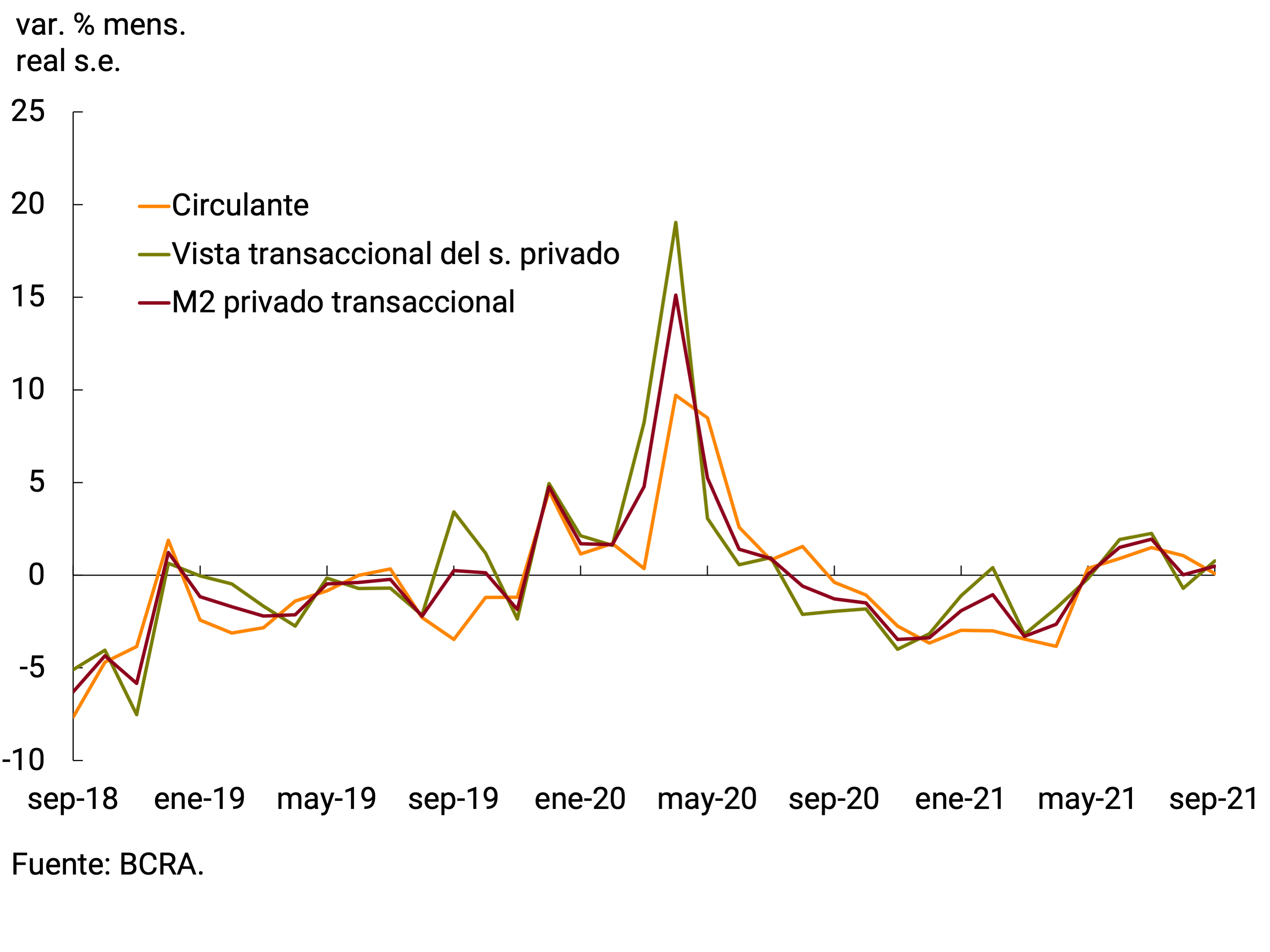

In real terms1 and seasonally adjusted (s.e.), means of payment (private transactional M22) would have shown a slight increase (0.4%). At the level of its components, transactional demand deposits would have grown slightly (0.7%), while working capital held by the public would have remained practically unchanged (0.1%), breaking with a period of four consecutive months of increases. Thus, so far this year, payment methods have accumulated a fall of around 5% s.e. at constant prices (see Figures 2.1 and 2.2).

Figure 2.1 | M2 Private transactional and its components

Index at current prices

Figure 2.2 | M2 Private transactional

Monthly change s.e. at constant prices by component

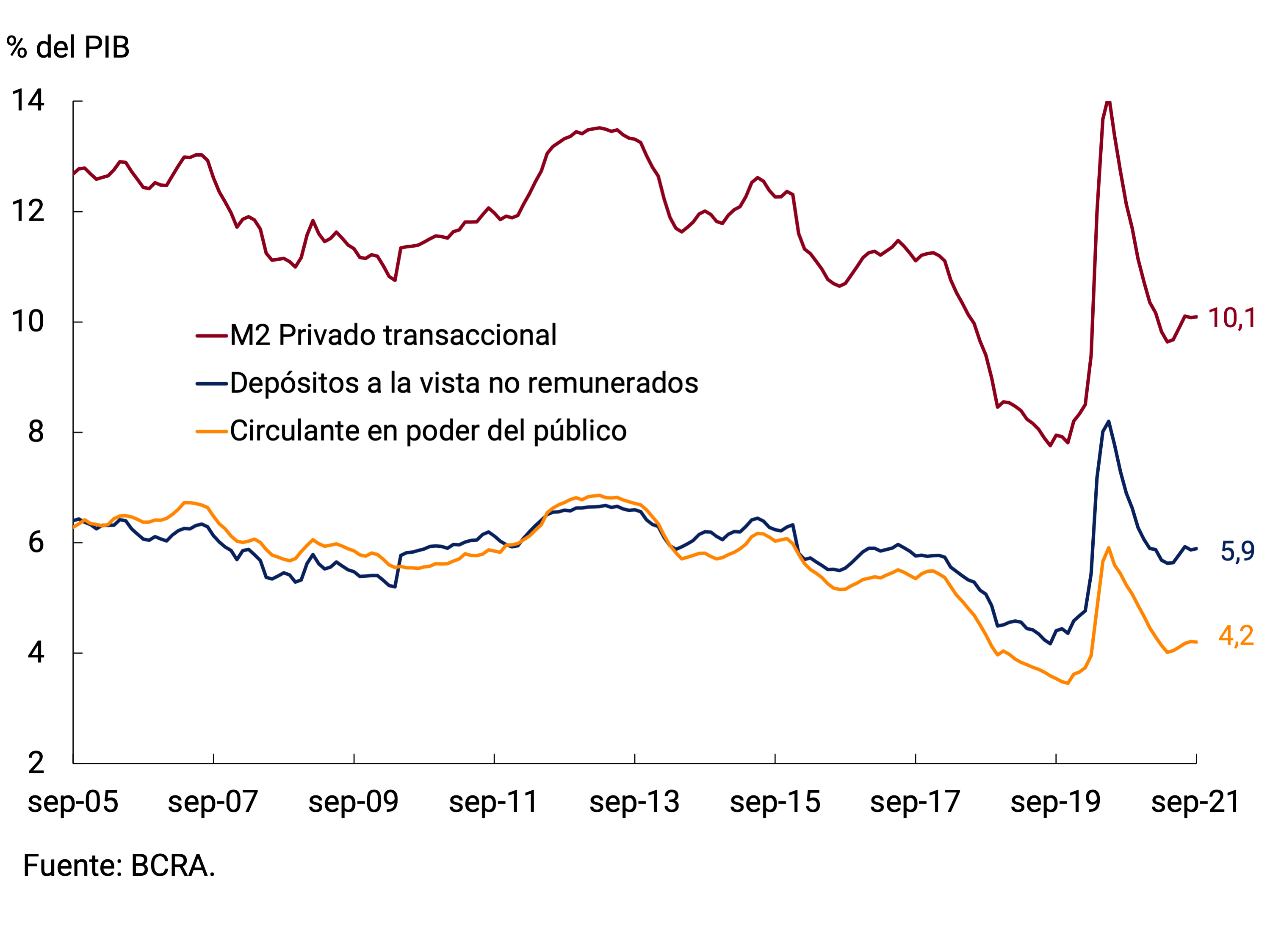

In terms of GDP, private transactional M2 continued to stand at around 10%, 1.3 p.p. below the average ratio for the period 2010-2019 and -4.0 p.p. compared to the peak reached in 2020. Transactional demand deposits accounted for 5.9% of GDP, remaining around that value since mid-year. Finally, the ratio of public currency to GDP also remained relatively stable at 4.2%, close to its lowest value in the last 15 years (see Figure 2.3).

Figure 2.3 | Transactional private M2 in terms of GDP

3. Savings instruments in pesos

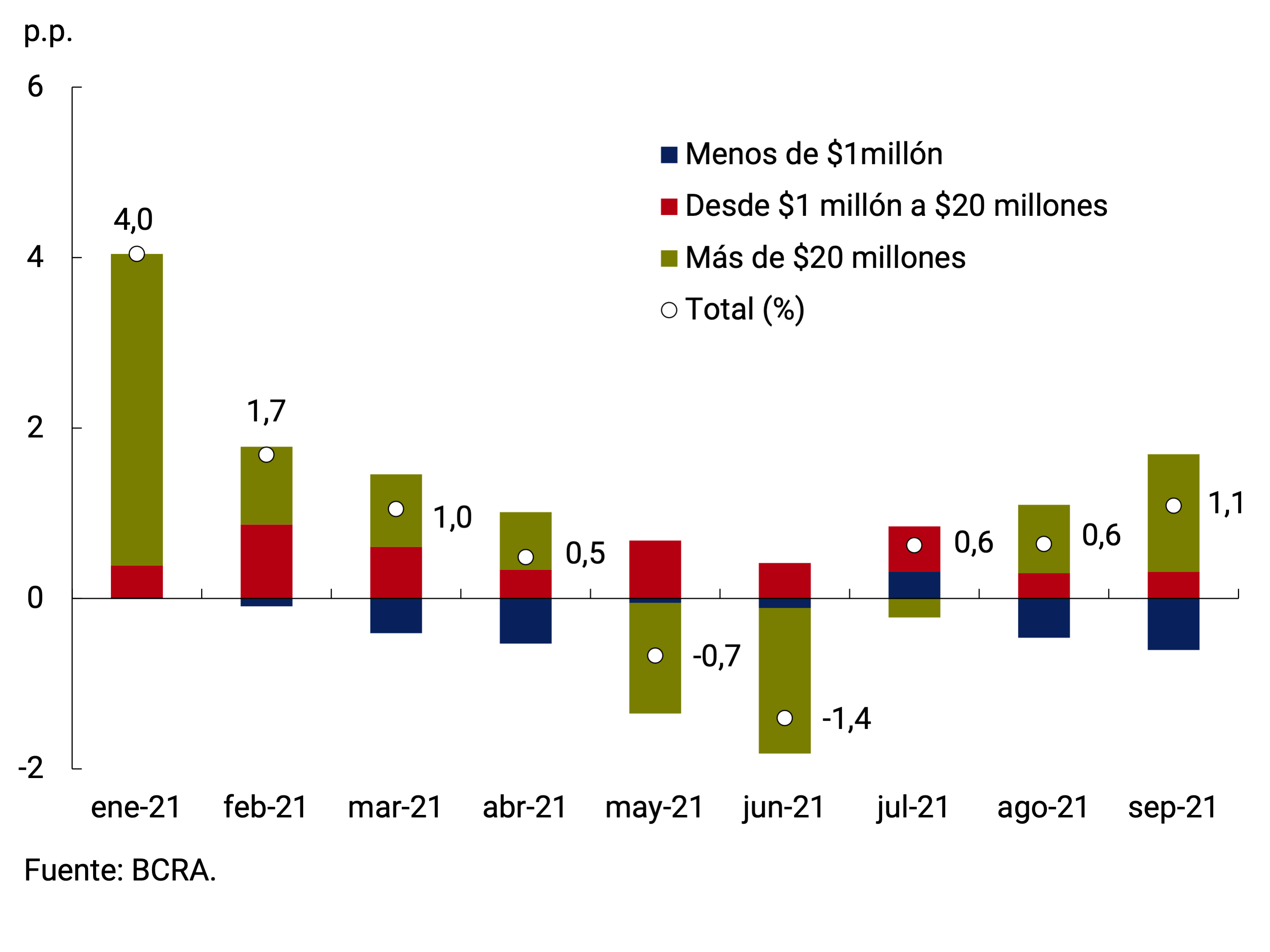

Fixed-term deposits in pesos in the private sector would have completed the third consecutive month with a positive monthly rate of change at constant prices (1.1% s.e.) and so far this year they have accumulated an increase of 7.7% in real terms. Growth in September would have been higher than in previous months and was once again concentrated in deposits of more than $20 million (see Figures 3.1 and 3.2).

Figure 3.1 | Fixed-term deposits in pesos from the private

sector Daily balance at constant prices by amount stratum

Figure 3.2 | Fixed-term deposits in pesos of the private

sector Contribution by layer of amount to the real monthly variation

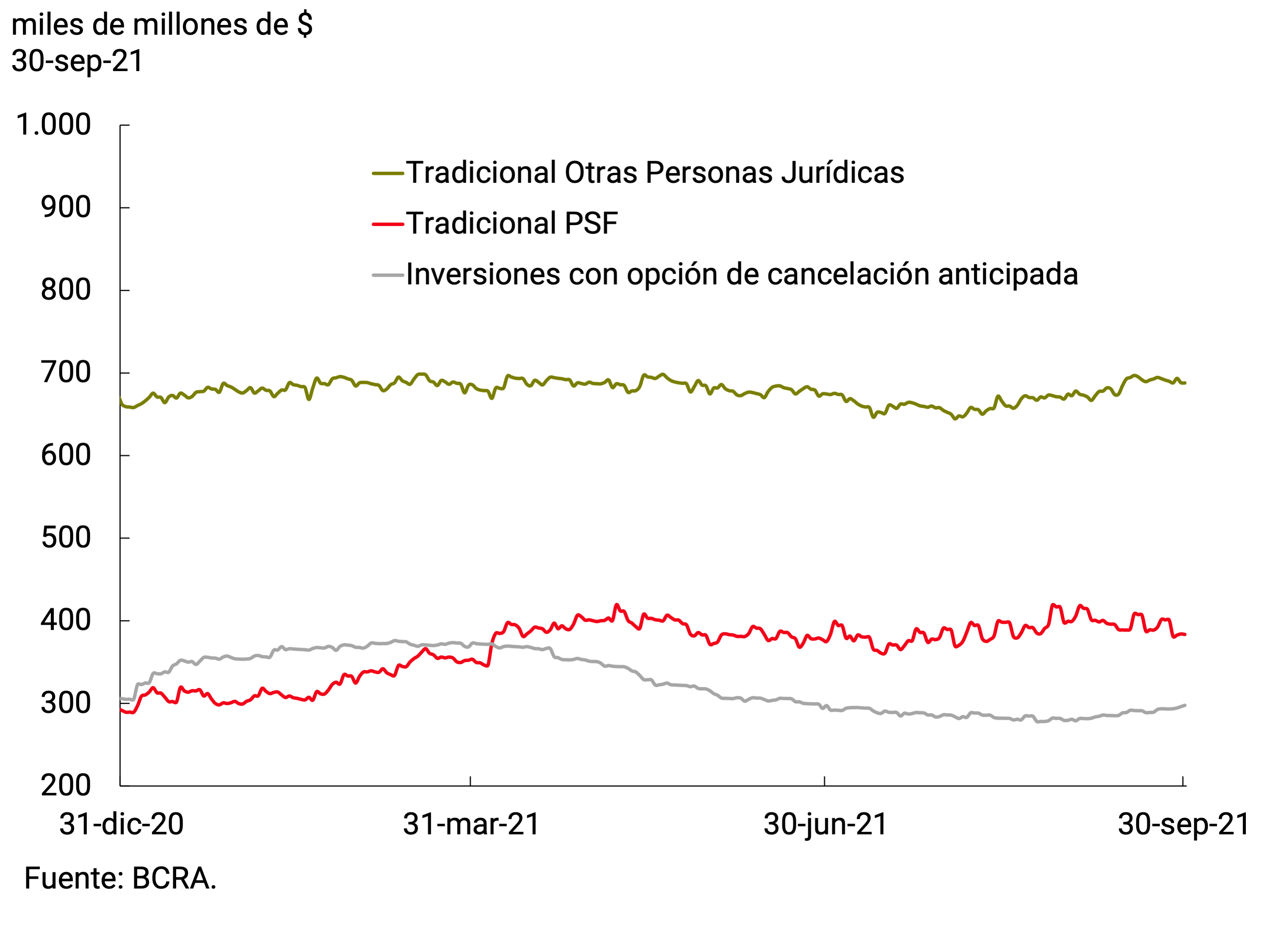

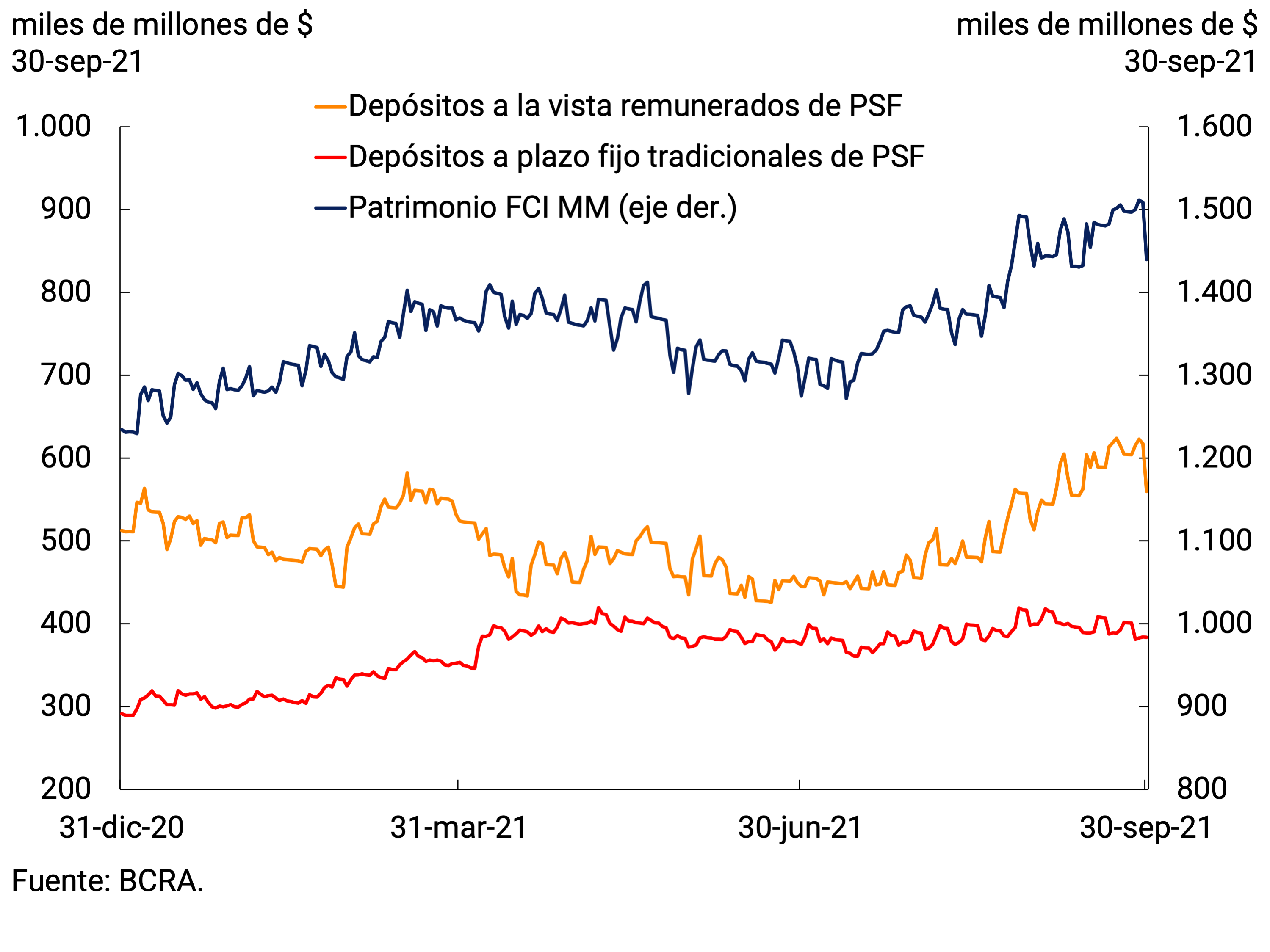

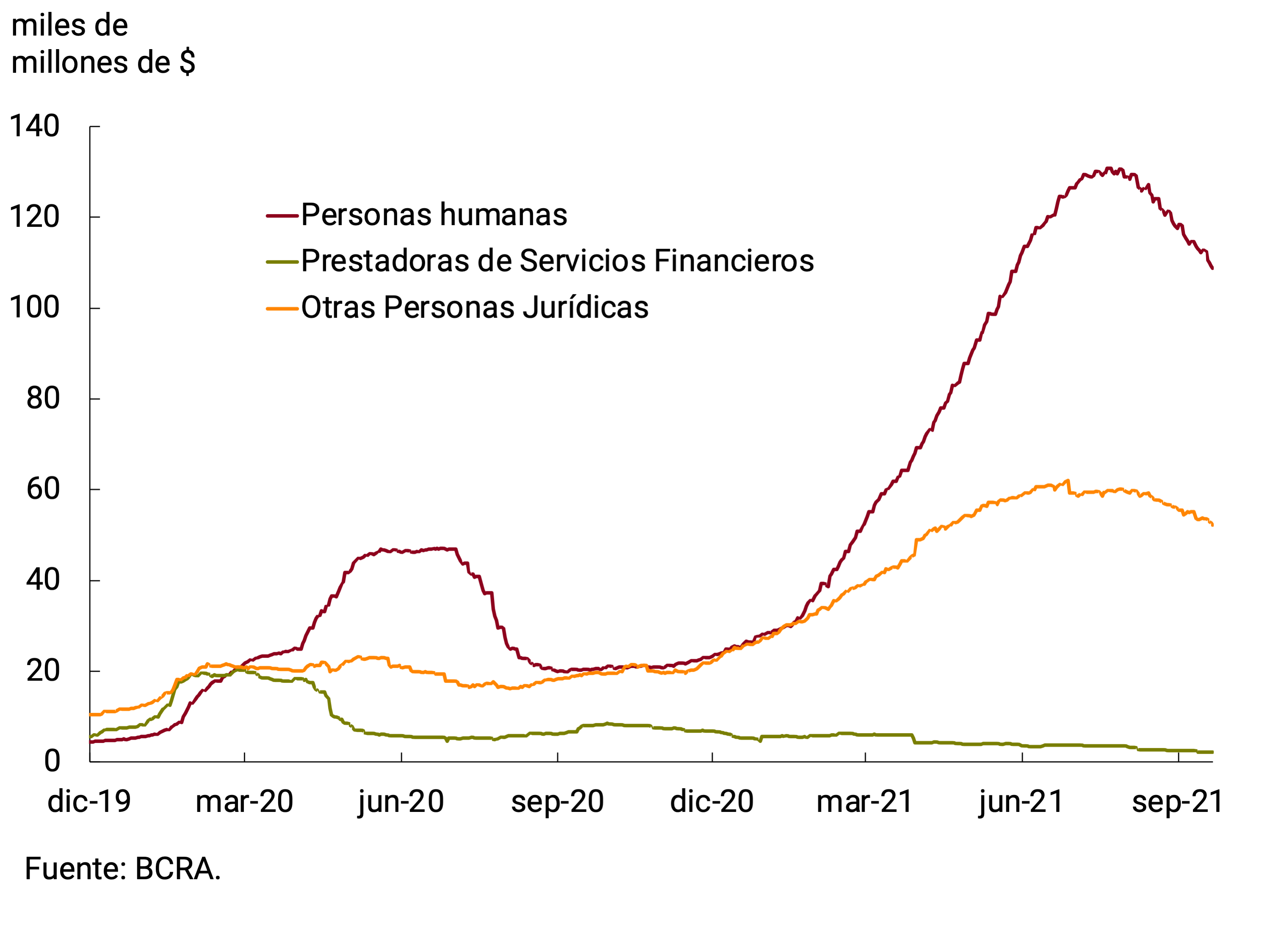

Among the main players in the wholesale segment, companies accounted for most of the growth in traditional term placements. Since the beginning of August, after the period of higher wage expenses and tax payments, this type of depositor showed a sustained increase in its holdings (see Figure 3.3). For their part, Financial Services Providers (FSPs), including Money Market Mutual Funds (FCI MM), exhibited an increase in their assets in real terms throughout the month. This increased availability of funds was mainly allocated to interest-bearing demand deposits, while maintaining their traditional fixed-term placements unchanged (see Figure 3.4). The greater preference for shorter-term assets, as is usual in pre-election periods, was also reflected in the nominal growth presented by investments with early cancellation options, after several months of remaining without major changes. Interest rates relevant to the wholesale segment remained relatively stable. The TM20 of private banks stood at 33.9% n.a. in September (39.8% y.o.y.), around 7 p.p. and 3.5 p.p. above that paid to legal entities for investments with an early cancellation option and the average interest rate on interest-bearing demand deposits, respectively.

Figure 3.3 | Private sector time deposits of more than $20 million by depositor

type Balance at constant prices

Figure 3.4 | Assets of FCI MM and its main investments

Balance at constant prices

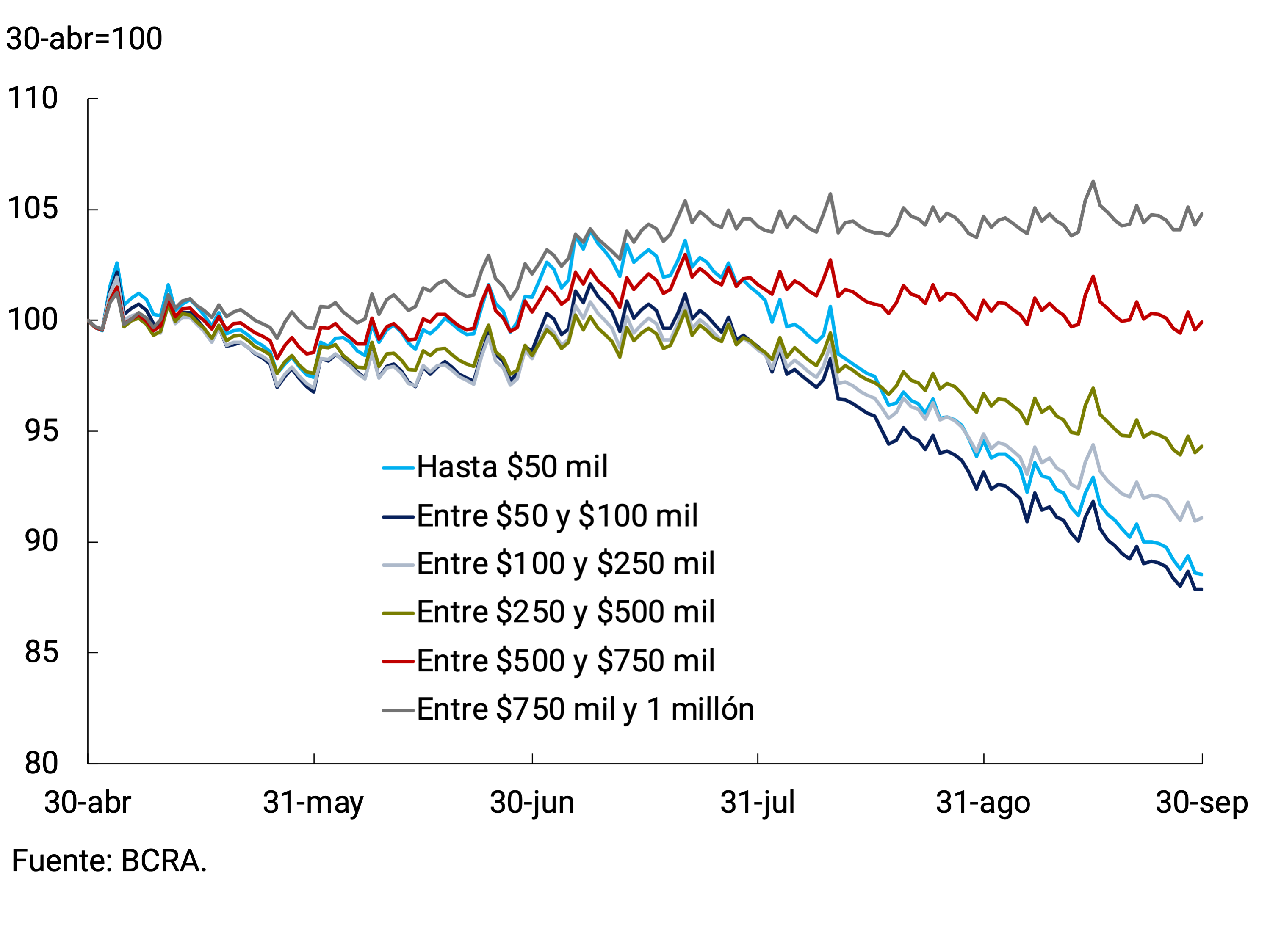

As for deposits of lower strata, placements of between $1 and $20 million at constant prices would have exhibited a slight increase; Meanwhile, deposits of up to $1 million continued with the downward trend once adjusted for price evolution. It should be noted that, within the retail segment, placements of the lowest strata (up to $500,000) are those that show a decrease, while deposits of more than $500,000 remained relatively stable (see Figure 3.5). The interest rate on time deposits of less than $1 million paid to individuals stood at an average of 36.3% n.a. (43.0% e.a.)3.

Deposits denominated in UVA (adjustable by CER) deepened their rate of decline, in a context of moderation in inflation and the fact that this type of deposits involve longer maturities than traditional placements. Thus, the average monthly balance stood at $169,175 million, which would have implied a 9.5% contraction at constant prices. This drop was explained both by traditional placements and by those that have an early cancellation option. The lower dynamism of this type of deposit was reflected in both the holdings of natural and legal persons (see Figure 3.6).

All in all, the broad monetary aggregate (private M3)4 at constant prices would have registered an increase of 1.4% s.e. in September, which would place this expansion among the highest in recent years. In the year-on-year comparison, this aggregate would have presented a contraction of the order of 7%. In terms of Output, it registered a slight acceleration to 18.7%, a record above the average observed between 2010 and 2019.

Figure 3.5 | Time deposits of up to $1 million from the private

sector Index at constant prices

Figure 3.6 | Fixed-term deposits in UVA from the private

sector Balance at current prices

4. Monetary base

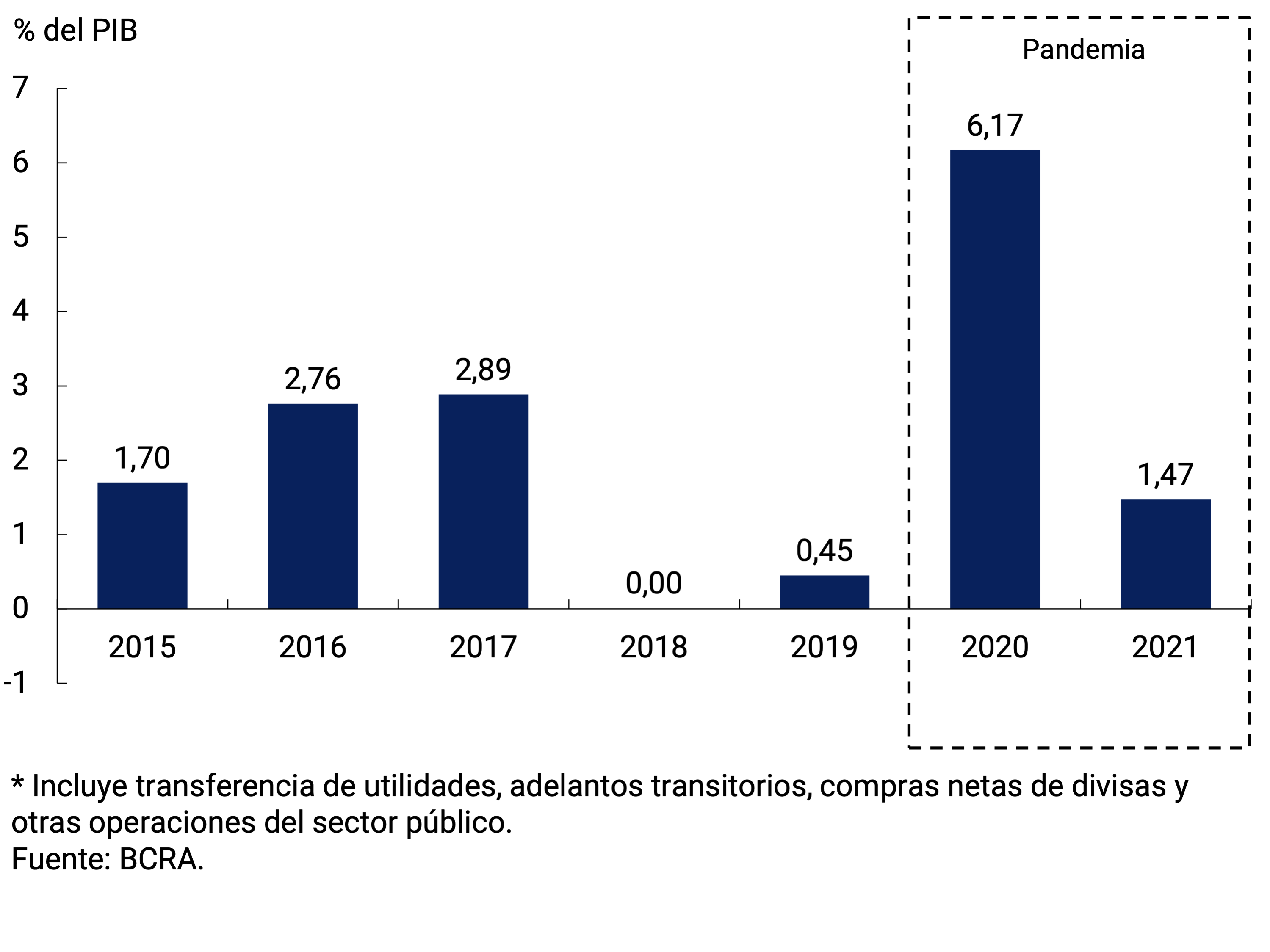

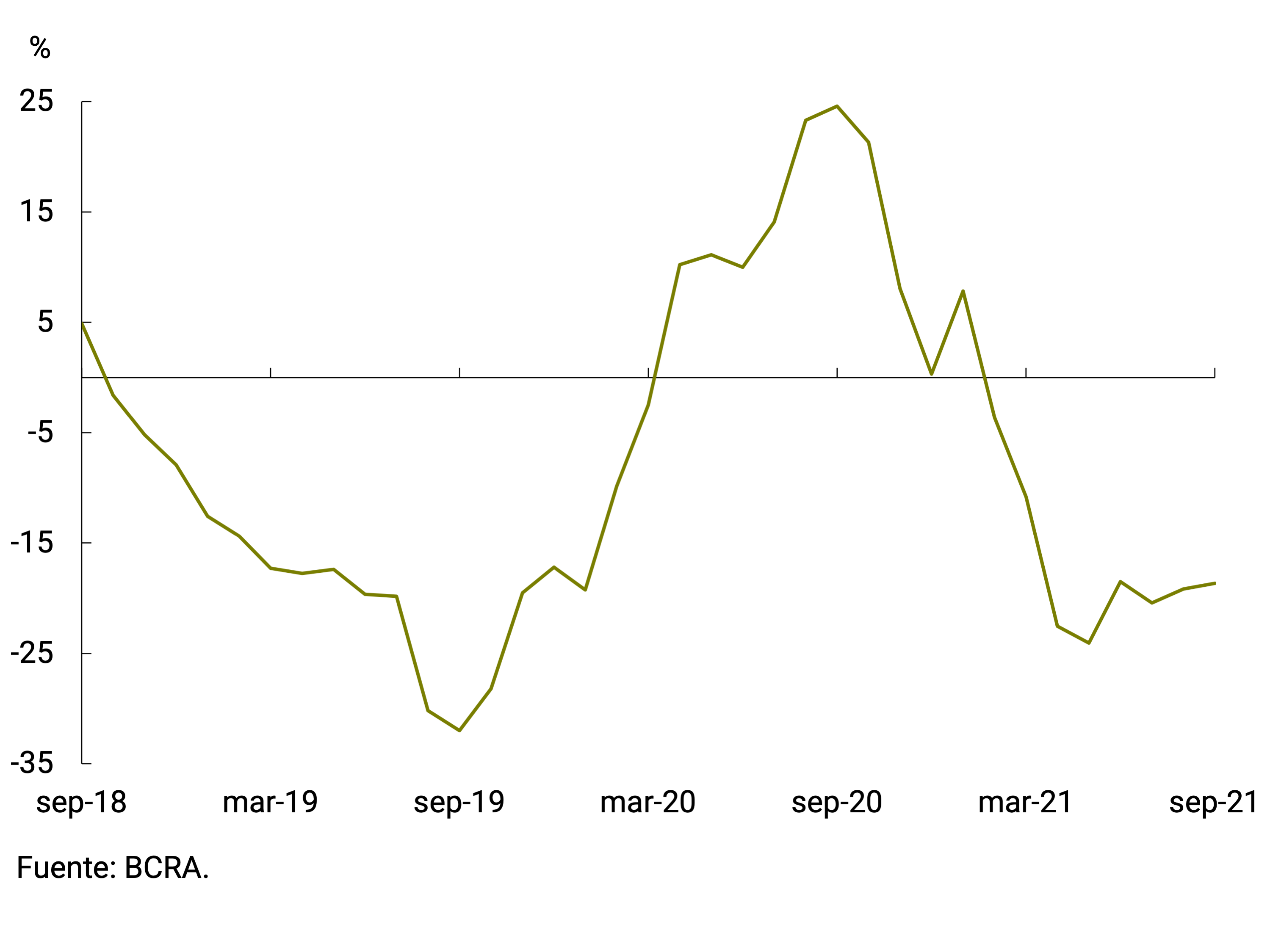

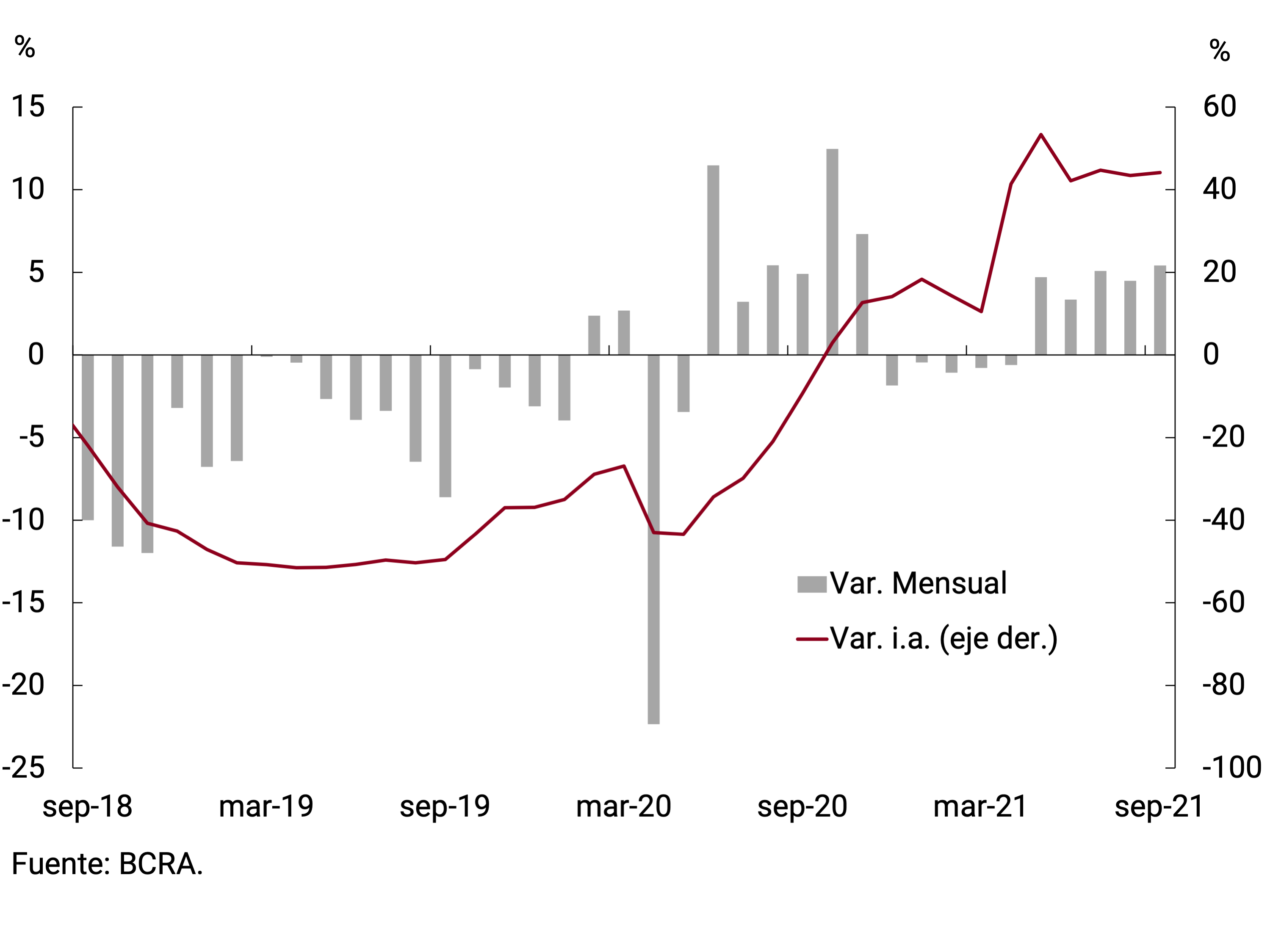

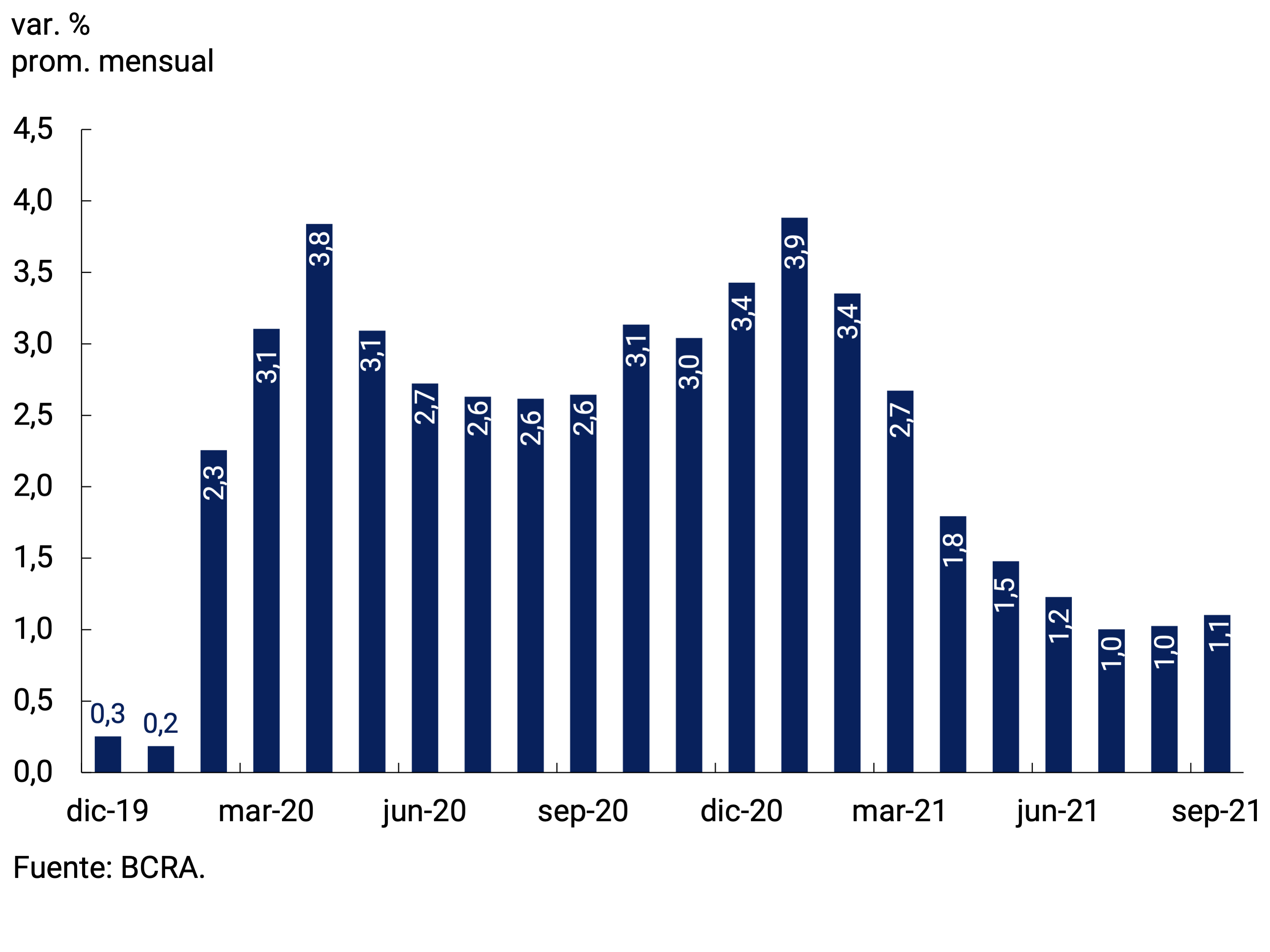

In September, the Monetary Base stood at $2,937 billion, remaining at a level similar to that of the previous month. In fact, the average increase for the month was 0.3% (+$9,444 million). The primary expansion of the public sector was almost entirely offset by the absorption of liquidity associated with the net sale of foreign currency to the private sector and monetary regulation instruments. Thus, the primary issuance of the public sector so far this year was 1.5% of GDP, a markedly lower figure than in the first year of the pandemic and similar to that of 2015 (see Figure 4.1). In year-on-year terms and at constant prices, the Monetary Base stabilized in recent months at around a contraction of around 19% (see Figure 4.2).

Figure 4.1 | Primary expansion of the public sector*

Accumulated to September of each year

Figure 4.2 | Monetary Base

Year-on-year change at constant prices

5. Loans to the private sector

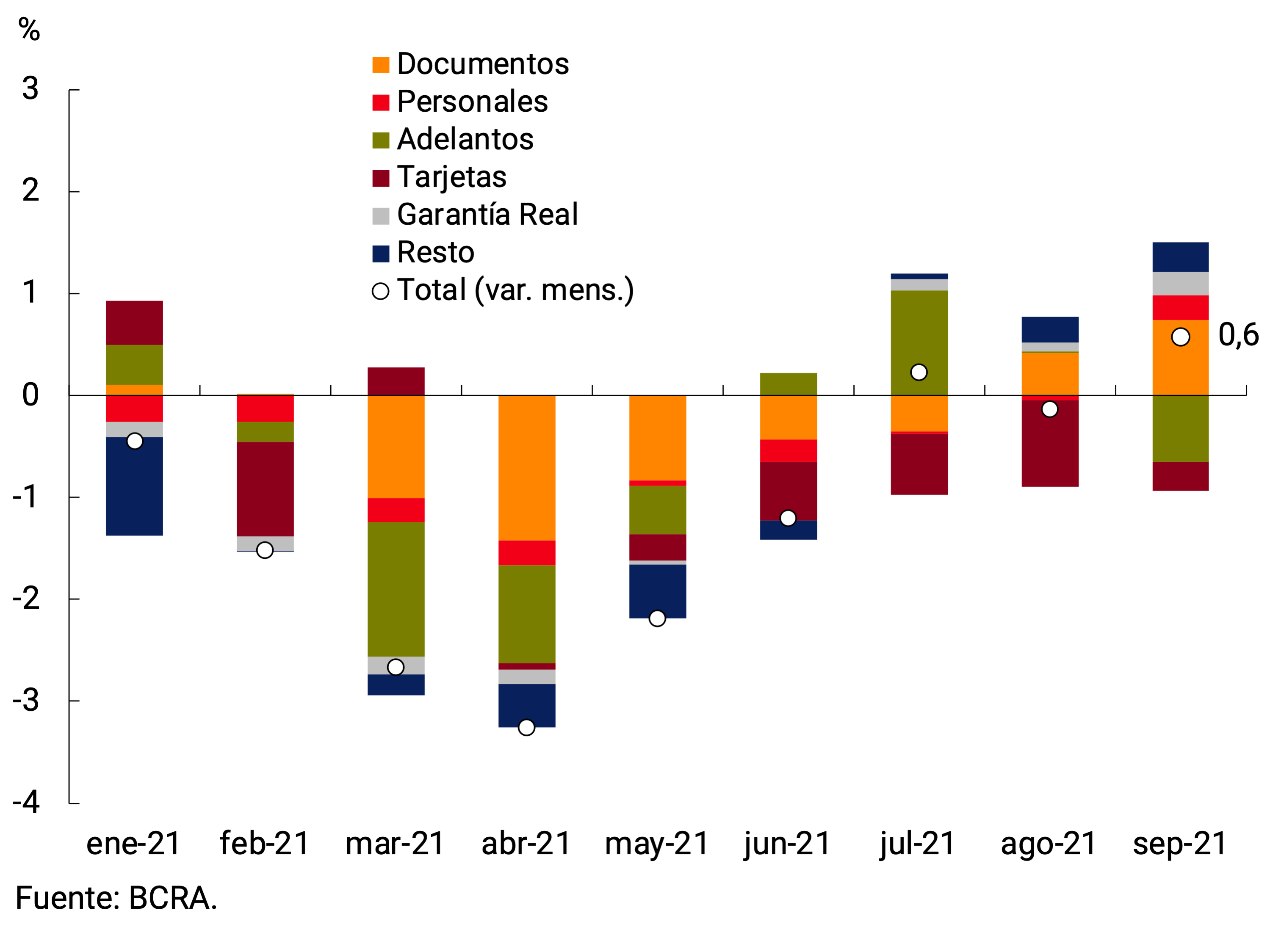

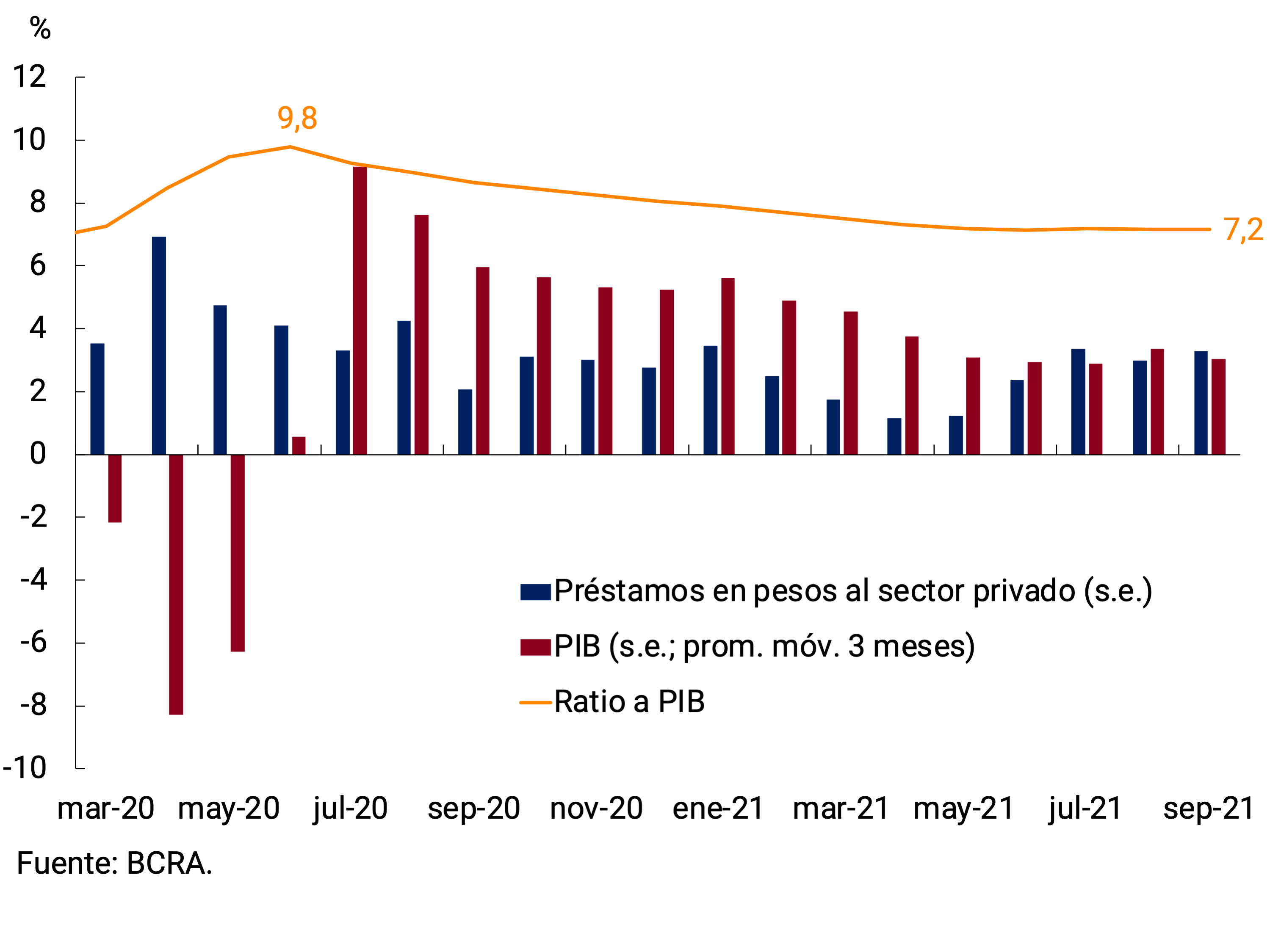

In September, loans in pesos to the private sector would have grown 0.6% monthly, considering the values in real terms and without seasonality. Among the different lines of credit, the impetus came mainly from documents and, to a lesser extent, from collateral and personal loans. The positive contribution of these lines to the monthly variation was partially offset by the behavior of advances and credit card financing (see Figure 5.1). In terms of GDP, loans in pesos to the private sector continued to be around 7% (see Figure 5.2).

Figure 5.1 | Loans in Pesos to the Real Private Sector

without seasonality; contrib. to monthly growth

Figure 5.2 | Loans in pesos to the private sector as a percentage of GDP

Lines with essentially commercial destinations would have exhibited a growth of 0.5% s.e. at constant prices. Within these financings, a heterogeneous behavior was observed. On the one hand, financing granted through current account advances would have presented a monthly drop of 6.4% s.e. at constant prices, after 3 months of positive real variations. Meanwhile, single-signature documents and discounted documents would have registered real increases of 0.8% and 5.4% s.e., respectively (see Chart 5.3). The great dynamism of documentary loans is associated with the Financing Line for Productive Investment (LFIP) for MSMEs. In September, the average interest rate applied to the discount of documents was 30.7% n.a. and that of single-signature documents was 35.1% n.a., figures consistent with the LFIP interest rates for both working capital and investment projects. When analyzing the composition of commercial credit by type of debtor, we observe that financing to MSMEs would have expanded by 4.5% in September at constant prices, with an average monthly increase in the quarter of around 2.1% (see Figure 5.4).

Figure 5.3 | Discounted documents without seasonality

Var. at constant prices

Figure 5.4 | Commercial loans to the private sector by type of debtor

Current price balance

At the end of September, loans granted under the LFIP accumulated disbursements of approximately $1,040 billion since its implementation, which implies a growth of 14.3% compared to the end of August. As for the destinations of these funds, about 84% of the total disbursed corresponds to the financing of working capital and the rest to the line that finances investment projects (see Figure 5.5). At the time of publication, the number of companies that accessed the LFIP amounted to 160,000. It should be noted that in September the BCRA decided to extend the validity of the LFIP until the end of March 20225, maintaining the quota of 7.5% of deposits in pesos of the non-financial private sector in pesos6 for Group A entities and 25% of said quota for public sector financial agents that do not belong to Group A. The new line provides special treatment for the gastronomy, hotel, cultural and leisure services sectors, which can access the working capital line with an interest rate of 35% and a grace period of 6 months to start paying the loan. For the purposes of meeting the quota, these financings will be computed at 120% of their value. In addition, eligible financing included those granted to small companies with agricultural activity as long as the funds are intended to increase the productive capacity of beef and/or bovine milk. Thus, small agricultural producers will be able to access the financing line for investment and working capital projects with interest rates of 30% and 35%, respectively7.

With respect to consumer-related loans, credit card financing would have exhibited a monthly drop of 0.9% s.e. in real terms. However, in the last days of September they presented greater dynamism, due to the relaunch of the line of credit at rate 0 for single-payers8, which accumulated disbursements of $10,100 million in the month. On the other hand, personal loans would have registered a monthly growth of 1.4% s.e. at constant prices, ending a streak of more than 3 years of negative real variations. The interest rate corresponding to personal loans showed a slight increase (0.5 p.p.) in the average of September and stood at 53.6% n.a.

With regard to secured lines, collateral loans continued to stand out with sustained growth in real terms. Thus, in September the monthly growth rate at constant prices would have been 4.9% s.e., accumulating an expansion of 33% in the last twelve months (see Figure 5.6). For its part, the balance of mortgage loans would have presented a monthly fall of 0.3% in real terms without seasonality, standing 24.3% below the record of the same month of the previous year.

Figure 5.5 | Financing granted through the Productive Investment Financing Line (LFIP)

Accumulated disbursed amounts; data at the end of the month

Figure 5.6 | Title loans without seasonality

Var. at constant prices

6. Liquidity in pesos of financial institutions

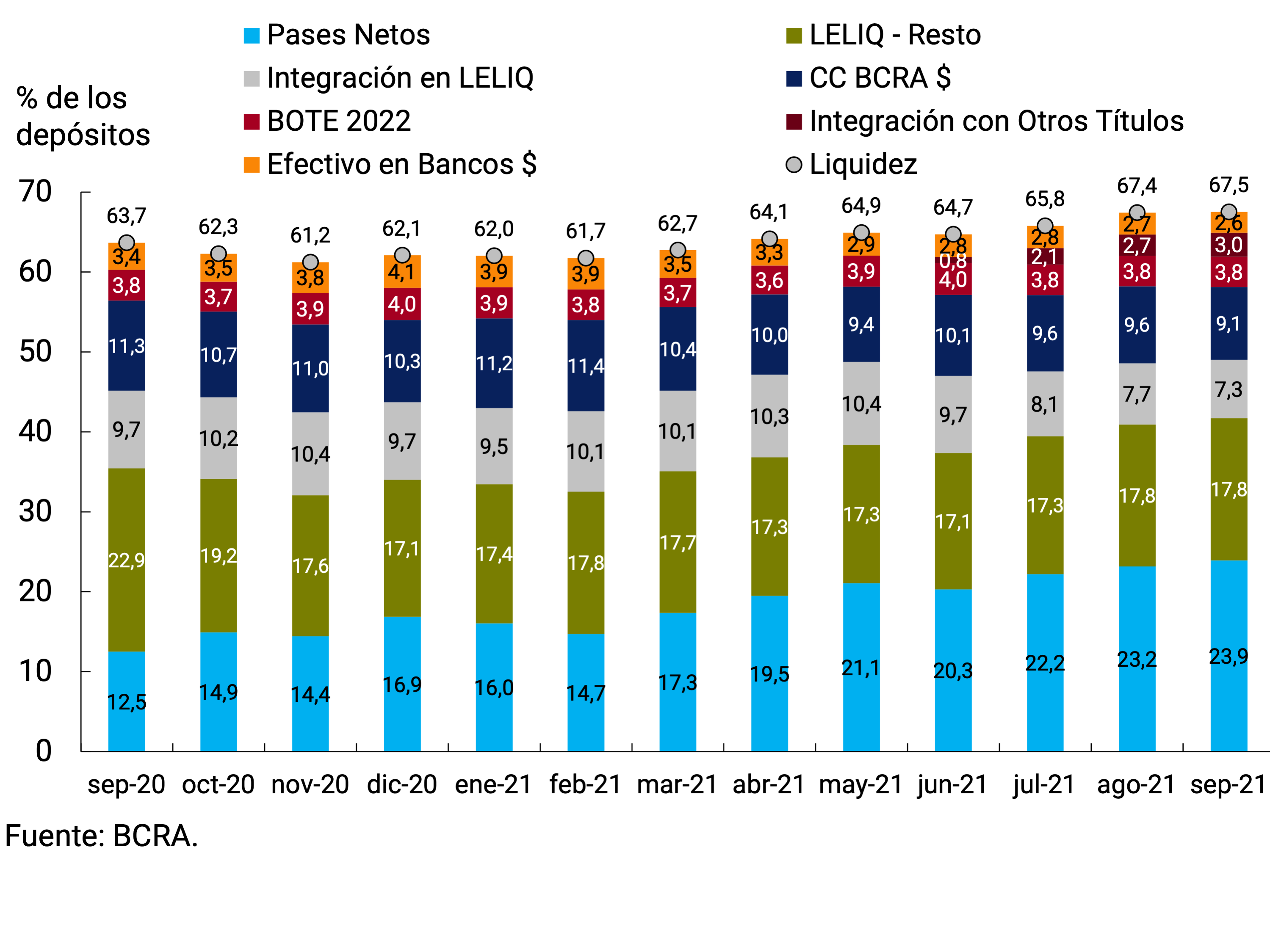

Ample bank liquidity in local currency9 remained broadly unchanged in September, averaging 67.5% of deposits. Thus, it remained at historically high levels (see Figure 6.1). As for its components, the growth in the integration of minimum cash with public securities stands out, which went from 2.7% of deposits in August to 3% in September. On the other hand, a decrease in integration with LELIQ was observed. There was also an increase in net passes and a fall in current accounts at the BCRA. On the other hand, cash in banks remained without significant changes at an average of 2.6% of deposits.

From the regulatory point of view, it is worth mentioning that in September the increase in the maximum deduction for financing granted within the framework of the “Ahora 12” Program came into force, which went from 6% to 8% of deposits10. In turn, this month also came into force the deduction of minimum cash for the equivalent of 60% of the financing agreed through the line of credit at a 0% rate to single-tax persons11.

Figure 6.1 | Liquidity in pesos of financial institutions

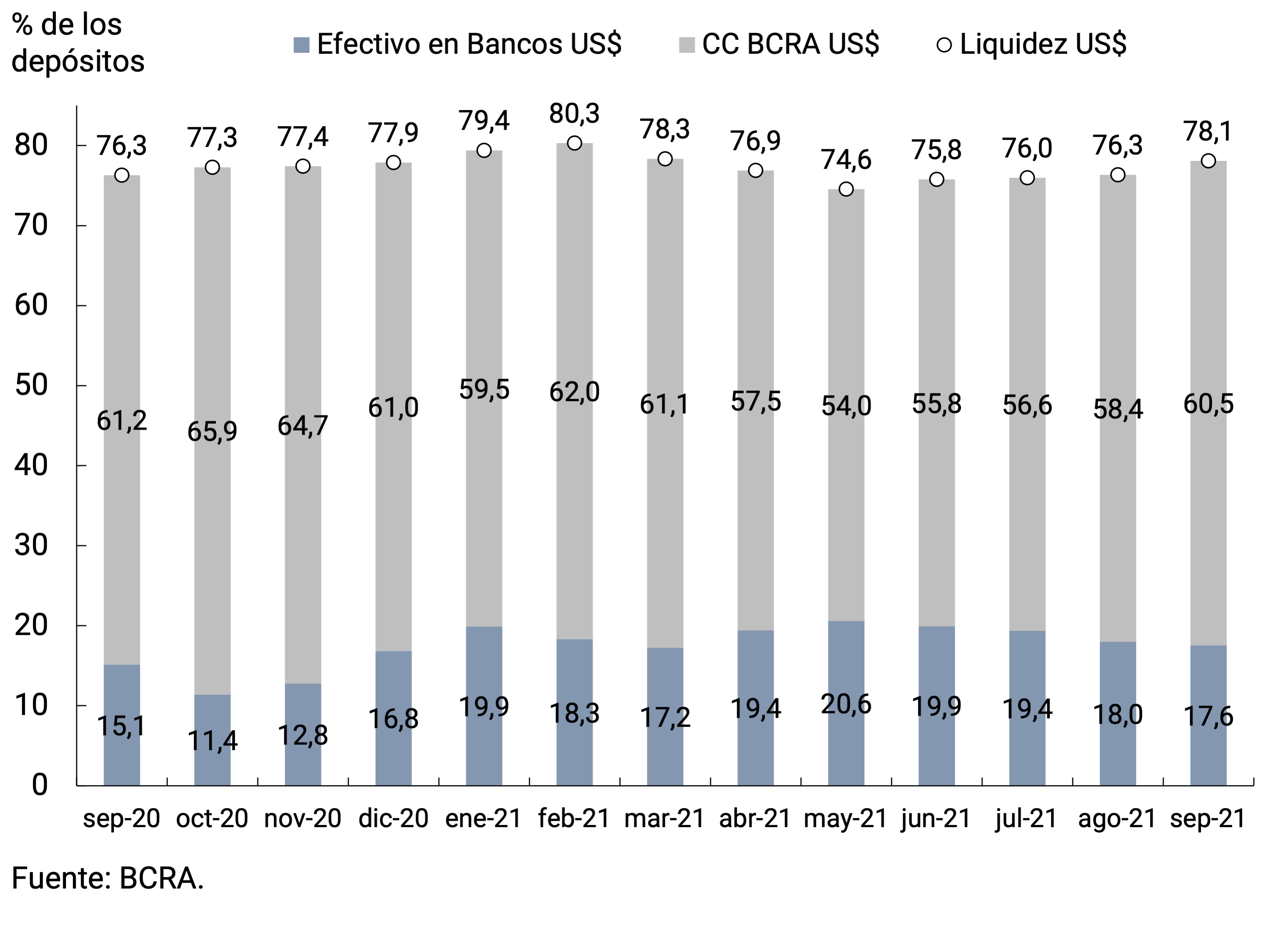

7. Foreign currency

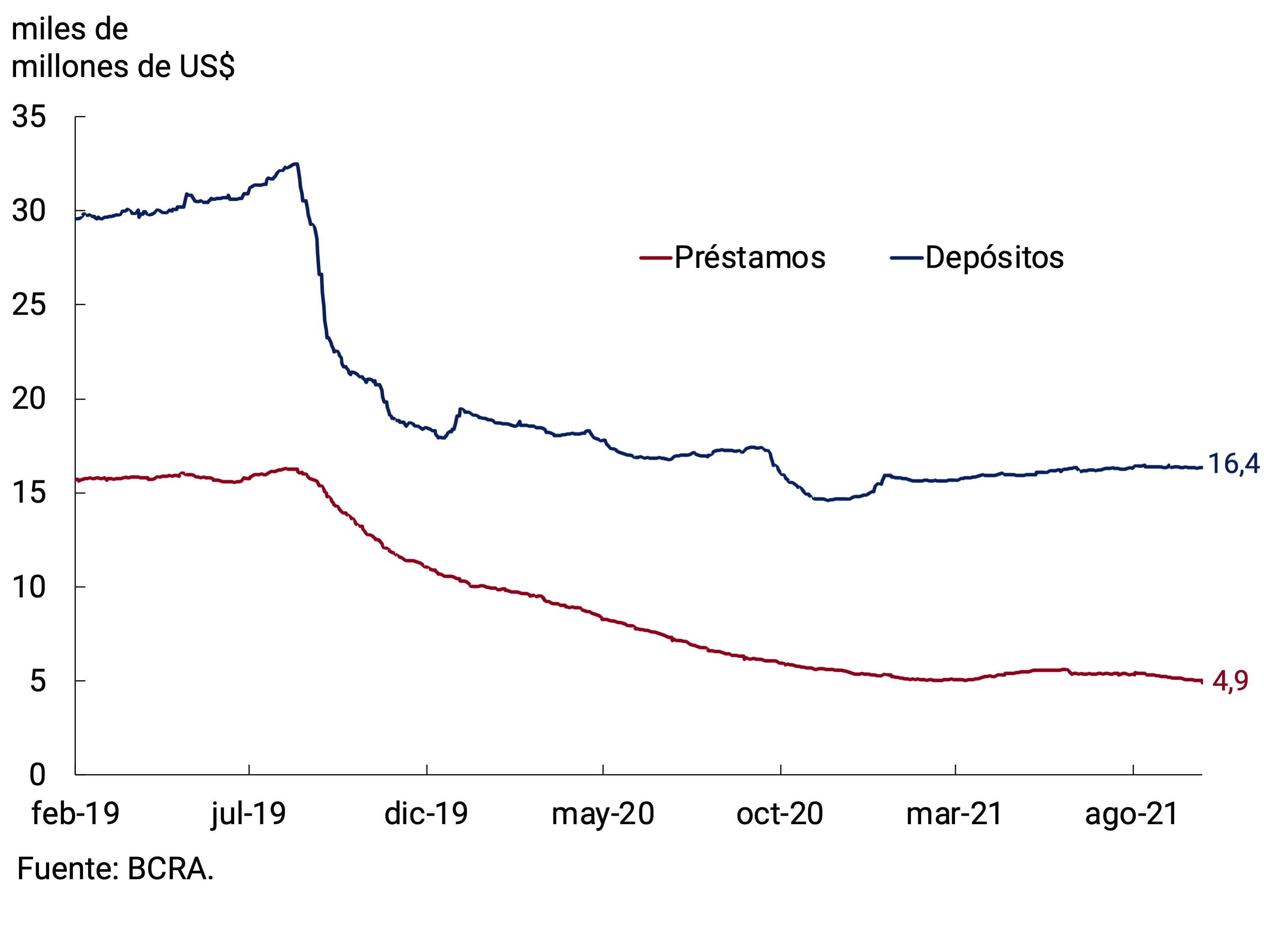

In the foreign currency segment, private sector deposits registered little significant variations, while loans showed a downward trend throughout the month. In fact, the average monthly balance of deposits reached US$16,348 million, standing just US$39 million below the balance of August. Meanwhile, credit in foreign currency to the private sector registered a monthly contraction of US$228 million in September, with the average monthly balance standing at US$5,081 million. The fall was concentrated in financing instrumented through signature documents (see Figure 7.1).

In this context, bank liquidity in foreign currency registered an increase of 1.8 p.p. in the month and averaged 78.1% of deposits. This liquidity dynamic was explained by the increase in current accounts at the BCRA, which was partially offset by a fall in cash in banks, similar to what occurred in previous months (see Figure 7.2).

With regard to regulatory modifications, and in accordance with the special phytosanitary protocol that sales to China must satisfy, it was decided to increase from 15 to 30 days the deadline for the settlement of foreign currency generated in the export of barley and sorghum to that country. In turn, local financial institutions were allowed to access the foreign exchange market to meet their obligations to non-residents for financial guarantees granted as of October12.

Figure 7.1 | Balance of private sector foreign currency deposits and loans

Figure 7.2 | Liquidity in foreign currency of financial institutions

After nine consecutive months of positive variations, the BCRA’s International Reserves reflected a fall of US$3,269 million compared to the end of August. Thus, they ended the month with a balance of US$42,911 million (see Figure 7.3). This dynamic was influenced by the payment made to the IMF in mid-September for around US$1,900 million. The net sale of foreign currency to the private sector for around US$957 million also had an impact.

Finally, the bilateral nominal exchange rate against the U.S. dollar increased 1.1% in September, a slightly higher rate of expansion than in the previous two months, standing at $98.28/US$ on average for the month (see Figure 7.4). The slower rate of depreciation of the domestic currency in recent months seeks to contribute to the disinflation process.

Figure 7.3 | International

reserves Daily balance

Figure 7.4 | Variation in the bilateral nominal exchange rate with the United States

Glossary

ANSES: National Social Security Administration.

BADLAR: Interest rate on fixed-term deposits for amounts greater than one million pesos and a term of 30 to 35 days.

BCRA: Central Bank of the Argentine Republic.

BM: Monetary Base, includes monetary circulation plus deposits in pesos in current account at the BCRA.

CC BCRA: Current account deposits at the BCRA.

CER: Reference Stabilization Coefficient.

NVC: National Securities Commission.

SDR: Special Drawing Rights.

EFNB: Non-Banking Financial Institutions.

EM: Minimum Cash.

FCI: Common Investment Fund.

A.I.: Year-on-year .

IAMC: Argentine Institute of Capital Markets

CPI: Consumer Price Index.

ITCNM: Multilateral Nominal Exchange Rate Index

ITCRM: Multilateral Real Exchange Rate Index

LEBAC: Central Bank bills.

LELIQ: Liquidity Bills of the BCRA.

LFIP: Financing Line for Productive Investment.

M2 Total: Means of payment, which includes working capital held by the public, cancelling cheques in pesos and demand deposits in pesos from the public and non-financial private sector.

Private M2: Means of payment, includes working capital held by the public, cancelling cheques in pesos and demand deposits in pesos from the non-financial private sector.

Private transactional M2: Means of payment, includes working capital held by the public, cancelling cheques in pesos and non-remunerated demand deposits in pesos from the non-financial private sector.

M3 Total: Broad aggregate in pesos, includes the current currency held by the public, cancelling checks in pesos and the total deposits in pesos of the public and non-financial private sector.

Private M3: Broad aggregate in pesos, includes the working capital held by the public, cancelling checks in pesos and the total deposits in pesos of the non-financial private sector.

MERVAL: Buenos Aires Stock Market.

MM: Money Market.

N.A.: Annual nominal

E.A.: Annual Effective

NOCOM: Cash Clearing Notes.

ON: Negotiable Obligation.

GDP: Gross Domestic Product.

P.B.: Basic points.

P.P.: Percentage points.

MSMEs: Micro, Small and Medium Enterprises.

ROFEX: Rosario Term Market.

S.E.: No seasonality

SISCEN: Centralized System of Information Requirements of the BCRA.

TCN: Nominal Exchange Rate

IRR: Internal Rate of Return.

TM20: Interest rate on fixed-term deposits for amounts greater than 20 million pesos and a term of 30 to 35 days.

TNA: Annual Nominal Rate.

UVA: Unit of Purchasing Value

References

1 INDEC will release September’s inflation data on October 14.

2 M2 private excluding interest-bearing demand deposits from companies and financial service providers. This component was excluded since it is more similar to a savings instrument than to a means of payment.

3 It should be noted that the average interest rate observed is slightly below the minimum guaranteed interest rate, because it includes deposits of up to $1 million of individuals who, in total, exceed one million pesos in the financial institution.

4 Includes the working capital held by the public and the deposits in pesos of the non-financial private sector (sight, term and others).

5 See section Regulatory Summary (Com. A7369).

6 Calculated on the average of private sector deposits for the month of September.

7 See section Regulatory Summary (Com. A7373).

8 See IMM of August 2021.

9 Includes current accounts at the BCRA, cash in banks, balances of passes arranged with the BCRA, holdings of LELIQ, and bonds eligible for reserve requirements.

10 Communication A7334. See Regulatory Summary Section of the August Monthly Monetary Report.

11 Communication A7342. See Regulatory Summary Section of the August Monthly Monetary Report.

12 See section Regulatory Summary (Com. A7374).

Share on