1. Executive Summary

In a scenario of high uncertainty, typical of electoral periods, throughout October economic agents chose to position themselves in liquid assets. Thus, means of payment registered an increase at constant prices and without seasonality, interrupting the downward trend observed throughout the year. Interest-bearing demand deposits also registered an increase, both from Financial Services Providers and from the rest of the companies. The flip side of this increase was the contraction of fixed-term deposits. All in all, the broad monetary aggregate (private M3) on a monthly average at constant prices and without seasonality would have registered a monthly contraction of 2.1% in October.

In mid-October, the BCRA raised the monetary policy interest rate (LELIQ 28 days) by 15 percentage points (p.p.), bringing it to 133% n.a. (254.8% y.a.). It also raised interest rates on the rest of the monetary regulation instruments and minimum interest rates on fixed-term deposits. With this increase, the aim was to tend towards positive real returns on term placements in local currency, in order to sustain their demand, which had begun to show a downward trend.

Finally, commercial loans in pesos to the private sector grew in real terms and without seasonality in October, a dynamic that was partially offset by the contraction of the remaining lines of credit. However, the loan balance registered an increase after two months of sharp declines.

2. Payment methods

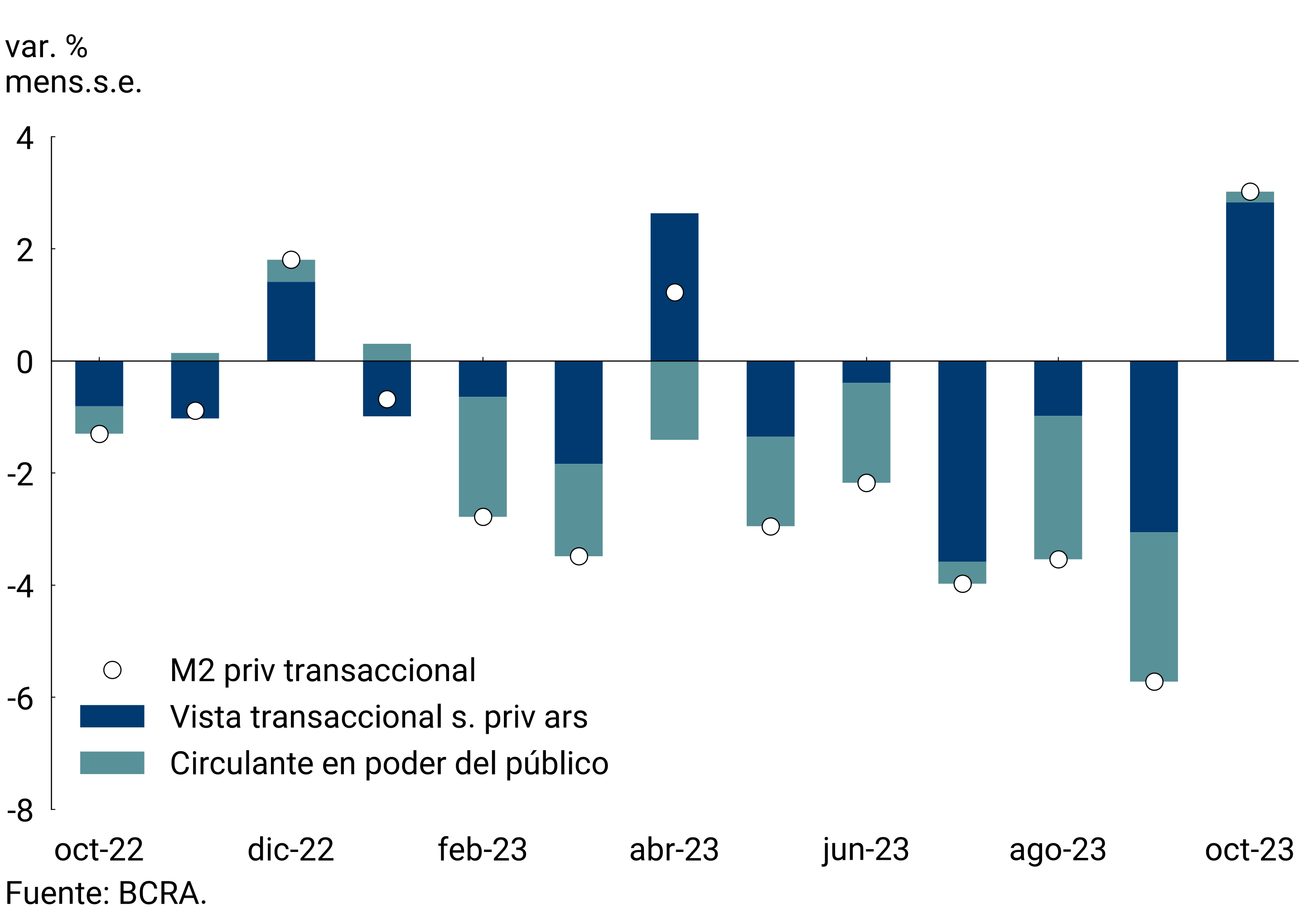

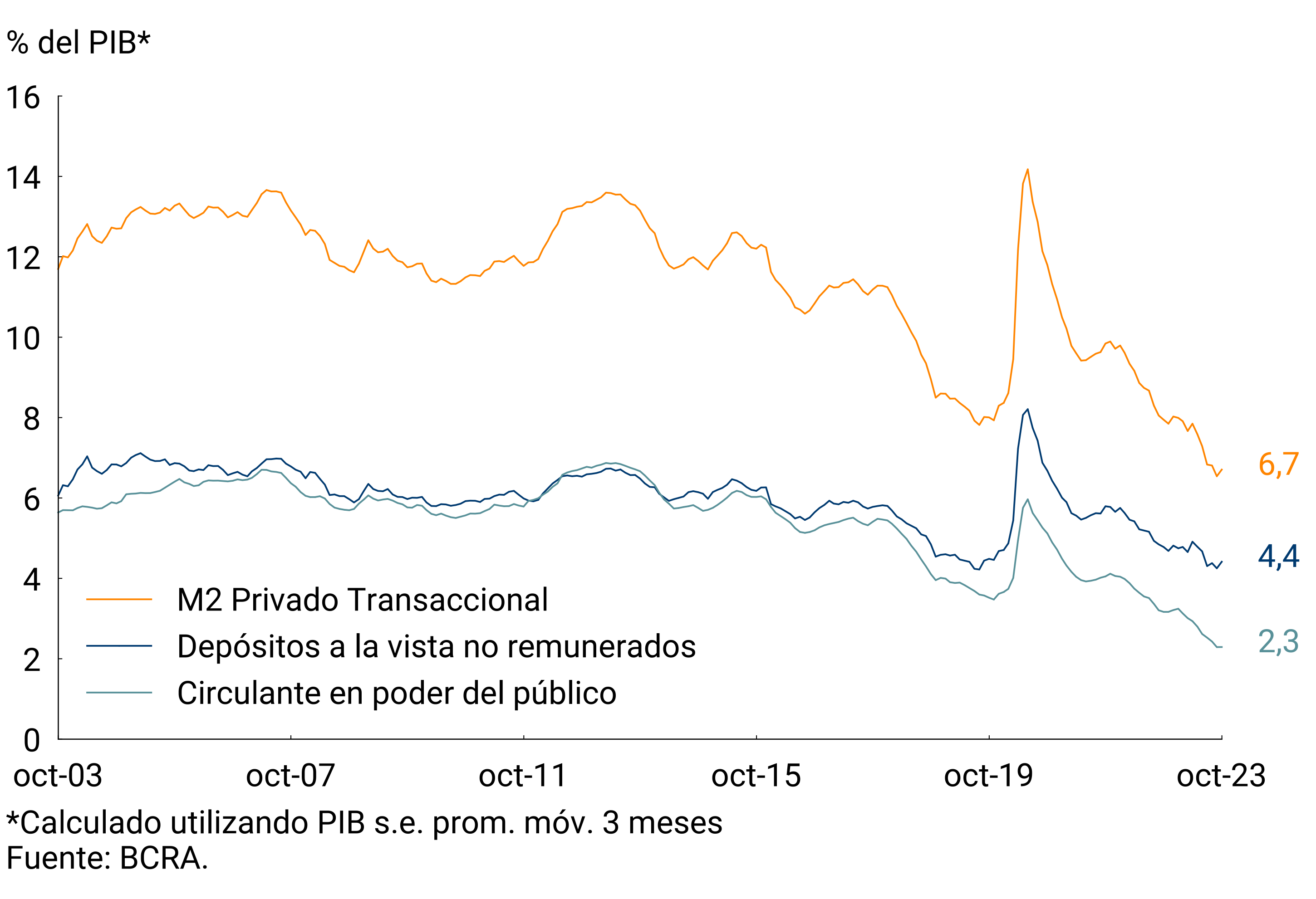

In a scenario of high uncertainty, typical of electoral periods, throughout October economic agents chose to position themselves in liquid assets. In real and seasonally adjusted terms (s.e.), means of payment (private transactional M21) would have registered an expansion of 3.0% in the month, thus interrupting the downward trend observed in recent months. At the component level, the increase was mainly explained by the performance of non-interest-bearing demand deposits and, to a lesser extent, by the expansion of working capital held by the public (see Figure 2.1). However, private transactional M2 would have registered a year-on-year contraction of 18.8% in real terms. In terms of Output, means of payment would have stood at 6.7%, showing an increase of 0.2 p.p. compared to the previous month (see Chart 2.2). Beyond the slight recovery observed in October, both the total and its components were around their lowest values in the last 20 years in terms of Output.

Figure 2.1 | Private transactional M2 at constant

prices Contribution by component to the monthly vari. s.e.

Figure 2.2 | Private transactional M2 as % of GDP

3. Savings instruments in pesos

In line with the readjustment of interest rates on monetary policy instruments, the Board of Directors of the BCRA decided to increase the minimum guaranteed rates on fixed-term deposits in the tenth month of year2. In this way, the aim was to maintain the incentive to save in domestic currency and contribute to financial and exchange rate balance. Specifically, the monetary authority raised the minimum guaranteed interest rate for placements by individuals from 118% n.a. to 133% n.a., which is equivalent to an effective monthly yield of 10.9%. Meanwhile, for the rest of the depositors in the financial system, the minimum guaranteed interest rate rose from 111% n.a. to 126% n.a., with the effective monthly interest standing at 10.4%3.

The rise in the interest rate on time deposits occurred in a context of a fall in the balances of these instruments in pesos of the private sector, both in real and nominal terms. This dismantling of positions fueled the increase in means of payment in the month. After the rate hike, the trend was partially reversed. All in all, fixed-term placements would have experienced a contraction of 12.5% s.e. at constant prices in October, and thus would accumulate a fall of around 27% in the year. Thus, the balance of this type of instrument at constant prices was reduced to a record similar to that observed between 2010 and 2019. In the same sense, as a percentage of GDP they would have stood at 5.8% in October, implying a decrease of 0.9 p.p. compared to September.

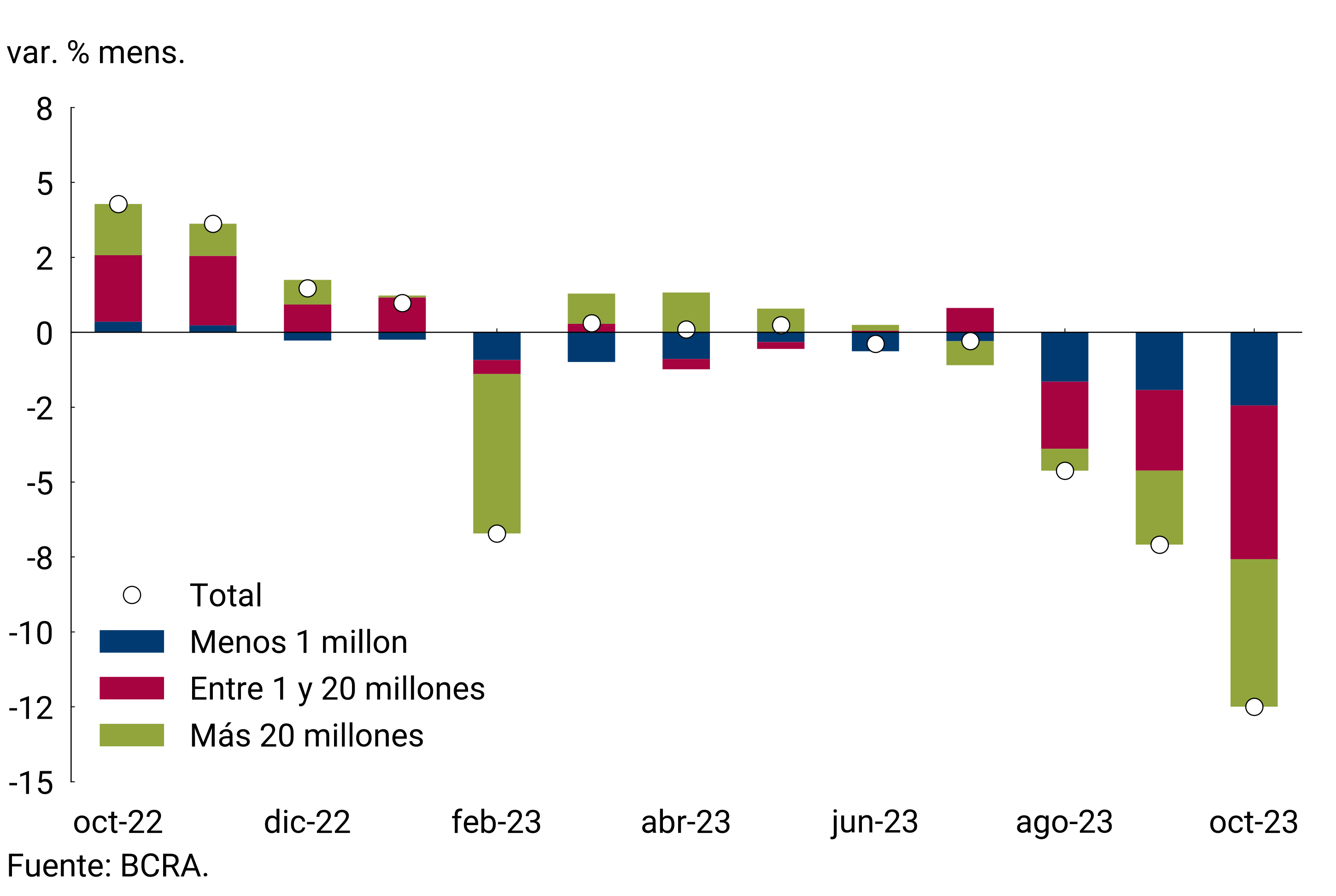

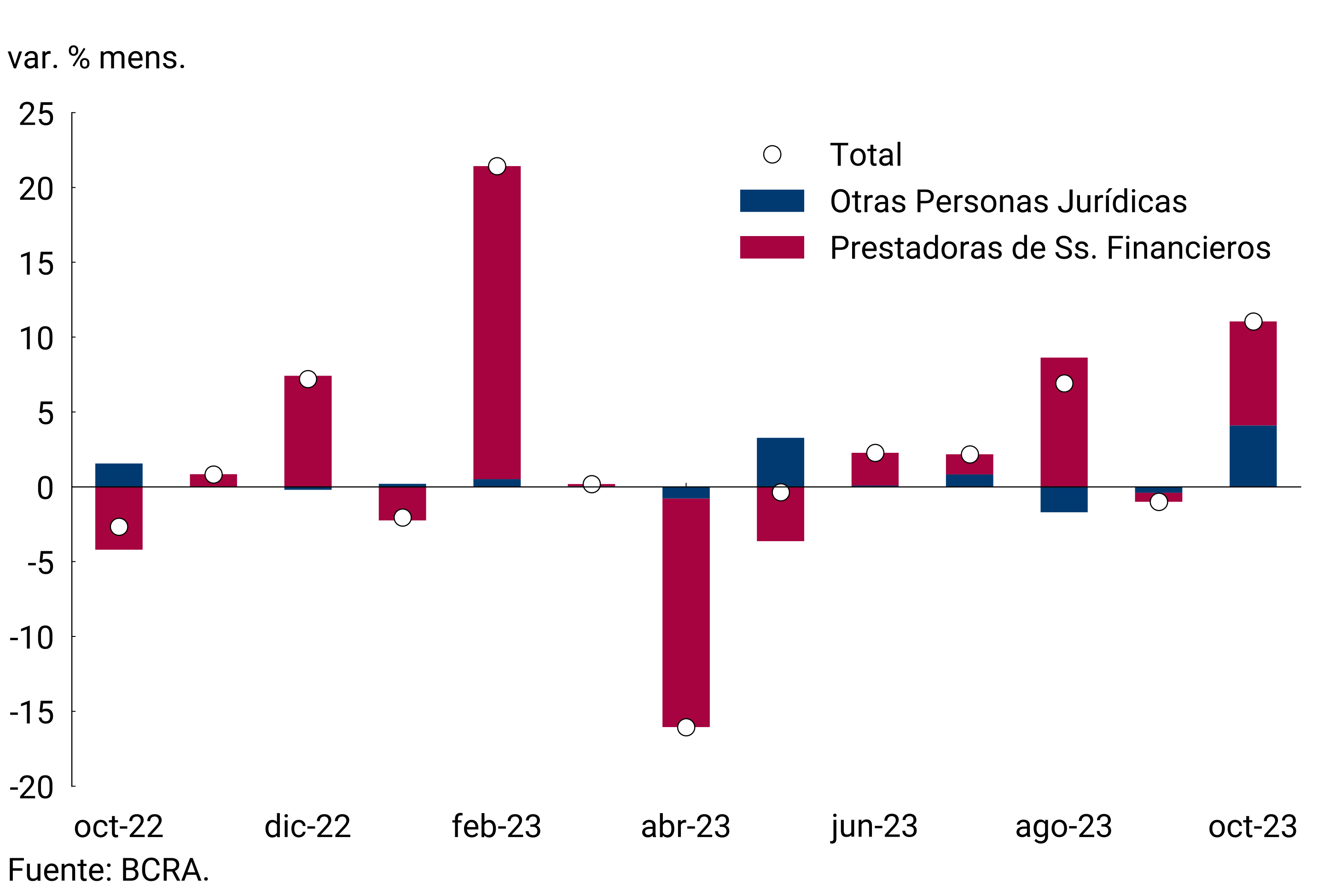

Analyzing the evolution at constant prices of term placements by strata of amount, there is a generalized decrease in all segments in the month (see Figure 3.1). The retail segment was the one that registered the steepest drop, followed by the stratum of $1 to $20 million, with variations in real terms of -18.0% s.e. and -12.8% s.e., respectively. The drop in deposits of more than $20 million was 10.7% s.e. and was mainly explained by the lower traditional fixed-term holdings of Financial Services Providers (FSPs) and, to a lesser extent, of the rest of the companies. The counterpart of this behavior was an increase in interest-bearing demand deposits, which on average expanded by 11% at constant prices and without seasonality (see Figure 3.2). The Money Market Mutual Funds (MM FCI), the main agents within the PSF, also channeled part of the liquidity from the redemption of time deposits to passive passes with the BCRA.

Figure 3.1 | Time deposits in pesos in the private

sector Contribution to the real monthly var. by amount stratum

Figure 3.2 | Interest-bearing

demand deposits Contribution to the actual monthly var. per holder

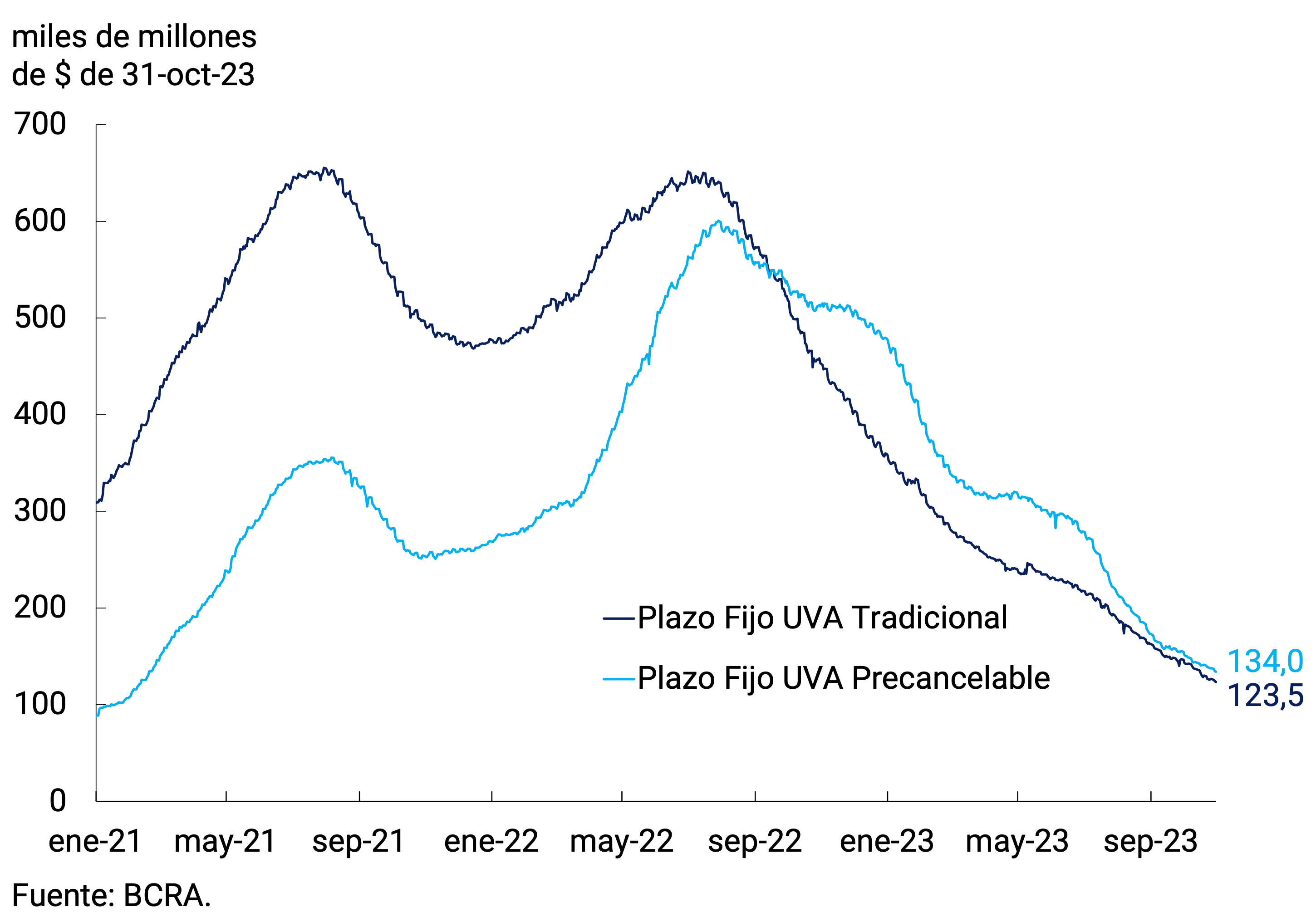

The segment of fixed-term deposits adjustable by CER continued to show a real contraction, accumulating 15 consecutive months of decline. The decrease was verified in both traditional and pre-cancellable UVA placements, whose monthly rates of change were -11.2% s.e. and -10.7% s.e. respectively (see Figure 3.3). Distinguishing by type of holder, the decrease was mainly due to the dynamics of placements by individuals, which represent approximately 69% of the total. All in all, the balance of UVA deposits reached $257,467 million at the end of October, which is equivalent to 1.9% of the total of term instruments denominated in domestic currency. On the other hand, deposits adjusted for the value of the reference exchange rate remained relatively stable on average in the tenth month of the year (see Figure 3.4).

Figure 3.3 | Fixed-term deposits in UVA of the private

sector Balance at constant prices by type of instrument

Figure 3.4 | Deposits adjustable by exchange

rate Balance at current prices

All in all, the broad monetary aggregate, private M34, at constant prices and adjusted for seasonality, would have exhibited a monthly fall of 2.1% in October. In the year-on-year comparison, this aggregate would have registered a decrease of 15.5% and as a percentage of GDP it would have stood at 15.1%, 0.4 p.p. below the previous month’s record.

4. Monetary base

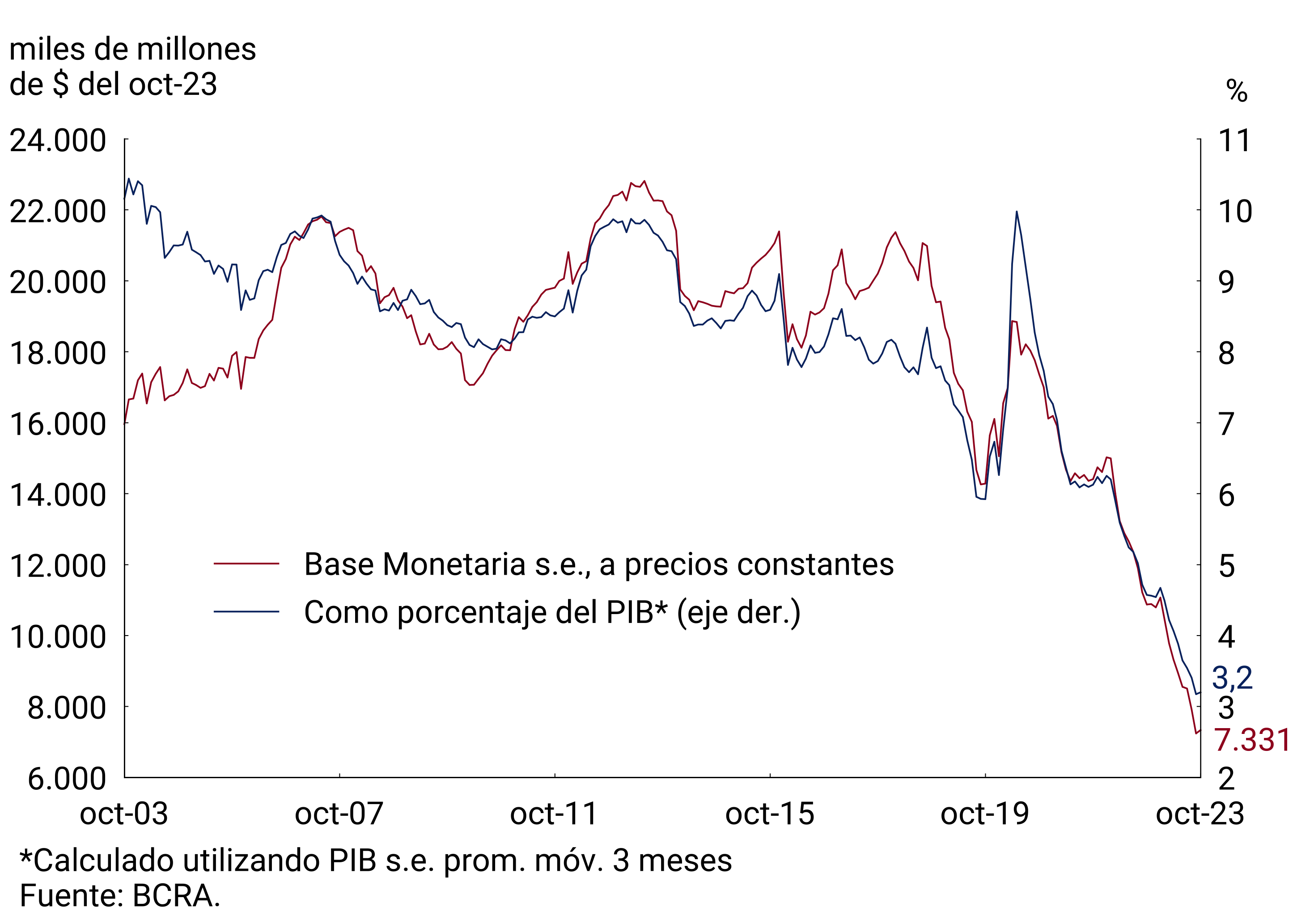

In October, the average balance of the Monetary Base was $7,203 billion, which implied a monthly expansion of 10.2% ($670 billion) at current prices. However, adjusted for seasonality and at constant prices, it would have exhibited an expansion of 1.3%, accumulating a fall of 32.6% in the last twelve months. As a GDP ratio, the Monetary Base would stand at 3.2%, remaining stable with respect to the September figure and standing at its lowest value since the exit from convertibility (see Figure 4.1).

Figure 4.1 | Monetary base

Figure 4.2 | Factors explaining the Monetary Base

Average monthly change

On the supply side of the Monetary Base, the BCRA’s interest-bearing liabilities resulted in an expansion of liquidity due to the fact that subscriptions were lower than maturities. On the other hand, operations with public securities in the secondary market and the execution of put option contracts on National Government securities by financial institutions also generated monetary expansion. These factors were partially offset by the net sale of foreign currency to the private sector (see Figure 4.2).

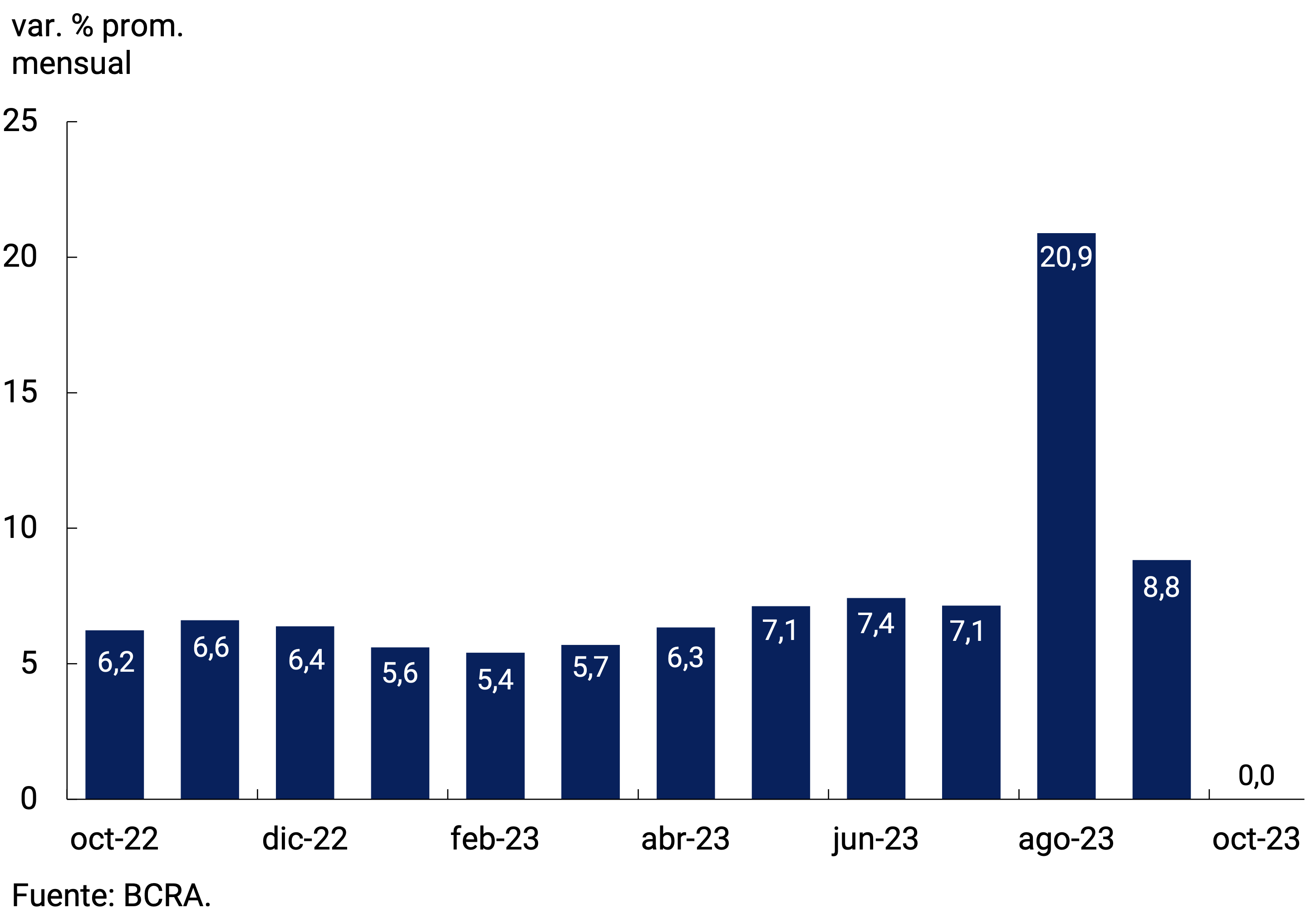

In the middle of the month, the BCRA decided to increase the level of interest rates on monetary policy instruments. In this way, the interest rate of the LELIQ was raised by 15 p.p. to 28 days, bringing it to 133% n.a. (254.8% e.a.). The interest rate on the LELIQ with a 180-day term was increased by the same magnitude and stood at 135.5% n.a. (182.3% y.a.). As for shorter-term instruments, the interest rate on 1-day pass-by-passes increased from 111% n.a. to 126% n.a. (251.8% y.a.); while the interest rate on 1-day active passes was set at 160% n.a. (393.6% e.a.). Finally, the spread of the NOTALIQ in the last auction was 2.5 p.p.

5. Loans to the private sector

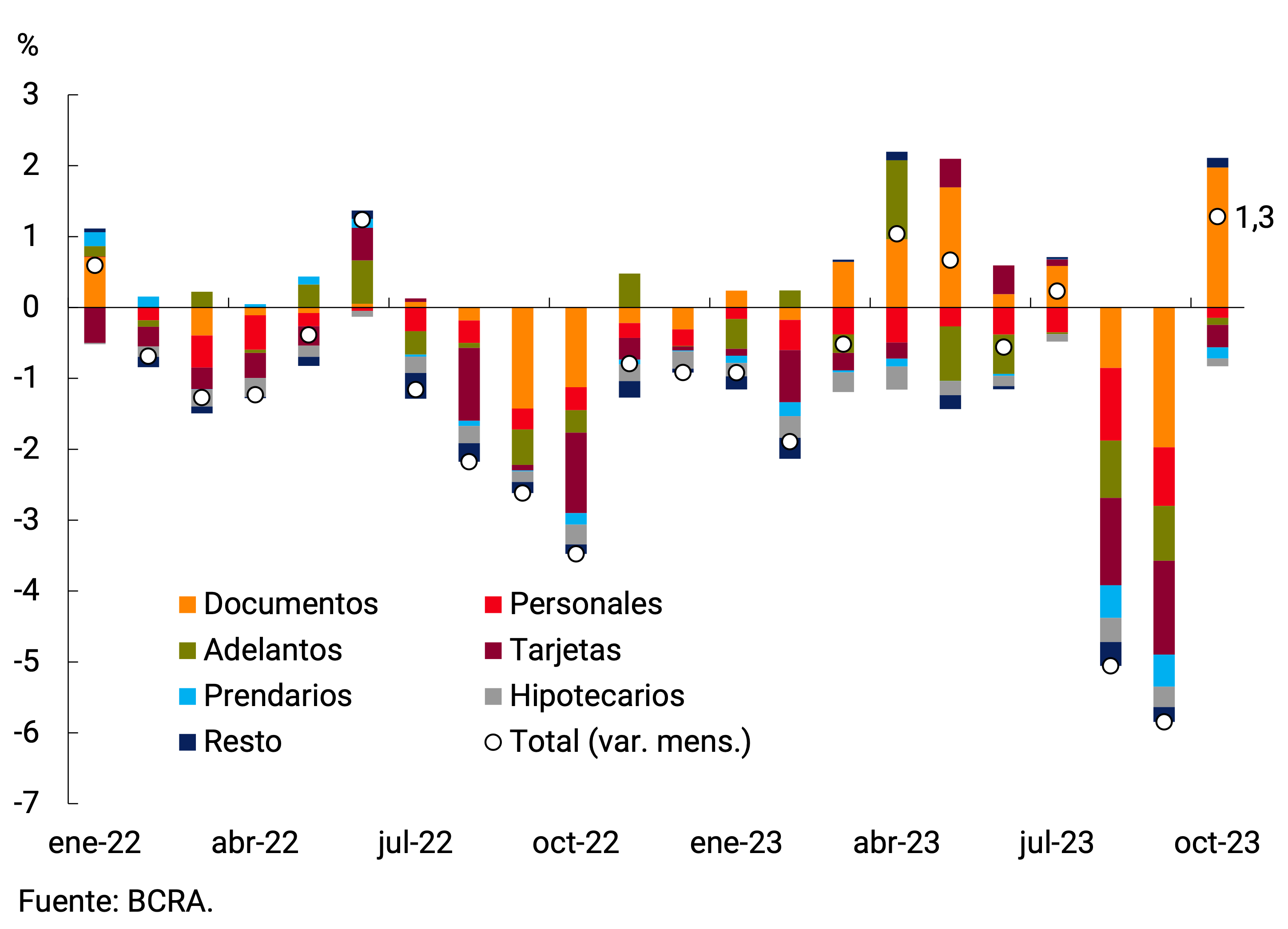

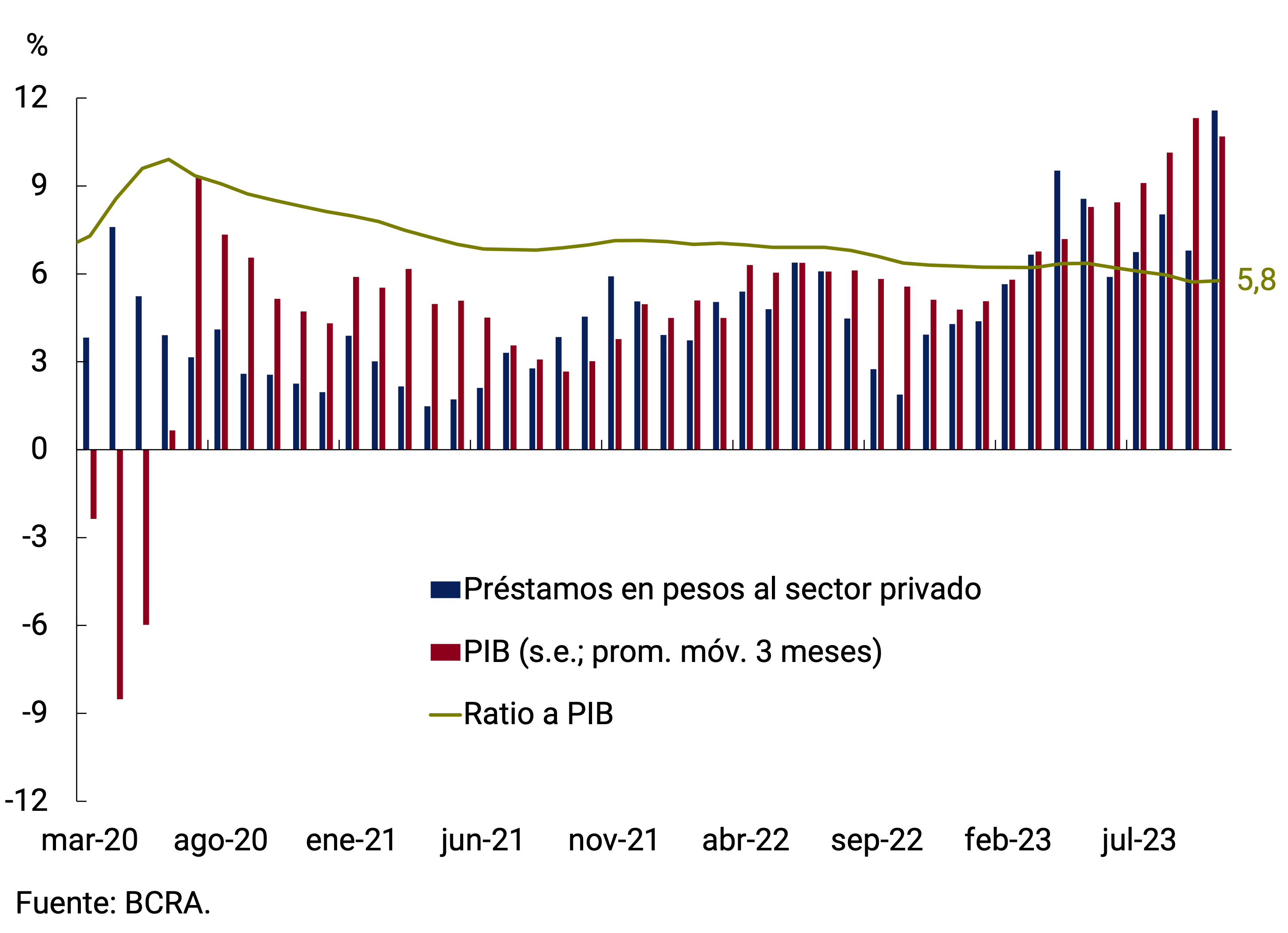

Loans in pesos to the private sector in real terms and without seasonality would have registered an expansion after two months of contractions. Thus, in October they would have exhibited a growth at constant prices of 1.3% s.e. and in the last 12 months they would accumulate a fall of around 13%. At the level of the large lines of credit, the growth in financing for commercial activity was partially offset by the dynamics of the rest of the loans (see Figure 5.1). As a percentage of GDP, loans in pesos to the private sector would stand at 5.8%, the lowest level in the last 20 years (see Figure 5.2).

Figure 5.1 | Loans in pesos to the private

sector Real without seasonality; contribution to monthly growth

Figure 5.2 | Loans in pesos to the private

sector In terms of GDP

Commercial lines would have shown a recovery, with a monthly increase of 4.4% s.e. in real terms, although they would be 1.1% below the record of a year ago. At the instrument level, loans granted through documents would have expanded in the month 6.5% s.e. at constant prices and would be 9.8% above their level a year ago. Within these lines, single-signature documents, with a longer average term, would have registered an increase of 4.7% s.e. Meanwhile, discounted documents would have grown 9.5% s.e. in the month. For their part, advances would have registered a contraction at constant prices of 0.9% s.e., and would be 16.3% below the level of October 2022.

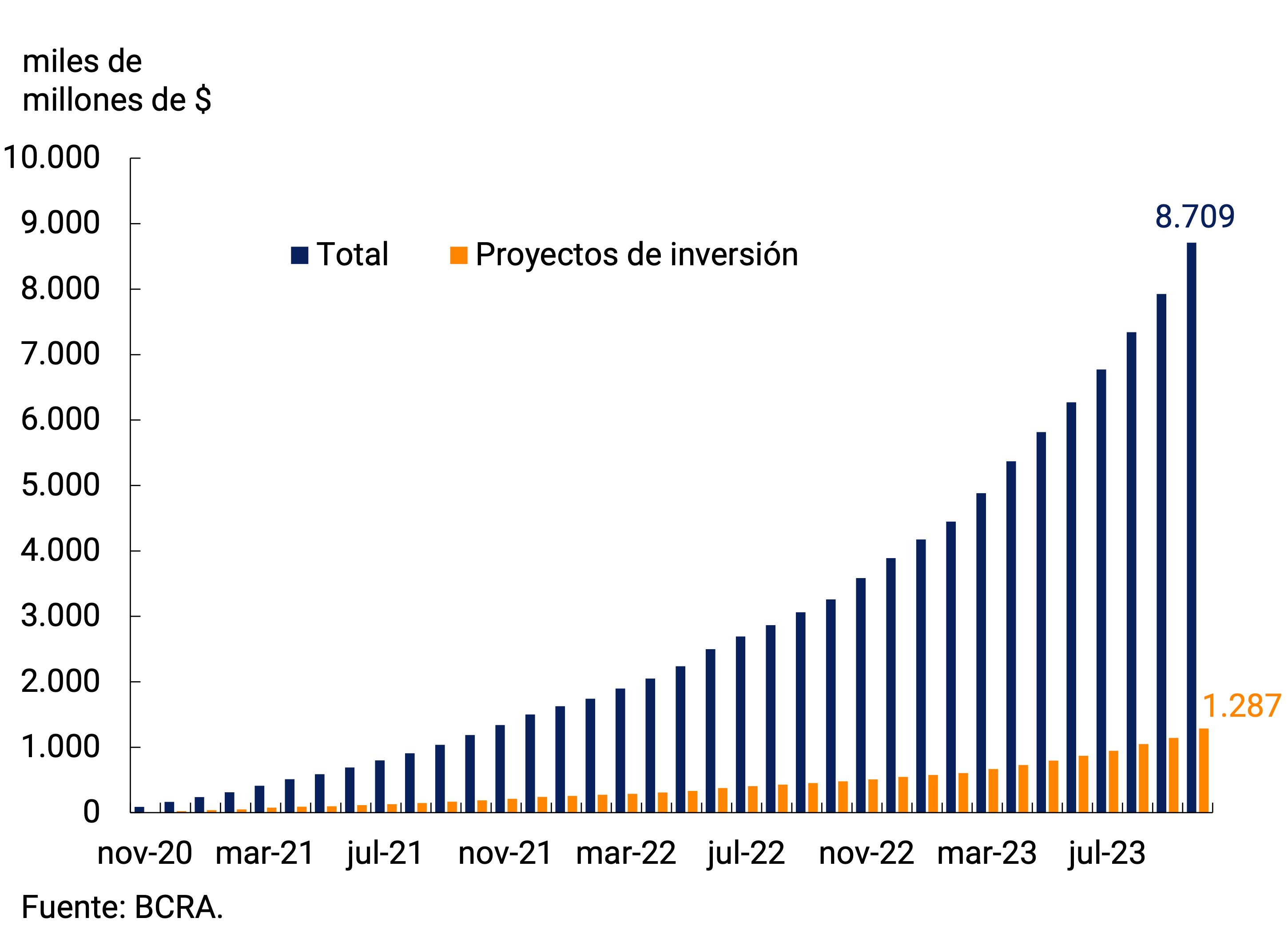

The Financing Line for Productive Investment (LFIP) continued to channel credit to the productive activity of Micro, Small and Medium-sized Enterprises (MSMEs). At the end of October, loans granted under the LFIP accumulated $8,709 billion since its launch, an increase of 9.9% compared to last month (see Figure 5.3). Of the total financing granted through the LFIP, 14.8% corresponds to investment projects and the rest to working capital. The average balance of financing granted through the LFIP reached approximately $2,000 billion in September (latest available information), which represents about 17.1% of total loans and 37.2% of total commercial loans.

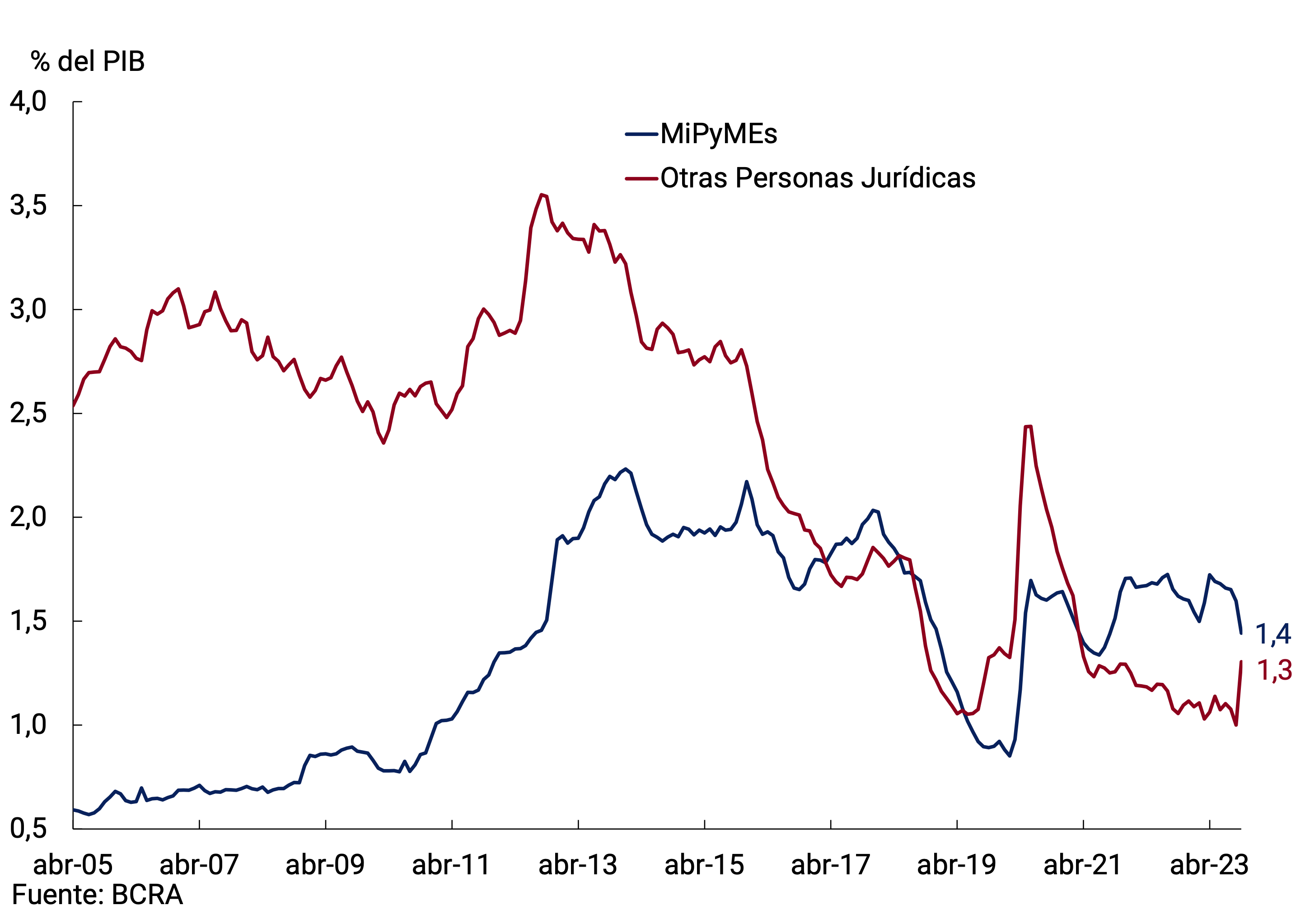

Distinguishing commercial loans by type of debtor, credit to MSMEs stood at around 1.4% of GDP, slightly above the pre-pandemic record and the historical average. In the case of large companies, the credit-to-GDP ratio stands at around 1.3% of GDP, showing an increase compared to previous months (see Figure 5.4).

The LFIP helped to sustain credit to relatively smaller firms. Indeed, distinguishing commercial loans by type of debtor, credit to MSMEs stood at around 1.6% of GDP, above the pre-pandemic record and the historical average. On the other hand, in the case of large companies, the credit-to-GDP ratio rose slightly to 1.2% of GDP, remaining among the lowest records in the last 20 years (see Figure 5.4).

Figure 5.3 | Financing granted through the Productive Investment Financing Line (LFIP)

Accumulated disbursed amounts; data at the end of the month

Figure 5.4 | Commercial Loans by Type of Debtor

As a Percentage of GDP

For their part, consumer loans would have registered a contraction of 1.0% s.e. at constant prices during the month and would accumulate a fall of 17.8% in the last year. Financing instrumented with credit cards would have shown a contraction in real terms of 1.0% s.e. in the month, while personal loans would have fallen 1.1% s.e. in the same period. In year-on-year terms, these loans registered variations of -11.6% and -28.7% at constant prices, respectively.

With regard to lines with real collateral, in real terms, pledge loans would have registered a decrease of 2.4% s.e., bringing the year-on-year fall to 22.2%. For its part, the balance of mortgage loans would have shown a monthly decrease of 2.7% s.e. (-43.5% y.o.y.).

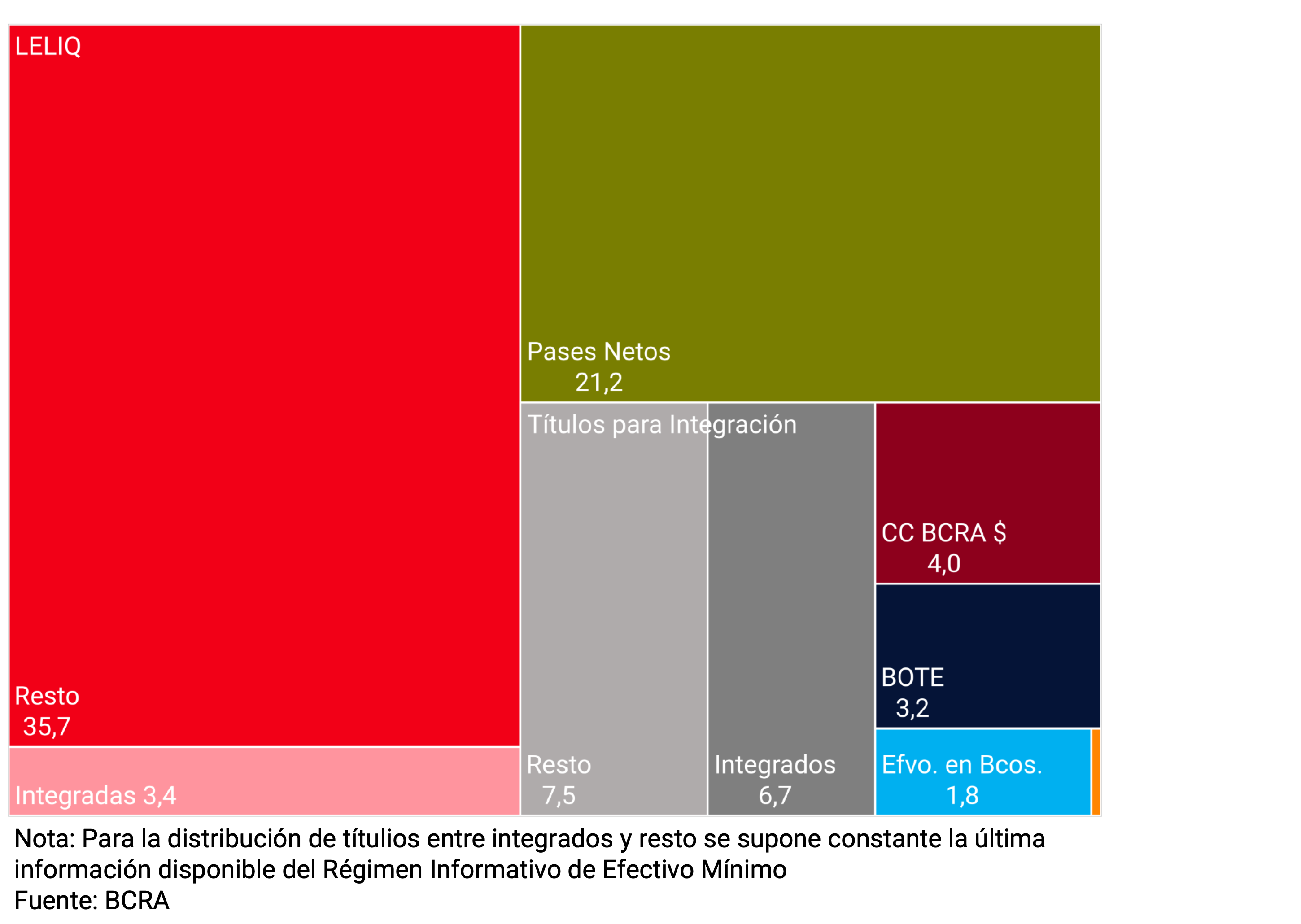

6. Liquidity in pesos of financial institutions

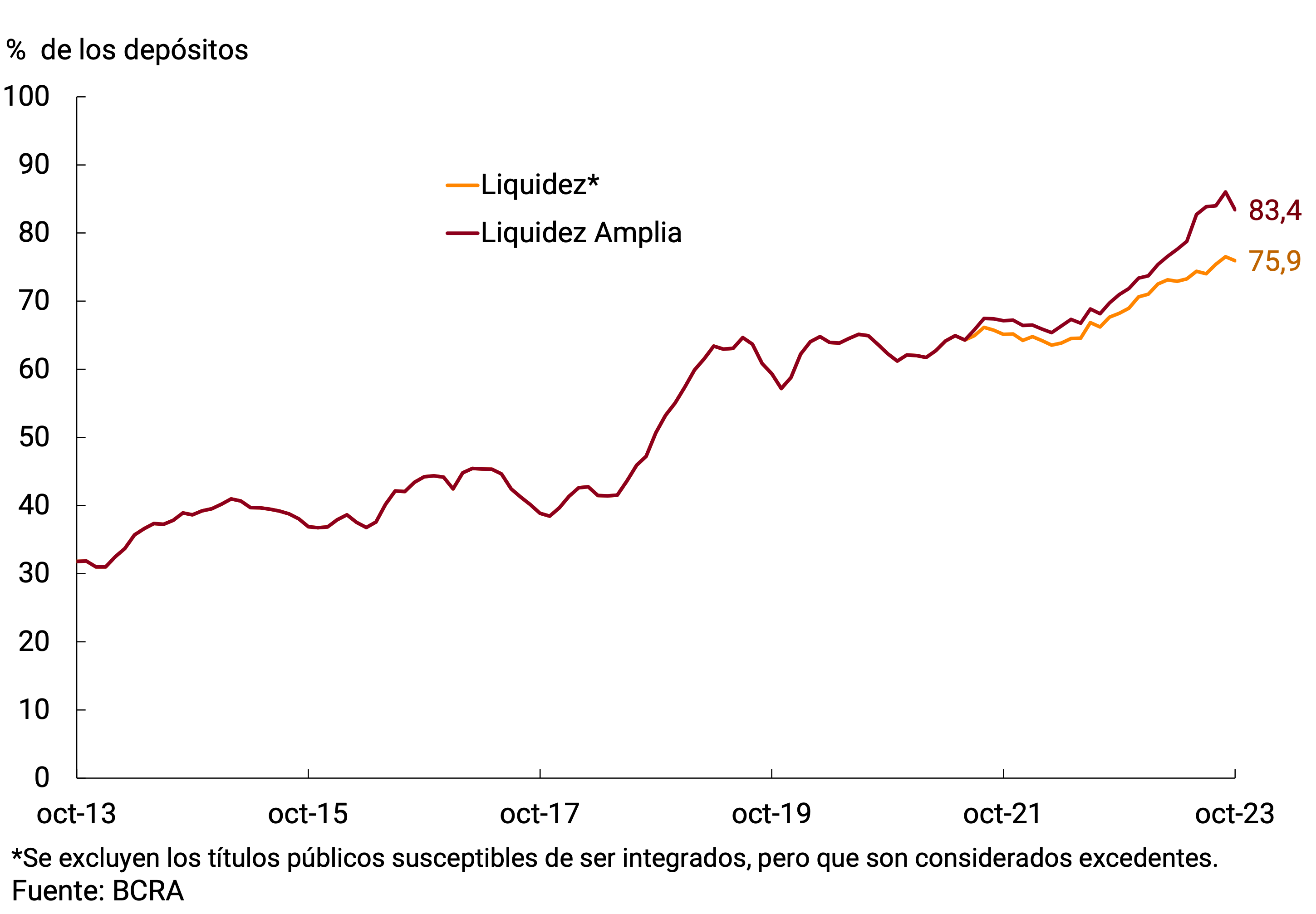

In October, ample bank liquidity in local currency5 fell by 2.5 p.p. compared to September, averaging 83.4% of deposits (see Figures 6.1 and 6.2). In any case, it remained at historically high levels. The fall was explained by the decrease in the Central Bank’s remunerated liabilities and public securities for minimum cash integration.

Regarding the composition of interest-bearing liabilities, 1-day pass-throughs increased their participation in the total of instruments, reaching a representativeness of 34%. On the other hand, the LELIQ with a 28-day term represented, on average, 61% of the total, reducing their relative share compared to the previous month. LEDIV and LEGAR increased their participation compared to the previous month, averaging 4% of total interest-bearing liabilities. The rest was made up of the longer-term species, concentrated exclusively in NOTALIQ, which accounted for only 0.1% of the October balance.

Figure 6.1 | Liquidity levels in pesos of financial institutions

Figure 6.2 | Composition of liquidity of financial

institutions % of deposits

7. Foreign currency

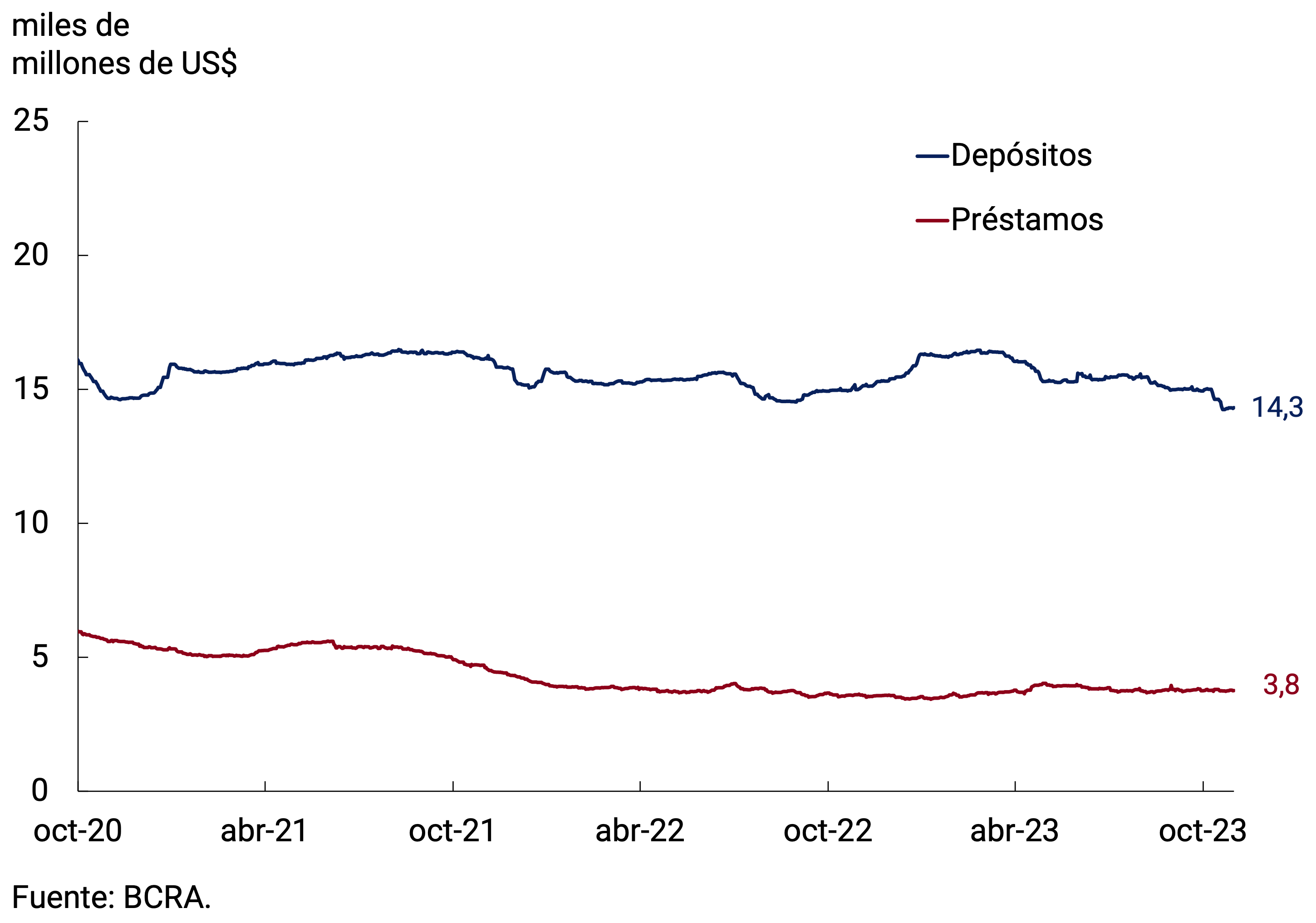

In the foreign currency segment, the main assets and liabilities of financial institutions had a mixed performance. On the one hand, private sector deposits fell by US$623 million in the month and ended October with a balance of US$14,315 million. This drop was concentrated in the deposits of human persons. On the other hand, the balance of loans to the private sector remained practically unchanged and ended the month at US$3,753 million (see Figure 7.1).

Figure 7.1 | Balance of private sector foreign currency deposits and loans

Figure 7.2 | Liquidity in foreign currency of financial institutions

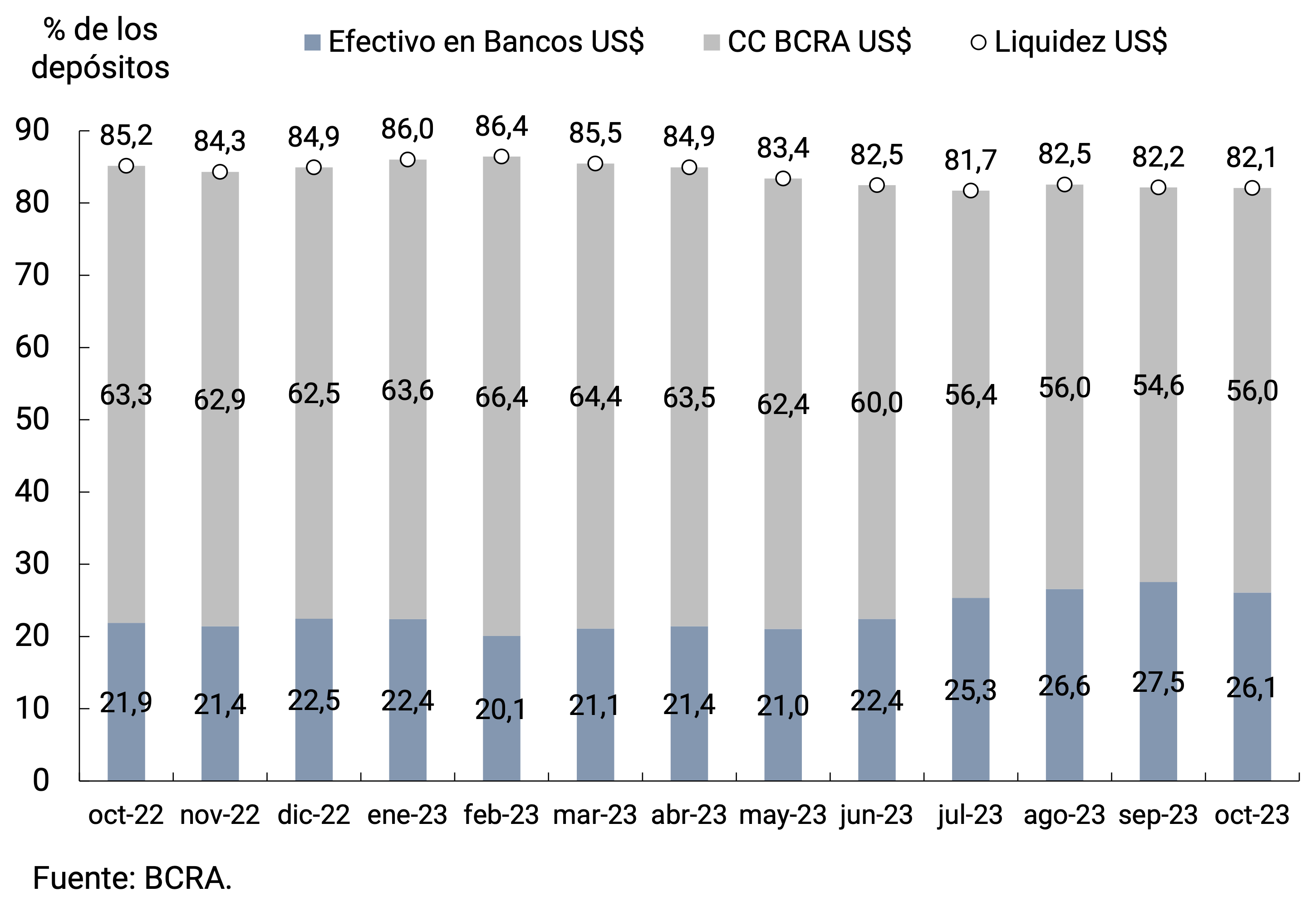

The liquidity of financial institutions in the foreign currency segment stood at 82.1% of deposits, remaining at historically high levels. In terms of composition, there was an increase in current accounts at the BCRA to the detriment of cash in banks (see Figure 7.2).

During the month, a series of regulatory modifications were made in foreign exchange matters in relation to access to the foreign exchange market. Among them, a regulation that favors SMEs that import inputs and capital goods for their productive activitiesstands out 6, 7. In turn, with the aim of increasing the supply of foreign currency, in the last days of the month, it was established, effective until November 17, 2023, the obligation to enter and settle in the Single and Free Exchange Market (MULC) 70% of the equivalent value in foreign currency of exported goods and the charges for services provided to non-residents reached. as well as advances, pre-financing and post-financing from abroad, leaving the remaining 30% to carry out purchase and sale operations with negotiable securities acquired with settlement in foreign currency and sold with settlement in local currency8. The BCRA sanctioned complementary regulations to these decrees9, such as the possibility of crediting the resulting funds in pesos to an account whose remuneration is determined according to the evolution of the exchange rate or allocating them to the subscription of bills liquidable in pesos for the Reference Exchange Rate10.

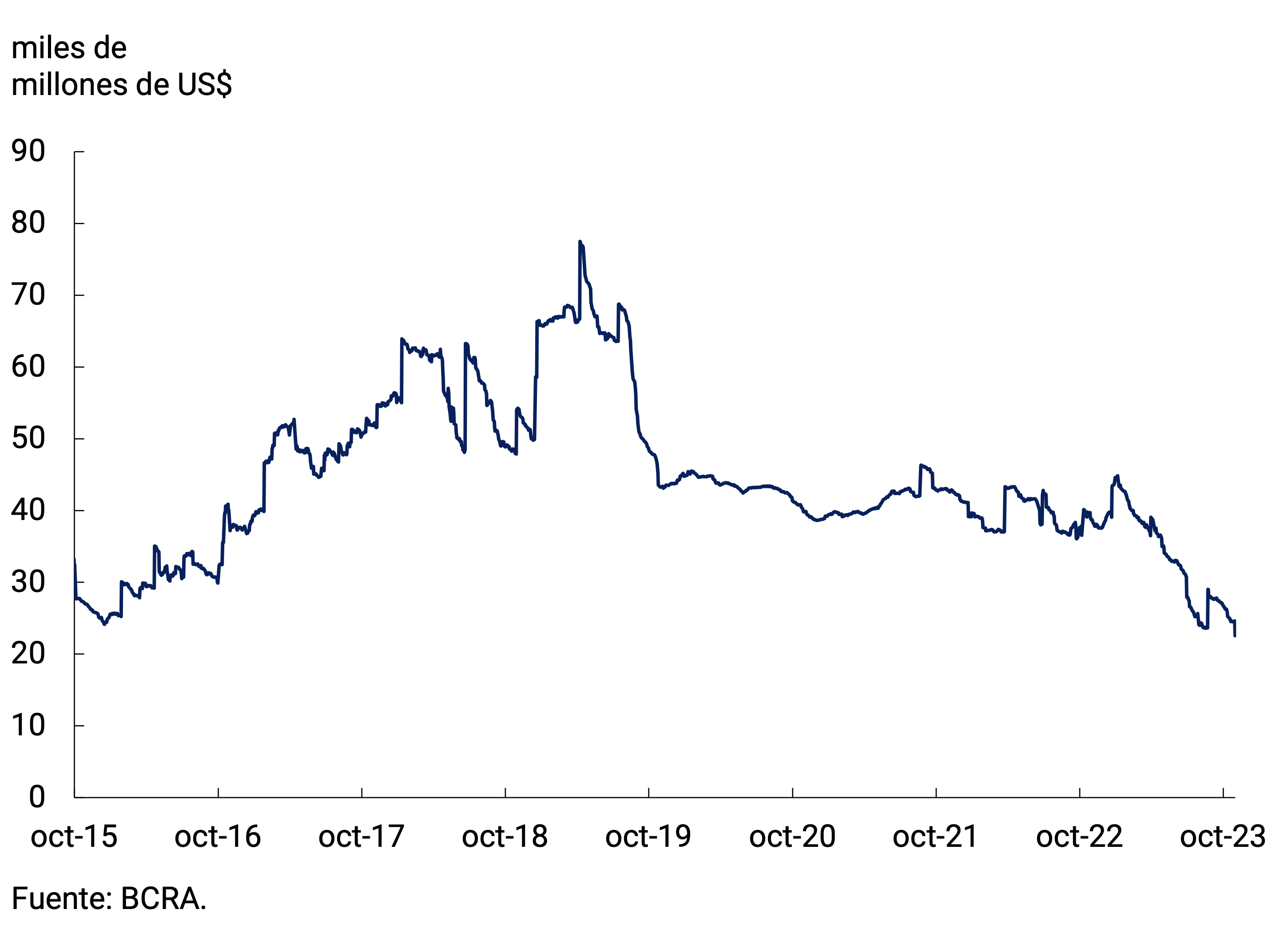

The BCRA’s International Reserves ended October with a balance of US$22,559 million, registering a fall of US$4,366 million compared to the end of September. This dynamic was influenced by the payment of capital to the International Monetary Fund, which expired on the last day of the month. Specifically, a payment of US$2,600 million was made. Other factors that explained the decline were the change in minimum cash accounts and foreign exchange sales to the private sector, a trend that reversed in the latter part of the month (see Figure 7.3).

Finally, after recalibrating it in mid-August, the BCRA decided to keep the bilateral nominal exchange rate (TCN) unchanged against the US dollar at $350/US$ (see Figure 7.4).

Figure 7.3 | International Reserve Balance

Figure 7.4 | Bilateral Nominal Exchange Rate against the US Dollar

Glossary

ANSES: National Social Security Administration.

AFIP: Federal Administration of Public Revenues.

BADLAR: Interest rate on fixed-term deposits for amounts greater than one million pesos and a term of 30 to 35 days.

BCRA: Central Bank of the Argentine Republic.

BM: Monetary Base, includes monetary circulation plus deposits in pesos in current account at the BCRA.

CC BCRA: Current account deposits at the BCRA.

CER: Reference Stabilization Coefficient.

NVC: National Securities Commission.

SDR: Special Drawing Rights.

E.A.: Effective Annual.

EFNB: Non-Banking Financial Institutions.

EM: Minimum Cash.

FCI: Common Investment Fund.

A.I.: Year-on-year .

IAMC: Argentine Institute of Capital Markets

CPI: Consumer Price Index.

ITCNM: Multilateral Nominal Exchange Rate Index

ITCRM: Multilateral Real Exchange Rate Index

LEBAC: Central Bank bills.

LELIQ: Liquidity Bills of the BCRA.

LFIP: Financing Line for Productive Investment.

M2 Total: Means of payment, which includes working capital held by the public, cancelling cheques in pesos and demand deposits in pesos from the public and non-financial private sector.

Private M2: Means of payment, includes working capital held by the public, cancelling cheques in pesos and demand deposits in pesos from the non-financial private sector.

Private transactional M2: Means of payment, includes working capital held by the public, cancelling cheques in pesos and non-remunerated demand deposits in pesos from the non-financial private sector.

M3 Total: Broad aggregate in pesos, includes the current currency held by the public, cancelling checks in pesos and the total deposits in pesos of the public and non-financial private sector.

Private M3: Broad aggregate in pesos, includes the working capital held by the public, cancelling checks in pesos and the total deposits in pesos of the non-financial private sector.

MERVAL: Buenos Aires Stock Market.

MM: Money Market.

N.A.: Annual nominal.

NOCOM: Cash Clearing Notes.

ON: Negotiable Obligation.

GDP: Gross Domestic Product.

P.B.: basis points.

PSP.: Payment Service Provider.

p.p.: percentage points.

MSMEs: Micro, Small and Medium Enterprises.

ROFEX: Rosario Term Market.

S.E.: No seasonality

SISCEN: Centralized System of Information Requirements of the BCRA.

SIMPES: Comprehensive System for Monitoring Payments of Services Abroad.

TCN: Nominal Exchange Rate

IRR: Internal Rate of Return.

TM20: Interest rate on fixed-term deposits for amounts greater than 20 million pesos and a term of 30 to 35 days.

TNA: Annual Nominal Rate.

UVA: Unit of Purchasing Value

References

1 Corresponds to private M2 excluding interest-bearing demand deposits from companies and financial service providers. This component was excluded since it is more similar to a savings instrument than to a means of payment.

2 The interest rates currently in force are those established by communication “A” 7862.

3 The rest of the depositors are made up of individuals with deposits of more than $30 million and legal entities.

4 Private M3 includes working capital held by the public and deposits in pesos of the non-financial private sector (demand, term and others).

5 Includes current accounts at the BCRA, cash in banks, balances of net passes arranged with the BCRA, holdings of LELIQ and NOTALIQ, and public bonds eligible for reserve requirements.

6 Communication “A” 7874.

7 Other rules that were applied during the period were communications “A” 7864, 7866.

8 Decree 549/2023 of the National Executive Branch.

9 Communications “A” A” 7853, “A” 7854, “A” 7867 and “A” 7868.

10 Communication “A” 7873.

Share on