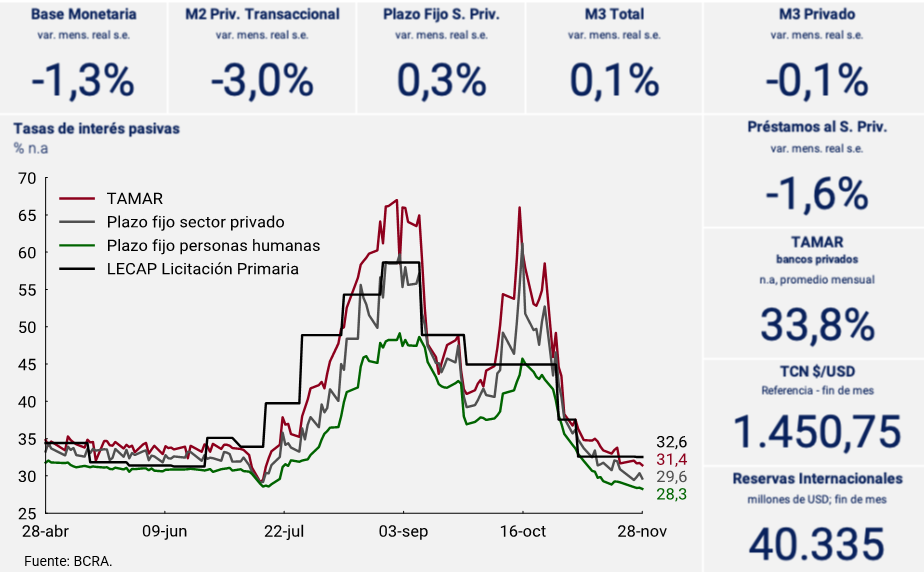

Executive summary

In November, the broad monetary aggregate (private M3) registered a slight contraction in real terms and without seasonality (-0.1%), which was concentrated in the transactional segment. In fact, means of payment (private transactional M2) registered a fall of 3.0% s.e. at constant prices, explained by the behavior of unpaid sight and, to a lesser extent, by the working capital held by the public.

Meanwhile, fixed-term deposits showed a slight increase at constant prices (0.3% s.e.), even in a context of lower interest rates paid for these placements, after the electoral uncertainty dissipated. On the other hand, the interest-bearing view, whose main holders are the “Financial Services Providers”, grew in the month by 0.4% s.e. in real terms, with the increase concentrated in the last days of November, a trend that continued at the beginning of December. This dynamic was influenced by a resolution of the CNV, through which a maximum limit of 20% of the assets of the Money Market FCIs was set to invest in bonds.

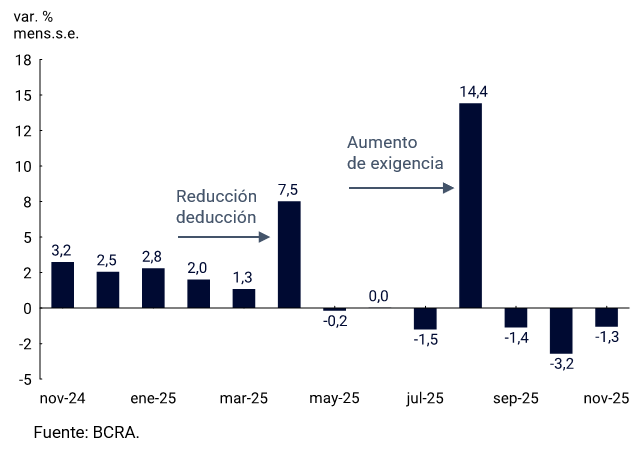

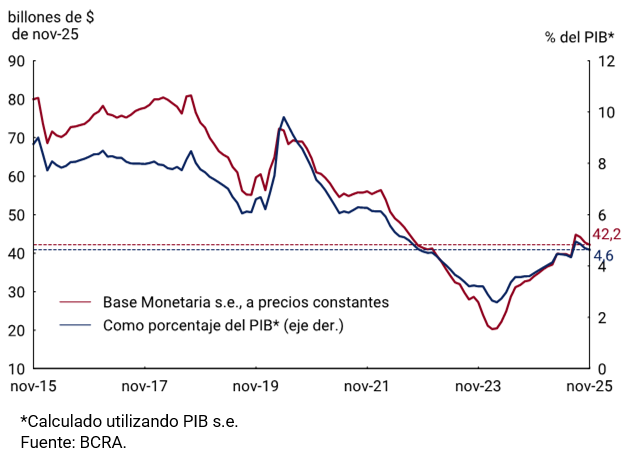

As for primary creation, the Monetary Base fell 1.3% in real terms in November, standing at 4.6% of GDP. Looking ahead to the last month of the year, in which it presents a marked positive seasonality, the BCRA made progress in the normalization of reserve requirements, reducing the requirement that can be integrated in pesos as of December. In addition, it provided that the minimum daily integration is 75% of the total minimum cash requirement in pesos for the period.

Finally, loans in pesos to the private sector registered a monthly contraction of 1.6% s.e. at constant prices, with falls in most lines. The exception was mortgage credit and financing through advances. However, in year-on-year terms they grew 35%.

2. Evolution of the real quantity of money

In November, the broad monetary aggregate (private M3)1 registered an average monthly increase of $1.5 trillion, which implied a slight contraction in real terms and without seasonality (-0.1%). As a percentage of GDP, private M3 stood at 13.3%, around the record of the first ten months of the year and markedly below the historical average (17.6% in the period 2004-2025). At the component level, means of payment, measured through private transactional M2, registered a contraction of 3.0% s.e. at constant prices (see Figure 2.1). It was disseminated at the level of its elements, with a fall at constant prices of the circulating currency held by the public and transactional demand deposits of 0.9% s.e. and 4.4% s.e., respectively. On the other hand, interest-bearing deposits showed an increase at constant prices and without seasonality. After the fall of the previous month, fixed-term loans registered a slight expansion (0.3%; see Figure 2.2). This increase was explained by the higher holdings of legal entities, mainly Financial Services Providers, and was partially offset by a contraction in the holdings of natural persons. Interest rates on these instruments fell throughout the month, with uncertainty dispelled after the legislative elections. On the other hand, interest-bearing demand placements registered an increase of 0.4% s.e. in real terms. The growth was concentrated in the last days of the month and was explained by a rebalancing of the portfolio of the Money Market FCIs in favor of this type of placements and to the detriment of sureties, given that the CNV set a maximum limit of 20% of its assets for the holding of the latter. Although this regulation came into force on December 1, the days prior to its announcement began to observe a change in the composition of the assets in the Money Market FCI portfolio2

3. Money Creation

3.1. Primary creation

The Monetary Base, at constant prices and adjusted for seasonality, registered a contraction of 1.3% on a monthly average in November (see Figure 3.1.1). In terms of GDP, it stood at 4.6%, approaching again the values of the middle of this year (see Figure 3.1.2). It should be noted that towards the end of the month the BCRA made progress in the normalization of reserve requirements, reducing the requirement that can be integrated in pesos as of December. In addition, it provided that the minimum daily integration is 75% of the total minimum cash requirement in pesos for period3. The measure was taken, after overcoming the volatility of the electoral process, in view of the last month of the year, in which the Monetary Base typically presents a marked positive seasonality.

Between balances at the end of the month, the Monetary Base contracted by $0.4 trillion due to the BCRA’s operations in the secondary market (open market operations) and its participation in the round of simultaneous operations. With respect to tax operations, which were practically neutral, it is worth mentioning that foreign currency sales were made to the National Treasury on three occasions throughout the month. They were made with funds from his account in pesos at the BCRA, so their monetary effect was null.

Figure 3.1.1 | Monetary Base

At constant prices and without seasonality; avg. var.

Figure 3.1.2 | Monetary Base

At constant prices and in terms of GDP

3.2. Secondary creation

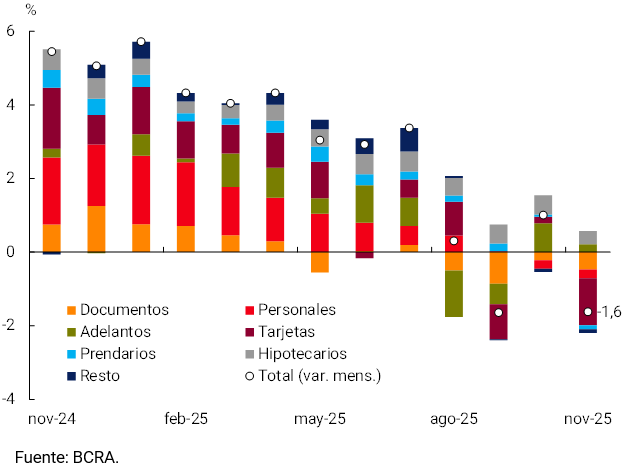

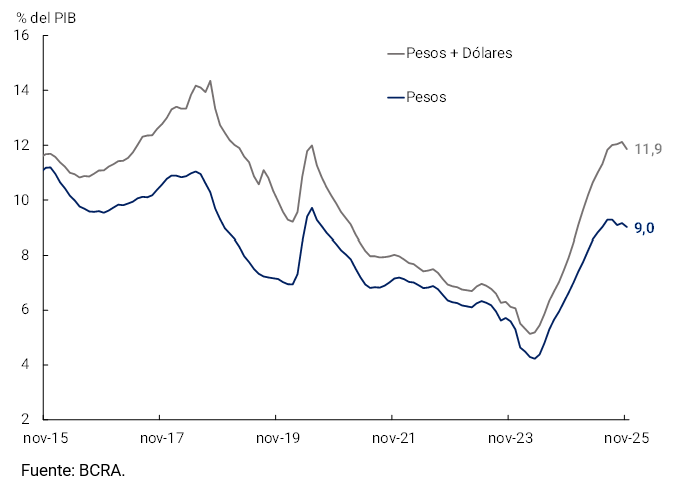

In November, loans in pesos to the private sector registered a fall of 1.6% in real terms and adjusted for seasonality. Most lines of credit showed a decrease in the month, with the exception of advances and mortgage loans (see Figure 3.2.1). This variation is consistent with a secondary expansion of $1.6 trillion. In year-on-year terms, loans grew 34.8% at constant prices and in terms of GDP stood at 9%, doubling the record at the beginning of 2024. Also including loans in dollars, the credit-to-GDP ratio amounted to 11.9% (see Figure 3.2.2).

Figure 3.2.1 | Contribution to var. monthly of loans in pesos to the private

sector At constant prices and without seasonality

Figure 3.2.2 | Loans to the private sector in terms of GDP

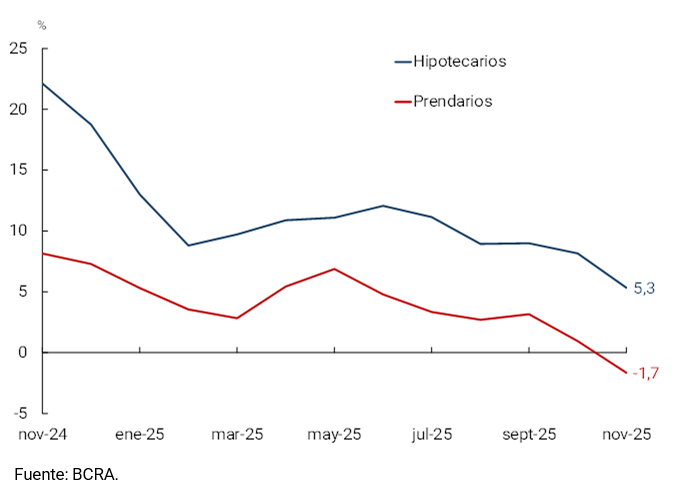

Among loans with real collateral, mortgage credit stood out once again, registering 17 months of uninterrupted growth, with a monthly expansion of 5.3% s.e. at constant prices (see Figure 3.2.3). Loans for the purchase of housing accumulate an increase of 232.4% in the last 12 months. Practically all of the growth of this line was explained by mortgage loans adjustable by UVA. On the other hand, pledge loans registered a fall of 1.7% s.e. at constant prices, being the first contraction since May last year. However, they were 54.4% higher than the level of a year ago in real terms.

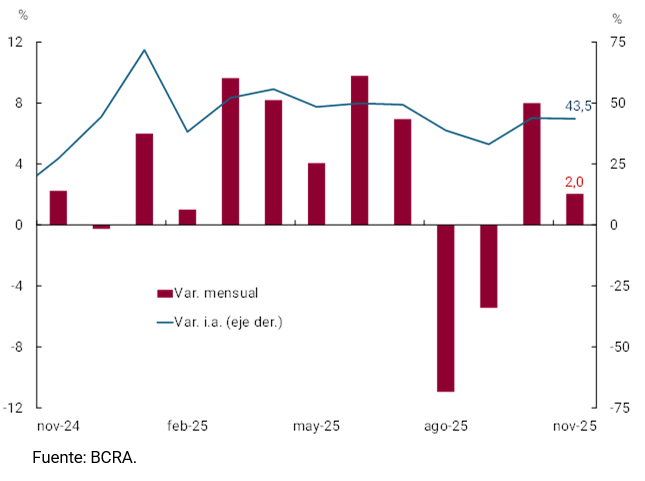

Commercial loans fell 0.9% s.e. in the month at constant prices, reversing the rise recorded in October. The contraction was concentrated in signature-only documents (-3.3% s.e.), which have an average term (weighted by amount) of 16 and a half months. Meanwhile, the shorter-term lines registered increases. In fact, discounted documents expanded 2.2% s.e. in the month, and advances grew 2.0% s.e. in real terms in November compared to October (see Figure 3.2.4).

Finally, consumer loans exhibited a contraction in the month of 3.2% s.e. in real terms, the largest since the beginning of 2024. The drop was largely explained by credit card financing, which fell 5.0% s.e. in real terms compared to October. However, in the last 12 months they have accumulated an increase of 19.9% in real terms. Finally, personal loans registered a fall at constant prices of 1.1% s.e. and accumulated a year-on-year increase of 61.7% measured at constant prices.

Figure 3.2.3 | Loans with real

collateral Var. monthly at constant prices and without seasonality

Figure 3.2.4 | Advances

At constant prices and without seasonality

4. Foreign currency

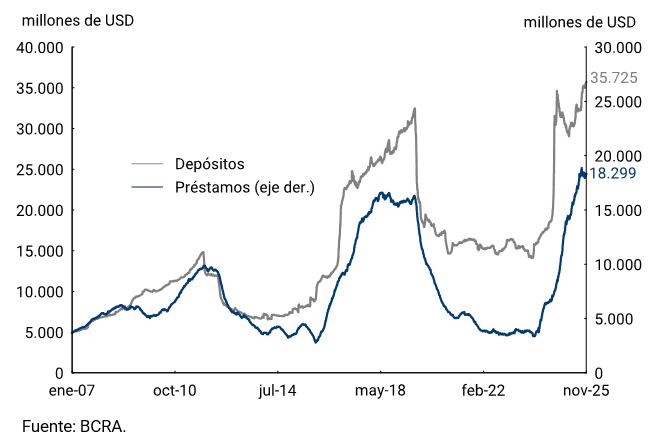

The main assets and liabilities in foreign currency of financial institutions showed dissimilar behaviors in November. On the one hand, private sector deposits increased by USD615 million in November, distributed in similar parts between deposits in savings banks and fixed-term placements. Thus, the balance at the end of the month stood at USD35,725 million, reaching a new all-time high (see Figure 4.1). It should be noted that at the end of November, the BOPREAL (series 3) matured for a total amount between principal and interest of USD1,012.5 million. Since the month ended on a Sunday, the payment was made on the first following business day, which implied an increase in dollar deposits on December 1. On the other hand, loans to the private sector registered a drop in the month of USD150 million, to end the month with a balance of USD18,299 million. Part of this drop is explained by the cancellation of loans with the proceeds of the placement of Negotiable Obligations by companies in the international market.

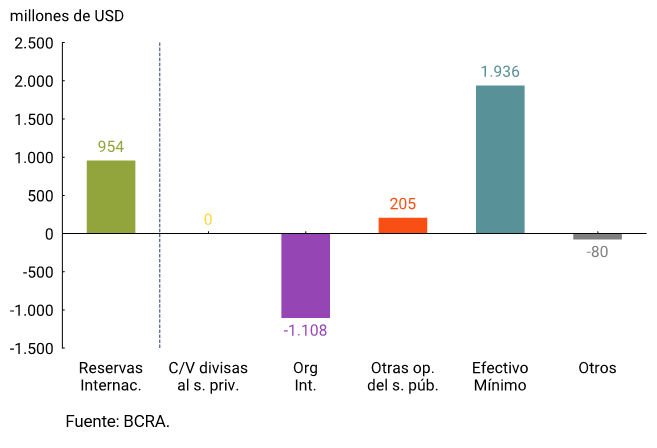

The BCRA’s International Reserves ended November with a balance of USD40,335 million, which implied an increase of USD954 million compared to the end of October. This dynamic was mainly explained by the increase in the current account in foreign currency of financial institutions at the BCRA, in a context of growth in dollar deposits. This increase was cushioned by the payment of maturities with International Organizations, more precisely the payment of interest with the IMF for USD793.6 million (see Figure 4.1).

Figure 4.1 | | Private Sector Deposits and Loans in Foreign

Currency Daily Balance

Figure 4.2 | Gross

International Reserves Daily Balance

Glossary

ANSES: National Social Security Administration.

AFIP: Federal Administration of Public Revenues.

BADLAR: Interest rate on fixed-term deposits for amounts greater than one million pesos and a term of 30 to 35 days.

BCRA: Central Bank of the Argentine Republic.

BM: Monetary Base, includes monetary circulation plus deposits in pesos in current account at the BCRA.

BOPREAL Bonds for the Reconstruction of a Free Argentina.

CC BCRA: Current account deposits at the BCRA.

CER: Reference Stabilization Coefficient.

NVC: National Securities Commission.

SDR: Special Drawing Rights.

EFNB: Non-Banking Financial Institutions.

EM: Minimum Cash.

FCI: Common Investment Fund.

IMF: International Monetary Fund.

A.I.: Year-on-year .

IAMC: Argentine Institute of Capital Markets

CPI: Consumer Price Index.

ITCNM: Multilateral Nominal Exchange Rate Index

ITCRM: Multilateral Real Exchange Rate Index

LECAP: National Treasury Bills Capitalizable in Pesos.

LFIP: Financing Line for Productive Investment.

M2 Total: Means of payment, which includes working capital held by the public, cancelling cheques in pesos and demand deposits in pesos from the public and non-financial private sector.

Private M2: Means of payment, includes working capital held by the public, cancelling cheques in pesos and demand deposits in pesos from the non-financial private sector.

Private transactional M2: Means of payment, includes working capital held by the public, cancelling cheques in pesos and non-remunerated demand deposits in pesos from the non-financial private sector.

M3 Total: Broad aggregate in pesos, includes the current currency held by the public, cancelling checks in pesos and the total deposits in pesos of the public and non-financial private sector.

Private M3: Broad aggregate in pesos, includes the working capital held by the public, cancelling checks in pesos and the total deposits in pesos of the non-financial private sector.

MSMEs: Micro, Small and Medium Enterprises.

MERVAL: Buenos Aires Stock Market.

MM: Money Market.

MLC: Free Exchange Market.

N.A.: Annual nominal.

E.A.: Effective Annual.

NOCOM: Cash Clearing Notes.

ON: Negotiable Obligation.

GDP: Gross Domestic Product.

P.B.: basis points.

PSP.: Payment Service Provider.

p.p.: percentage points.

ROFEX: Rosario Term Market.

S.E.: No seasonality

SISCEN: Centralized System of Information Requirements of the BCRA.

SIMPES: Comprehensive System for Monitoring Payments of Services Abroad.

TCN: Nominal Exchange Rate

IRR: Internal Rate of Return.

TM20: Interest rate on fixed-term deposits for amounts greater than 20 million pesos and a term of 30 to 35 days.

TNA: Annual Nominal Rate.

UVA: Unit of Purchasing Value

References

1 The private M3 includes the working capital held by the public and the deposits in pesos of the non-financial private sector (demand, time and others).

2 See RG No. 1092 of the National Securities Commission (CNV).

3 See Communication 8335.

Share on