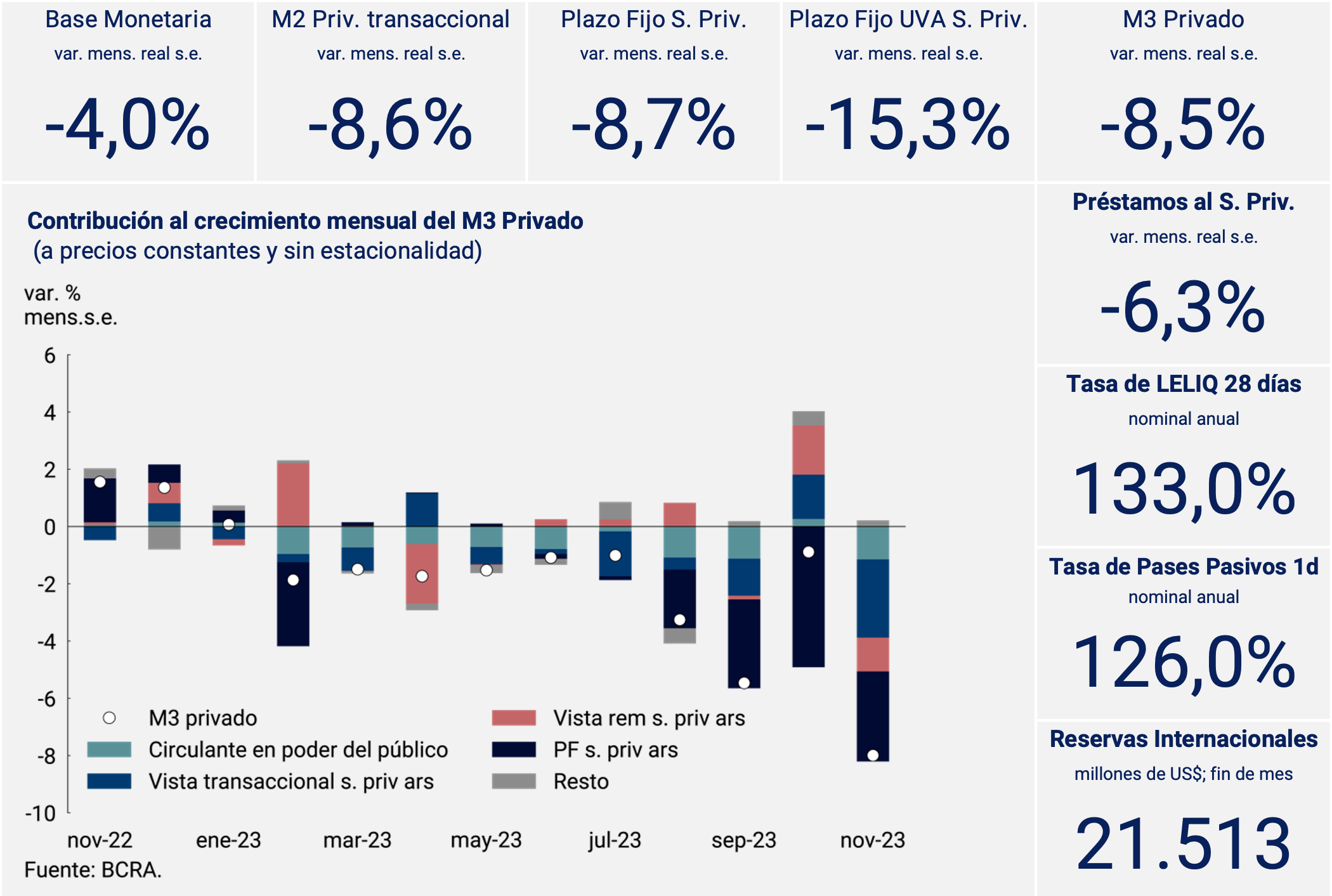

1. Executive Summary

On November 19, the second round of the presidential elections was held, which continued to bring volatility to the markets. The BCRA decided to keep the interest rates of monetary regulation instruments and the minimum interest rates on fixed-term deposits unchanged, after having increased them by 15 p.p. in October.

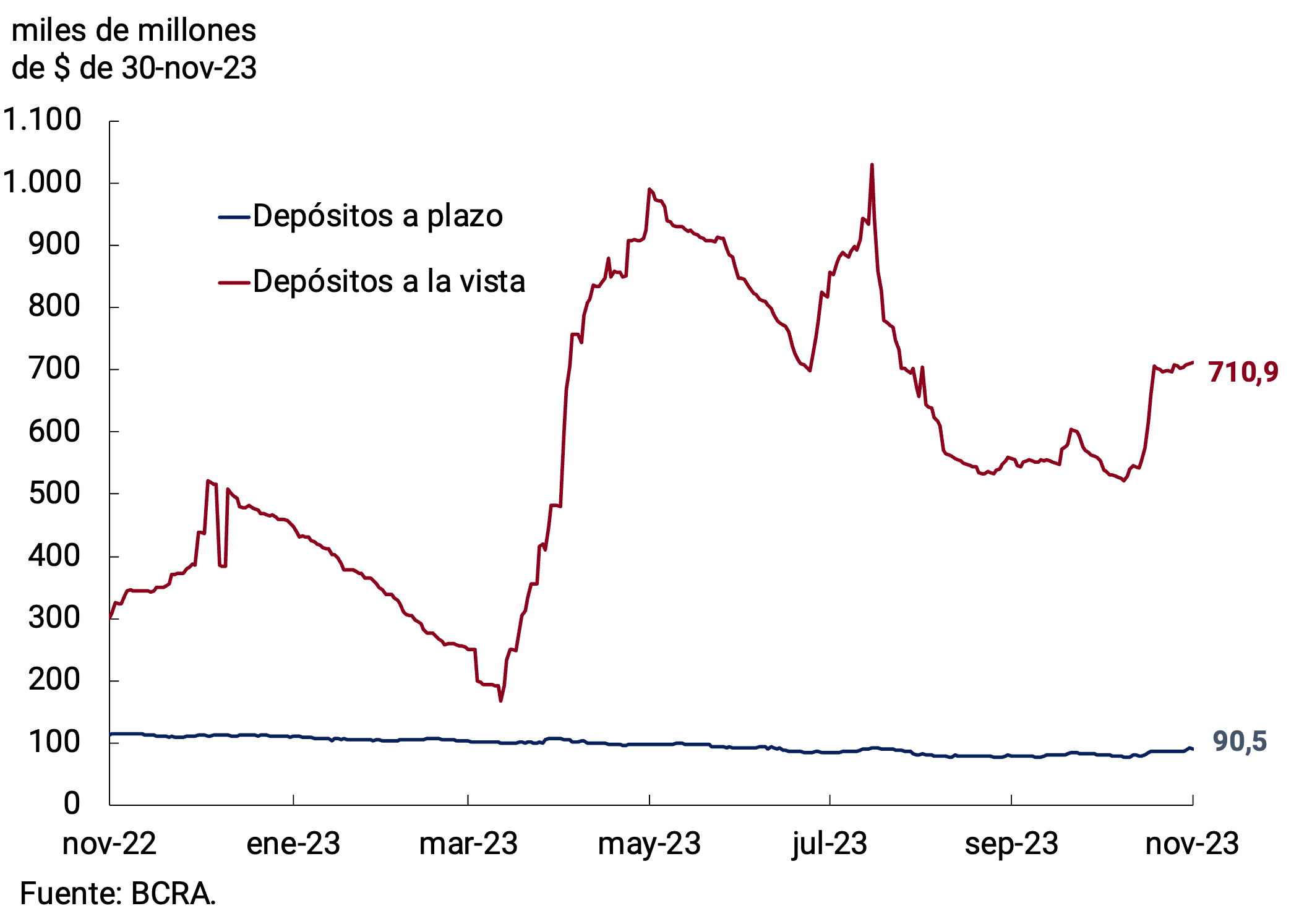

The broad monetary aggregate (private M3) presented a pronounced contraction in November at constant prices and without seasonality, explained both by a reduction in means of payment and in instruments remunerated in pesos. In particular, fixed-term deposits in pesos of the private sector in real terms and without seasonality registered a contraction of a smaller magnitude than in October, although still among the largest in recent decades. The largest falls per depositor were seen in companies and financial services providers. Interest-bearing demand deposits showed a marked contraction in the month, explained by the lower holdings of Money Market Mutual Funds, one of the main players in this segment. These funds rotated their portfolio towards passive passes with the BCRA, in a context in which equity remained at constant prices without variations in the month.

On the other hand, loans in pesos to the private sector registered a contraction at constant prices and without seasonality, which was generalized at the level of the large lines of credit. Thus, credit to GDP is at the lowest levels in the last 20 years.

2. Payment methods

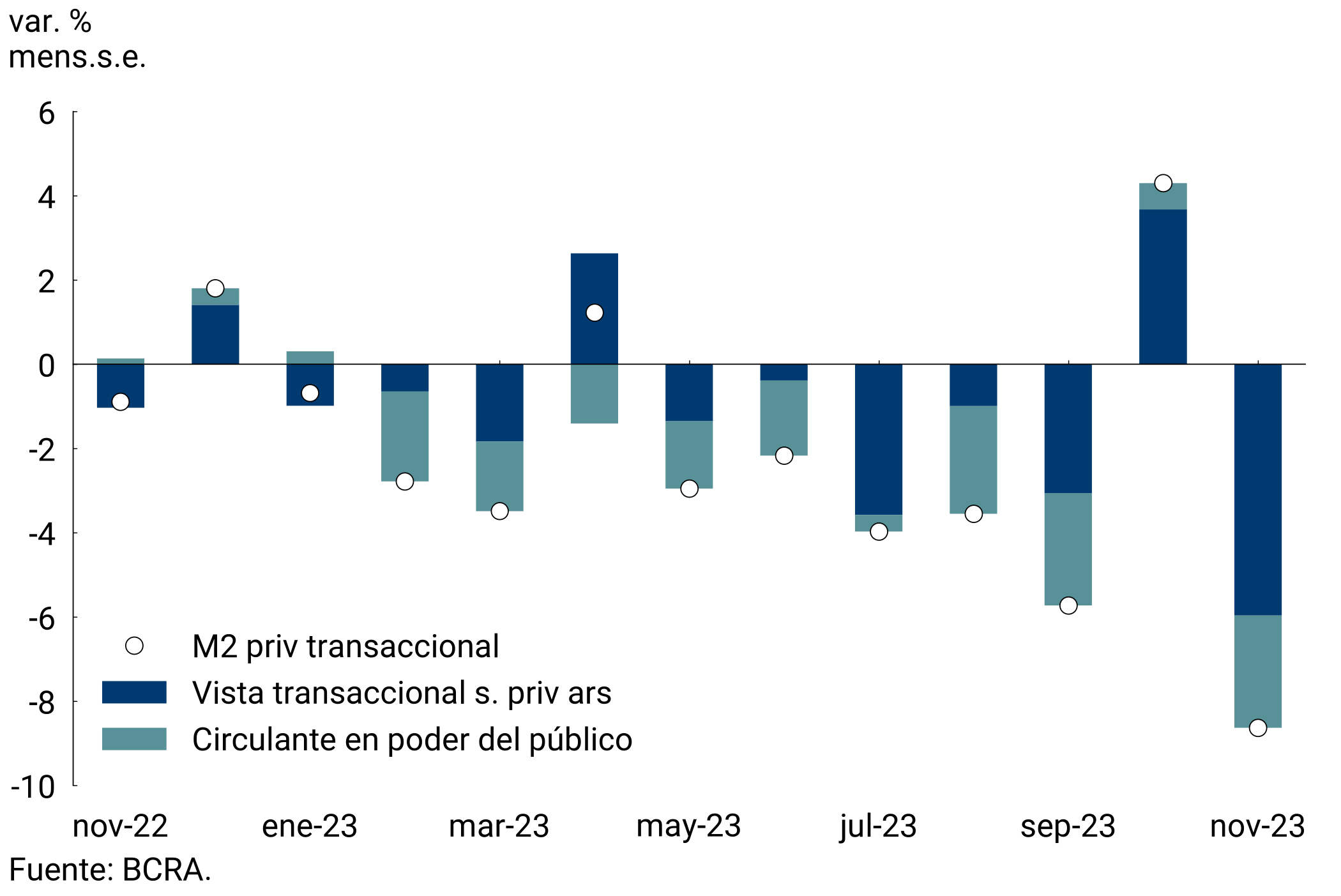

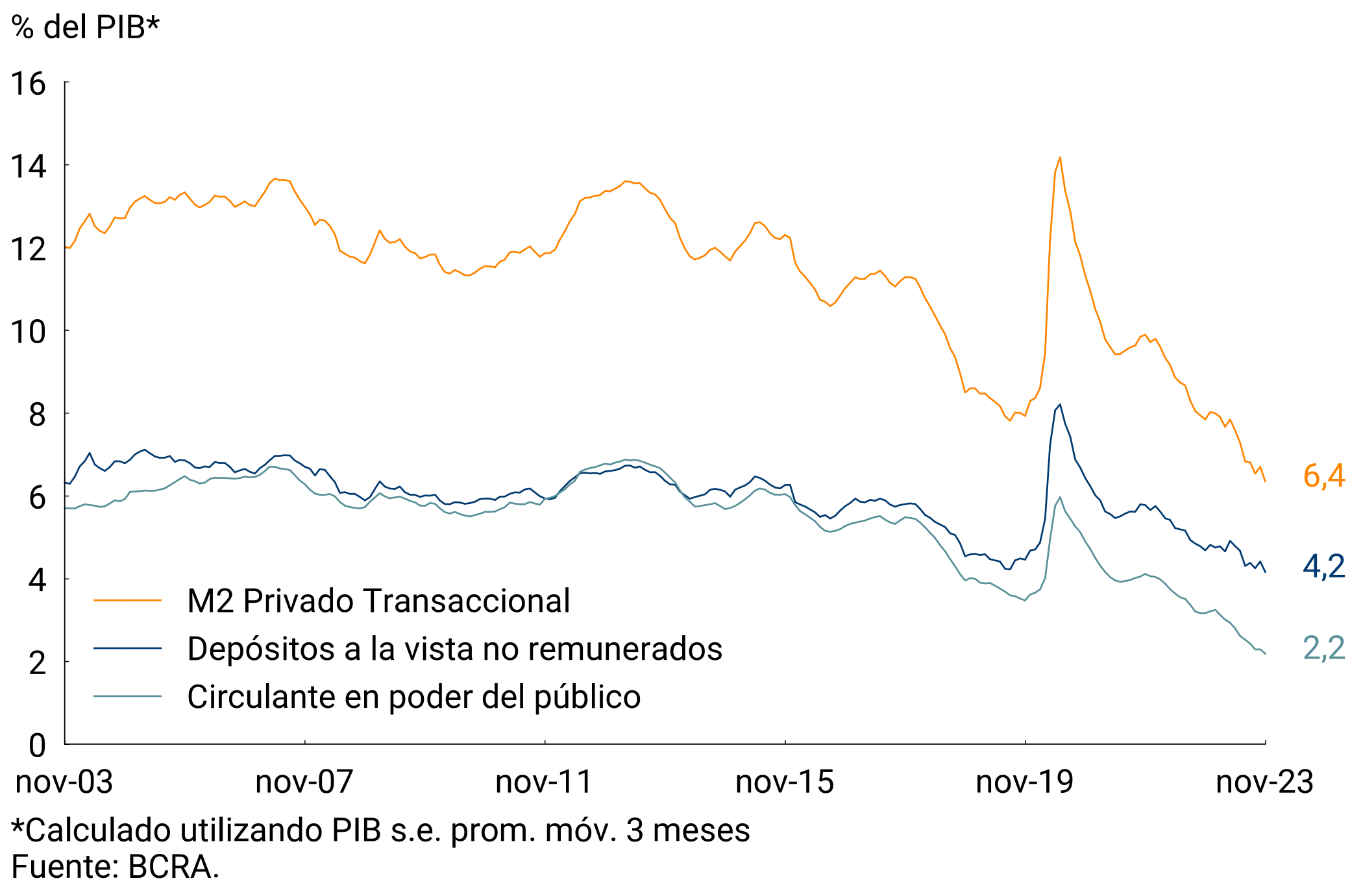

In real and seasonally adjusted terms (s.e.), means of payment (private transactional M21) would have registered a decrease of 8.6% in November, marking the largest monthly contraction in the last 20 years. This dynamic was due both to the behavior of working capital held by the public and of non-interest-bearing demand deposits (see Figure 2.1). Thus, private transactional M2 would accumulate a fall of around 25.5% in the year. In the year-on-year comparison, and at constant prices, it would be 24.2% below the level of November 2022. As a Product ratio, means of payment reached a new all-time low and stood at 6.4%, showing a decrease of 0.4 p.p. compared to the previous month (see Figure 2.2). At the component level, the working capital held by the public stood at 2.2% in terms of GDP, while demand deposits represented 4.2%, a level similar to those of mid-2019. In both cases, these records correspond to the lows of the last 20 years.

Figure 2.1 | Private transactional M2 at constant

prices Contribution by component to the monthly vari. s.e.

Figure 2.2 | Private transactional M2 as % of GDP

3. Savings instruments in pesos

The Board of Directors of the BCRA decided to maintain unchanged the minimum guaranteed interest rates on fixed-term deposits in the eleventh month of year2. Thus, the minimum guaranteed interest rate for placements by individuals remained at 133% n.a., which is equivalent to an effective monthly yield of 11%. Meanwhile, for the rest of the depositors in the financial system, the minimum guaranteed interest rate persisted at 126% n.a., with the effective monthly interest standing at 10.9%3.

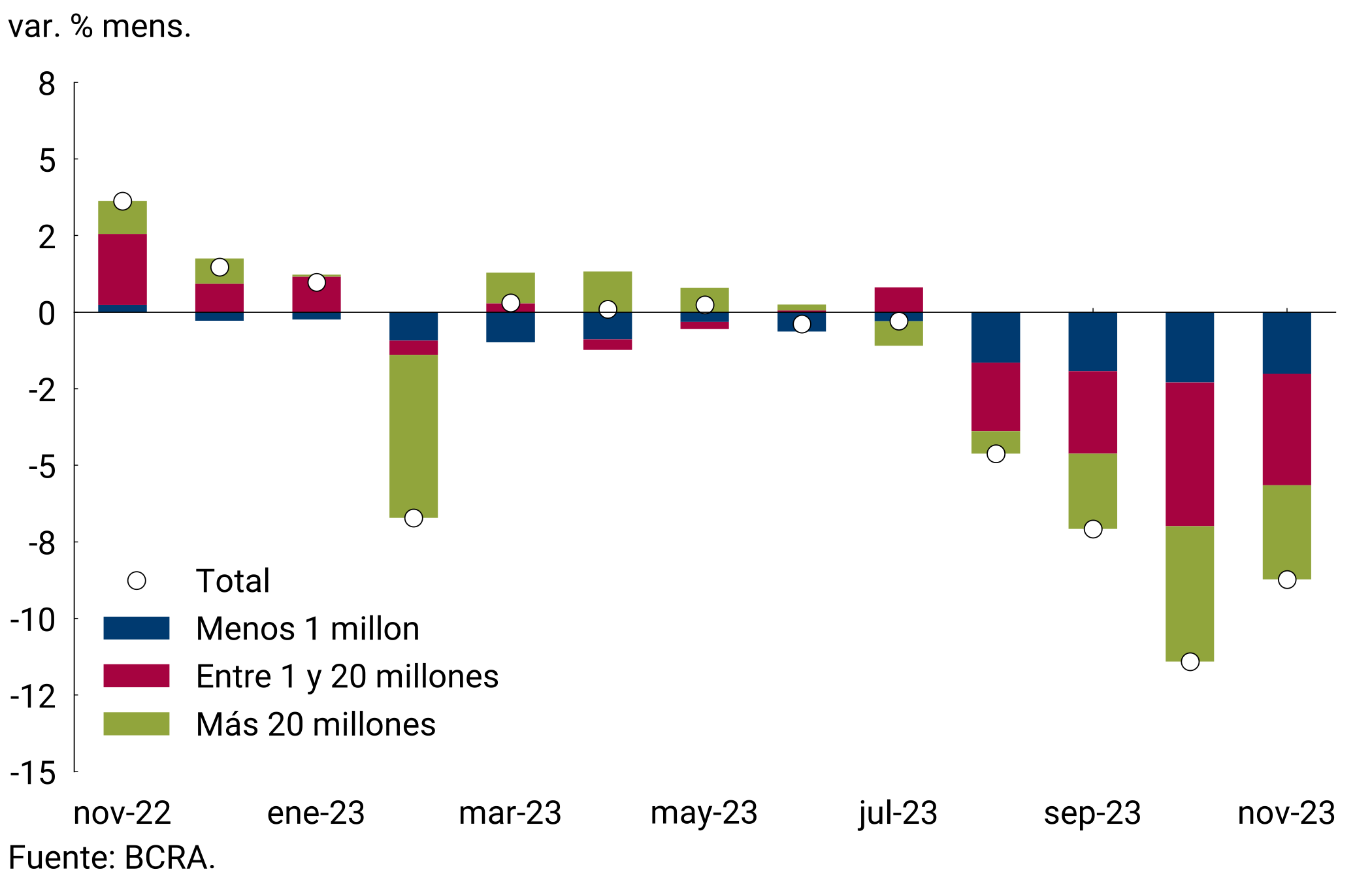

In this scenario, fixed-term deposits in pesos of the private sector in real terms again showed a fall in the eleventh month of the year, although of a smaller magnitude than that of October. In November, they would have experienced a monthly contraction of 8.7% s.e. at constant prices and, in this way, they would accumulate a drop of around 32.5% in the year. Thus, the balance of this type of instrument at constant prices was reduced to a record similar to the average observed between 2010 and 2019. In the same sense, as a percentage of GDP they would have stood at 5.5% in November, which would imply a decrease of 0.3 p.p. compared to October.

Analyzing the evolution of term placements by strata of amount, at constant prices, there is a generalized decrease in all segments throughout the month (see Figure 3.1). Deposits of less than $1 million decreased at a similar rate to the previous month, recording a fall of close to 15.8% s.e. in real terms. Meanwhile, deposits of more than $1 million cut their rate of decline compared to October. In particular, the segments of $1 to $20 million and more than $20 million would have registered variations of -9.1% s.e. and -6.5% s.e. at constant prices.

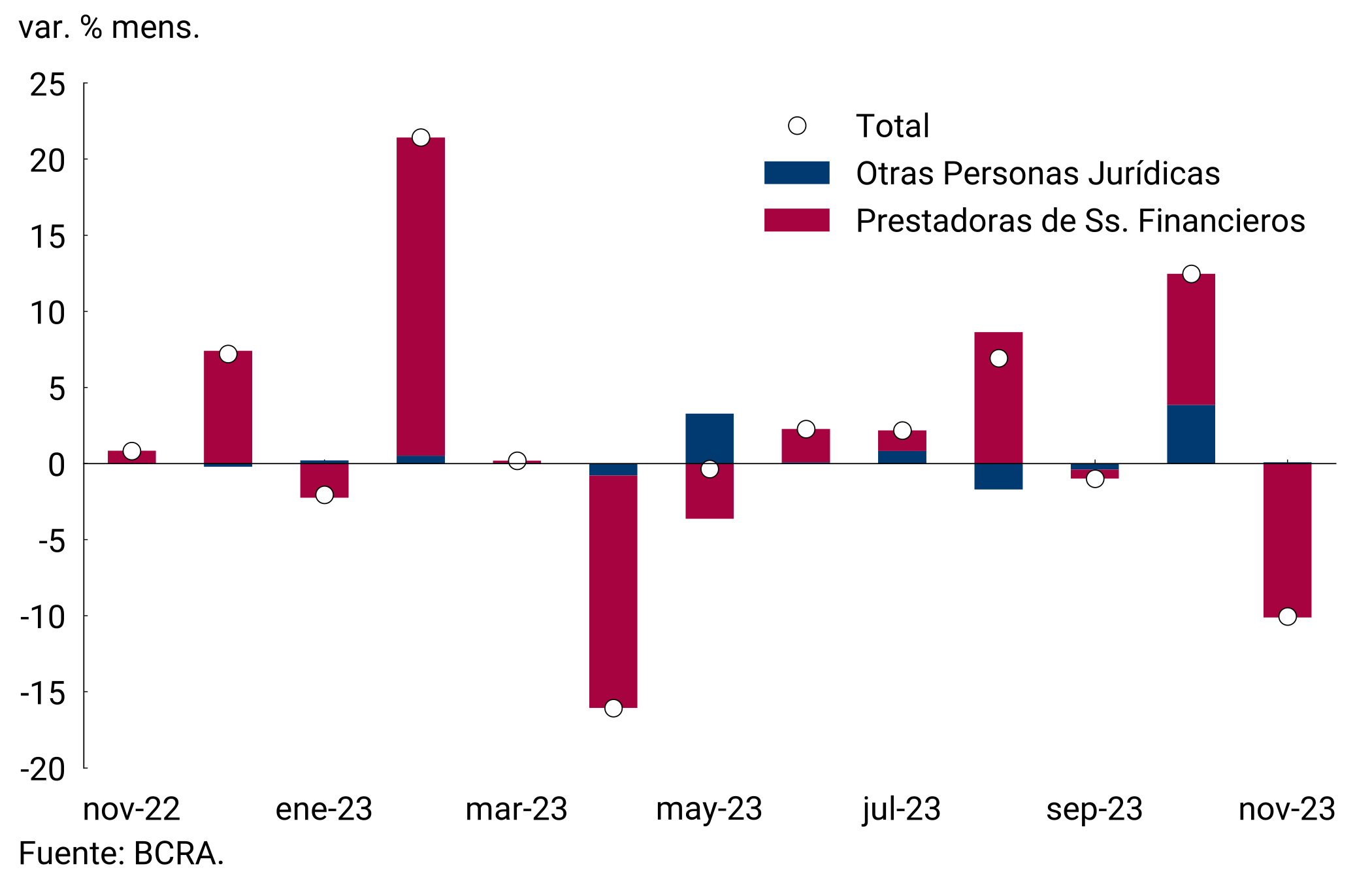

The Financial Services Providers (FSPs) not only dismantled fixed-term deposit positions (more than $20 million), but also interest-bearing demand placements. Thus, the holdings of interest-bearing demand deposits of the PSFs would have registered a decrease in November in real terms of -8% s.e. (see Figure 3.2). This behavior occurred despite the nominal growth in the assets of the Money Market Mutual Funds (FCI MM), which are the main players within the PSF. The freed up funding of these positions was mainly channeled towards passive passes with the BCRA, which reached a record of $4.5 billion at the end of November. This dynamic was impacted by the decrease observed in the interest rates of interest-bearing demand deposits, which implied that this instrument presented a negative spread with respect to the BCRA’s passive passes for FCI.

Figure 3.1 | Time deposits in pesos in the private

sector Contribution to the real monthly var. by amount stratum

Figure 3.2 | Interest-bearing

demand deposits Contribution to the actual monthly var. per holder

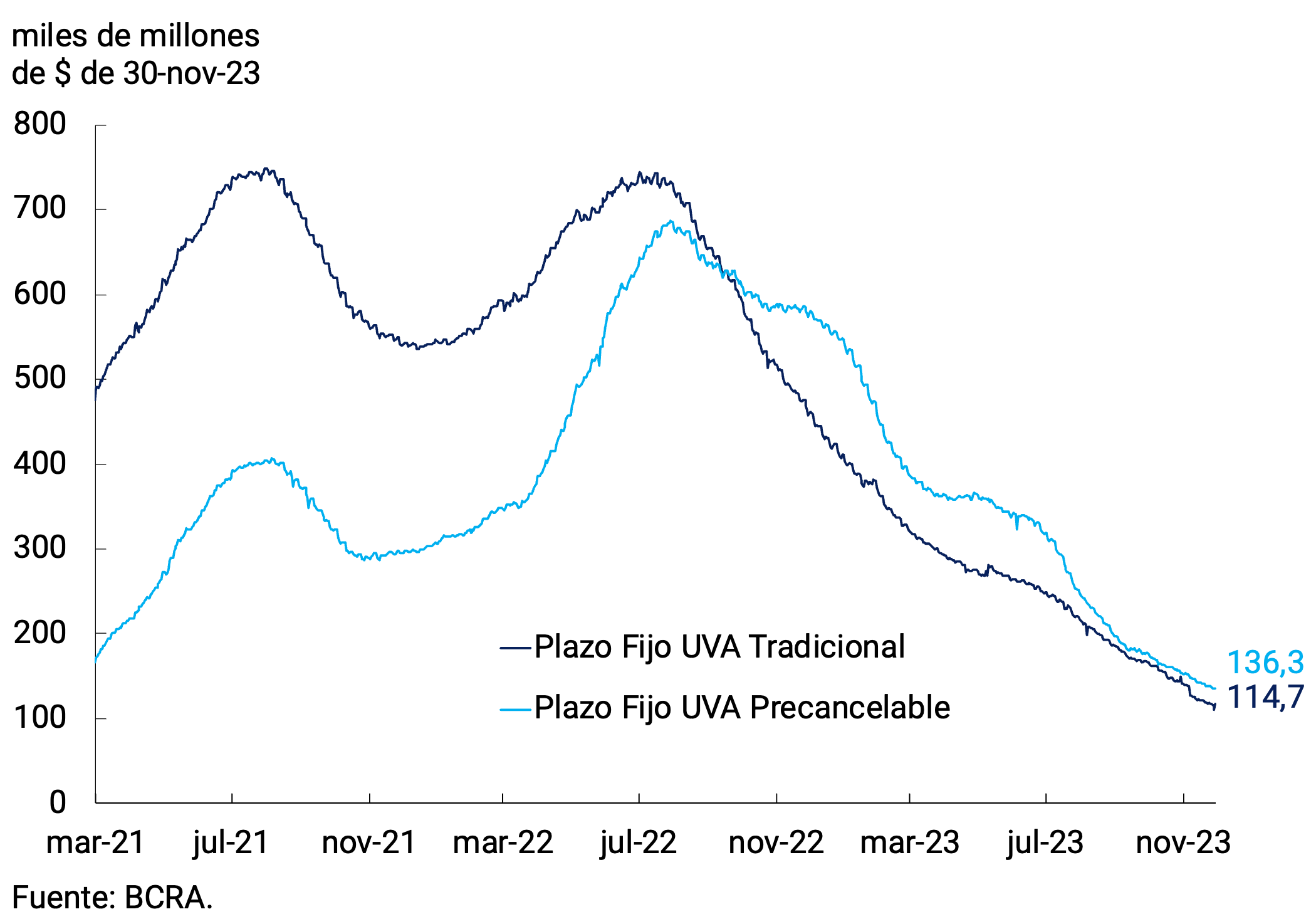

The segment of fixed-term deposits adjustable by CER continued to show a decrease in real terms, accumulating 16 consecutive months of contraction. The fall was verified in both traditional and pre-cancellable UVA placements, whose monthly rates of change were -18.8% s.e. and -12% s.e. respectively (see Chart 3.3). Distinguishing by type of holder, the decrease was mainly due to the dynamics of placements by individuals, which represent almost 69% of the total. All in all, the balance of deposits in UVA reached $248,333 million at the end of November, which is equivalent to 1.9% of the total of term instruments denominated in domestic currency.

On the other hand, deposits adjusted for the value of the reference exchange rate showed an increase in November. By type of deposit, demand placements remained stable in the first part of the month, and then experienced strong growth in the second half. Thus, an average monthly expansion of 9% was observed at constant prices, and an increase of 32% in real terms between balances at the end of the month. On the other hand, fixed-term deposits adjusted for the exchange rate registered a smaller average expansion (1.6% at constant prices; see Figure 3.4) and represent only 0.6% of time deposits. Regarding this type of placement, on the last day of the month, it was provided that financial institutions will no longer be obliged to offer new deposits in demand or term accounts whose remuneration is based on the variation in the exchange rate of the US dollar. This measure is complementary to another by which LEDIV at zero rate (dollar bills liquidable in pesos at the reference exchange rate) was no longer offered to financial institutions as well as to the rest of the admitted subscribers4.

Figure 3.3 | Fixed-term deposits in UVA of the private

sector Balance at constant prices by type of instrument

Figure 3.4 | Deposits adjustable by exchange

rate Balance at current prices

All in all, the broad monetary aggregate, private M35, at constant prices and adjusted for seasonality, would have exhibited a monthly fall of 8.5% in November. In the year-on-year comparison, this aggregate would have registered a decrease of 23% and as a percentage of GDP it would have stood at 14.3%, 0.8 p.p. below the previous month’s record.

4. Monetary base

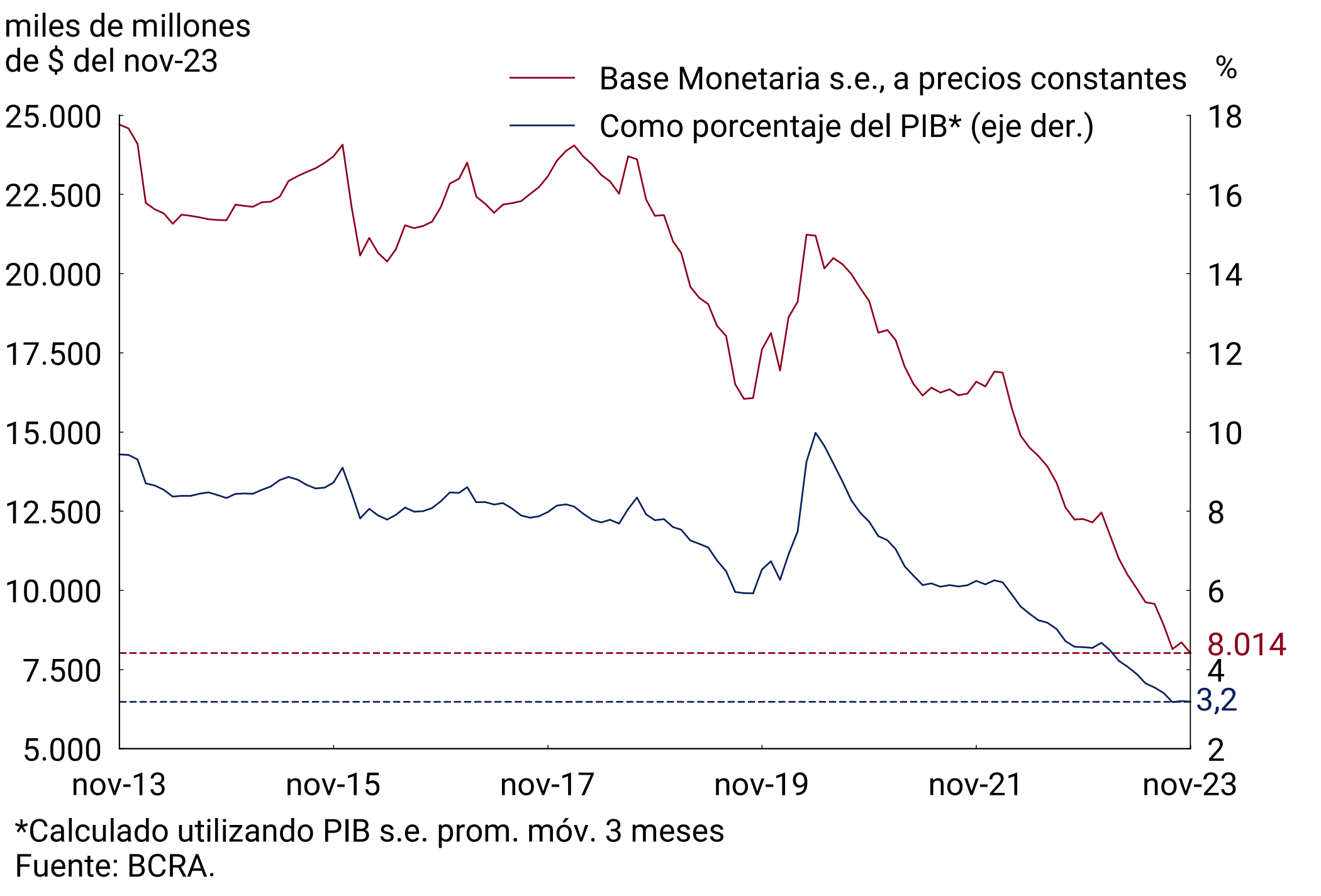

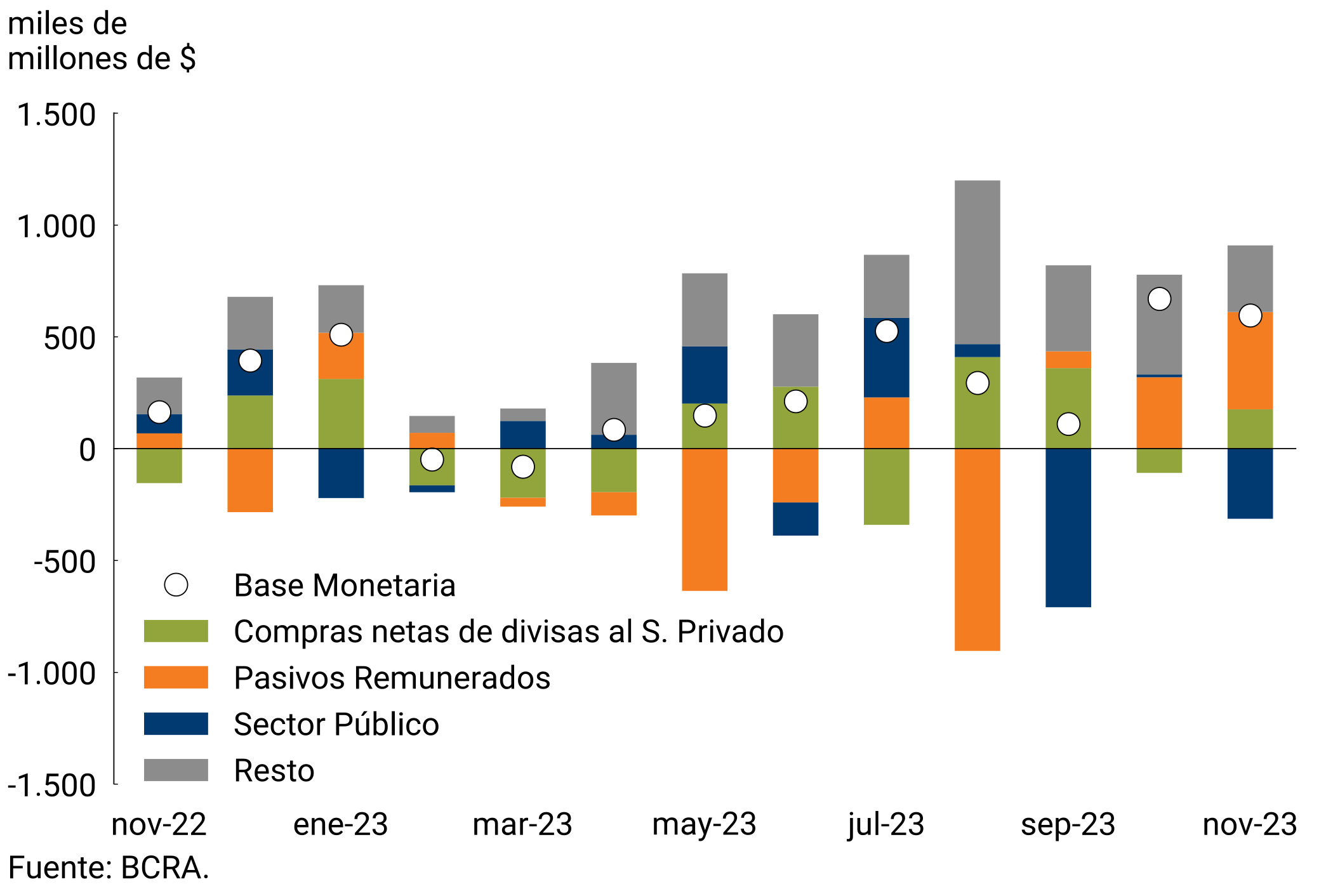

In November, the average balance of the Monetary Base was $7,798 billion, which implied a monthly expansion of 8.3% ($595 billion) at current prices. However, adjusted for seasonality and at constant prices, it would have exhibited a contraction of 4.0%, accumulating a fall of 34.6% in the last twelve months. As a GDP ratio, the Monetary Base would stand at 3.2%, remaining practically unchanged from October and among its lowest values since the exit from convertibility (see Figure 4.1).

Figure 4.1 | Monetary base

Figure 4.2 | Factors explaining the Monetary Base

Average monthly change

On the supply side of the Monetary Base, most of the variation factors were expansionary. The BCRA’s interest-bearing liabilities generated an expansion of liquidity. Operations with public securities in the secondary market and the execution of put option contracts on national government securities by financial institutions also generated monetary expansion, as did the net purchase of foreign currency from the private sector. Meanwhile, public sector operations had a contractionary effect on average in November (see Figure 4.2).

Finally, it should be noted that the BCRA decided to keep its benchmark interest rates unchanged in November, after raising them by 15 p.p. the previous month. Thus, the interest rate on the LELIQ with a 28-day term remained at 133% n.a. (254.8% y.a.), while the interest rate on the LELIQ with a 180-day term remained at 135.5% n.a. (182.3% y.a.). As for shorter-term instruments, the interest rate on 1-day pass-by-passes stood at 126% n.a. (251.8% y.a.); Meanwhile, the interest rate on 1-day active passes stands at 160% n.a. (393.6% e.a.). Finally, the NOTALIQ spread remained at 2.5 p.p.

5. Loans to the private sector

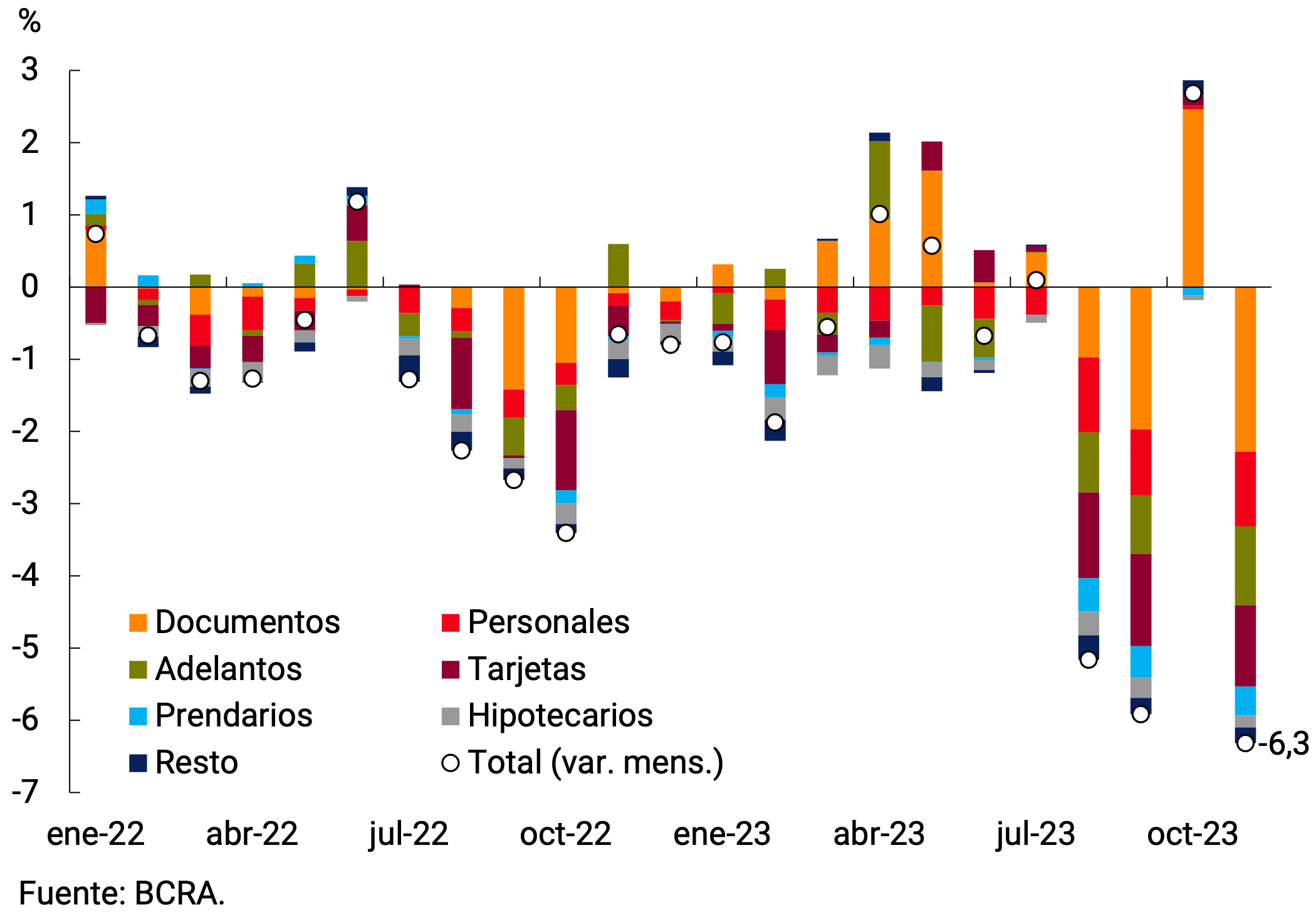

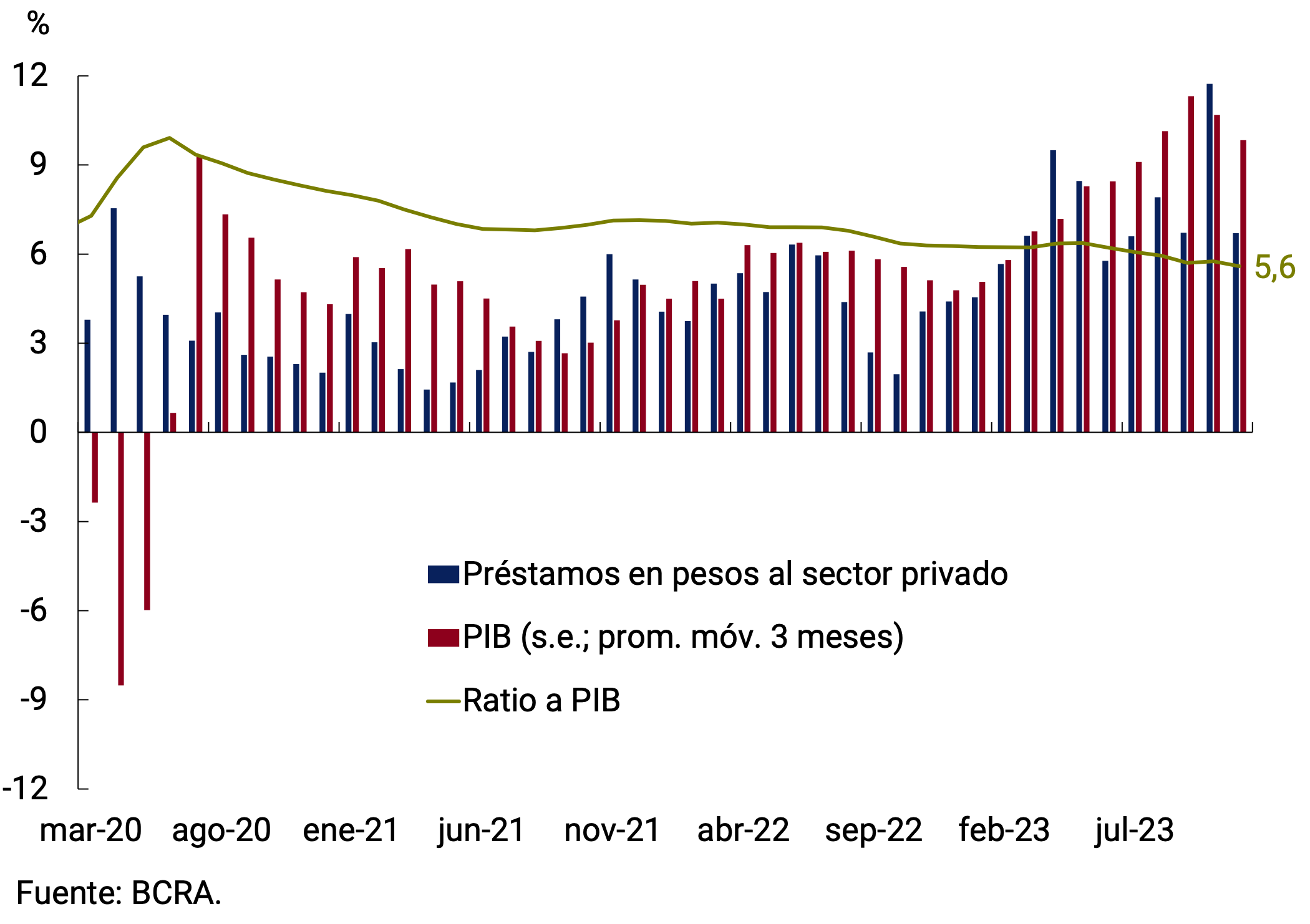

Loans in pesos to the private sector in real terms and without seasonality registered a marked contraction after the recovery exhibited in October. In fact, in November they would have exhibited a decrease at constant prices of 6.3% s.e. and in the last 12 months they would accumulate a fall of around 16.5%. At the level of large lines of credit, the fall was extended to all financing (see Figure 5.1). As a percentage of GDP, loans in pesos to the private sector would stand at 5.6%, the lowest level in the last 20 years (see Figure 5.2).

Figure 5.1 | Loans in pesos to the private

sector Real without seasonality; contribution to monthly growth

Figure 5.2 | Loans in pesos to the private

sector In terms of GDP

Commercial lines would have shown the greatest decrease, with a monthly drop of 7.7% s.e. in real terms and would be 8.3% below the record of a year ago. At the instrument level, loans granted through documents would have contracted in November 7.2% s.e. and would be 3.7% above their level a year ago. Within these lines, single-signature documents, with a longer average term, would have registered a decrease of 6.5% s.e. Meanwhile, discounted securities would have fallen 7.7% s.e. in the month. For its part, advances would have contracted 10.5% s.e., and would be 28.0% below the level of November 2022.

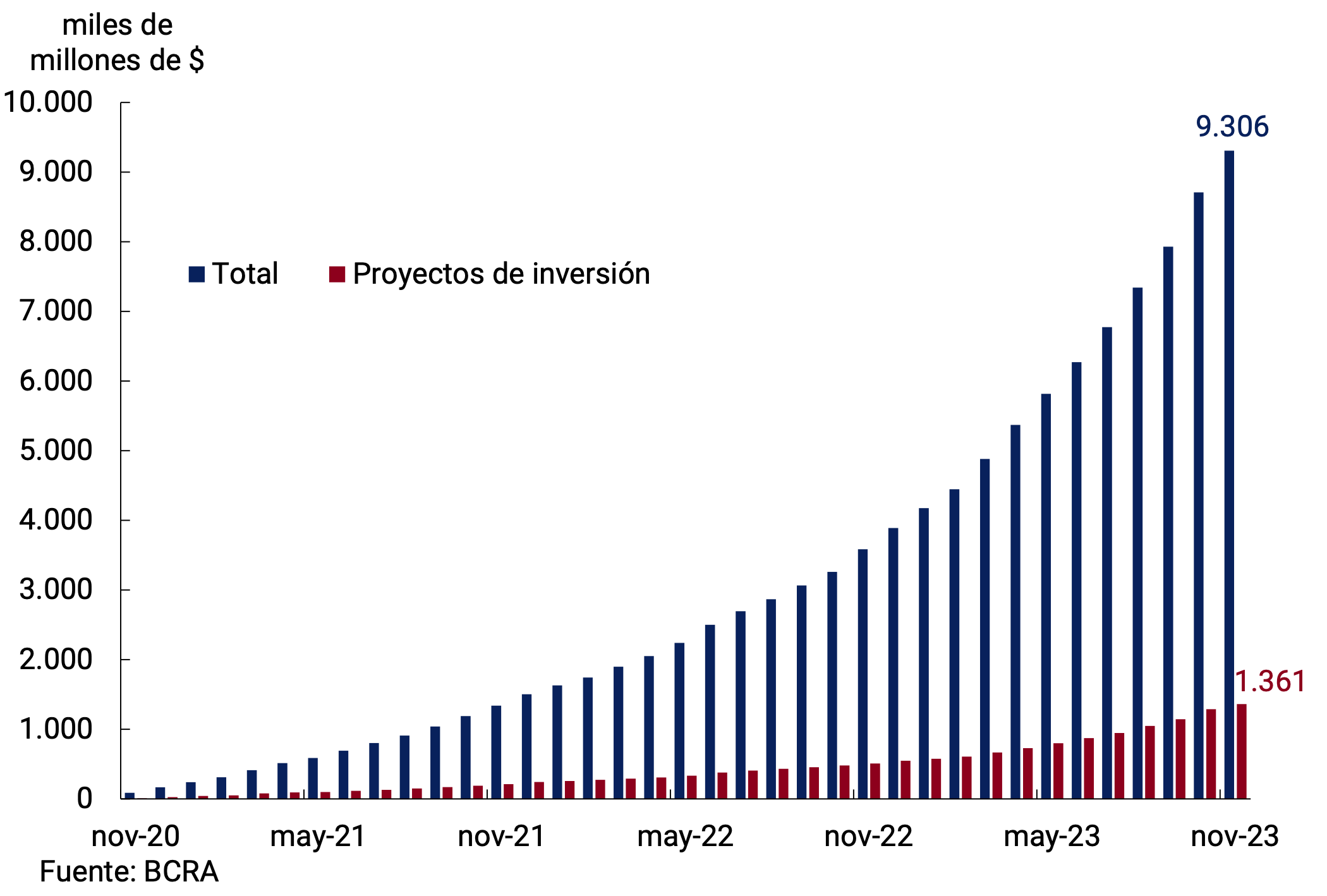

The Financing Line for Productive Investment (LFIP) continued to channel credit to the productive activity of Micro, Small and Medium-sized Enterprises (MSMEs). At the end of November, loans granted under the LFIP accumulated $9.306 billion since its launch, an increase of 6.9% compared to last month (see Figure 5.3). Of the total financing granted through the LFIP, 14.6% corresponds to investment projects and the rest to working capital. The average balance of financing granted through the LFIP reached approximately $2,527 billion in October (latest available information), which represents about 19% of total loans and 40.1% of total commercial loans.

Classifying commercial loans according to the type of debtor, credit to MSMEs was around 1.3% of GDP, slightly above the pre-pandemic record and the historical average. In the case of large companies, the credit-to-GDP ratio was at a level similar to that of MSMEs, unchanged from October (see Figure 5.4).

Figure 5.3 | Financing granted through the Productive Investment Financing Line (LFIP)

Accumulated disbursed amounts; data at the end of the month

Figure 5.4 | Commercial Loans by Type of Debtor

As a Percentage of GDP

For their part, consumer loans would have registered a drop of 5.0% s.e. at constant prices during the month and would accumulate a fall of 19.7% in the last year. Financing instrumented with credit cards would have shown a contraction in real terms of 3.8% s.e. in the month, while personal loans would have fallen 7.8% s.e. in the same period. In year-on-year terms, these loans registered variations of -12.5% and -32.7% at constant prices, respectively.

With regard to lines with real collateral, in real terms, collateral loans would have registered a decrease of 6.5% s.e., bringing the year-on-year fall to 25.7%. For its part, the balance of mortgage loans would have shown a monthly decrease of 4.2% s.e. (-42.8% y.o.y.).

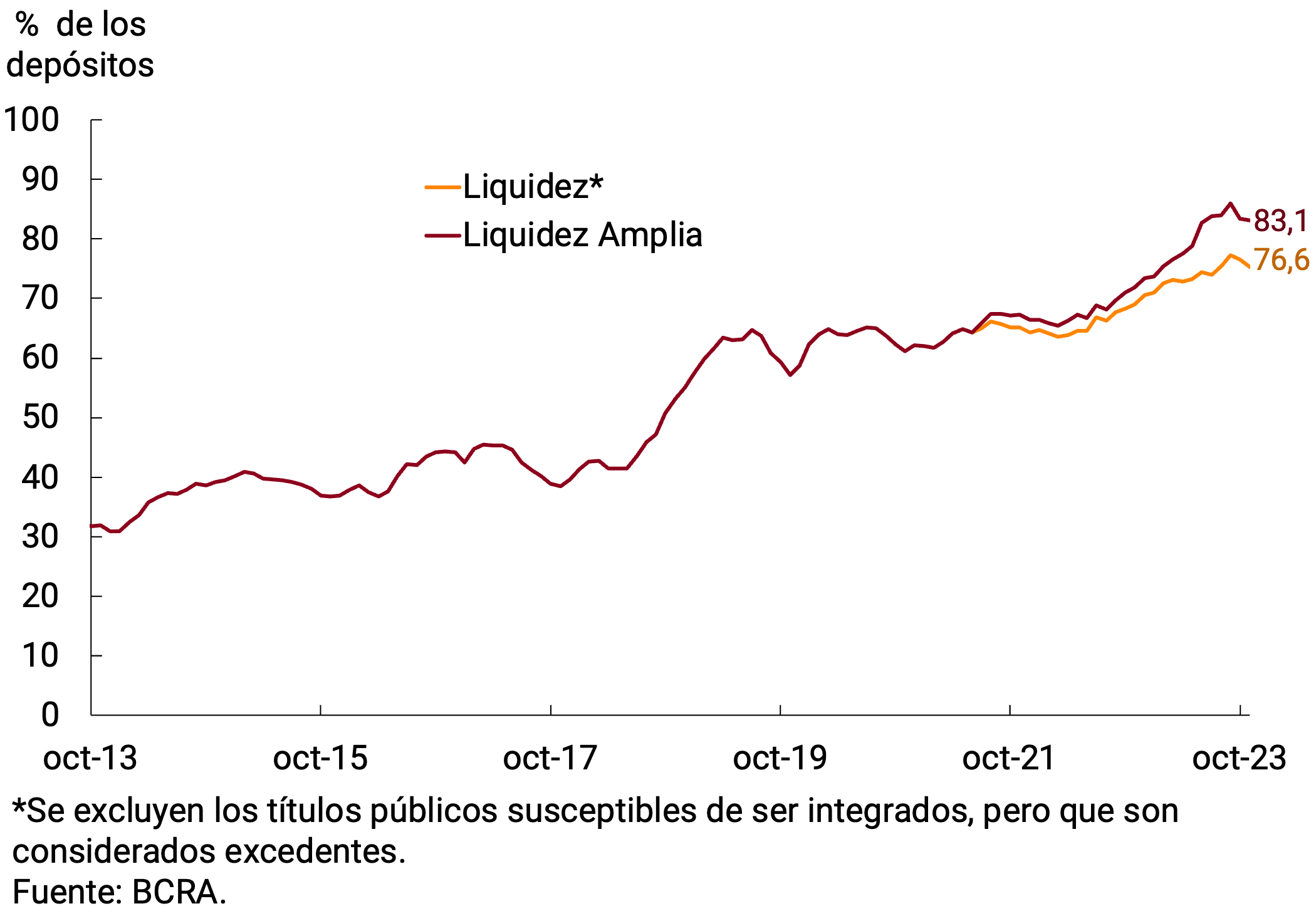

6. Liquidity in pesos of financial institutions

In November, ample bank liquidity in local currency6 fell 0.3 p.p. compared to the previous month, averaging 83.1% of deposits, remaining at historically high levels (see Figures 6.1 and 6.2). This fall was mainly explained by the holding of interest-bearing liabilities of the BCRA by the entities, partially offset by the increase in current accounts at the Central Bank. The latter is associated both with an increase in the minimum cash requirement as a result of the growth in demand deposits in October, and with the surplus position maintained by financial institutions.

Within interest-bearing liabilities, a transfer of funds from LELIQ at 28 days to passive passes at 1 day was observed. Thus, the latter increased their participation in the total of instruments, reaching a representativeness of 52% with peak data at the end of the month. On the other hand, the LELIQ with a 28-day term represented, at the end of the month, 38% of the total, reducing their relative share. LEDIV and LEGAR closed November representing 10% of total interest-bearing liabilities, with an increase. The rest was made up of the longer-term species, concentrated exclusively in NOTALIQ, which represented only 0.1% of the balance.

Figure 6.1 | Liquidity levels in pesos of financial institutions

Figure 6.2 | Composition of liquidity of financial

institutions % of deposits

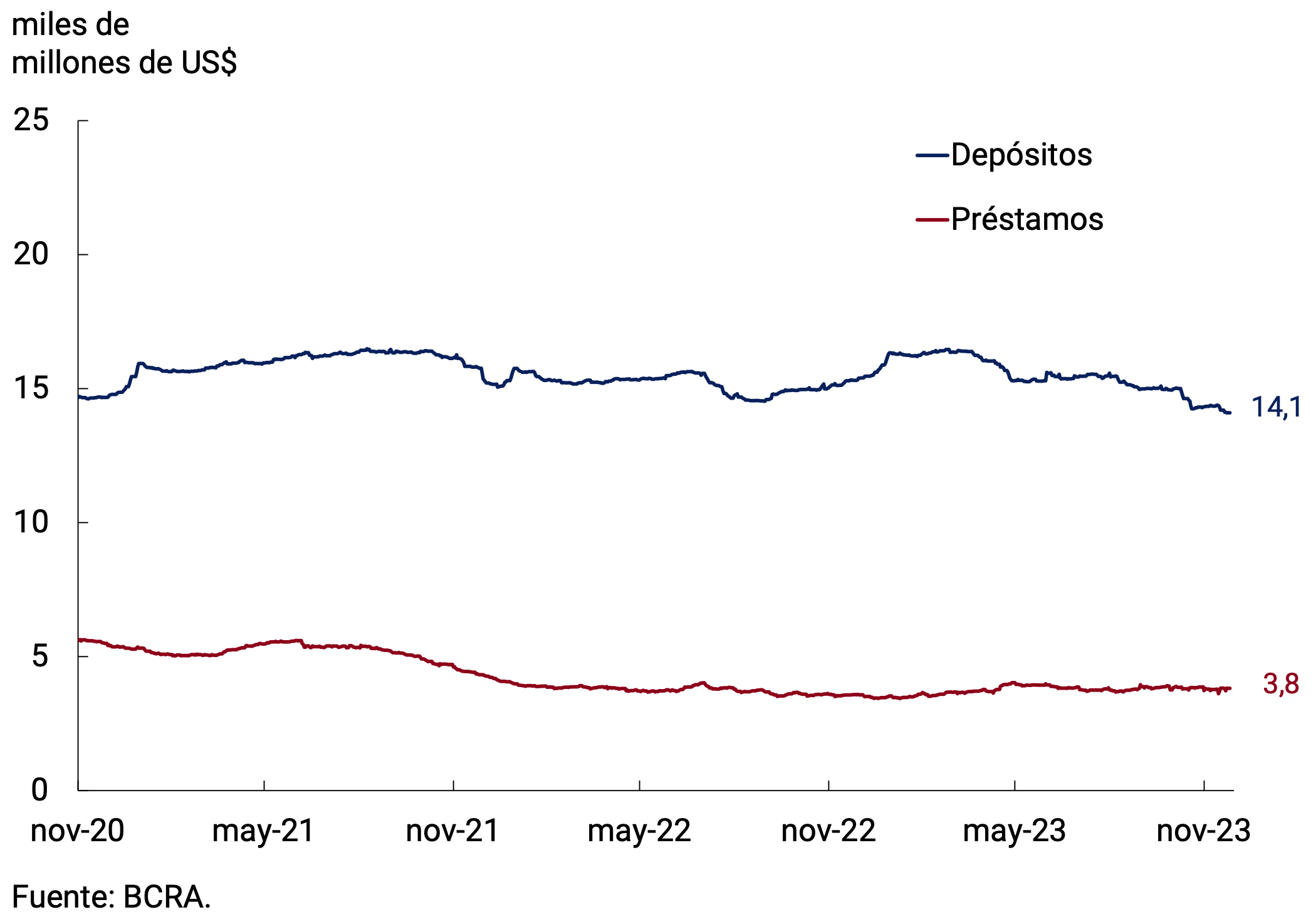

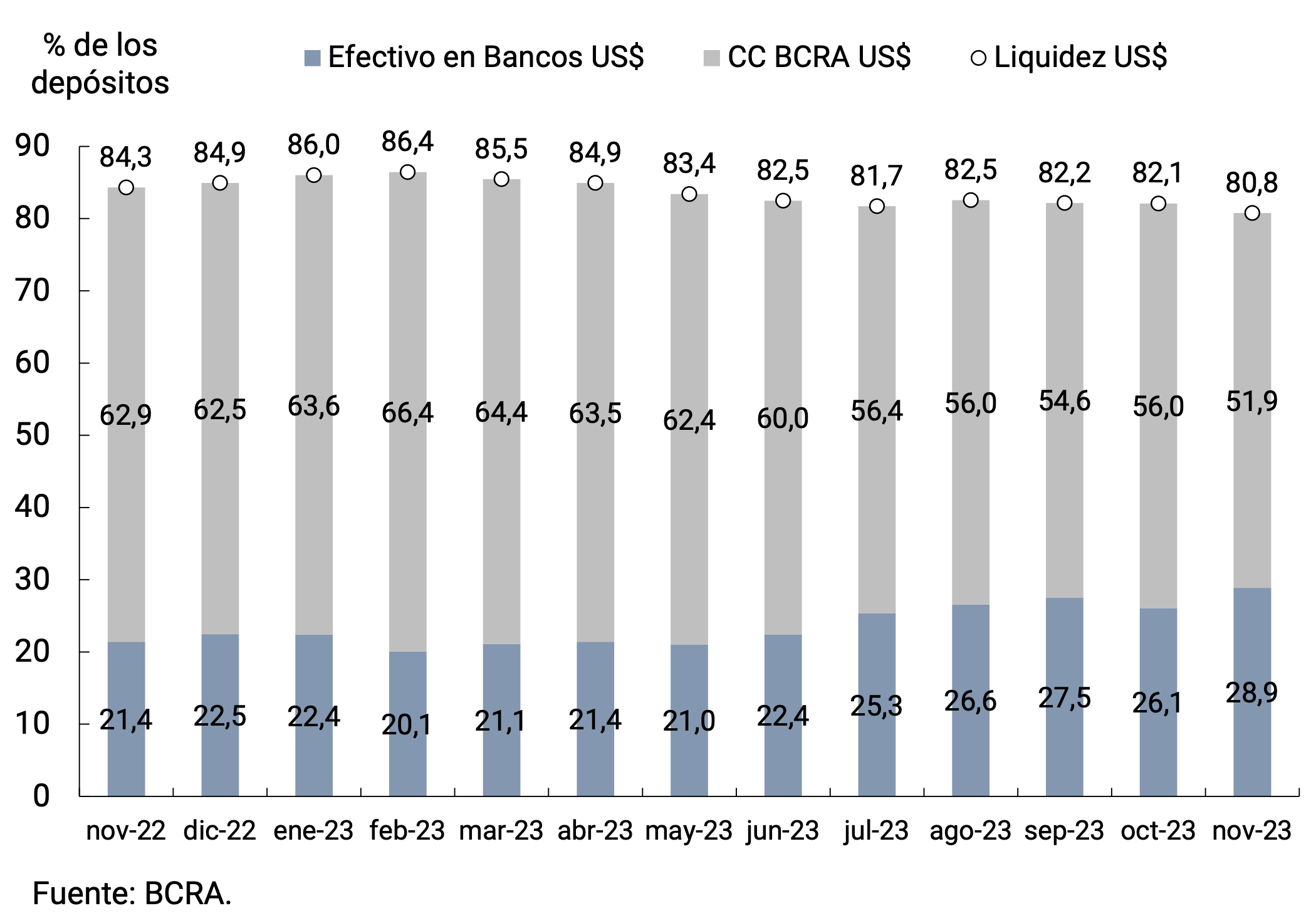

7. Foreign currency

In the foreign currency segment, the main assets and liabilities of financial institutions showed negative variations. On the one hand, private sector deposits fell by US$181 million in the month and ended October with a balance of US$14,136 million. This drop was concentrated in the deposits of human persons. On the other hand, the balance of loans to the private sector fell by US$96 million and ended the month at US$3,773 million (see Figure 7.1).

Figure 7.1 | Balance of private sector foreign currency deposits and loans

Figure 7.2 | Liquidity in foreign currency of financial institutions

The liquidity of financial institutions in the foreign currency segment stood at 80.8% of deposits, remaining at historically high levels. In terms of its composition, an increase in cash in banks was observed to the detriment of current accounts in the BCRA (see Figure 7.2).

During the month, some regulatory modifications were made in foreign exchange matters, among which it is possible to mention the relaxation of the requirements for customers who access the foreign exchange market to make payments for services to non-residents provided that they meet certain conditions mentioned in regulation7. Modifications were also made related to foreign exchange market revenues from the sale of non-financial assets8. On the other hand, the Federal Administration of Public Revenues (AFIP) increased from 45% to 100% the collection of income tax applied to operations covered by the PAIS Tax. Thus, the total surcharge on the value of the exchange rate for purchases and expenses abroad became, as of November 22, 155% (30% PAIS tax, 25% perception of personal assets and 100% perception of profits)9.

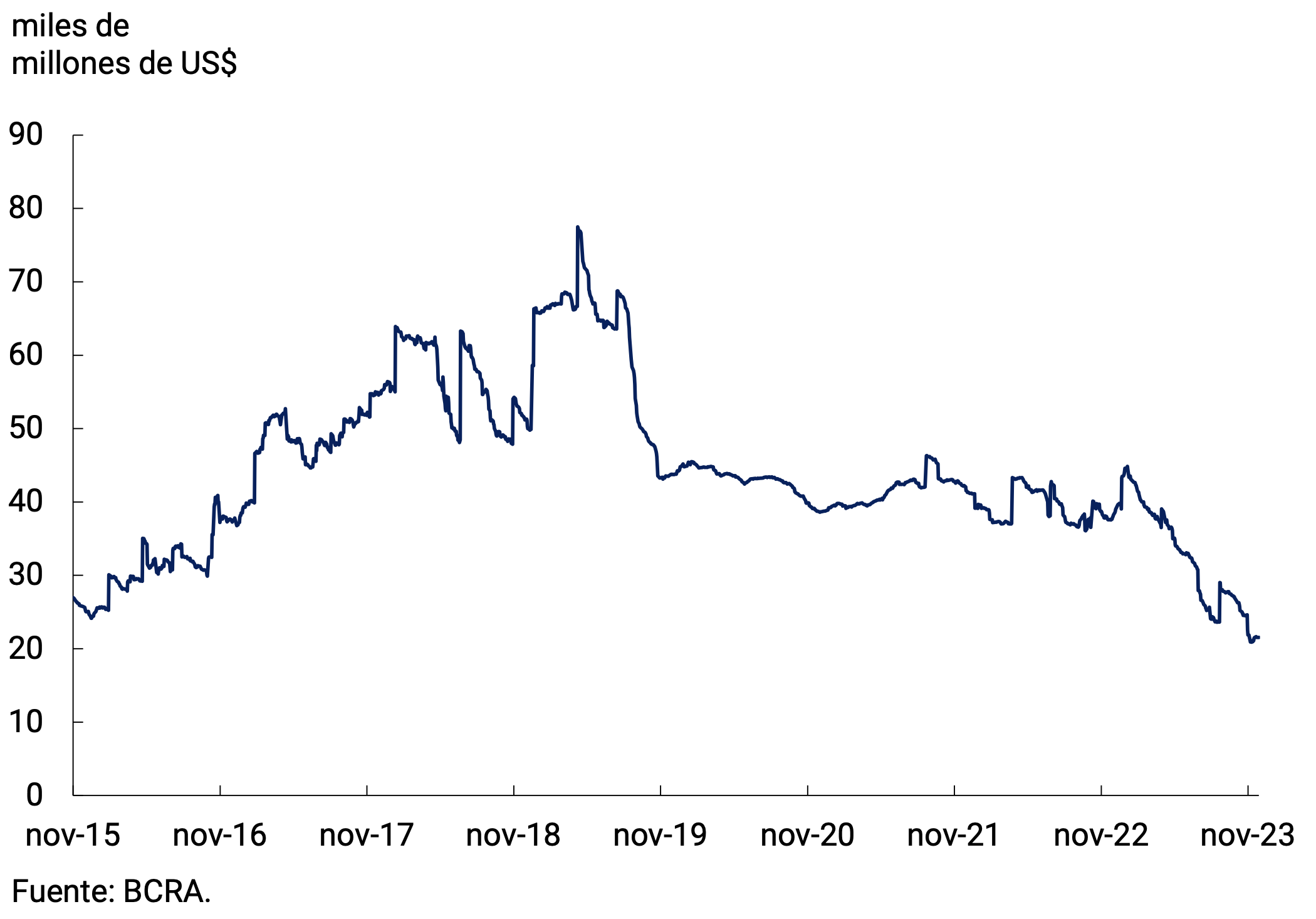

The BCRA’s International Reserves ended November with a balance of US$21,513 million, registering a fall of US$1,046 million compared to the end of October. This dynamic was influenced by the payment of principal and interest to the International Monetary Fund in the first days of the month. Specifically, these payments totaled US$1,663 million. This decline was partially offset by net foreign exchange purchases and exchange differences (see Figure 7.3).

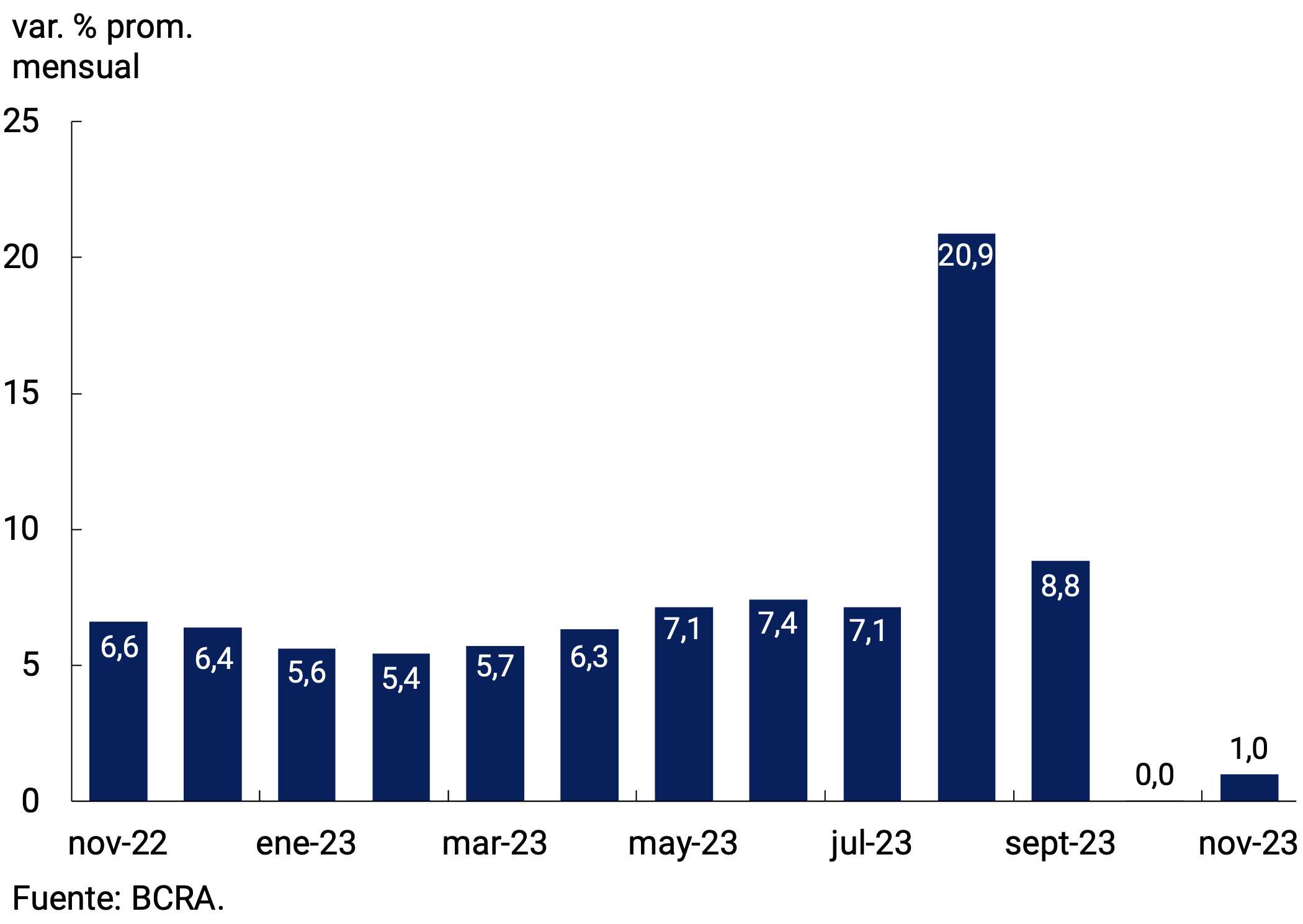

Finally, since the middle of the month, the BCRA began to adjust the bilateral nominal exchange rate (TCN) against the US dollar. Thus, the TCN registered an average increase of 0.98% compared to the previous month, ending the month at $360.53/US$ (see Figure 7.4).

Figure 7.3 | International Reserve Balance

Figure 7.4 | Bilateral Nominal Exchange Rate against the US Dollar

Glossary

ANSES: National Social Security Administration.

AFIP: Federal Administration of Public Revenues.

BADLAR: Interest rate on fixed-term deposits for amounts greater than one million pesos and a term of 30 to 35 days.

BCRA: Central Bank of the Argentine Republic.

BM: Monetary Base, includes monetary circulation plus deposits in pesos in current account at the BCRA.

CC BCRA: Current account deposits at the BCRA.

CER: Reference Stabilization Coefficient.

NVC: National Securities Commission.

SDR: Special Drawing Rights.

E.A.: Effective Annual.

EFNB: Non-Banking Financial Institutions.

EM: Minimum Cash.

FCI: Common Investment Fund.

A.I.: Year-on-year .

IAMC: Argentine Institute of Capital Markets

CPI: Consumer Price Index.

ITCNM: Multilateral Nominal Exchange Rate Index

ITCRM: Multilateral Real Exchange Rate Index

LEBAC: Central Bank bills.

LELIQ: Liquidity Bills of the BCRA.

LFIP: Financing Line for Productive Investment.

M2 Total: Means of payment, which includes working capital held by the public, cancelling cheques in pesos and demand deposits in pesos from the public and non-financial private sector.

Private M2: Means of payment, includes working capital held by the public, cancelling cheques in pesos and demand deposits in pesos from the non-financial private sector.

Private transactional M2: Means of payment, includes working capital held by the public, cancelling cheques in pesos and non-remunerated demand deposits in pesos from the non-financial private sector.

M3 Total: Broad aggregate in pesos, includes the current currency held by the public, cancelling checks in pesos and the total deposits in pesos of the public and non-financial private sector.

Private M3: Broad aggregate in pesos, includes the working capital held by the public, cancelling checks in pesos and the total deposits in pesos of the non-financial private sector.

MERVAL: Buenos Aires Stock Market.

MM: Money Market.

N.A.: Annual nominal.

NOCOM: Cash Clearing Notes.

ON: Negotiable Obligation.

GDP: Gross Domestic Product.

P.B.: basis points.

PSP.: Payment Service Provider.

p.p.: percentage points.

MSMEs: Micro, Small and Medium Enterprises.

ROFEX: Rosario Term Market.

S.E.: No seasonality

SISCEN: Centralized System of Information Requirements of the BCRA.

SIMPES: Comprehensive System for Monitoring Payments of Services Abroad.

TCN: Nominal Exchange Rate

IRR: Internal Rate of Return.

TM20: Interest rate on fixed-term deposits for amounts greater than 20 million pesos and a term of 30 to 35 days.

TNA: Annual Nominal Rate.

UVA: Unit of Purchasing Value

References

1 Corresponds to private M2 excluding interest-bearing demand deposits from companies and financial service providers. This component was excluded since it is more similar to a savings instrument than to a means of payment.

2 The interest rates currently in force are those established by communication “A” 7862.

3 The rest of the depositors are made up of individuals with deposits of more than $30 million and legal entities.

4 Communication “A” 7898.

5 The private M3 includes the working capital held by the public and the deposits in pesos of the non-financial private sector (demand, time and others).

6 Includes current accounts at the BCRA, cash in banks, balances of net passes arranged with the BCRA, holdings of LELIQ and NOTALIQ, and public bonds eligible for reserve requirements.

7 Communications “A” 7893.

8 Communications “A” 7894.

9 AFIP General Resolution 5450/2023.

Share on