1. Executive Summary

In real and seasonally adjusted terms, the means of payment (private transactional M2) would have registered a new increase in November. In the month, the entry of salary adjustment brackets of several unions and the payment of the monthly supplement for the Family Salary were impacted.

In a context of greater dynamism of the means of payment, fixed-term deposits would have contracted in real terms in the month. In terms of instruments, the demand was concentrated on those with a shorter term. In particular, the increase in investments with early cancellation option was highlighted, both in the segment of pesos and instruments adjustable by CER.

Loans in pesos to the non-financial private sector grew in real terms for the third consecutive month, marking the largest increase since the beginning of 2020 and ranking among the highest records in the last 15 years. The boost came mainly from commercial lines and was generalized by type of debtor (MSMEs and large companies).

In the foreign currency segment, the main assets and liabilities of financial institutions showed negative variations. In a context in which bank liquidity in foreign currency remains at record levels (above 80% of deposits), financial institutions faced the withdrawal of deposits without inconvenience.

2. Payment methods

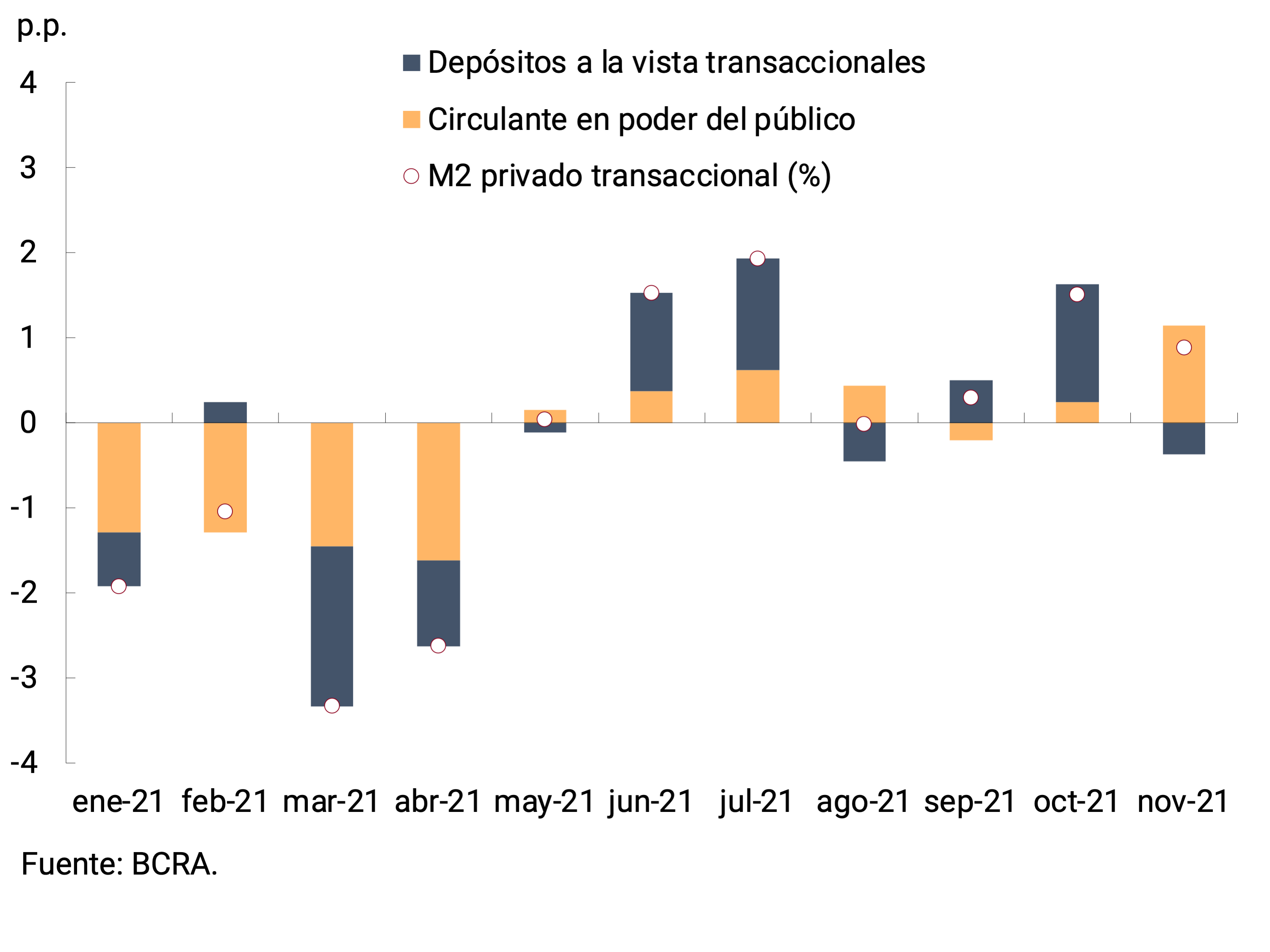

In real terms1 and seasonally adjusted (s.e.), means of payment (private transactional M22) would have registered a new increase in November. This dynamic was mainly explained by the behavior of working capital held by the public, given that non-interest-bearing demand deposits contributed negatively to the variation of the month (see Charts 2.1).

Among the factors that impacted during the month on the evolution of the means of payment, it is possible to point out the entry of tranches of salary adjustments agreed in parity by several unions of wide scope. Likewise, towards the end of October, ANSES began to pay the monthly supplement for the Family Salary, a payment that was repeated in the first days of November. This supplement is intended for registered workers with family incomes of up to $115,062, single-tax people (categories A, B, C and D) and holders of Unemployment Benefit who have dependent children and who are receiving family allowances3. It should be noted that lower-income sectors make more intensive use of cash, which also helped explain the greater demand for banknotes and coins.

Figure 2.1 | Private transactional M2 at constant

prices Contribution by component to the monthly vari. s.e.

Figure 2.2 | Transactional private M2 in terms of GDP

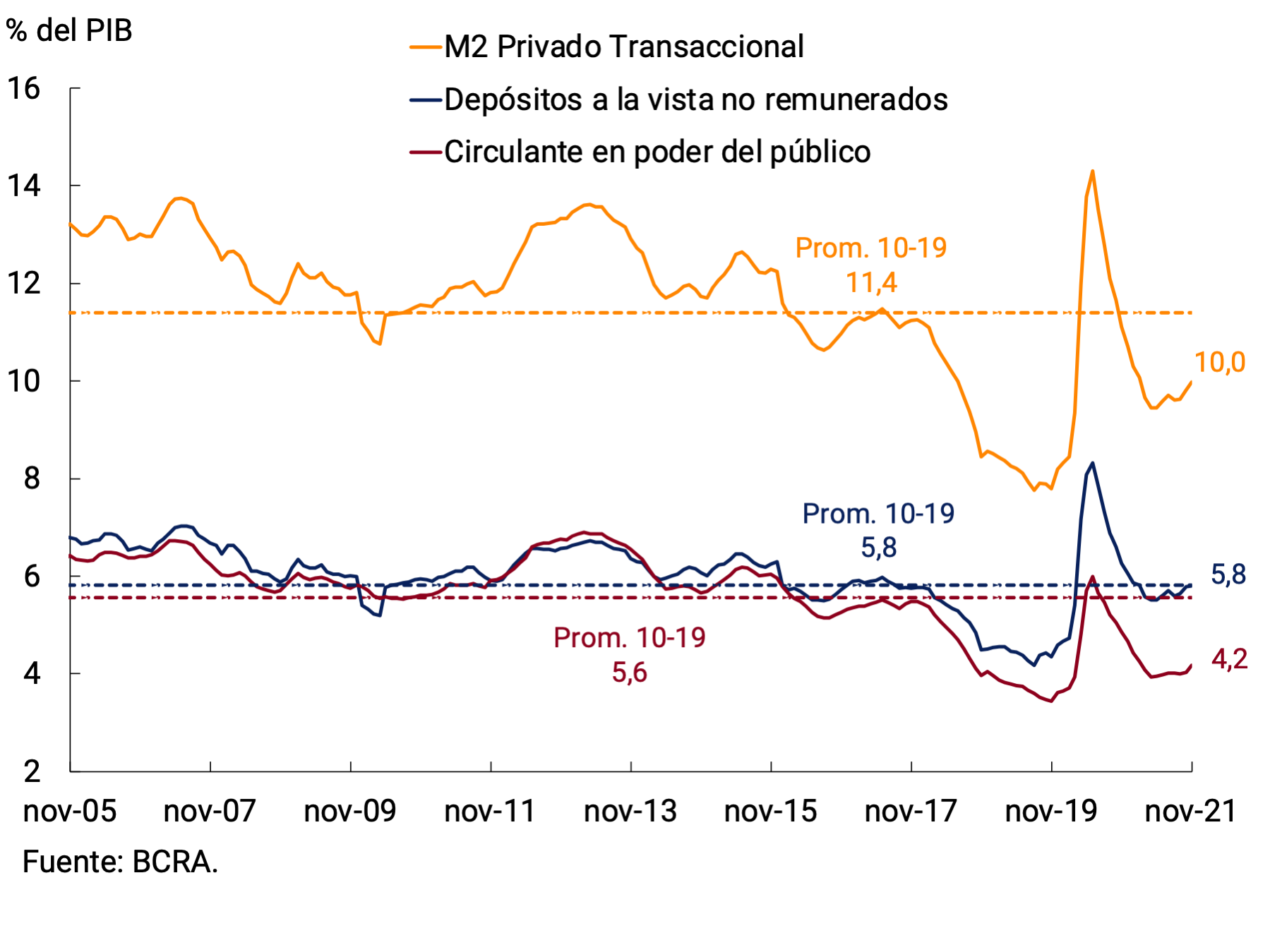

The transactional private M2 in terms of output continued to be below the average record for the 2010-2019 period. This was mainly explained by the dynamics of the circulating currency held by the public, given that the transactional view was around the historical average. In fact, banknotes and coins in the hands of the public were positioned 1.4 p.p. below the average recorded between 2010 and 2019 and at a value close to the minimum of the last 15 years (see Figure 2.2).

3. Savings instruments in pesos

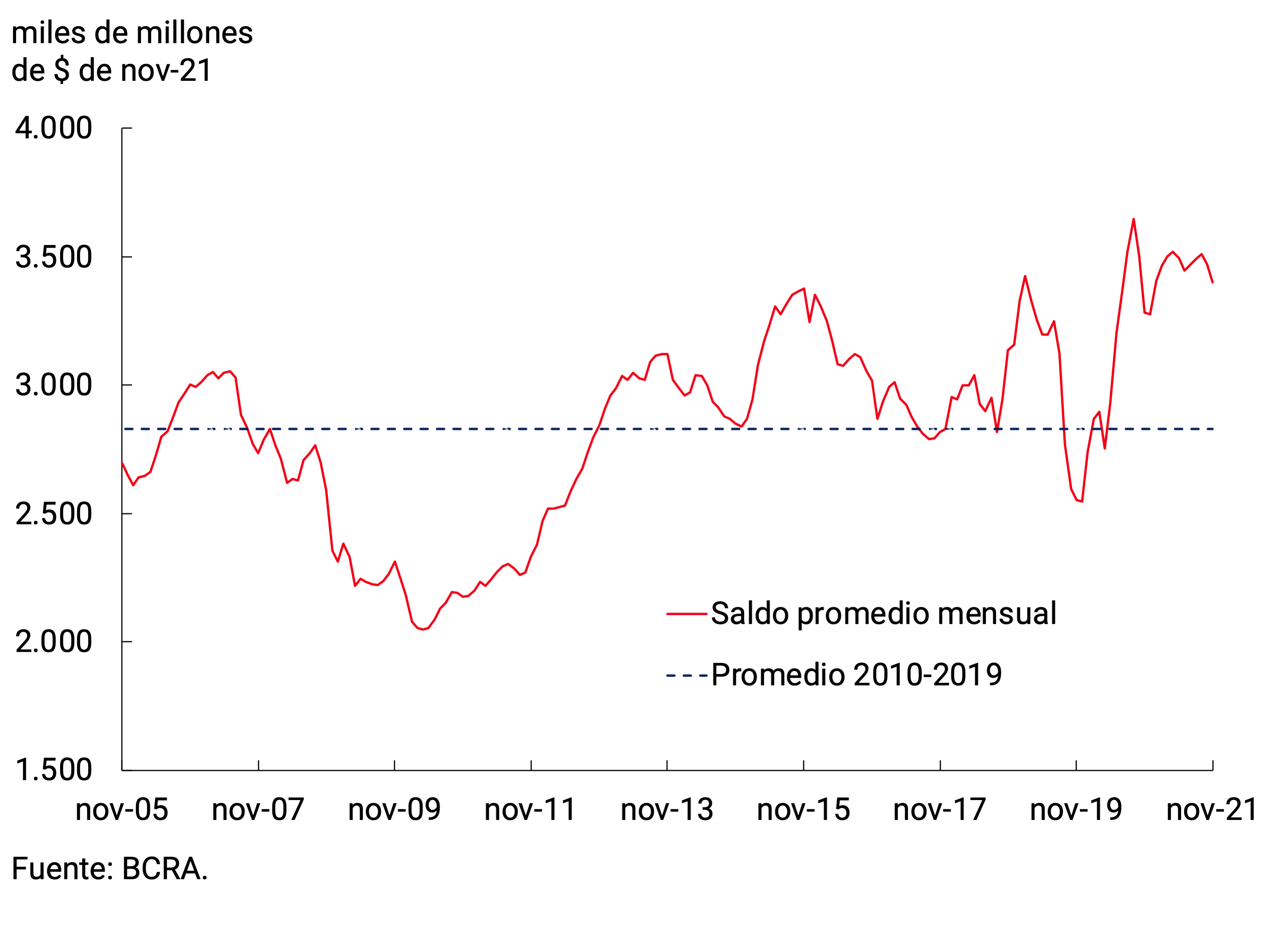

The greater dynamism of transactional means of payment was correlated with a lower demand for fixed-term instruments. In November, fixed-term deposits in pesos in the private sector would have registered a contraction in real terms. It should be noted, however, that time deposits at constant prices remain at 15-year highs (see Figure 3.1).

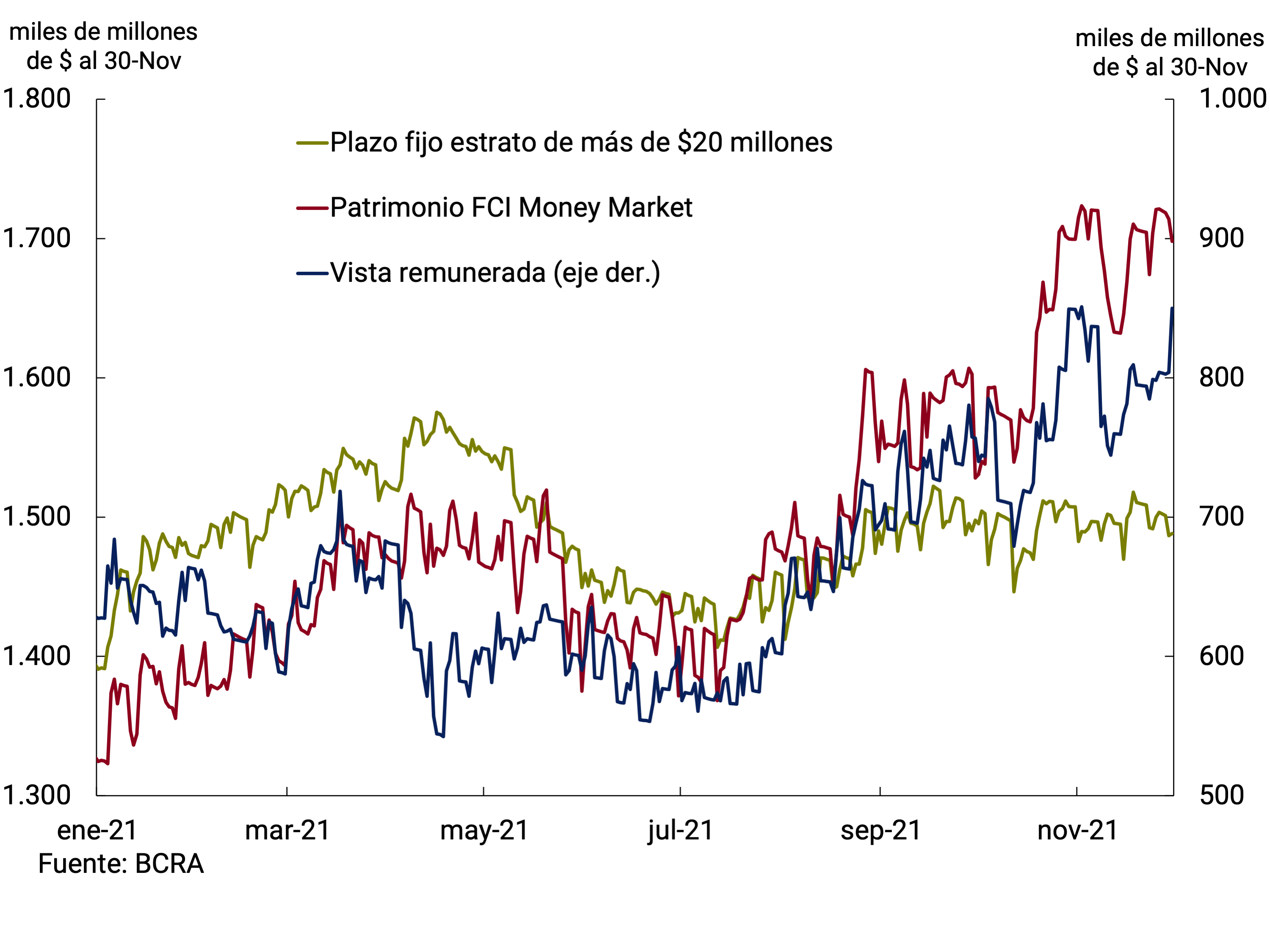

The fall of the month was concentrated in deposits of lower strata of amount. Deposits of less than $1 million at constant prices continued the downward trend of previous months. The interest rate on these deposits paid to individuals stood at 36.3% n.a. (43.0% e.a.)4 on average for the month. Placements of between $1 and $20 million also showed a drop, although of a smaller magnitude. Meanwhile, placements in the wholesale segment (more than $20 million) remained relatively stable at constant prices. The latter were influenced by the behavior of the Mutual Funds of Money Market (FCI MM), which are an important agent of this layer of amount. In fact, throughout the month the FCI MM accommodated equity changes through movements in interest-bearing demand deposits, keeping their holdings of term instruments practically unchanged (see Chart 3.2). The yield on time deposits of more than $20 million (TM20 from private banks) remained at 33.9% n.a. (39.8% y.a.).

Figure 3.1 | Fixed-term deposits in pesos of the private

sector Balance at constant prices

Figure 3.2 | Fixed-term deposits of more than $20 million, equity of the FCI MM and interest-bearing

view Balance at constant prices

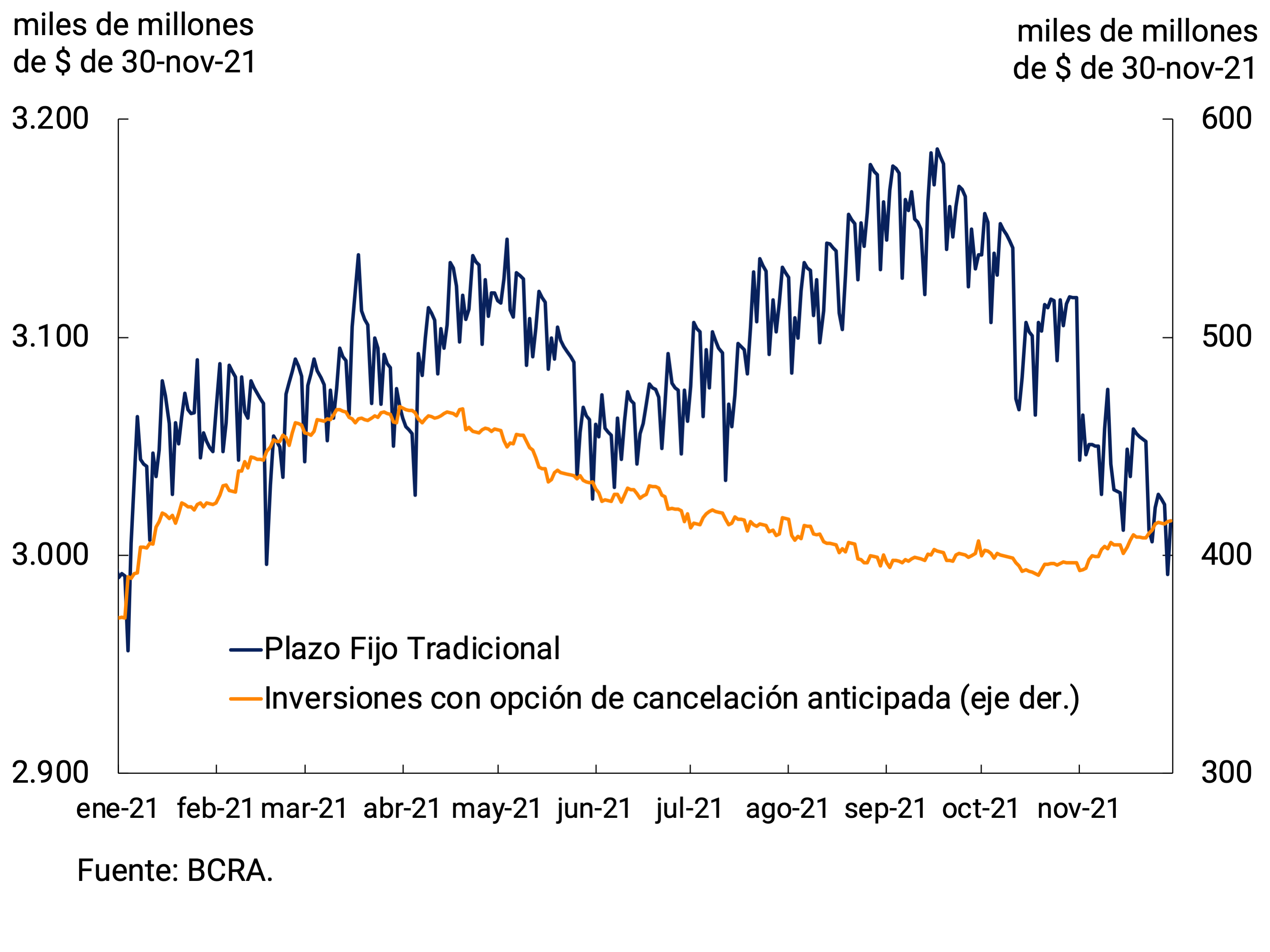

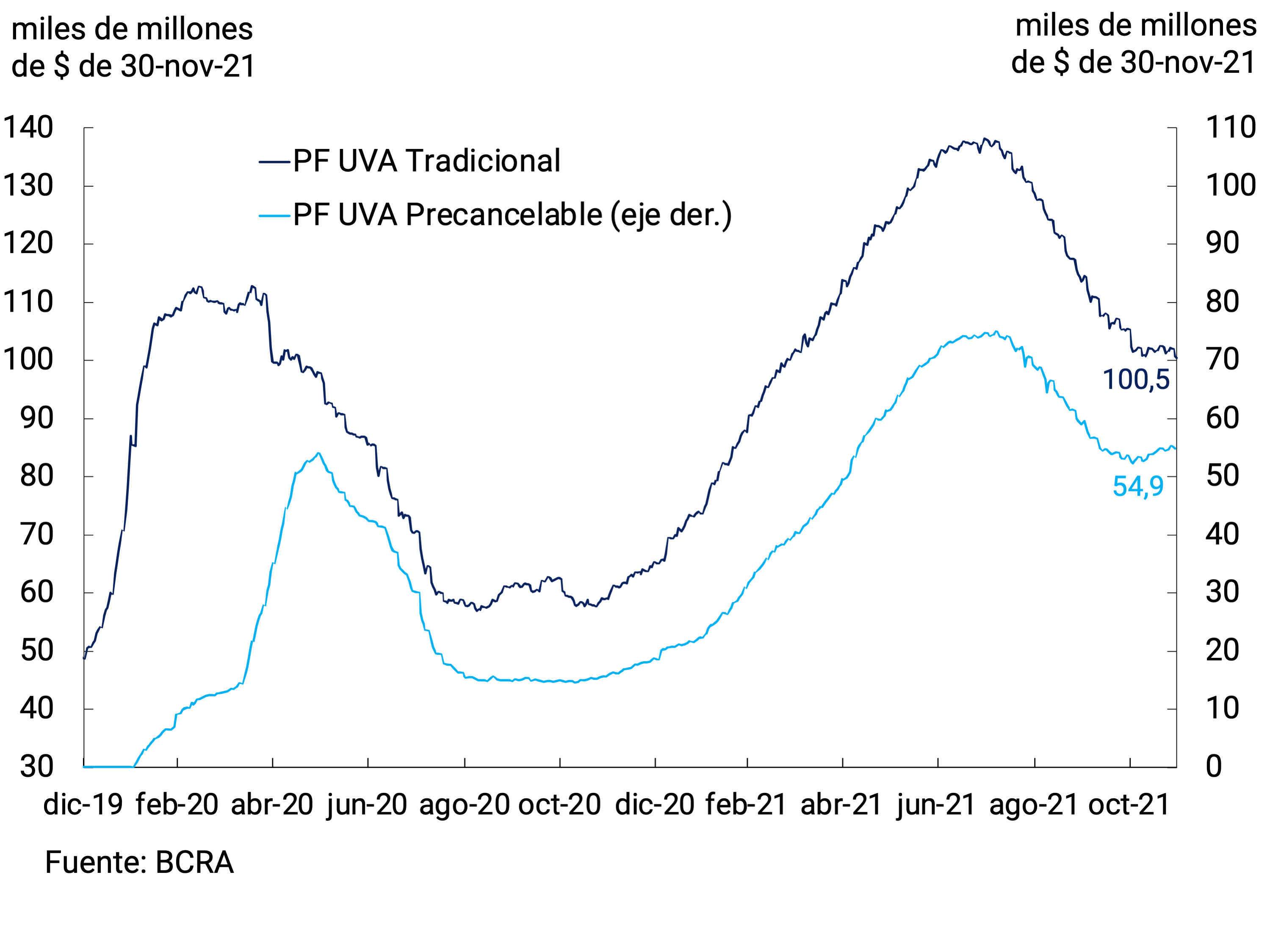

In terms of instruments, a bias was observed towards those assets with a shorter term. In fact, traditional fixed-term placements were the ones that explained the fall in the month; while deposits with early cancellation options showed a sustained increase since mid-October, driven by wholesale placements (see Figure 3.3). The greatest dynamism of pre-cancellable fixed-term deposits in the wholesale segment was verified both in the placements denominated in pesos and in those adjustable by CER. The growth of the latter broke the downward trend that began in the middle of the year (see Figure 3.4).

Figure 3.3 | Fixed-term deposits in pesos of the private

sector Balance at constant prices

Figure 3.4 | Fixed-term deposits in UVA from the private

sector Balance at constant prices

However, the broad monetary aggregate, private M35, at constant prices would have registered an increase of 1.5% s.e. in November, an expansion rate similar to that of the previous month. In the year-on-year comparison, this aggregate would have presented a contraction of the order of 2%. In terms of Output, it stood at 18.6%, which implied a slight increase (0.4 p.p.) compared to the previous month. However, it is 5.6 p.p. below the 2020 maximum.

4. Monetary base

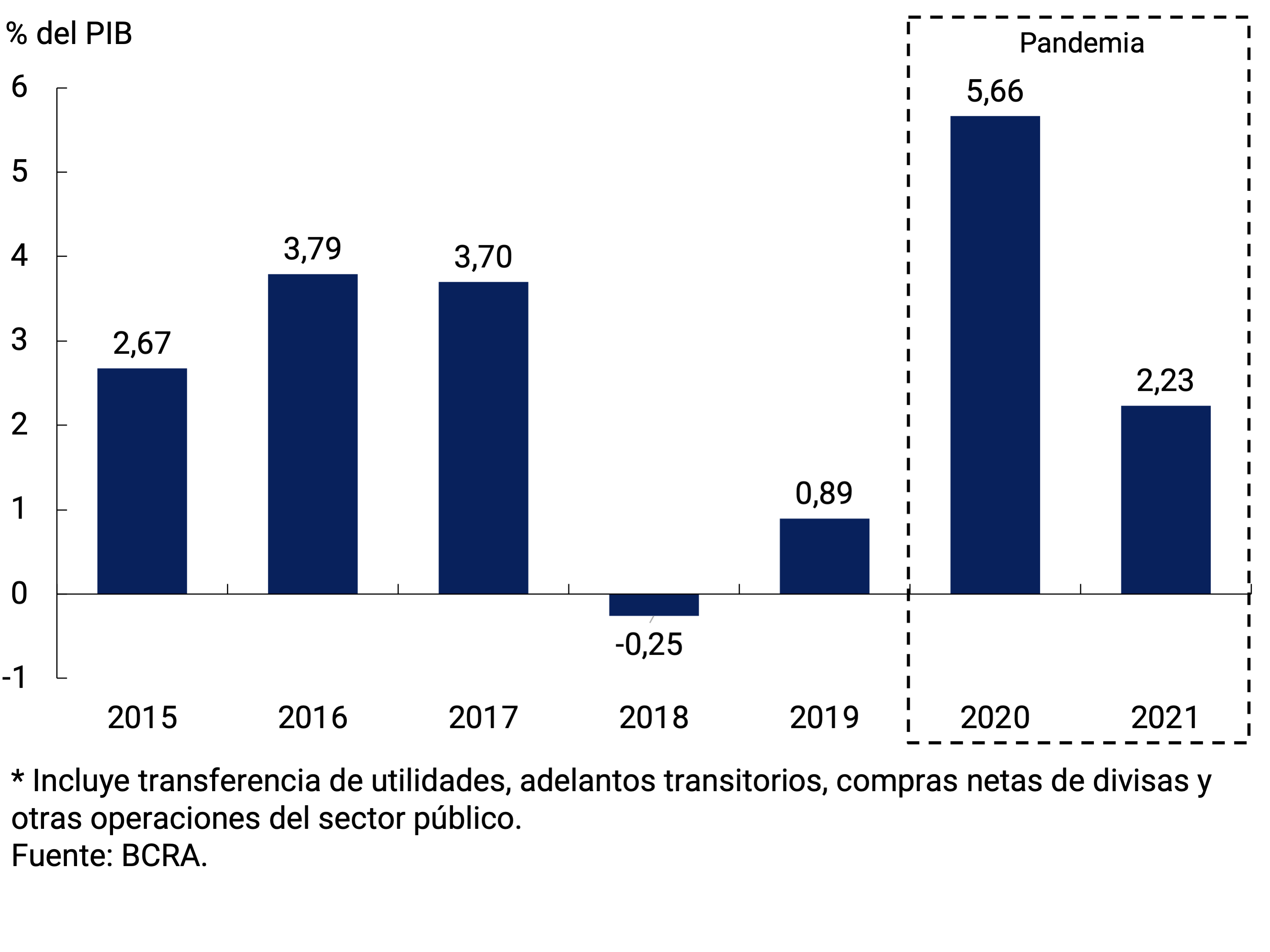

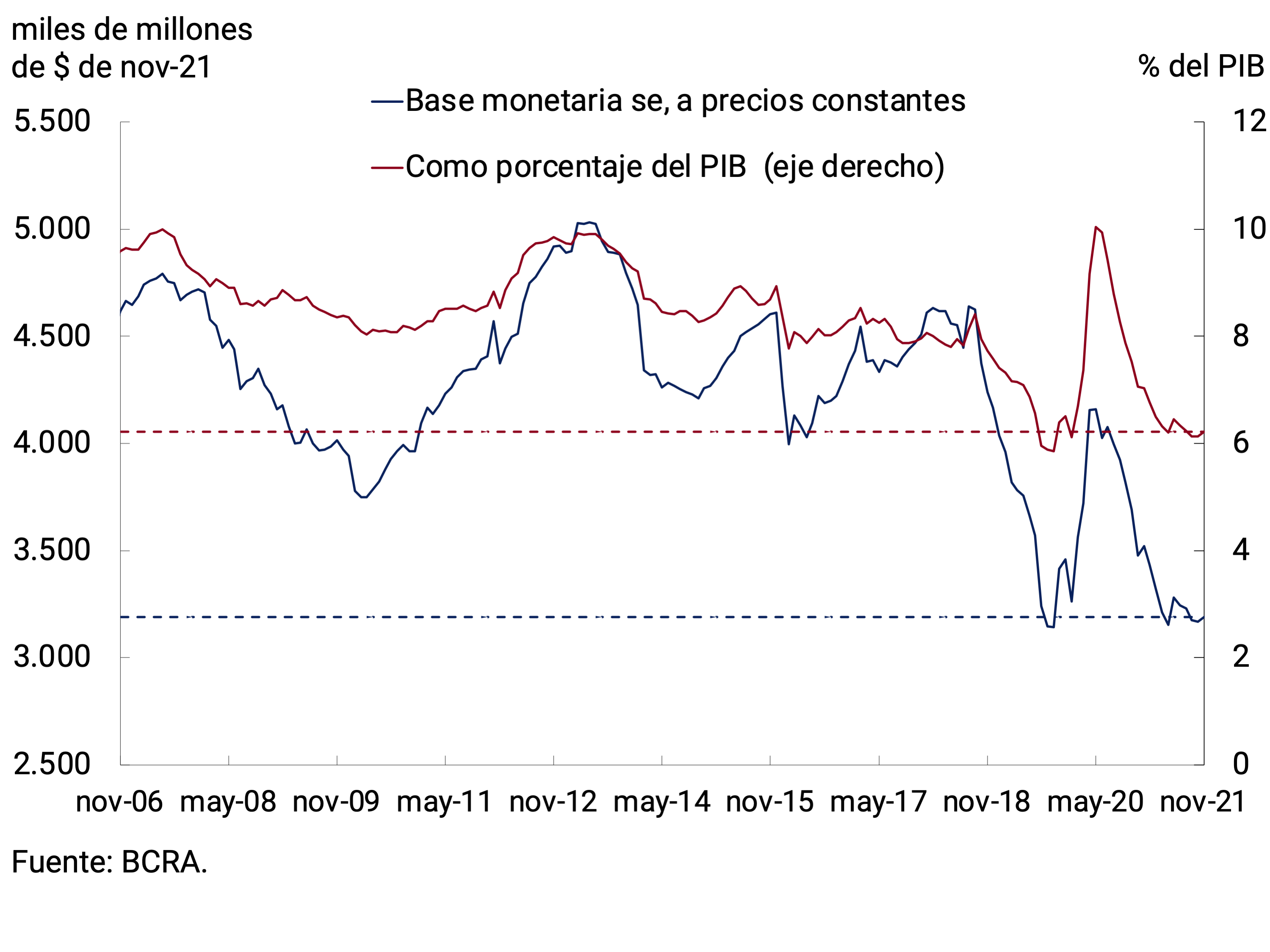

In November, the Monetary Base stood at $3,148 billion, which implied an average monthly nominal increase of 4.6% (+$138,780 million). The main factor of expansion was public sector operations. In the cumulative to November, these represented 2.2% of GDP, less than half of what was recorded in the first year of the pandemic and lower than that of the 2015-2017 period (see Figure 4.1). Adjusted for seasonality and expected inflation for the month, the Monetary Base would have registered a slight increase. In this way, it would have remained at the levels of previous months, with a year-on-year contraction of around 14%. In terms of GDP, the Monetary Base stood at 6.2%, a value similar to that of the end of 2019 (see Figure 4.2).

Figure 4.1 | Primary expansion of the public sector*

Cumulative to November of each year

Figure 4.2 | Monetary Base

5. Loans to the private sector

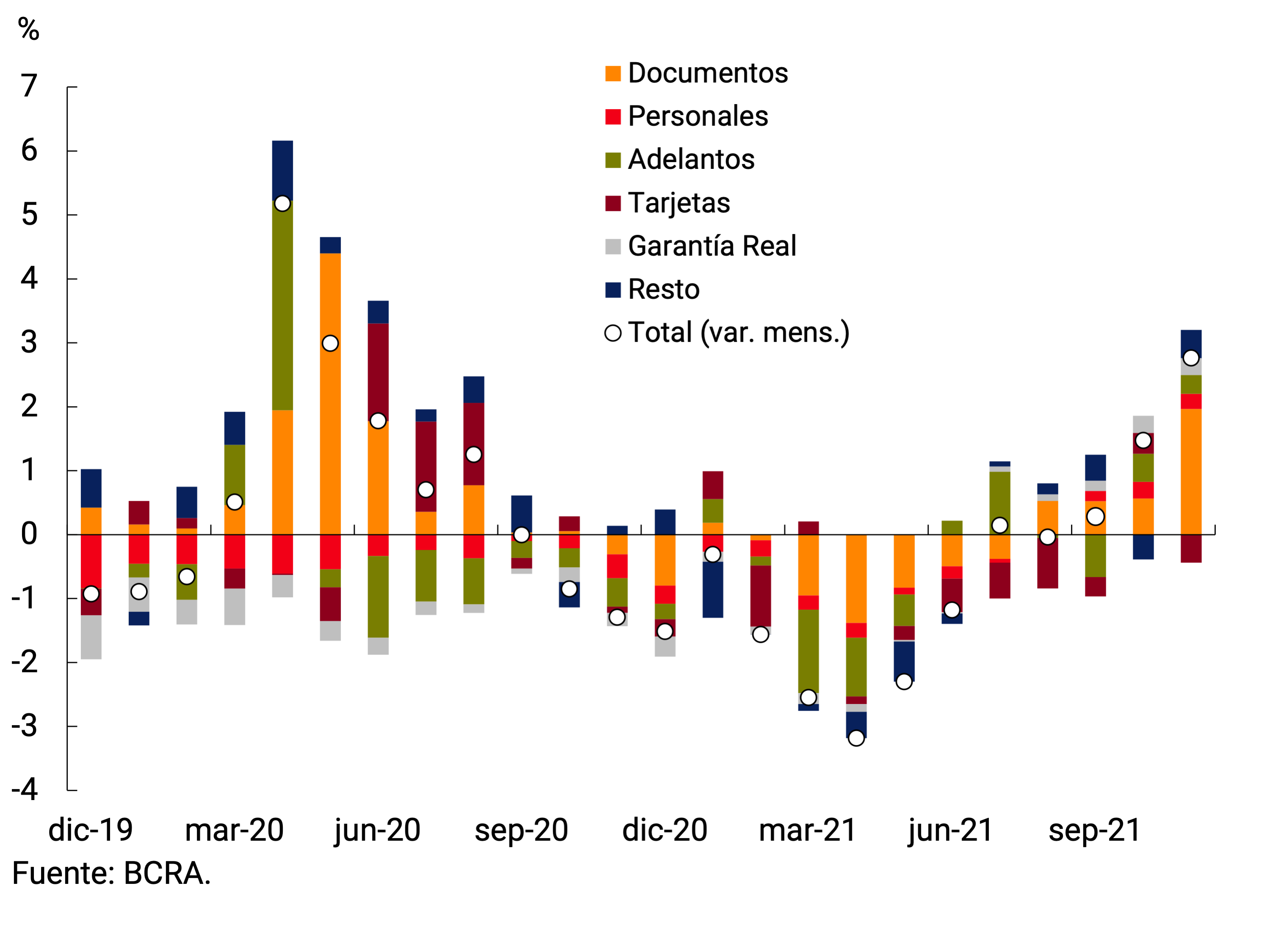

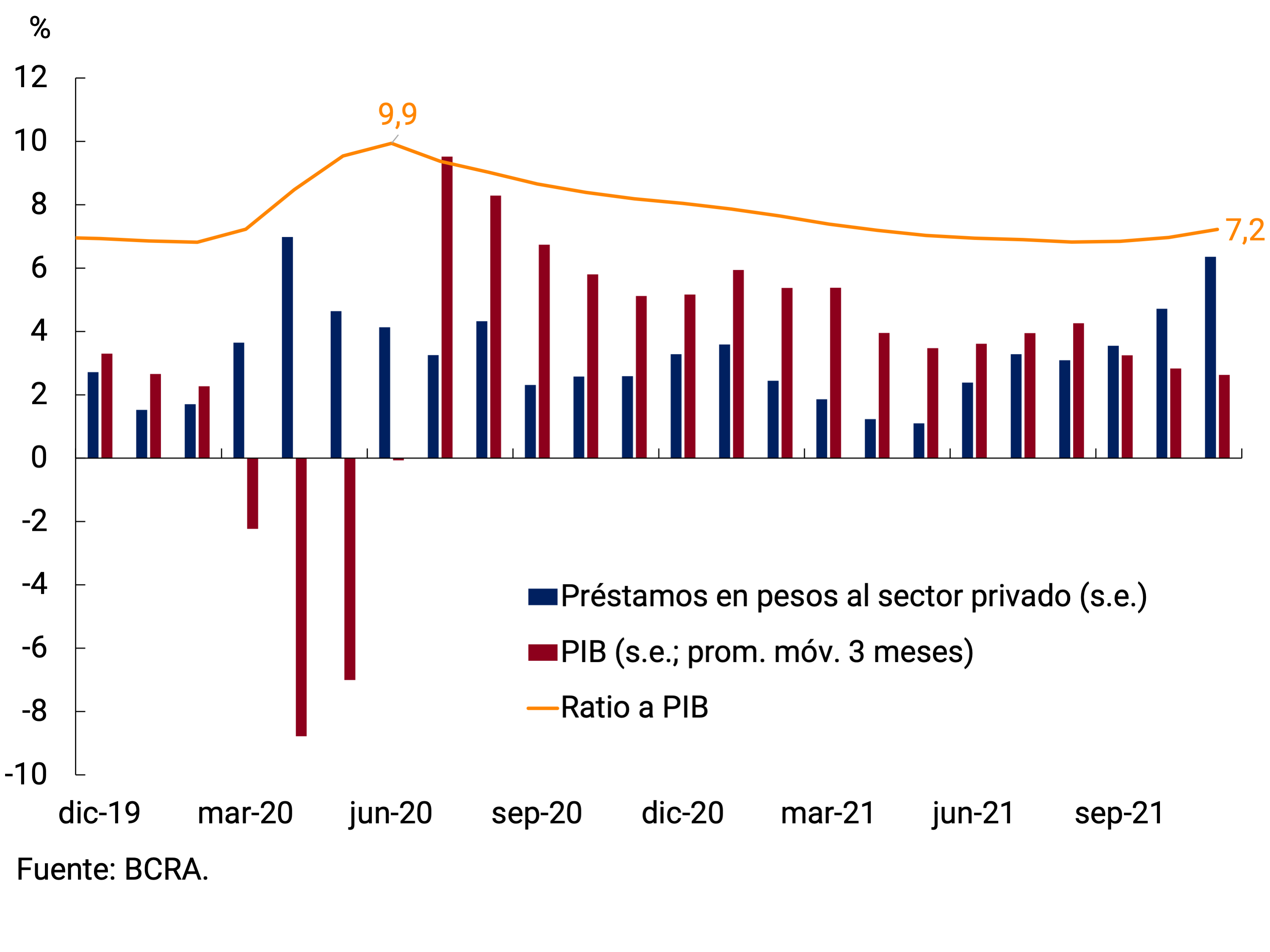

In November, loans in pesos to the private sector, in real terms and without seasonality, would have grown for the third consecutive month, marking the highest record in almost a year and a half. Among the different lines of credit, the impetus came mainly from commercial lines and, to a lesser extent, from personal and pledge loans (see Figure 5.1). The ratio of loans in pesos to the private sector to GDP stood at 7.2% in November, a value similar to that of previous months (see Figure 5.2).

Figure 5.1 | Loans in pesos to the Real Private

Sector without seasonality; contribution to monthly growth

Figure 5.2 | Loans in pesos to the private sector as a percentage of GDP

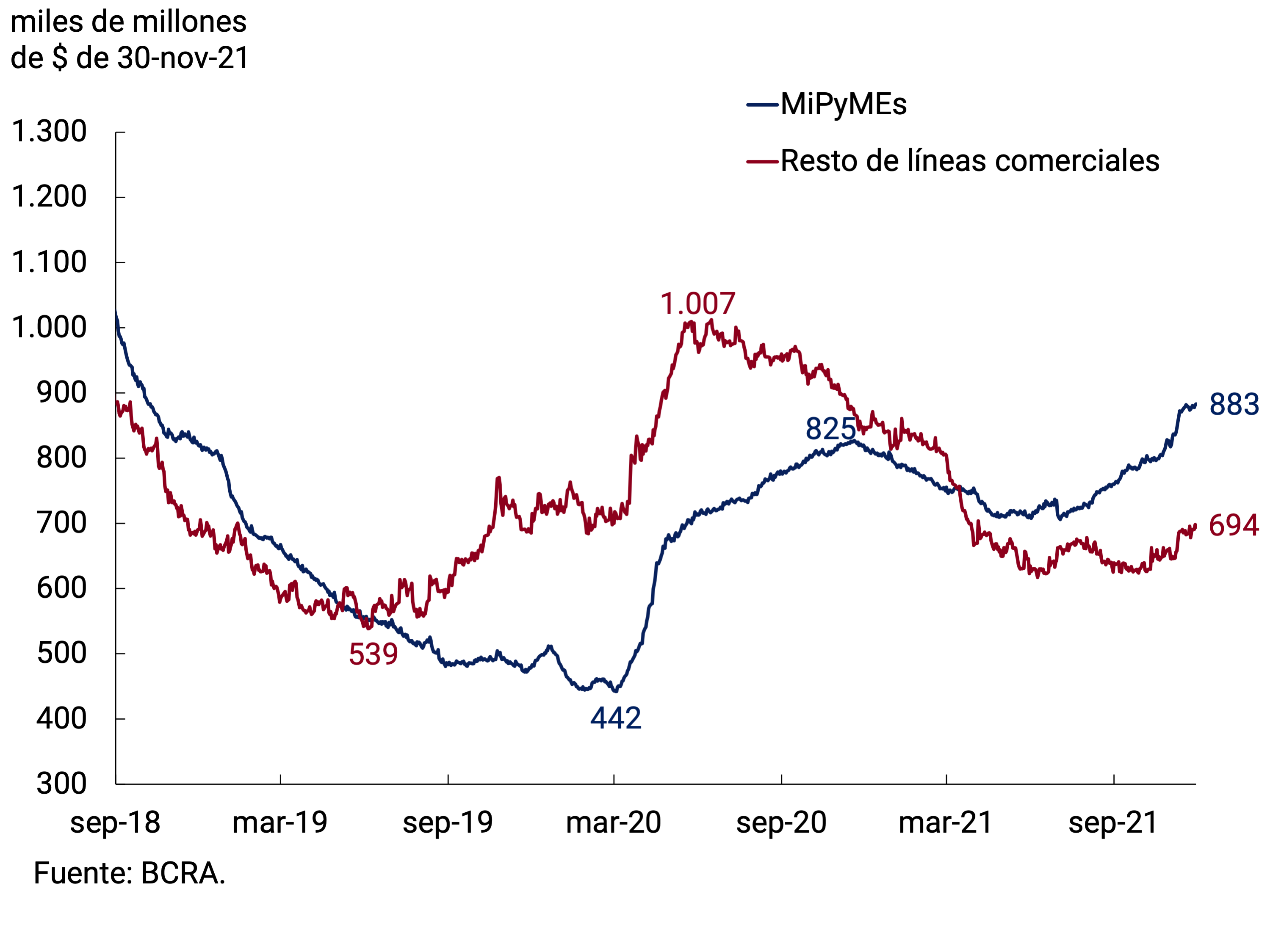

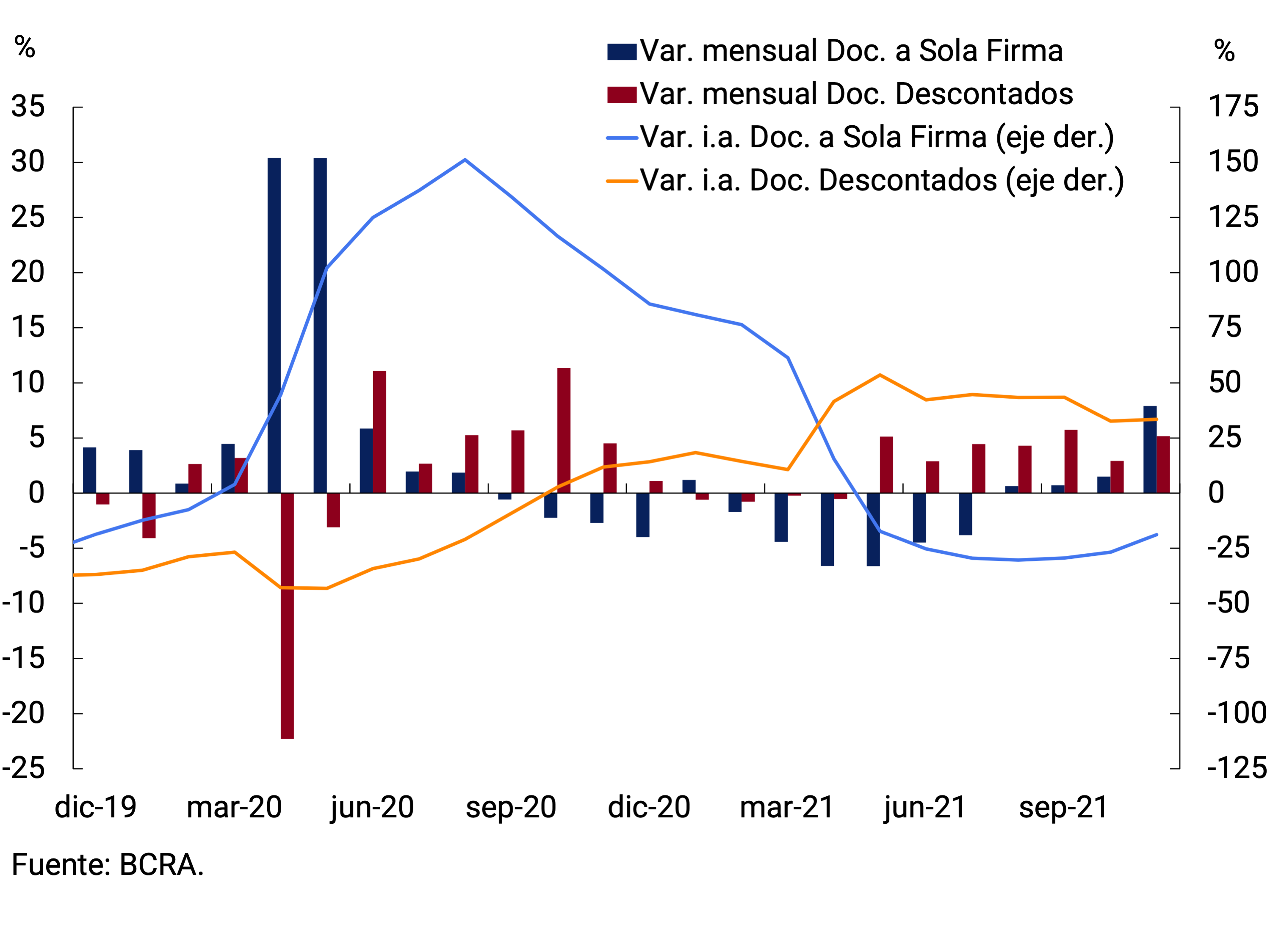

Lines with commercial destinations would have exhibited a monthly growth of close to 6% s.e. at constant prices. Analyzing its composition by type of debtor, it is verified that growth was driven by both types of firms, MSMEs and large companies (see Figure 5.3). In terms of instruments, the greatest boost came from the lines granted through documents, regardless of the term of these financings. In fact, the growth of single-signature documents, which have a longer average term, would have been 8.6% s.e. and that of discounted documents of 5.5% s.e., in both cases at constant prices (see Figure 5.4). On the other hand, the financing granted through current account advances would have exhibited an increase of approximately 3% s.e. at constant prices, which was mainly explained by that granted to large companies.

Figure 5.3 | Commercial loans to private individuals by type of debtor

Balance at constant prices

Figure 5.4 | Private documents without seasonality

Var. constant prices

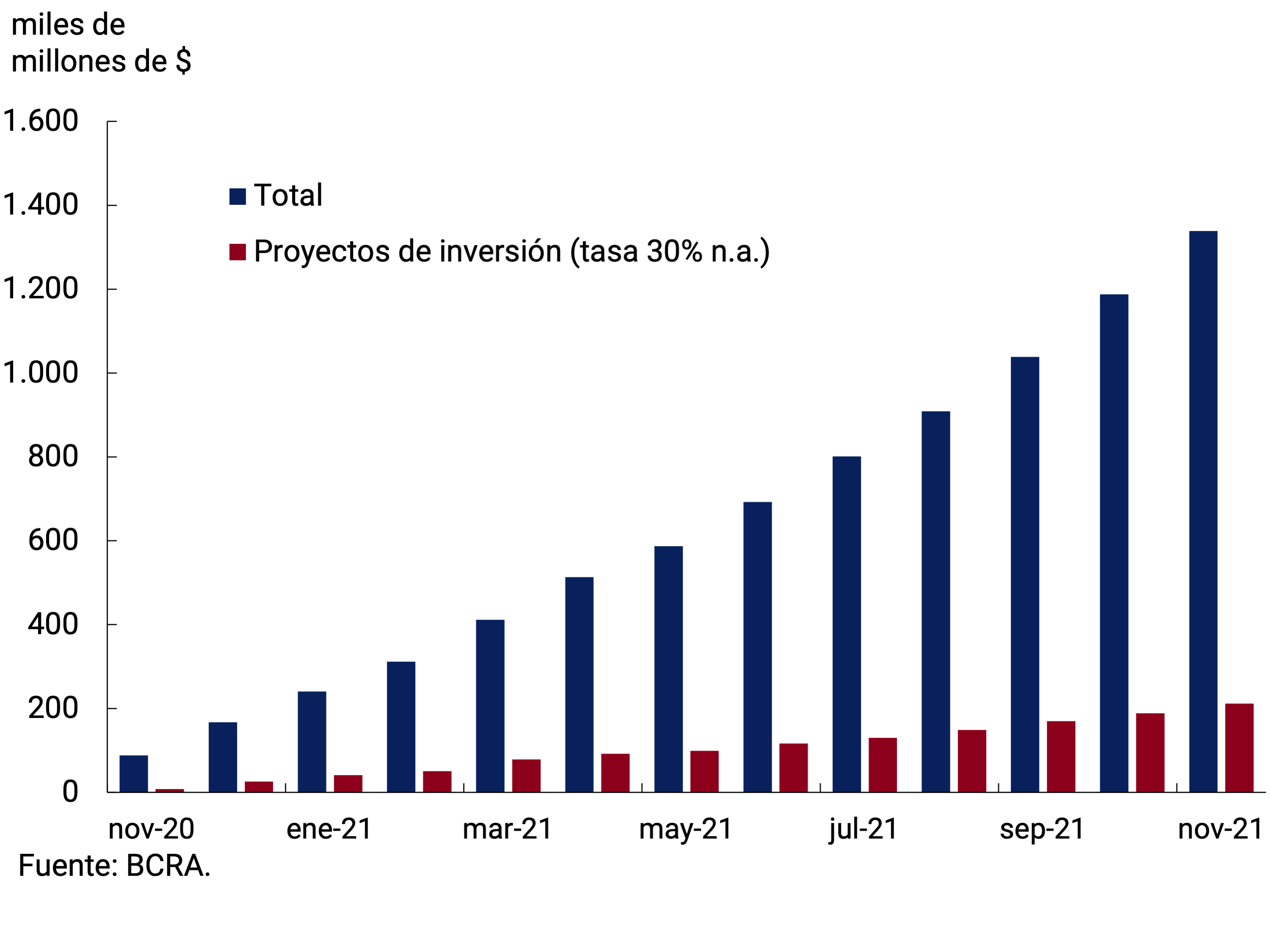

The greater dynamism shown by commercial credit was linked, in part, to the Financing Line for Productive Investment (LFIP) for MSMEs. At the end of November, loans granted under the LFIP accumulated disbursements of approximately $1.339 billion since its implementation. Thus, loans granted through the line increased 13% compared to the end of October. As for the destinations of these funds, about 84% of the total disbursed corresponds to the financing of working capital and the rest to the line that finances investment projects (see Figure 5.5). At the time of publication, the number of companies that accessed the LFIP amounted to 198,000.

Among loans associated with consumption, financing instrumented with credit cards would have exhibited a slight monthly contraction in real terms. Meanwhile, personal loans would have presented a monthly growth of 1.4% s.e. at constant prices, recording 3 consecutive months of positive real variations (see Chart 5.6). The interest rate corresponding to personal loans exhibited a decrease (1.1 p.p.) in the November average and stood at 51.8% n.a.

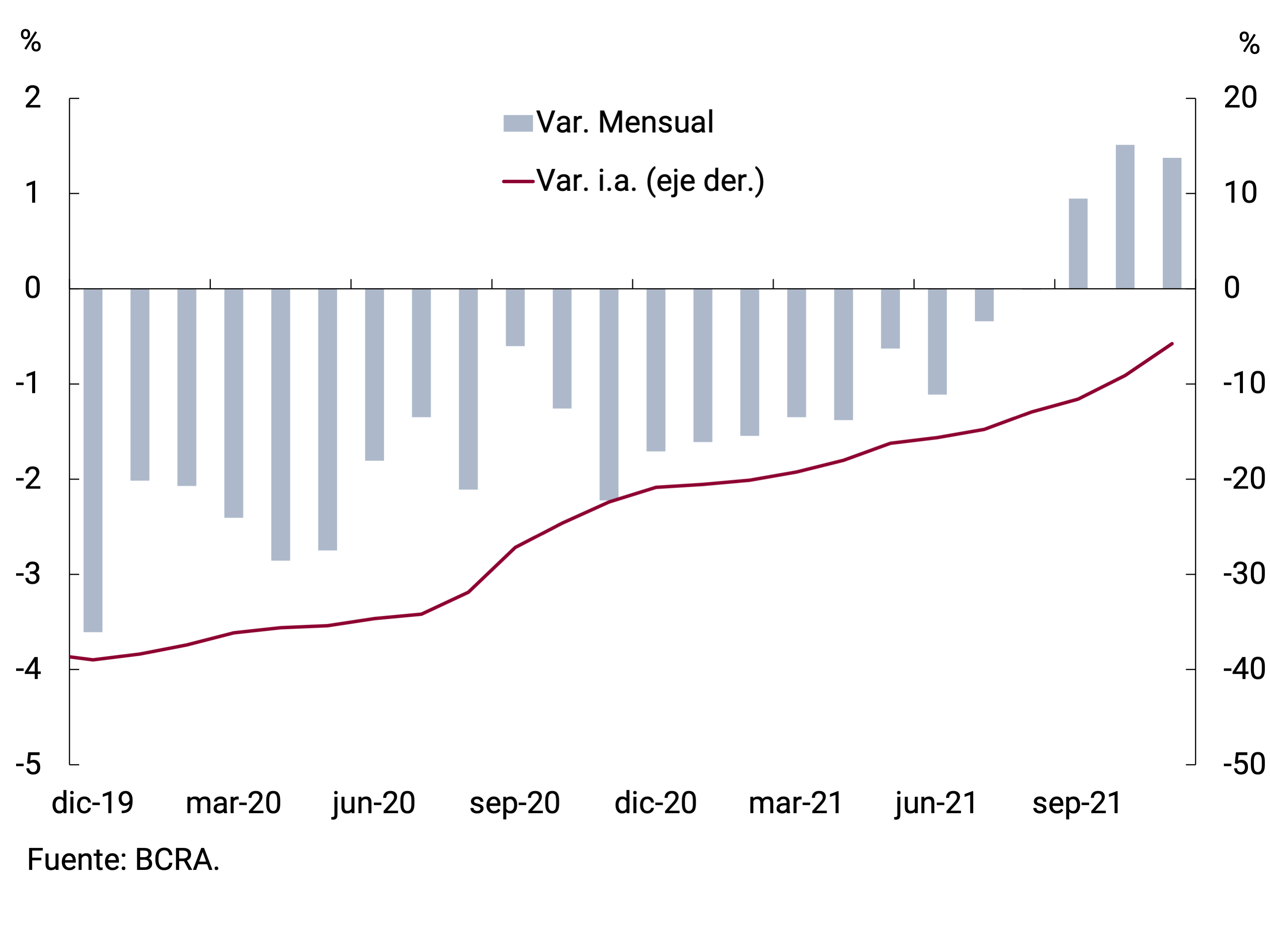

With regard to secured lines, collateral loans continued to stand out for their sustained growth in real terms. Thus, in November they would have shown a monthly increase of 4.8% s.e. at constant prices, accumulating in the last twelve months an expansion of 39.3%. On the other hand, the balance of mortgage loans practically remained in real terms and without seasonality, accumulating a contraction of 19% in the last 12 months.

Figure 5.5 | Financing granted through the Productive Investment Financing Line (LFIP)

Accumulated disbursed amounts; data at the end of the month

Figure 5.6 | Personal loans without seasonality

Var. at constant prices

6. Liquidity in pesos of financial institutions

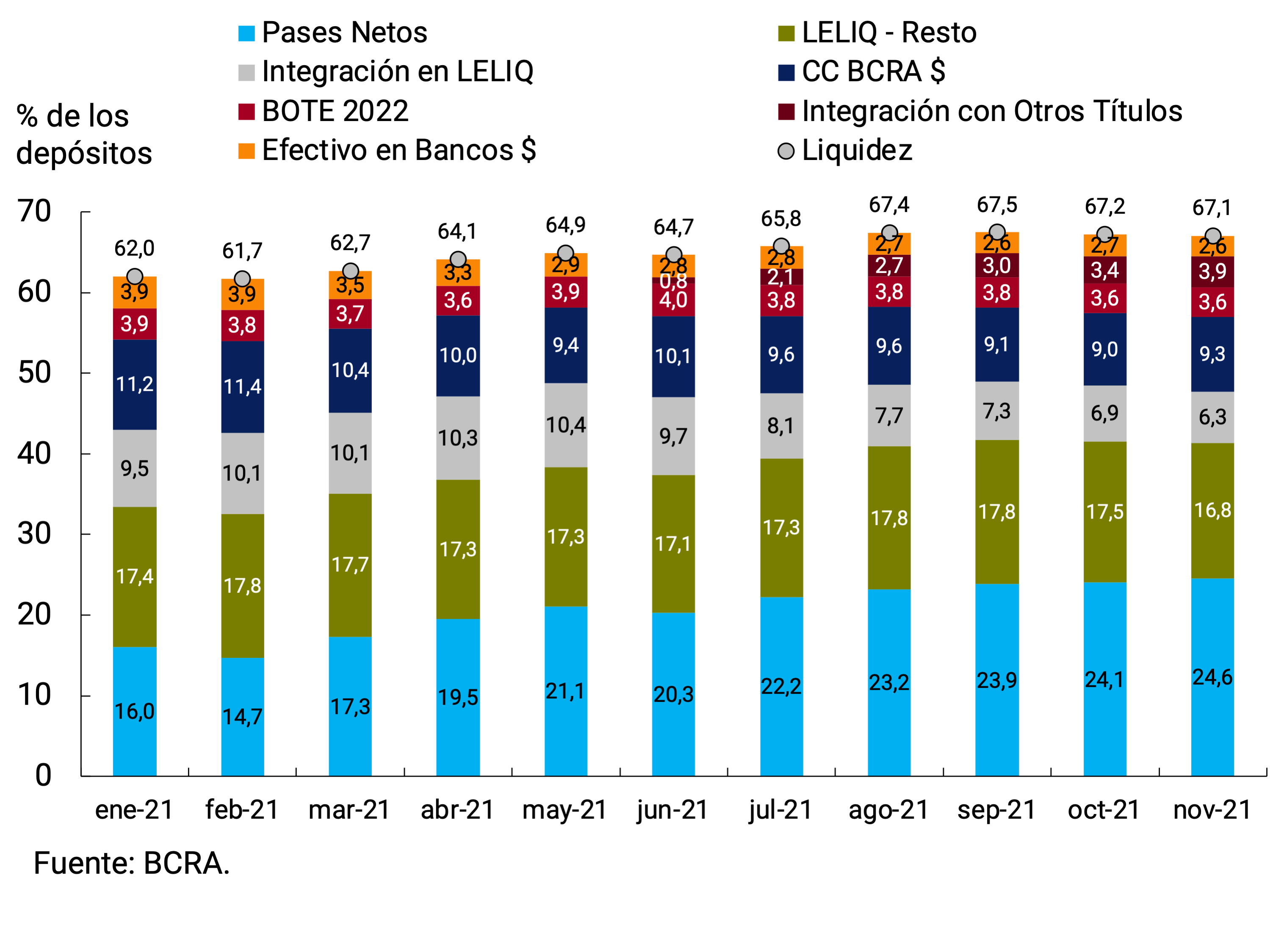

Ample bank liquidity in local currency6 averaged 67.1% of deposits, in line with the value of previous months. Thus, it remained at historically high levels (see Figure 6.1). In terms of its composition, there continued to be an increase in integration with public securities and a retraction of integration with LELIQ. In turn, among the voluntary holdings of remunerated liabilities of the Central Bank, liquidity turned in favor of the passes to the detriment of the LELIQs.

Figure 6.1 | Liquidity in pesos of financial institutions

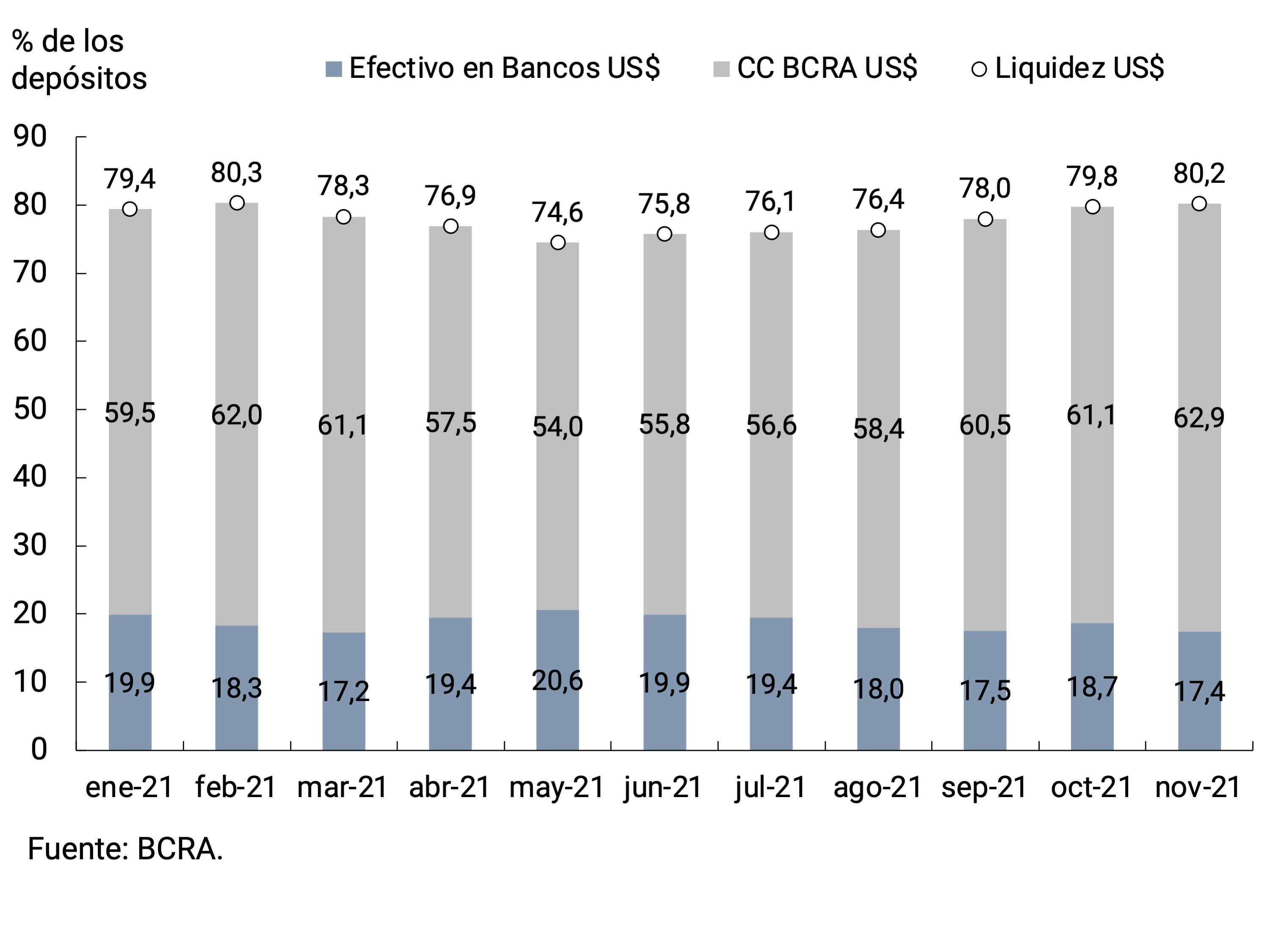

7. Foreign currency

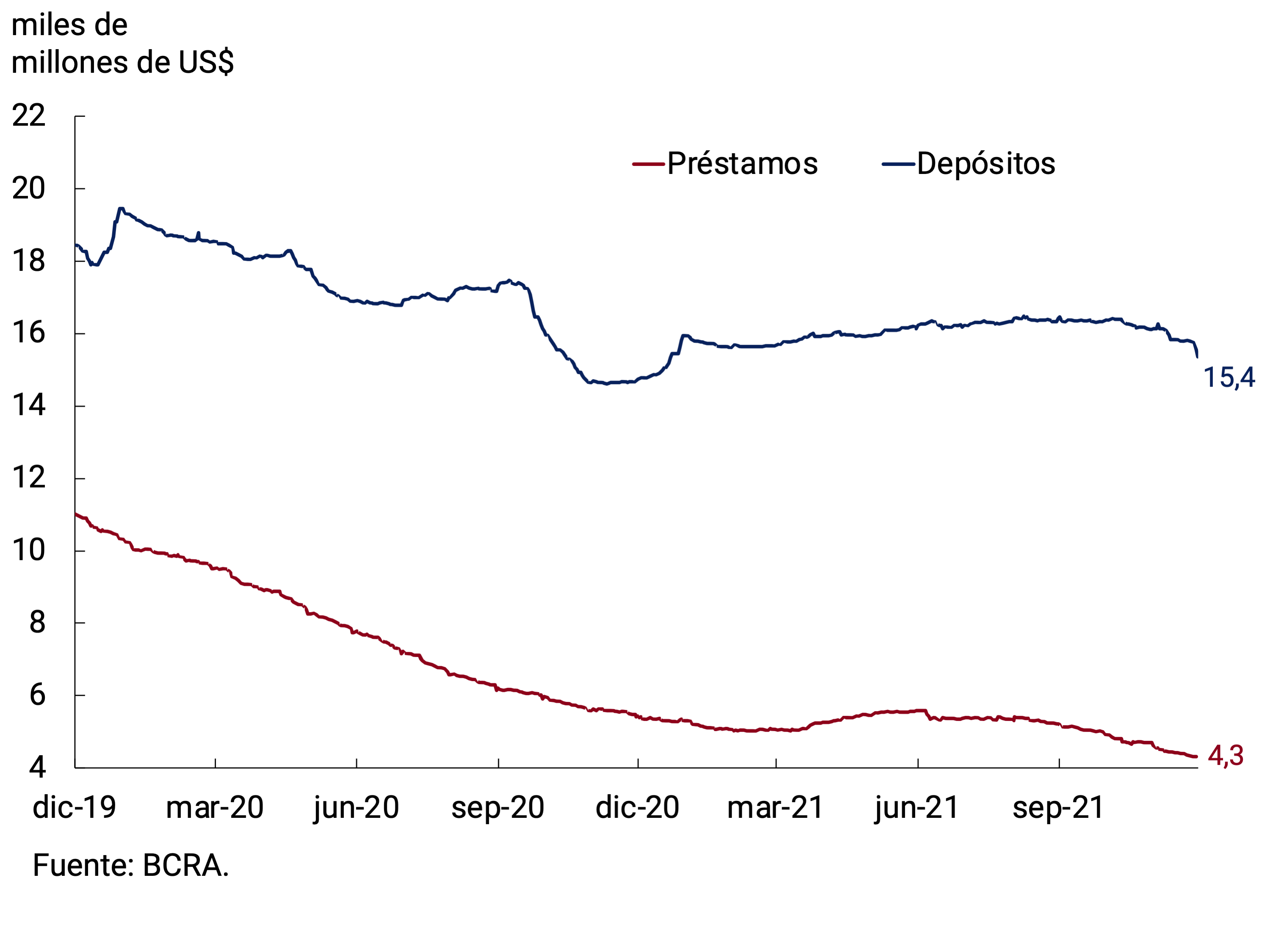

In the foreign currency segment, the main assets and liabilities of financial institutions registered negative variations in the month. Foreign currency loans to the private sector continued to show a downward trend throughout the month. Thus, the average monthly balance stood at approximately US$4,400 million, which implied a monthly decrease of close to US$300 million. The fall was concentrated in financing instrumented through single-signature documents. On the other hand, private sector deposits registered a fall in the month, in the peak comparison, of US$758 million, reaching US$15,363 million on the last day of the month (see Chart 7.1). This decrease was explained by the behavior of demand deposits of individuals of lower strata (up to US$ 50,000). It should be noted that bank liquidity in foreign currency was above 80% of deposits, remaining at record levels (see Figure 7.2). This allowed financial institutions to face the withdrawal of deposits without inconveniences.

With regard to regulatory modifications, at the beginning of the month, it was ordered that financial institutions maintain until the end of November a net global position in foreign currency that does not exceed the minimum between the cash position of November 4 and the monthly average of daily balances recorded in October 2021. without considering the securities issued by residents that have been imputed there7. Subsequently, the BCRA established that financial institutions must have a neutral spot exchange position in foreign currency as of December. It should be noted that this regulation has no impact on dollar deposits in the financial system or on the assets that support them8.

In turn, the BCRA continued with its strategy of promoting an efficient allocation of foreign currency. Thus, on the one hand, credit card issuers were prevented from financing purchases made by credit cards of tickets abroad and other tourist services abroad in installments9. On the other hand, the conditions of automatic access to the foreign exchange market for imports of capital goods were made more flexible, this will especially facilitate access to capital goods for various MSMEs that will increase their production and efficiency10.

Finally, in order to facilitate the entry of foreign currency and the management of electronic payment systems in the country, it was provided that the exchange and arbitration operations of non-resident individuals may be carried out without restrictions to the extent that the resulting funds are credited to a “Savings Bank for Tourists”. In addition, at the time of the closure of these savings banks, these operations are exempt from the complementary requirements established in the “Foreign and Foreign Exchange” regulations relating to the outflow of foreign currency in the foreign exchange market11.

Figure 7.1 | Balance of private sector foreign currency deposits and loans

Figure 7.2 | Liquidity in foreign currency of financial institutions

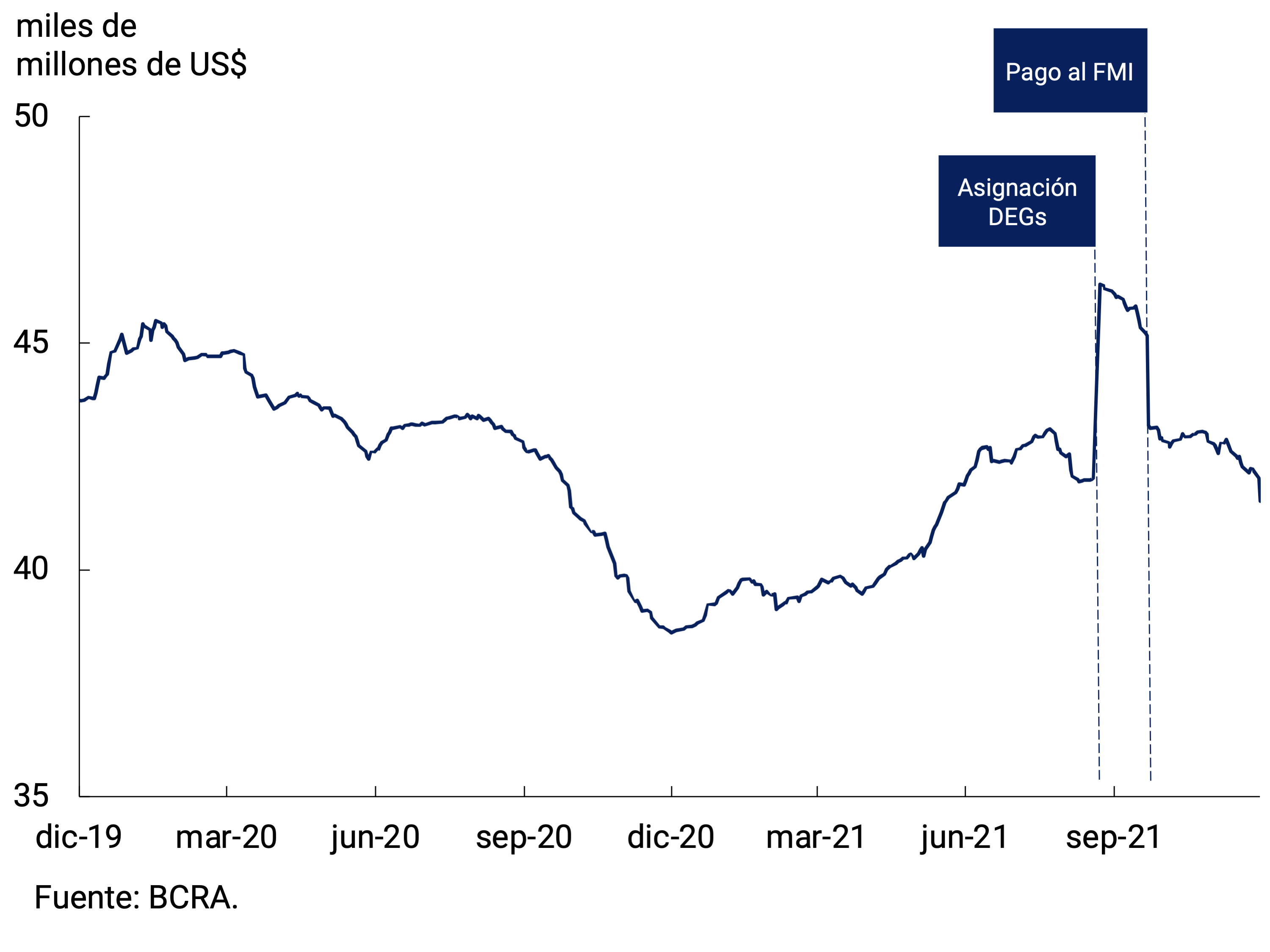

The BCRA’s International Reserves ended November with a balance of US$41,530 million, reflecting a fall of US$1,288 million compared to the end of October (see Figure 7.3). As for the variation factors, this fall was explained by the net sales of foreign currency to the private sector, the decrease in the minimum cash position and payments to international organizations. Among the latter, an interest payment to the IMF at the beginning of the month for approximately US$400 million stands out.

Finally, the bilateral nominal exchange rate against the U.S. dollar increased 1.1% in November, in line with the variation of previous months. Thus, it stood at an average of $100.31/US$ (see Figure 7.4). The limited pace of depreciation of the domestic currency in recent months seeks to contribute to the disinflation process.

Figure 7.3 | International Reserves

Daily Balance

Figure 7.4 | Variation in the bilateral nominal exchange rate with the United States

Glossary

ANSES: National Social Security Administration.

BADLAR: Interest rate on fixed-term deposits for amounts greater than one million pesos and a term of 30 to 35 days.

BCRA: Central Bank of the Argentine Republic.

BM: Monetary Base, includes monetary circulation plus deposits in pesos in current account at the BCRA.

CC BCRA: Current account deposits at the BCRA.

CER: Reference Stabilization Coefficient.

NVC: National Securities Commission.

SDR: Special Drawing Rights.

EFNB: Non-Banking Financial Institutions.

EM: Minimum Cash.

FCI: Common Investment Fund.

A.I.: Year-on-year .

IAMC: Argentine Institute of Capital Markets

CPI: Consumer Price Index.

ITCNM: Multilateral Nominal Exchange Rate Index

ITCRM: Multilateral Real Exchange Rate Index

LEBAC: Central Bank bills.

LELIQ: Liquidity Bills of the BCRA.

LFIP: Financing Line for Productive Investment.

M2 Total: Means of payment, which includes working capital held by the public, cancelling cheques in pesos and demand deposits in pesos from the public and non-financial private sector.

Private M2: Means of payment, includes working capital held by the public, cancelling cheques in pesos and demand deposits in pesos from the non-financial private sector.

Private transactional M2: Means of payment, includes working capital held by the public, cancelling cheques in pesos and non-remunerated demand deposits in pesos from the non-financial private sector.

M3 Total: Broad aggregate in pesos, includes the current currency held by the public, cancelling checks in pesos and the total deposits in pesos of the public and non-financial private sector.

Private M3: Broad aggregate in pesos, includes the working capital held by the public, cancelling checks in pesos and the total deposits in pesos of the non-financial private sector.

MERVAL: Buenos Aires Stock Market.

MM: Money Market.

N.A.: Annual nominal

E.A.: Annual Effective

NOCOM: Cash Clearing Notes.

ON: Negotiable Obligation.

GDP: Gross Domestic Product.

P.B.: Basic points.

P.P.: Percentage points.

MSMEs: Micro, Small and Medium Enterprises.

ROFEX: Rosario Term Market.

S.E.: No seasonality

SISCEN: Centralized System of Information Requirements of the BCRA.

TCN: Nominal Exchange Rate

IRR: Internal Rate of Return.

TM20: Interest rate on fixed-term deposits for amounts greater than 20 million pesos and a term of 30 to 35 days.

TNA: Annual Nominal Rate.

UVA: Unit of Purchasing Value

References

1 The INDEC will release the inflation data for November on December 14.

2 M2 private excluding interest-bearing demand deposits from companies and financial service providers. This component was excluded since it is more similar to a savings instrument than to a means of payment.

3 See Decree 719/21.

4 The average interest rate observed is slightly below the minimum guaranteed interest rate, because it includes deposits of up to $1 million of individuals who, in total, in the financial institution can exceed one million pesos and, therefore, charge a lower interest rate for amounts that exceed this threshold. In addition, this minimum rate only corresponds to banks in Group A and G-SIB, and may be the lowest minimum rate for the rest of the entities.

5 Includes the working capital held by the public and the deposits in pesos of the non-financial private sector (sight, term and others).

6 Includes current accounts at the BCRA, cash in banks, balances of net passes arranged with the BCRA, holdings of LELIQ, and bonds eligible for reserve requirements.

Share on