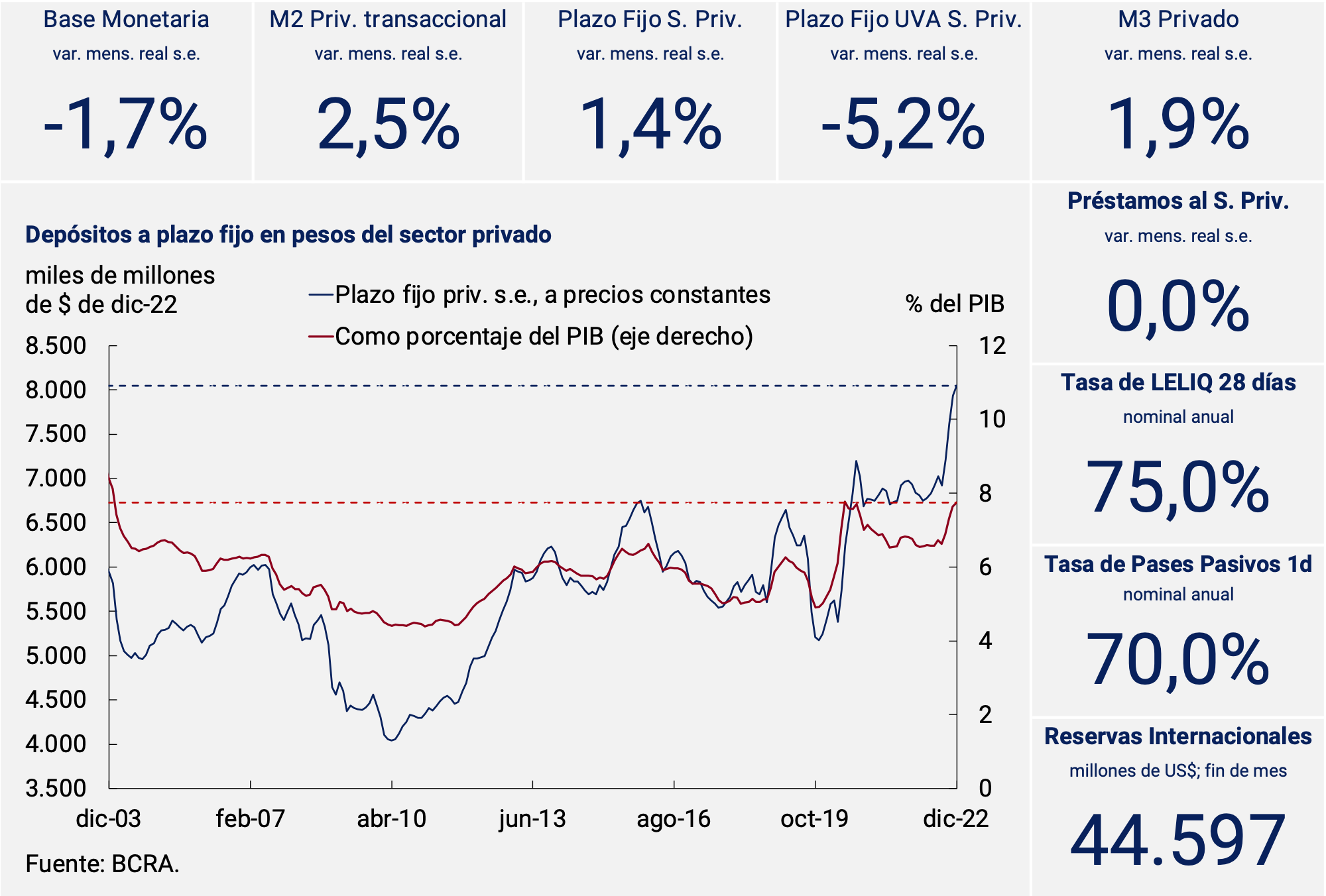

Executive summary

The broad monetary aggregate (private M3) at constant prices and without seasonality would have registered an increase in the last month of the year. At the component level, means of payment showed an increase, unlike what happened during almost the entire year, and fixed-term deposits continued to grow. Thus, the latter would have set a new high at constant prices in historical terms and in a record similar to the maximum of the pandemic in terms of Output.

The growth in term placements occurred in an environment of positive real rates. During December, the minimum interest rates on deposits remained at 75% n.a. (107.05% e.a.) for placements by individuals for up to an amount of $10 million and at 66.5% n.a. (91.07% e.a.) for the rest of the depositors in the financial system.

On November 28, the “Export Increase Program” was reopened, which allowed the soybean complex to liquidate foreign currency at an exceptional and transitory value of $230/US$ until December 30. The BCRA acquired US$3,155 million through this mechanism and, together with the rest of the foreign exchange operations of the private sector, left a net balance of US$2,330 million in the month. These operations implied an expansion of liquidity that was sterilized with interest-bearing liabilities.

Finally, loans to the private sector at constant prices and without seasonality would have remained unchanged in the month, after 5 consecutive months of contraction. In this way, they would have ended the year with a year-on-year drop of approximately 12%.

2. Payment methods

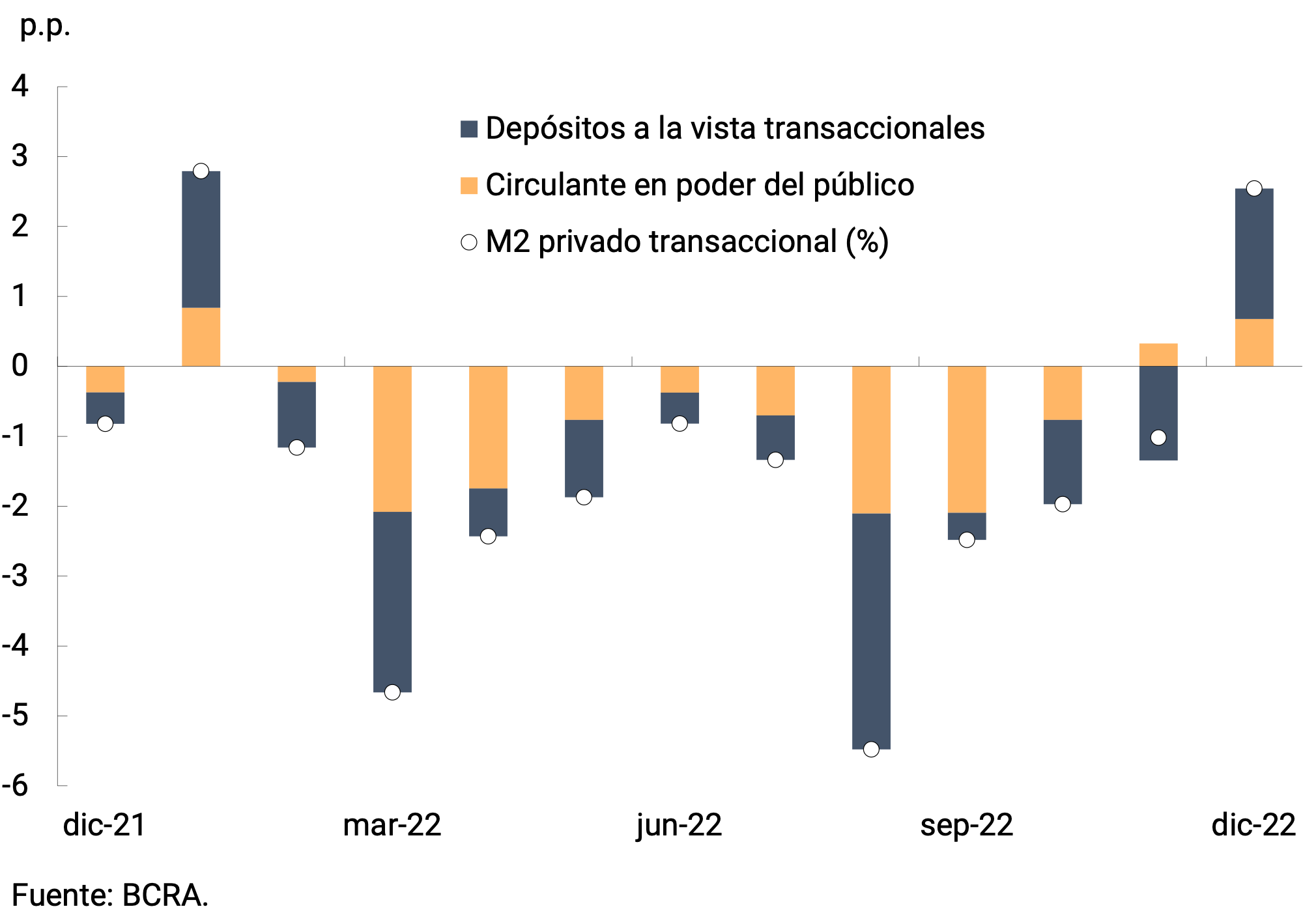

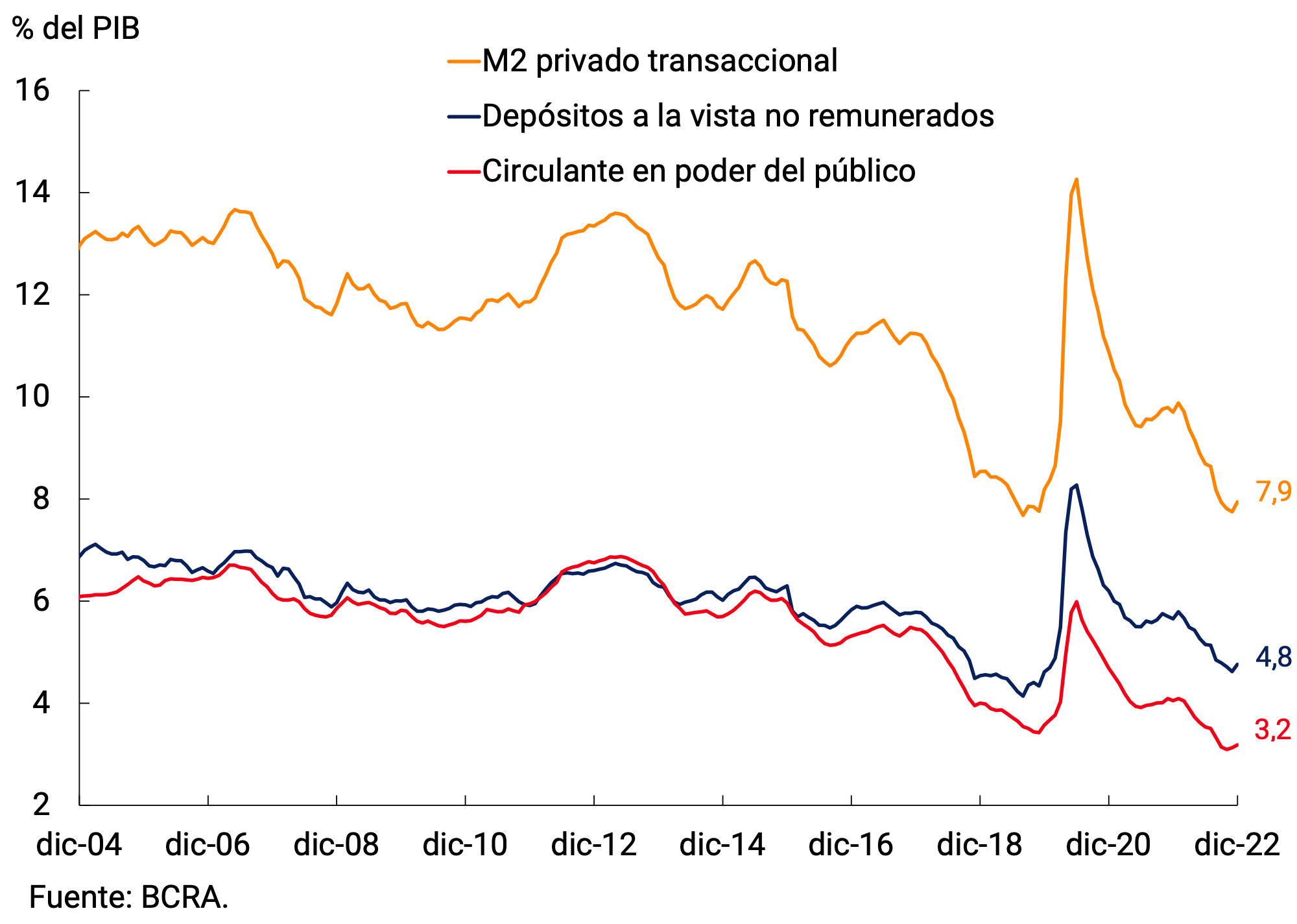

Means of payment (transactional private M21) at constant and seasonally adjusted prices (s.e.) would have registered an expansion of 2.5% in December, thus reversing the downward trend observed practically throughout the year (see Figure 2.1). At the level of its components, the increase was explained by the behavior of non-interest-bearing demand deposits and, to a lesser extent, by the expansion of working capital held by the public. In the year-on-year comparison, and at constant prices, the transactional private M2 would be 16.4% below the level of December 2021. In terms of Output, means of payment would have stood at 7.9%, closing the year at a slightly higher rate than in previous months (see Chart 2.2). Both components of the means of payment remain in terms of GDP at around the lowest levels of the last 20 years.

Figure 2.1 | Private transactional M2 at constant

prices Contribution by component to the monthly vari. s.e.

Figure 2.2 | Private transactional M2

3. Savings instruments in pesos

The Board of Directors of the BCRA decided to maintain for the third consecutive month without changes the minimum guaranteed interest rates on fixed-term deposits on December2. This decision was taken taking into account the slowdown in the pace of price growth in November, the advance data for December and the short-term outlook. Thus, the minimum guaranteed rate for placements of individuals for an amount of up to $10 million remained at 75% n.a. (107.05% e.a.), while for the rest of the depositors of the financial system the interest rate stood at 66.5% n.a. (91.07% e.a.)3.

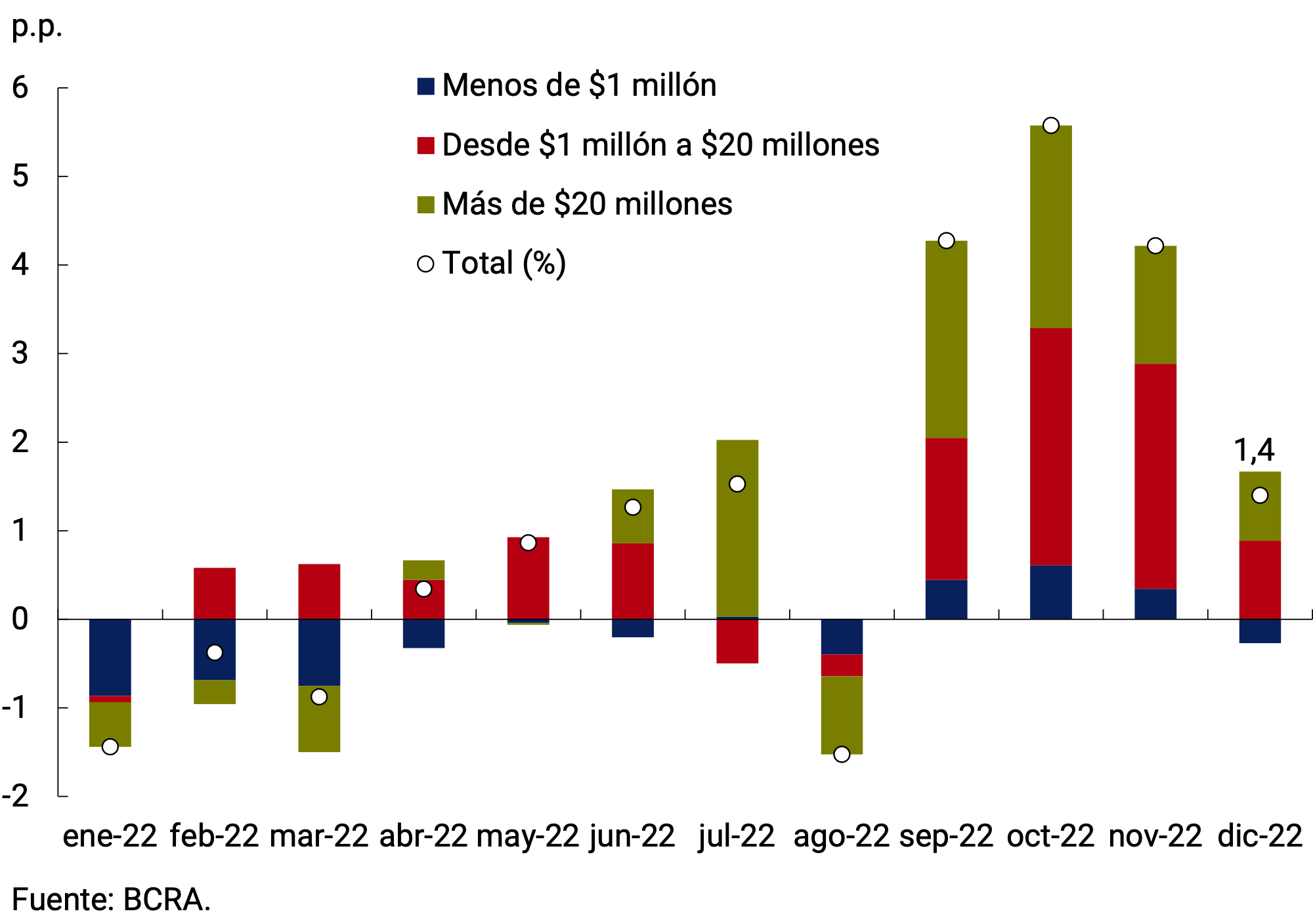

In December, fixed-term deposits in pesos of the private sector would have registered a monthly expansion at constant prices of 1.4% s.e., moderating their growth rate compared to previous months. As a result, in the last month of the year they set a new all-time high at constant prices and as a percentage of GDP they would stand at 7.7%, which is a record similar to the maximum reached during the pandemic.

Discriminating by amount stratum, it is verified that the growth of the month was concentrated in the segments of more than $1 million; the most dynamic being, in particular, the $1 to $20 million (see Figure 3.1). The average monthly growth in deposits of more than $20 million was partly explained by the carry-over effect of the previous month. Analyzing the daily evolution of this type of placement, it is verified that the traditional fixed-term holdings of Financial Services Providers (FSPs) ended the month at a level similar to that of the end of November and those of the rest of the companies registered a fall. Meanwhile, investments with early cancellation options (which cannot be classified by type of holder) reversed their downward trend (see Figure 3.2). Finally, deposits of less than $1 million showed a slight drop in real terms and without seasonality.

Figure 3.1 | Fixed-term deposits in pesos of the private

sector Contribution by stratum of amount to the var. mens. at constant prices and without seasonality

Figure 3.2 | Fixed-term deposits of more than $20 million

Balance at constant prices by type of depositor and instrument. Original Series

In a context of moderation in the inflation rate, the segment of fixed-term deposits adjustable by CER exhibited a new contraction in real terms, accumulating 5 consecutive months of declines. On this occasion, the decrease was verified in both traditional and pre-cancelable UVA placements, whose monthly rates of change stood at -9.5% s.e. and -1.6% s.e. at constant prices, respectively (see Figure 3.3). Distinguishing by type of holder within the instruments with CER adjustment, it can be seen that the average monthly fall was almost entirely explained by the dynamics of placements by individuals and companies (excluding PSFs; see Figure 3.4). All in all, UVA deposits ended the year with a balance of $352,700 million, which represented approximately 4.4% of the total of time instruments denominated in domestic currency.

Figure 3.3 | Fixed-term deposits in UVA from the private

sector Balance at constant prices by type of instrument

Figure 3.4 | Fixed-term deposits in UVA in the private

sector Balance at constant prices by type of holder

On the other hand, deposits adjusted for the value of the reference exchange rate registered an increase in the last month of the year, although with a heterogeneous behavior at the level of their components. Currently, the agricultural sector has two different types of deposits with foreign exchange coverage available: a demand account, commonly known as “chacareros deposits” and time investments, called DIVA dollar. The first type of deposit registered a variation at the end of the month of 37.4% at current prices, reaching a balance of $146,100 million at the end of December. It should be noted that the origin of these funds were the operations carried out under the “Export Increase Program”. Meanwhile, the DIVA dollar reached a balance of $42,500 million at the end of the month, which implied an average monthly contraction of 2.0% at current prices. To cover the exchange rate risk of these deposits, financial institutions have at their disposal the Bills with adjustment according to the value of the dollar (LEDIV).

All in all, the broad monetary aggregate, private M3, at constant prices and adjusted for seasonality, would have registered an expansion in December (1.9%), accumulating 4 consecutive months of positive variations4. In year-on-year terms, this aggregate would have experienced a decrease of 1.7% and as a percentage of GDP it would have stood at 17.7%, 0.3 p.p. above the previous month’s record and at a level similar to the 2010-19 average.

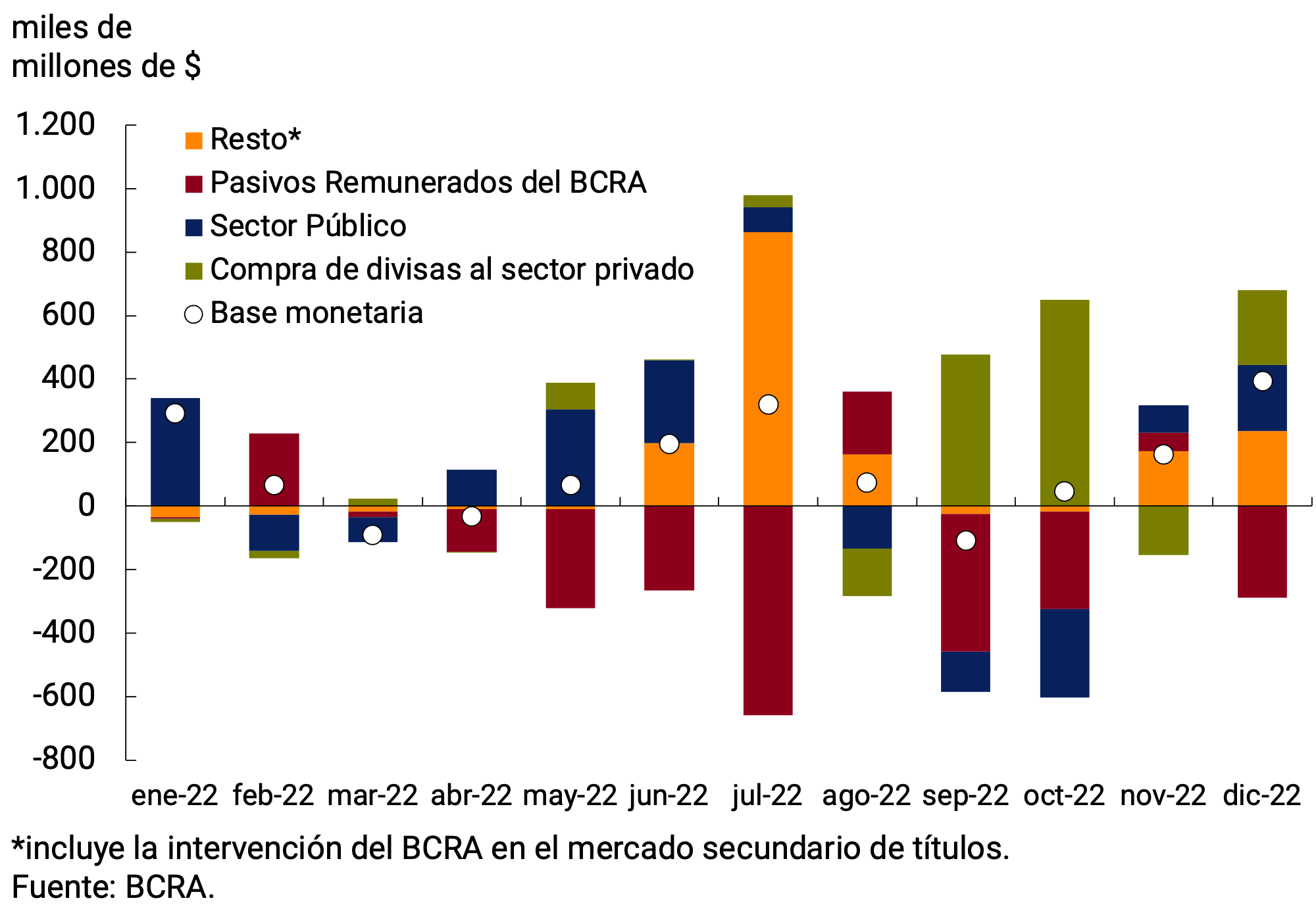

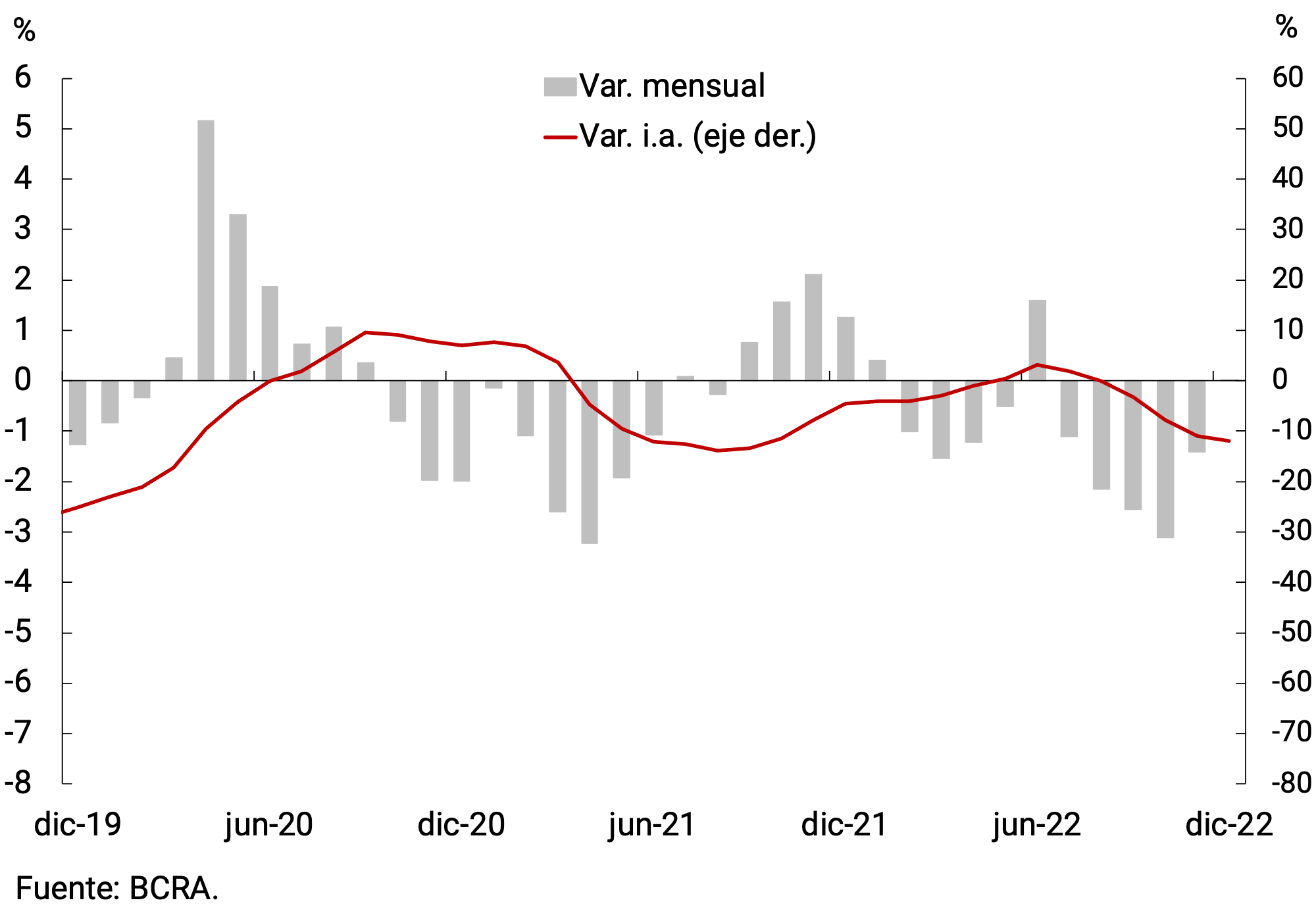

4. Monetary base

In December, the Monetary Base stood at an average of $4,781.9 billion, which implied a monthly increase of 9% ($393,590 million) in the original series at current prices. It should be noted that the Monetary Base presents a positive seasonality in December, so if we correct it for this effect it would have exhibited a contraction of 1.7% per month s.e. at constant prices. In 2022 it would accumulate a fall of close to 26% in real terms. As a GDP ratio, the Monetary Base would stand at 4.4%, 0.1 p.p. below the value recorded the previous month and at its lowest value since the exit from convertibility (see Figure 4.1).

Figure 4.1 | Monetary base

Figure 4.2 | Factors explaining the Monthly Average Monetary Base

On the supply side, the average monthly growth of the base was mainly explained by the net purchase of foreign currency from the private sector that prompted the reopening of the “Export Increase Program”. These funds were largely channeled to Money Market Mutual Funds (FCI MM)5, which resulted in an increase in interest-bearing deposits. Other factors in the expansion of the monetary base were the BCRA’s purchases in the secondary market for public securities, with the aim of limiting excessive price volatility, and public sector operations6. The expansion of liquidity was partially sterilized through monetary regulation instruments (see Figure 4.2).

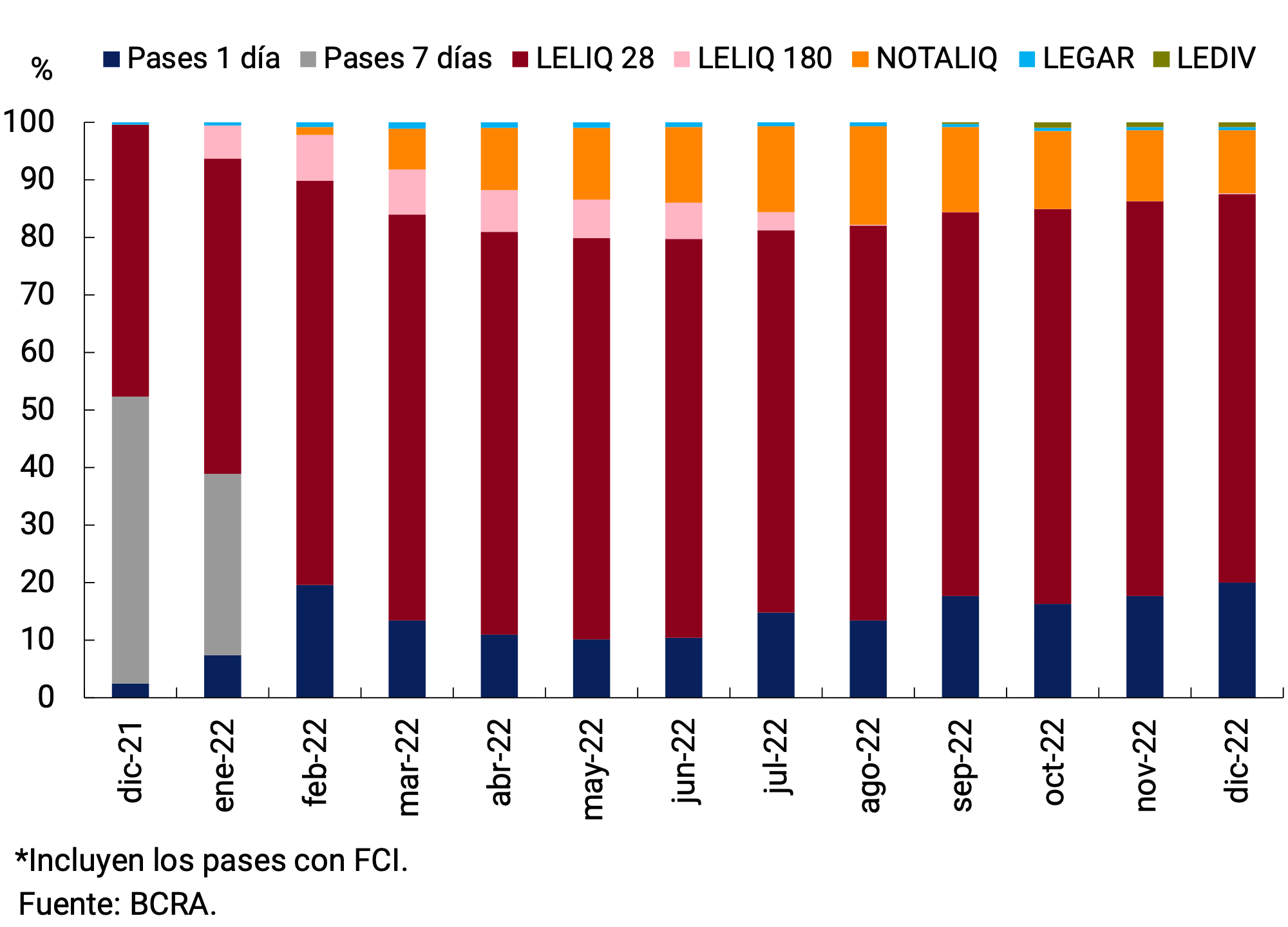

The BCRA kept its benchmark interest rates unchanged in December considering the slowdown in the inflation rate in November, the evolution of December’s leading indicators, and the future outlook for inflation. Thus, the real monetary policy interest rate is in positive territory, which contributes to consolidating financial and exchange rate stability. The interest rate on the 28-day LELIQ remained at 75% n.a. (107.35% y.a.), while the interest rate on the 180-day LELIQ remained at 83.5% n.a. (101.23% y.a.). As for shorter-term instruments, the interest rate on 1-day pass-throughs stands at 70% n.a. (101.24% y.a.); while the interest rate on 1-day active passes stands at 95% n.a. (158.25% e.a.). Finally, the spread of the NOTALIQ in the last auction of the month was set at 8.5 p.p.

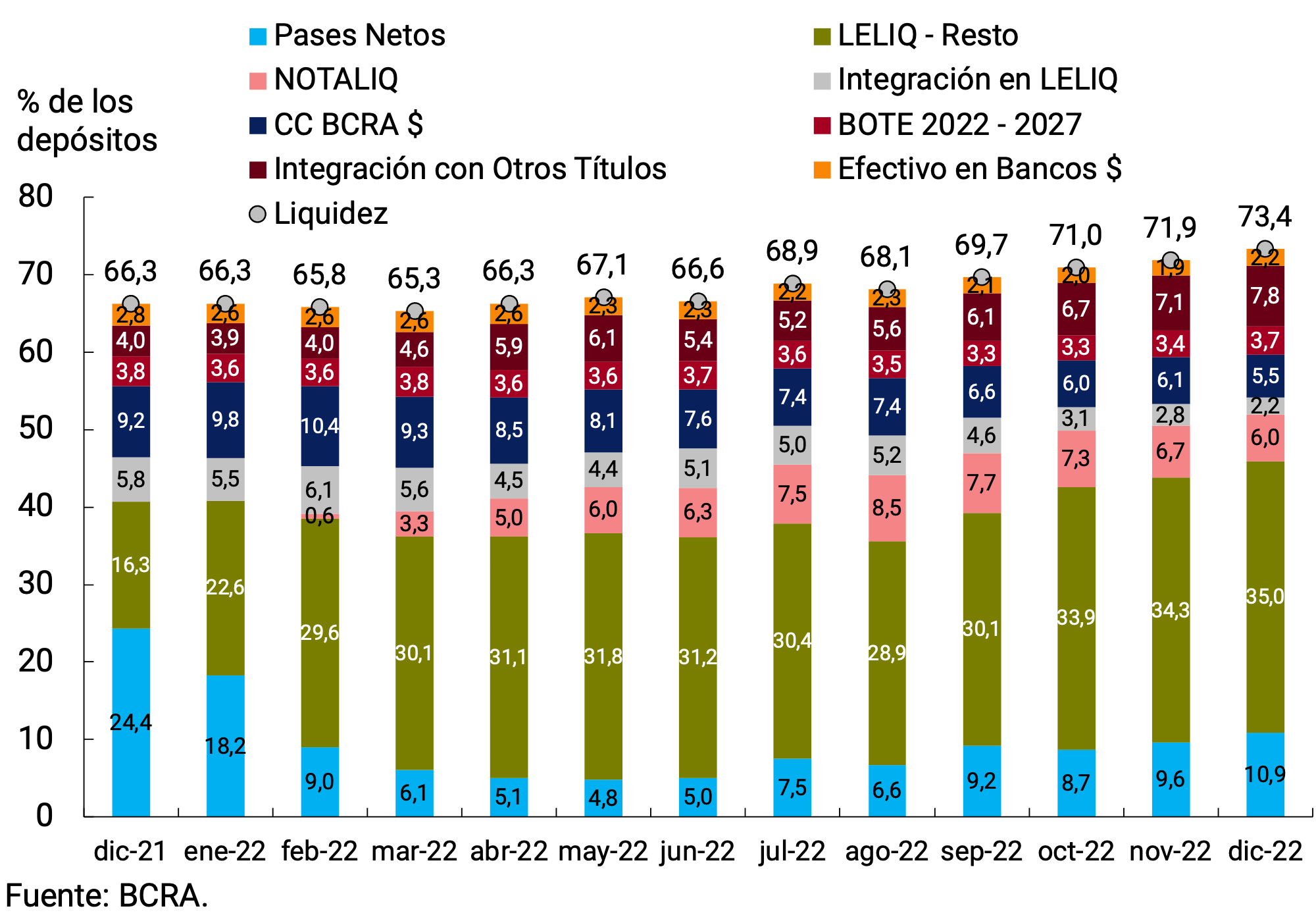

With the current configuration of instruments, in the last month of the year the remunerated liabilities were conformed, on average, at 67.6% by LELIQ with a 28-day term. The longer-term species accounted for 11.1% of the total, almost entirely concentrated in NOTALIQ. Meanwhile, 1-day pass-by-passes increased their share of total instruments, representing almost 20% of the total (2.2 p.p. more than the previous month). Finally, the LEDIVs, together with the LEGARs, accounted for the remaining 1.3%, remaining stable compared to November (see Figure 4.3).

Figure 4.3 | Composition of Interest-Bearing Liabilities of the BCRA

Monthly Average

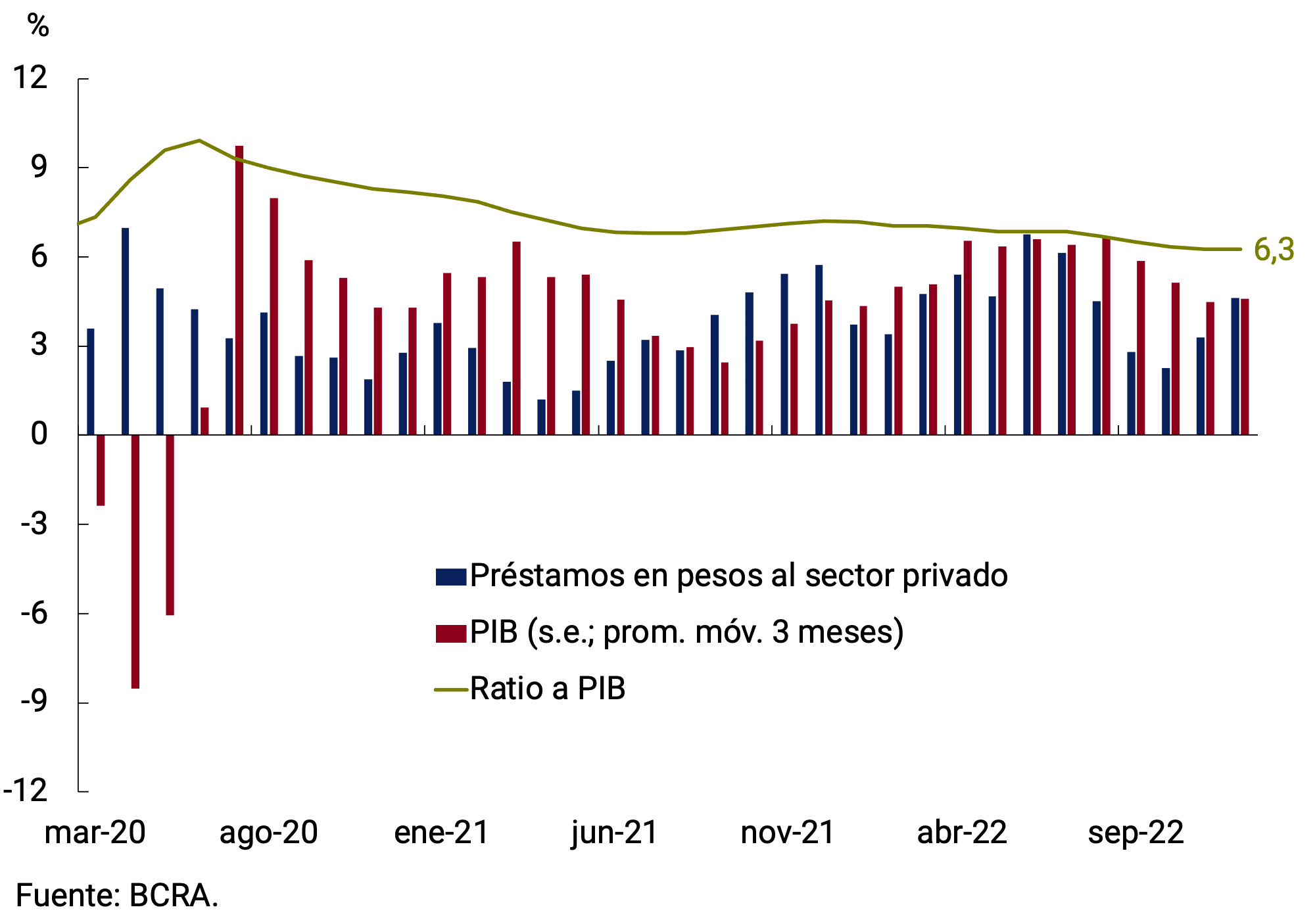

5. Loans to the private sector

During the last month of the year, loans in pesos to the private sector would have remained unchanged in real terms and without seasonality, after 5 consecutive months of decline, with a heterogeneous behavior between loan lines (see Figure 5.1). Thus, throughout 2022 credit would have accumulated a fall of 12.0% in real terms and would have stood at 6.3% in terms of GDP (see Figure 5.2).

Figure 5.1 | Loans in pesos to the private

sector Average monthly variation; Real without seasonality

Figure 5.2 | Loans in pesos to the private

sector In terms of GDP

When observing the evolution of loans by type of financing, mainly commercial lines showed the best relative performance with a monthly drop of only 0.3% s.e. at constant prices, closing 2022 with a contraction of 9% y.o.y. Among these financings, discounted documents (1.6% s.e.; -9.4% y.o.y.) and current account advances (0.5% s.e.; 4.7% y.o.y.) in real terms stood out. On the other hand, financing granted through single-signature documents would have shown a decrease at constant prices of 0.8% s.e. (-9.4% y.o.y.).

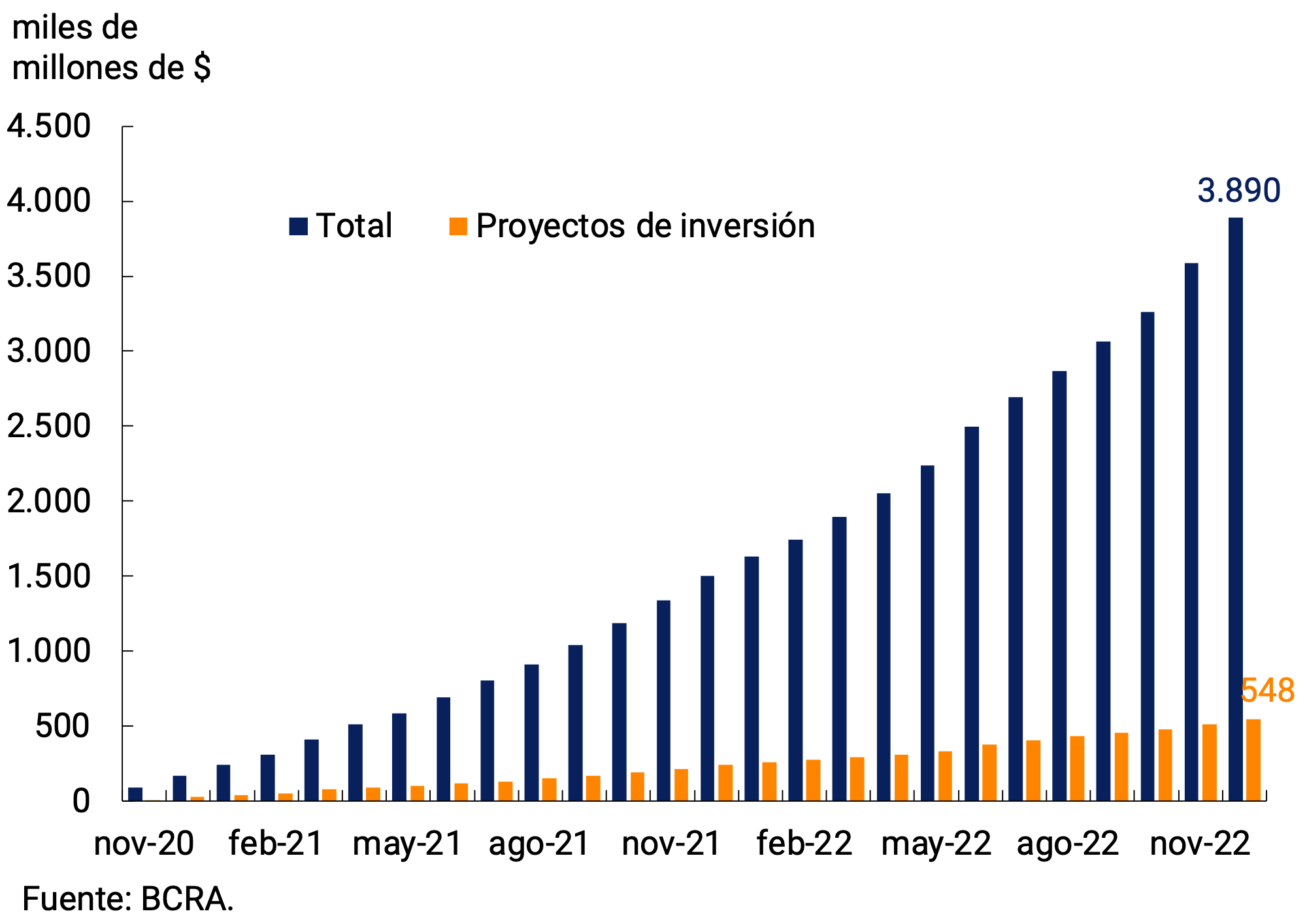

The Financing Line for Productive Investment (LFIP) continued to be the main tool used to channel productive credit to Micro, Small and Medium-sized Enterprises (MSMEs). A fines de diciembre, los préstamos otorgados en el marco de la LFIP acumularon aproximadamente $3.890 miles de millones desde su lanzamiento, con un incremento de 8,5% respecto al mes pasado (ver Gráfico 5.3). Por su parte, del total de las financiaciones otorgadas mediante la LFIP, 14% corresponde a proyectos de inversión y el resto a capital de trabajo. Cabe señalar que, el saldo promedio de las financiaciones otorgadas mediante la LFIP alcanzó aproximadamente a $1.212 miles de millones en noviembre (última información disponible). La línea representa cerca de un 19% de los préstamos totales y 45% del total de los préstamos comerciales.

Figure 5.3 | Financing granted through the Productive Investment Financing Line (LFIP)

Accumulated disbursed amounts; data at the end of the month

Figure 5.4 | Commercial Loans by type of debtor

Var. i.a. at constant prices of the 30-day moving average balance

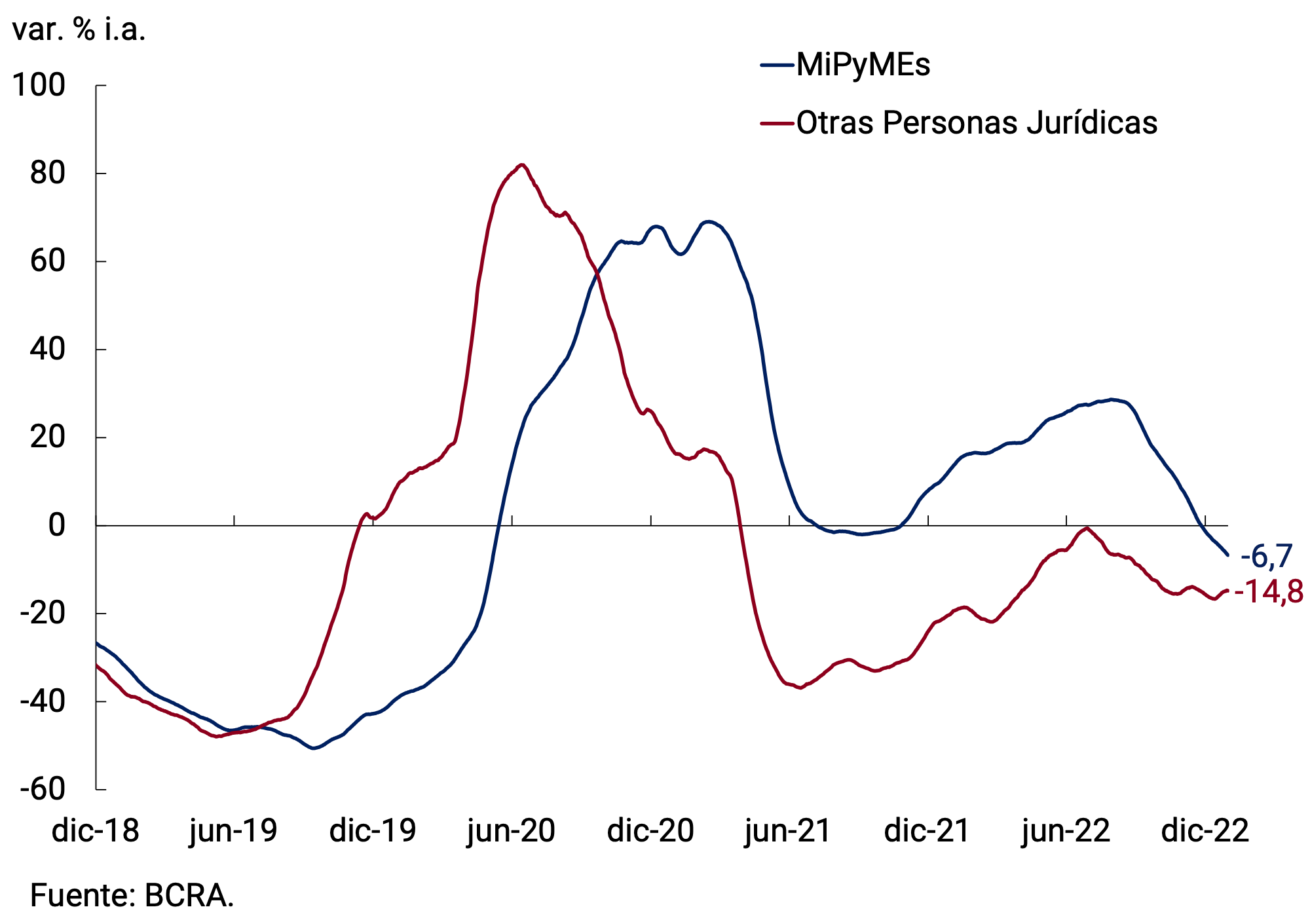

As for commercial credit by type of debtor, it can be seen that credit to MSMEs in real terms would have accumulated a fall of 6.7% in the year, while that destined to large companies would have shown a contraction of 14.8% (see Figure 5.4).

Among loans associated with consumption, financing instrumented with credit cards would have decreased in real terms by 1.0% s.e. in December, with a fall of 12.5% throughout 2022. Likewise, personal loans would have exhibited a 1.6% monthly drop at constant prices and would be 17.1% below the level of December 2021. The interest rate corresponding to personal loans averaged 81.7% n.a. in December (120.5% y.a.), with an increase of 2.5 p.p. compared to the previous month.

With regard to lines with real guarantees, collateral loans would have registered a slight increase in real terms (0.1% s.e.) and would be positioned 5.4% above the record of a year ago. For its part, the balance of mortgage loans would have shown a fall of 3.6% s.e. at constant prices in the month, accumulating a contraction of 30.1% in the year.

6. Liquidity in pesos of financial institutions

In December, ample bank liquidity in local currency7 showed an increase of 1.5 p.p. compared to November, averaging 73.4% of deposits. Thus, it reached a maximum level since the exit from convertibility. The rise was again driven by the BCRA’s interest-bearing liabilities (with increases in net passes and LELIQ, partially offset by the NOTALIQ) and by the integration with public securities (including the new BOTE 2027).

Among the regulatory changes with an impact on bank liquidity, it is worth mentioning that the validity of the minimum cash deduction associated with cash withdrawals at ATMs located in locations included in categories II to VI was extended until June 2023 in accordance with the provisions of the rules on “Categorization of locations for financial institutions”8.

Figure 6.1 | Liquidity in pesos of financial institutions

7. Foreign currency

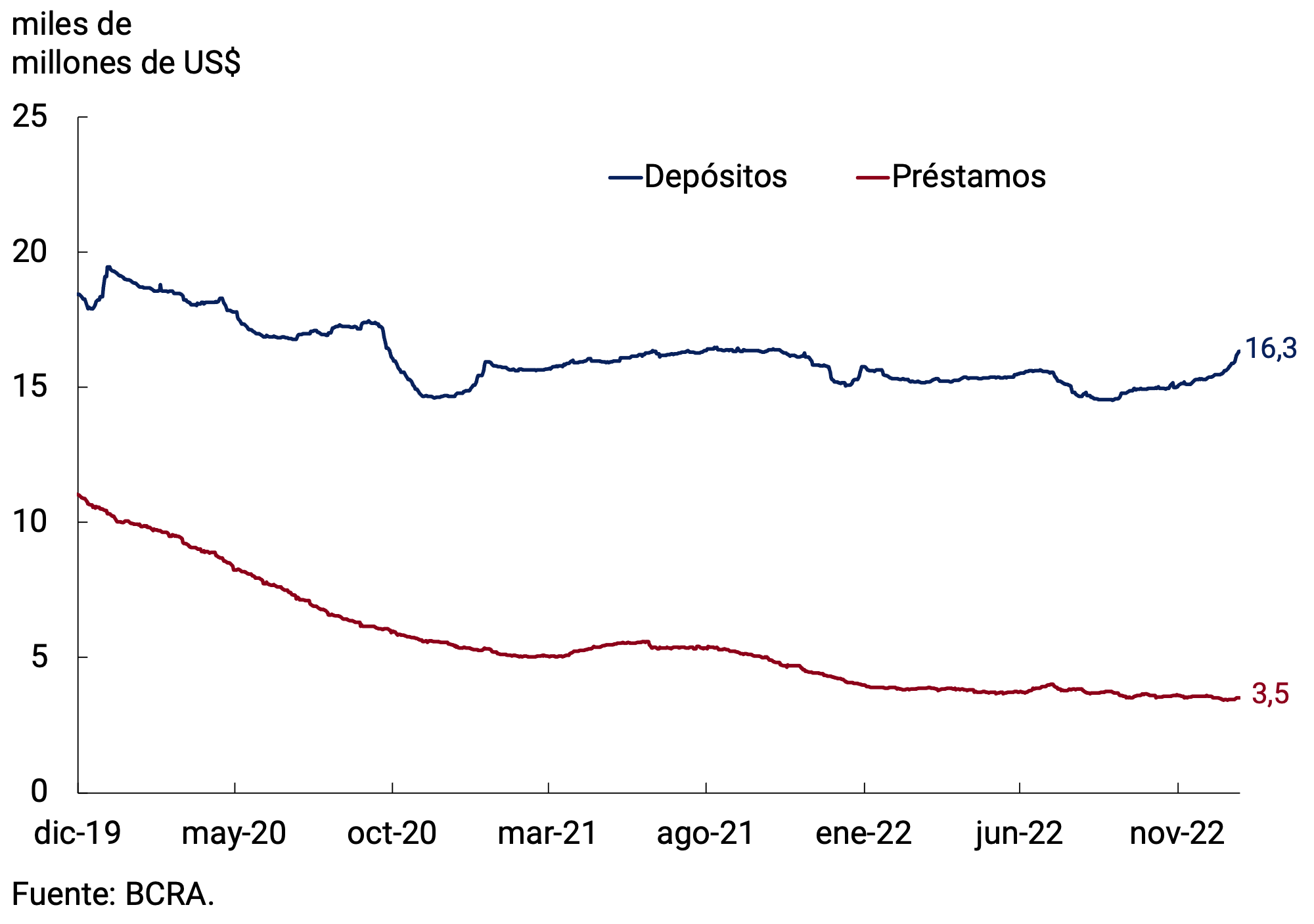

In the foreign currency segment, the main assets and liabilities of financial institutions had a mixed performance. On the one hand, the balance of private sector deposits increased for the fourth consecutive month, averaging US$15,684 million in the month, which implied an increase of US$475 million compared to November. It was mainly explained by demand deposits of individuals, which usually rise at this time of year given the exemption from the payment of the personal property tax to this type of placement. On the other hand, the average monthly balance of loans to the private sector in foreign currency was US$3,488 million, which implied a drop of US$74 million compared to the previous month (see Figure 7.1).

Figure 7.1 | Balance of private sector foreign currency deposits and loans

Figure 7.2 | Liquidity in foreign currency of financial institutions

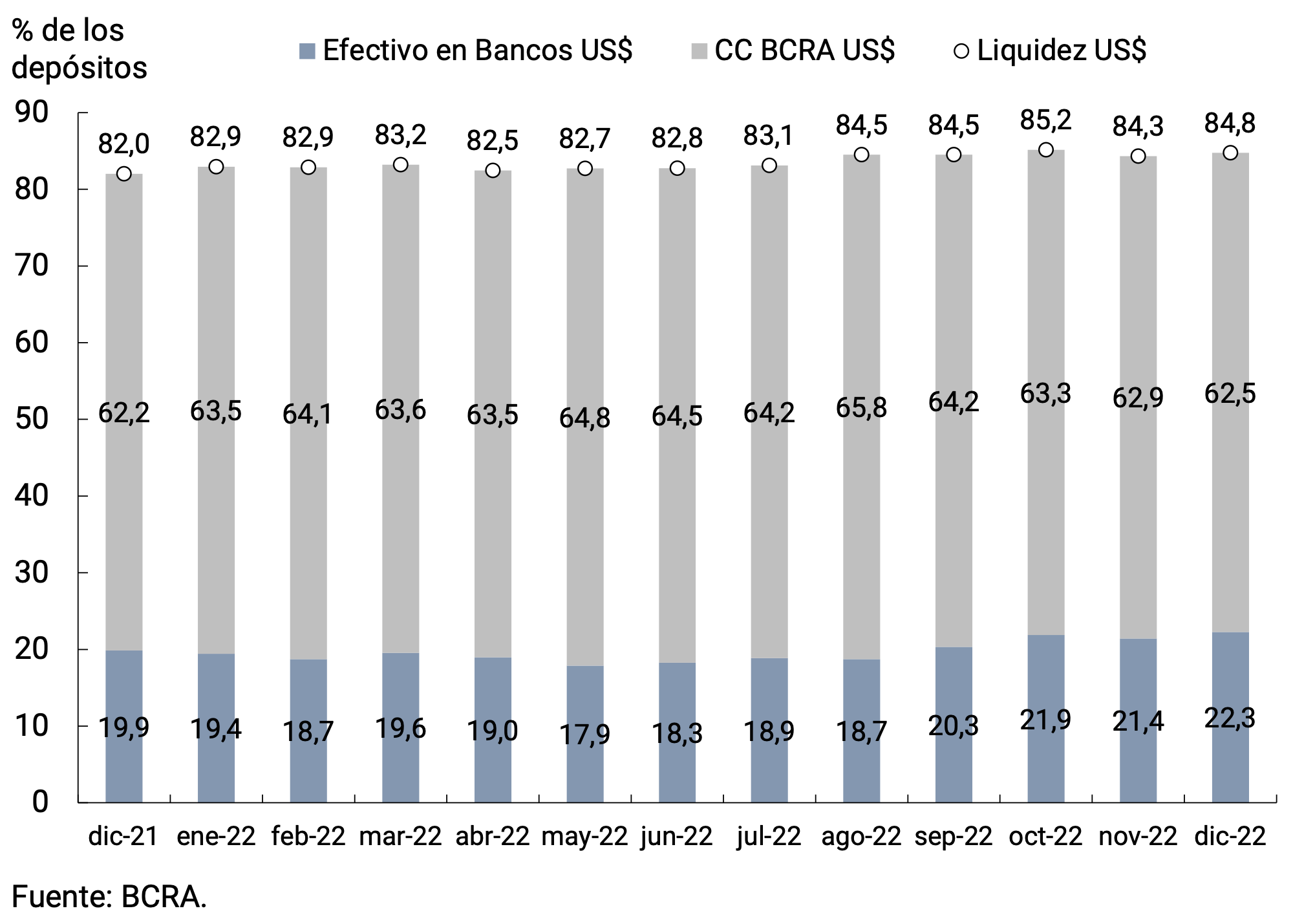

The liquidity of financial institutions in the foreign currency segment experienced an increase of 0.5 p.p. compared to the previous month, standing at 84.8% of deposits in December and remaining at historically high levels. The increase was explained by cash in banks, partially offset by a fall in current accounts in foreign currency (see Figure 7.2).

During December, a series of regulatory modifications took place in foreign exchange matters. Thus, in order to allocate foreign currency more efficiently, access to the foreign exchange market for the payment of imports of a new set of goods linked to health care was made more flexible9. For its part, with the aim of increasing the supply of foreign currency, the amount of the limit of financing admitted in pesos and/or foreign currency to “Large exporting companies”10 was raised and the deadline for entering and settling advances, pre-financing and post-financing from abroad was set at 180 calendar days when the transfer of foreign currency has entered the correspondent account of the local entity as of November 28 of 2022 and until December 3011. Finally, with the aim of promoting the development of certain productive sectors, the obligation to settle exports of goods and services that correspond to activities of the knowledge economywas relaxed 12.

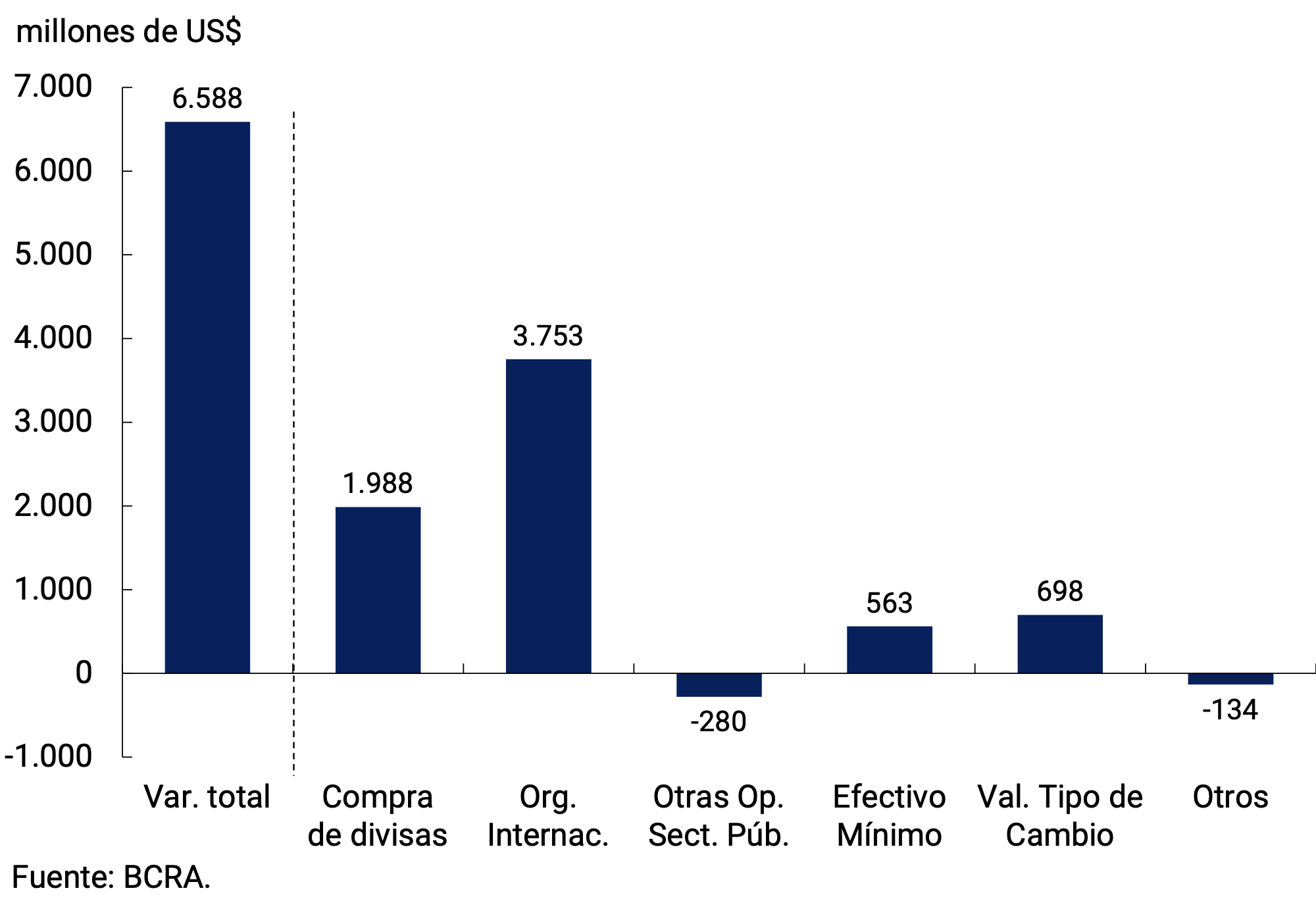

The BCRA’s International Reserves ended the year with a balance of US$44,597 million, registering an increase of US$6,588 million in December. This increase was mainly driven by the disbursement of US$6,021 million from the International Monetary Fund under the Extended Facilities Program (EPP), which was partially offset by capital payments to the IMF of US$2,717 million. In turn, since its reopening on November 28, the Export Increase Program allowed the BCRA to acquire foreign currency for US$3,155 million and, together with the rest of the foreign exchange operations of the private sector, left a net balance of US$2,330 million. Gains from the valuation of net foreign assets and the change in dollar balances in the current account at the BCRA also contributed positively (see Chart 7.3).

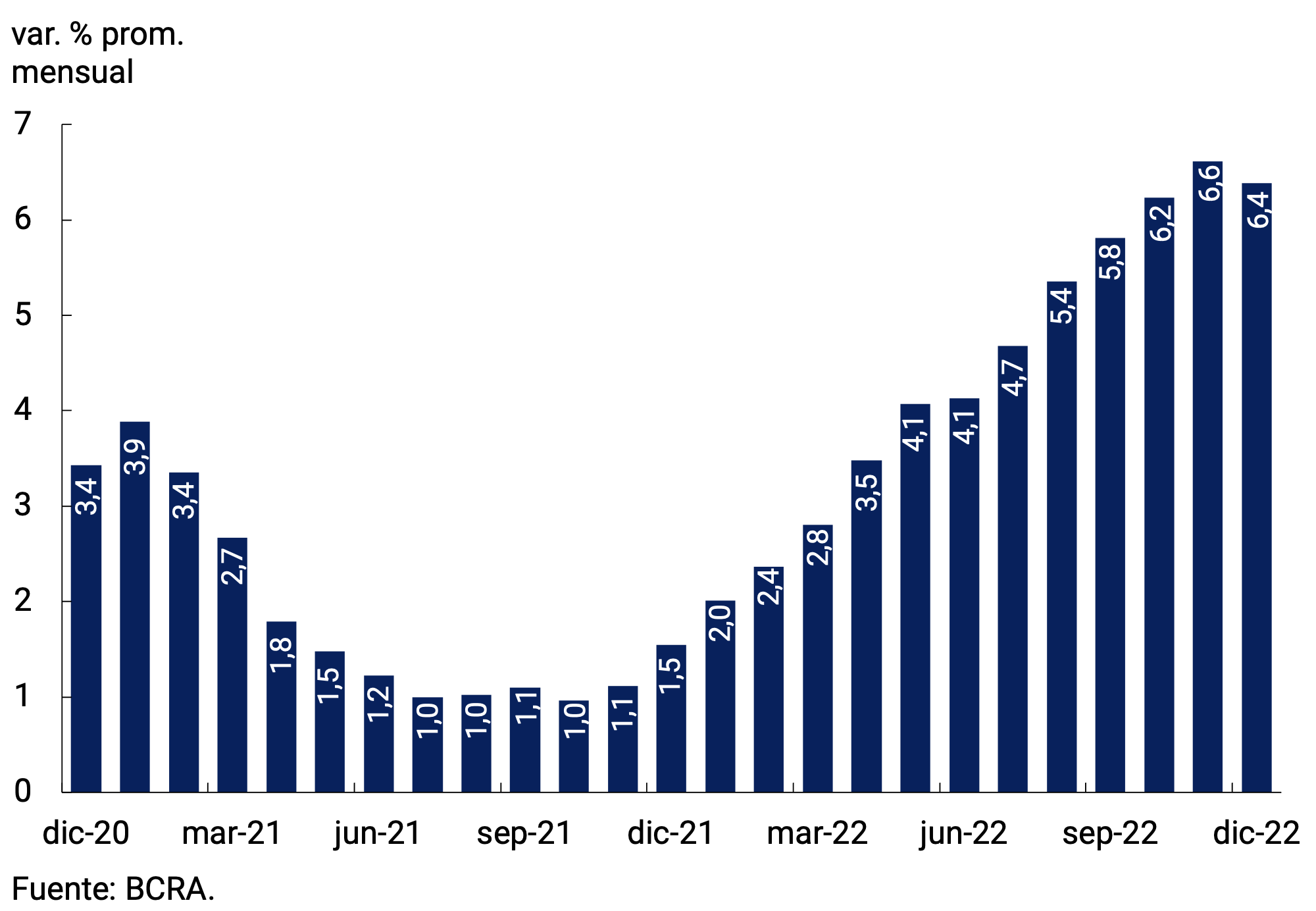

Finally, the bilateral nominal exchange rate (TCN) against the U.S. dollar increased 6.4% in December to settle, on average, at $172.45/US$ (see Figure 7.4). In this way, the BCRA has slowed down the pace of depreciation of the domestic currency in line with the moderation of inflation.

Figure 7.3 | Variation in the balance at the end of the month of International Reserves

: Explanation factors. December 2022

Figure 7.4 | Variation in the bilateral nominal exchange rate with the United States

Glossary

ANSES: National Social Security Administration.

AFIP: Federal Administration of Public Revenues.

BADLAR: Interest rate on fixed-term deposits for amounts greater than one million pesos and a term of 30 to 35 days.

BCRA: Central Bank of the Argentine Republic.

BM: Monetary Base, includes monetary circulation plus deposits in pesos in current account at the BCRA.

CC BCRA: Current account deposits at the BCRA.

CER: Reference Stabilization Coefficient.

NVC: National Securities Commission.

SDR: Special Drawing Rights.

EFNB: Non-Banking Financial Institutions.

EM: Minimum Cash.

FCI: Common Investment Fund.

A.I.: Year-on-year .

IAMC: Argentine Institute of Capital Markets

CPI: Consumer Price Index.

ITCNM: Multilateral Nominal Exchange Rate Index

ITCRM: Multilateral Real Exchange Rate Index

LEBAC: Central Bank bills.

LELIQ: Liquidity Bills of the BCRA.

LFIP: Financing Line for Productive Investment.

M2 Total: Means of payment, which includes working capital held by the public, cancelling cheques in pesos and demand deposits in pesos from the public and non-financial private sector.

Private M2: Means of payment, includes working capital held by the public, cancelling cheques in pesos and demand deposits in pesos from the non-financial private sector.

Private transactional M2: Means of payment, includes working capital held by the public, cancelling cheques in pesos and non-remunerated demand deposits in pesos from the non-financial private sector.

M3 Total: Broad aggregate in pesos, includes the current currency held by the public, cancelling checks in pesos and the total deposits in pesos of the public and non-financial private sector.

Private M3: Broad aggregate in pesos, includes the working capital held by the public, cancelling checks in pesos and the total deposits in pesos of the non-financial private sector.

MERVAL: Buenos Aires Stock Market.

MM: Money Market.

N.A.: Annual nominal.

E.A.: Effective Annual.

NOCOM: Cash Clearing Notes.

ON: Negotiable Obligation.

GDP: Gross Domestic Product.

P.B.: basis points.

PSP.: Payment Service Provider.

p.p.: percentage points.

MSMEs: Micro, Small and Medium Enterprises.

ROFEX: Rosario Term Market.

S.E.: No seasonality

SISCEN: Centralized System of Information Requirements of the BCRA.

SIMPES: Comprehensive System for Monitoring Payments of Services Abroad.

TCN: Nominal Exchange Rate

IRR: Internal Rate of Return.

TM20: Interest rate on fixed-term deposits for amounts greater than 20 million pesos and a term of 30 to 35 days.

TNA: Annual Nominal Rate.

UVA: Unit of Purchasing Value

References

1 Corresponds to private M2 excluding interest-bearing demand deposits from companies and financial service providers. This component was excluded since it is more similar to a savings instrument than to a means of payment.

2 The rates currently in force are those established by Communication “A” 7527.

3 The rest of the depositors are made up of Legal Entities and Individuals with deposits of more than $10 million.

4 Private M3 includes working capital held by the public and deposits in pesos of the non-financial private sector (demand, term and others).

5 Also, as already mentioned, to deposits with adjustment according to the quotation of the reference exchange rate.

6 Within the operations of the public sector, the purchase of SDRs from the National Treasury stands out.

7 Includes current accounts at the BCRA, cash in banks, balances of net passes arranged with the BCRA, holdings of LELIQ and NOTALIQ, and public bonds eligible for reserve requirements.

Share on