Executive summary

Total access points increased by 5.8% during 2019 | The financial system registered 30,726 access points (PDAs) as of December 2019. A predominance of electronic devices is observed, contributing 82% among ATMs and self-service terminals. Complementary financial services agencies (ACSFs) accounted for 0.2% of the total number of PDAs with 54 units distributed in the interior of the country.

There is a marked disparity in the distribution of FLW between provinces and between the departments that compose them | As of December 2019, 41.9% of the localities had at least one FLW and concentrated 91.3% of the adult population. Considering the adult population by locality, there is a decrease in the coverage index as the number of inhabitants decreases: only 22% of localities with less than 2,000 adult inhabitants had at least one PDA.

Extra-bank withdrawal points equated to ATMs | These points demonstrate a provincial distribution similar to that of the PDAs, with 65% concentrated between CABA, Buenos Aires, Córdoba and Santa Fe. The main items identified are supermarkets (21% of the total), service stations (13%) and pharmacy and perfumery stores (8%), while bill collection and service centers comprise 13% of the points.

Over the last decade, there has been an average year-on-year growth of about 8% in the number of deposit accounts in pesos per 10,000 adults | On average, 1.4 deposit accounts in pesos were registered per adult as of December 2019; 64% of them are associated with the receipt of some kind of periodic accreditation – salaries, retirements, pensions and social programs. On the other hand, 66% of deposit accounts registered a very low average monthly balance (less than $3,000), which would indicate the low use of deposit accounts for both transactional and passive savings purposes.

The number of fixed-term deposits in pesos per 100 deposit accounts in pesos has remained constant for a decade | This metric stood at 6 fixed terms in pesos for every 100 deposit accounts in pesos as of December 2019, a value around which it oscillated during the last ten years. This number reflects that only a small proportion of peso deposit account holders use fixed-term deposits as a savings instrument.

Electronic means of payment continued their growth path | Debit, credit and prepaid card purchases and electronic transfers registered increases relative to the population in recent years, despite the absence of growth in economic activity. In 2019, for every 100 cash withdrawals per adult, almost twice as many transactions were carried out by electronic means of payment.

The geographical distribution of fixed-term balances per adult has been extremely heterogeneous over the last decade | CABA, the district with the highest figures over time, exceeded each of the provinces of the NOA and NEA by at least 3 times as of December 2019. Likewise, while CABA presented a 13% drop in real terms over the last decade, Formosa (NEA) and Catamarca (NOA) registered a growth of 89% and 67%, respectively.

Half of the adult population had at least one funding as of September 2019 | Discrimination against this value indicates that 37% of adults had at least one financing granted by financial institutions. Considering an expanded financial system (SFA), which includes non-bank credit and/or purchase card issuers (ETCNBs) and other non-financial credit providers (NPPOCs), that figure rises to 49%. This access to credit is not homogeneous between men and women, with a gender gap to the detriment of women for the percentage of adults who access financing (5.8 p.p. in the SFA).

There is a disparity in the population with financing by region of the country | The NEA (40%), NOA (44%) and Cuyo (45%) regions were, in general, below the national average, while Patagonia (52%) and the Central region (51%) were above the national average.

The number of individuals with debt in an irregular situation increased | 74% of the SFA’s debtors were in a regular situation as of September 2019, i.e. they were able to adequately meet all their financial commitments. The reduction of 4 p.p. in the indicator during the previous 24 months is noteworthy. The disaggregation of this indicator according to the gender of the debtors denotes a difference in the repayment behavior of men and women, with women registering a higher percentage of debtors in a regular situation than men (75.7% vs. 72.4%).

Access to credit for MSMEs has steadily improved over the last decade | To a greater or lesser extent depending on the sector, size and region, the proportion of MSMEs with financing increased year after year. In the case of microenterprises, which represent 84% of all companies, the proportion increased from 38% to 53% from December 2007 to December 2018 in the case of those incorporated as legal entities and from 61% to 81% in the case of individuals who carry out a business activity.

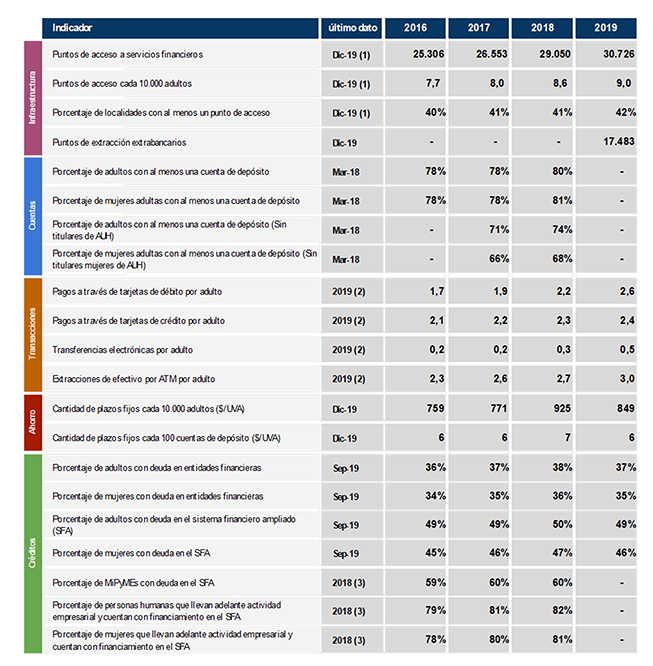

Indicator Table | Financial inclusion in Argentina

Notes:

(1) This includes access points for financial institutions (branches, mobile branches, ATMs, self-service terminals and complementary financial services agencies) and ATMs operated by non-financial institutions.

(2) Monthly average for each year.

(3) Data corresponding to companies incorporated as legal entities with financing during any month of 2018.

Local context

The integration of all households and businesses into financial services is a necessary step towards achieving a more equitable financial system. For this reason, the BCRA is implementing an active agenda for financial inclusion, understood as a key aspect to achieve social inclusion, prioritizing access to and use of financial services for the most vulnerable sectors.

Access to a bank account is presented as the first of a series of steps to consider the financial inclusion of an individual or company. Having a bank account allows access to financial services such as fund transfers, service payments, savings instruments and access to electronic channels such as internet banking and mobile banking.

For those who do not have a bank account, in January 2020 the Universal Free Account (CGU) that had been discontinued in 2016 was restored. This bank account is opened with the sole presentation of the DNI, it has no opening or maintenance cost, and all banks must offer it and open it at the request of unbanked people.

Another key aspect of financial inclusion lies in the use of savings products by individuals and companies. Saving allows the population, in general, to face unforeseen expenses or emergencies, plan the purchase of goods and services in the future and make investments to generate more wealth.

The low proportion of people who save in the financial system is observed in different segments of the population and is reflected in the intensity of use of instruments such as fixed-term loans. Since 2010, the number of fixed terms per 100 deposit accounts – both in pesos – has not changed greatly, going from 5 fixed terms in 2010 to 6 in December 20191.

To encourage savings in domestic currency, in January of this year a fixed-term alternative in UVA2 was promoted, guaranteeing a yield above the evolution of the consumer price index of at least 1%. Its minimum incorporation period is 90 days, but you can opt for early cancellation from 30 days after hiring. A significant proportion of the balance of fixed terms in the non-financial private sector is denominated in pesos and UVA (81% as of December 20193) and does not have the option of early cancellation.

In terms of credit, the financial system has pending challenges in the access of individuals and micro, small and medium-sized enterprises (MSMEs), which present asymmetries at the geographical level and company size. Four out of 10 adults4 own at least one credit product in financial institutions. This number rises to 5 out of 10, if non-financial credit providers who report their debtors to the BCRAare included 5. This indicator is mainly explained by the possession of credit cards (38% of the adult population), with access to medium and long-term instruments being extremely low (1.3% for pledge loans and 0.7% for mortgages)6.

At the gender level, access to credit products presents a gap to the detriment of women of 5.8 percentage points (p.p.) of difference in the percentage of adults with a product for each gender, while at the geographical level, the provinces located above the national average in terms of access to financing (49%) are located within the Central and Patagonian regions. while the NOA, NEA and Cuyo are several percentage points below.

Likewise, the adverse macroeconomic conditions in which the economy operated, and in particular the persistence of high interest rates in a context of contraction in activity, were reflected in the proportion of individuals and companies with financing in an irregular situation. In this sense, of the total number of individuals with access to credit, the proportion of those in an irregular situation increased by 4 p.p. between September 2017 and the same month in 2019. For its part, in the last two years, the proportion of companies with debt in an irregular situation grew by around 3 p.p. for all company sizes.

In this context, the BCRA relaxed the regulatory conditions to encourage credit to families through the AHORA 127 Program, which makes it possible to purchase goods in fixed installments without interest through bank credit cards, and modified limits on the annual nominal interest rate for financing through credit cards8 banking and non-banking. Both measures seek to boost the recovery of consumer credit and protect the most vulnerable sectors.

In addition, to avoid abusive practices and promote greater financial inclusion, the prohibition of using interbank direct debit for loan collection was prohibited, which was designed as a voluntary and reversible payment tool9. From this measure, the interbank debit linked to new loans can be processed through the so-called “spot DEBIN”, a mechanism that requires the express authorization of the receiving customer prior to making each debit.

The financing of productive and business activity, in which companies registered as individuals (PH companies) and others as legal entities (PJ companies) participate, raises the need to generate more equitable access with respect to the size of the production unit. In the case of PJ companies, half of the microenterprises have taken financing during 2018, while large companies did so almost in their entirety. This situation is more balanced in the case of PH companies, although the weight of financing in the financial system is substantially lower than that registered by PJ companies (10% vs. 90%). In line with the aforementioned measures for individuals, the BCRA readjusted the regulatory conditions to encourage financing to MSMEs at a fixed interest rate of less than 35% per year10.

In terms of protection for users of financial services, new regulations were established for payment service providers (PSPs): (1) the funds of customers credited to payment accounts must be in demand accounts, in pesos, in financial institutions in the country and, at all times, immediately available upon request and (2) customers may apply the balances of payment accounts in common funds of money and the PSP must report the balances invested separately from the rest of the funds.

Although this type of payment accounts could contribute to the financial inclusion of the population, when combined with investment instruments and little information about the associated risks, it can lead to unexpected results for the user in the face of falls in the profitability of mutual funds.

Responses to Financial Inclusion Challenges in the Context of the Health

EmergencyIn the context of the health emergency affecting the world’s population, the BCRA has issued a set of regulations aimed at mitigating the impact of the economic crisis as a result of the Coronavirus COVID-19 pandemic. These measures aim to ensure that the financial system can provide more support to both companies and families and that the payment chain does not suffer. The most relevant measures from the perspective of financial inclusion are mentioned, which are explained in greater detail in the Regulatory Annex.

In line with the mandatory quarantine ordered by the National Executive Branch, branches remained closed to the public, and financial institutions must continue to provide services to users remotely11. By way of exception, branches were opened for the payment of social security and pensions and social assistance benefits, plans or programs12. Subsequently, the branches opened to the general public, with limitations on operations and through a shift system to avoid the agglomeration of people in the branches.

In the case of companies, the measures promoted the offer of financing lines to MSMEs at low cost (maximum annual interest rate of 24%) applied to working capital. Subsequently, the incentives for these lines were increased when the funds are intended for the payment of salaries to employees13. The National State, through the Argentine Guarantee Fund (FoGar), made available a fund to guarantee MSME working capital loans, for up to 100% in the cases of micro and small enterprises and monotributistas of all categories; and 25% in the cases of medium-sized companies section 1 and 214.

In the case of individuals, incentives were increased for financial institutions to allocate financing to the AHORA 12 Program in order to meet the consumption of families and the suspension of charges and commissions for operations carried out through all ATMs15 was established. In relation to credit card maturities, it was determined that: (1) the unpaid balances of credits granted by financial institutions, whose installments are due between 01.04 and 30.06, do not accrue punitive interest, and (2) their cancellation is made once the mandatory quarantine is over, without any surcharge and with a financing rate not exceeding 49%16. Subsequently, a reduction to 43% of the maximum annual nominal rate for compensatory interest that financial institutions can receive for balances financed in credit cards was ordered. Likewise, they must automatically refinance the unpaid balances of credit cards with a one-year term with a 3-month grace period and 9 monthly installments, equal and consecutive to said rate.

For both individuals and companies, the parameters with which bank debtors are classified were temporarily made more flexible. The current classification system takes into account, among other variables, the number of days of arrears of each debtor. Until September 2020, a period of 60 days will be added to the classification of each debtor for each category, allowing the difficulties caused by the crisis in various branches of economic activity to be contemplated17.

1. Physical infrastructure

Physical infrastructure plays a fundamental role in the access of people and companies to the financial system, providing face-to-face and electronic service channels for carrying out operations. These points perform different functions, such as making payments, withdrawals or transfers, channeling savings through different investment instruments or applying for a loan, among others.

In a large territory such as Argentina, the geographical coverage of financial services poses an additional challenge. It is not only relevant to analyze infrastructure indicators in relation to population, but also to observe what happens at the level of different administrative or territorial units. In this sense, access points can be analyzed within the perimeter of a province or department or according to an area that does not obey a political division but, on the contrary, that verifies certain particular socioeconomic characteristics. Following international guidelines, Financial Services Access Points (PDAs) are defined as any physical entity where a person can carry out their deposit or withdrawal operations with a financial institution.

In our country, PDAs are made up of bank branches (including mobile branches),18 ATMs, self-service terminals (TAS) and complementary financial services agencies (ACSFs, known in the literature as banking correspondents).

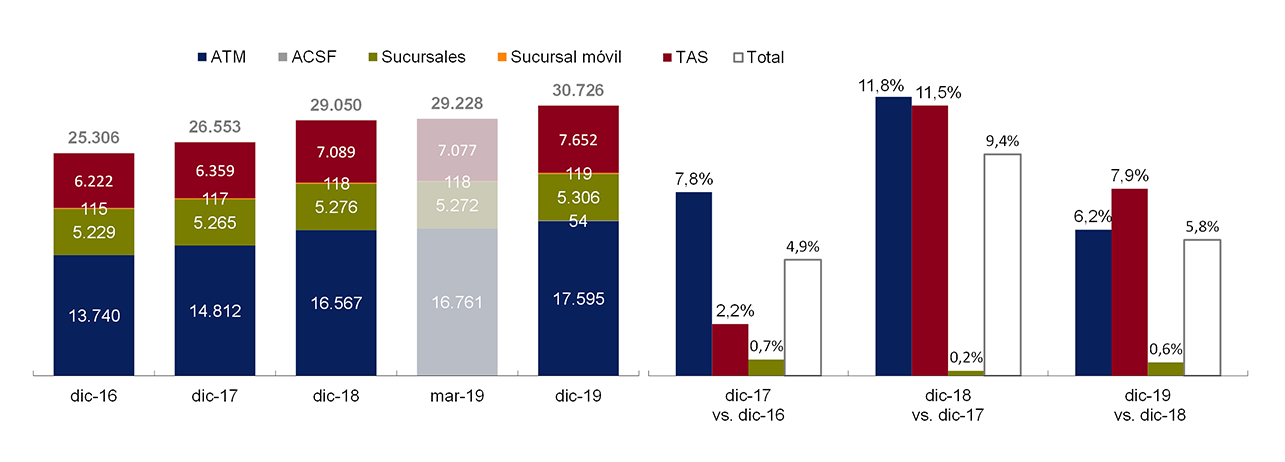

As of December 2019, the financial system registered 30,726 PDAs nationwide, showing a growth of 5.8% compared to the same month in 2018. As for the distribution among the different types of PDAs, 57.3% corresponded to ATMs, 24.9% to TAS, 17.3% to branches and 0.4% to mobile branches. The ACSFs, whose figure was incorporated into the local regulation in November 2018, did not present a significant contribution, having reached only 54 units (0.2% of the total). The sustained growth of FLW, which outpaces population growth, shows an improvement in the availability of FLW by the financial system.

The distribution shows a predominance of electronic devices over PDAs that imply greater physical and human infrastructure requirements for their operation, a trend that is observed globally. In general, electronic devices are located inside branches (74% for ATMs and 99% for TAS), while the remaining part are installed in other locations, such as supermarkets, service stations or shopping centers. It should be noted that the latter allow for greater decentralization of the ADPs, helping to increase geographical coverage and improving the population’s access to financial services.

The evolution of FLW shows an upward trend, with an average year-on-year growth of 6.7% in the last three years. At the individual level, ATMs are the type of PDA that shows the greatest increase (8.6% year-on-year average -p.i.), followed by TAS (7.2% p.i.) and, finally, branches, with very little significant growth (0.5% p.i.). In other countries in the region (and globally as well), the low growth of branches is associated with several factors, such as the significant growth in the number of banking correspondents and the remote or electronic provision of financial services.

Figure 1.1 | Number of FLDs by type and annual growth

Source | BCRA and networks.

As mentioned above, the absolute amount of ACSF is still low and, although regulation allows financial institutions to delegate to them all the activities they carry out with their customers, only a third allow transactional operations such as cash withdrawals and the collection of taxes and services, thus reducing the potential impact in terms of financial inclusion. A positive aspect is that all the ACSFs are located outside CABA and Buenos Aires, feeding more PDAs to the interior of the country.

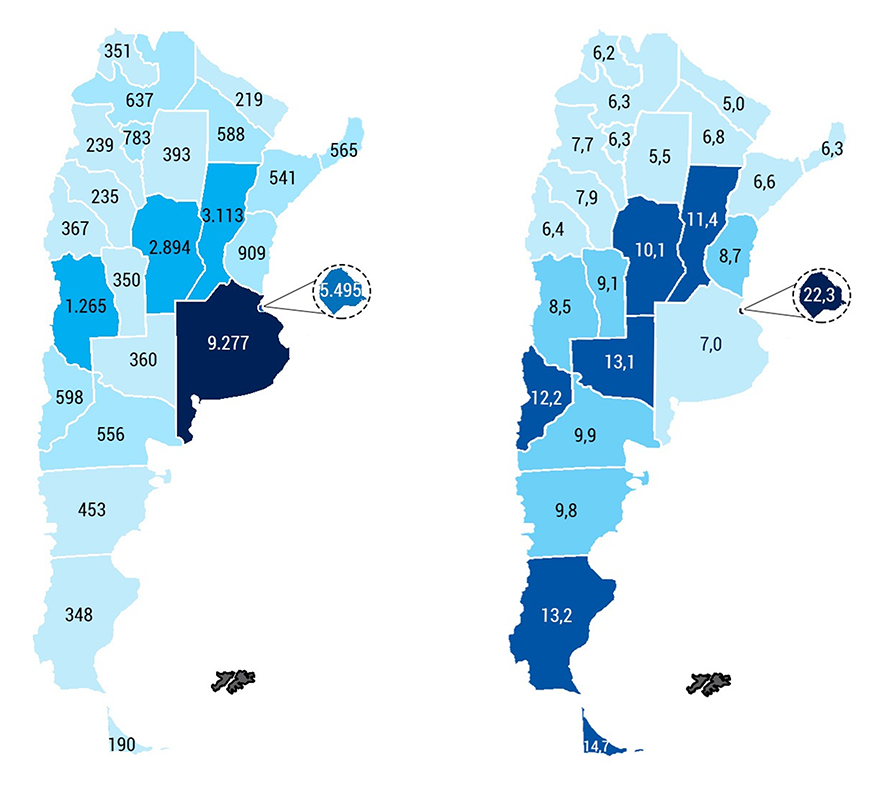

At the provincial level, 48% of the ADPs were concentrated in CABA and Buenos Aires, which shows marked differences in their geographical distribution. Among other factors, these disparities are associated with the distribution of the population, since districts with a greater number of adults would tend to have a greater amount of FLW. Thus, for the purposes of making a more accurate comparison between jurisdictions, it is necessary to take into account the number of inhabitants of each one.

As of December 2019, Argentina had 9 PDAs per 10,000 adults, with CABA being the jurisdiction with the best performance (22.3), while Tierra del Fuego, despite being the province with the lowest absolute number of PDAs, was in second place (14.7). Additionally, it is observed that all the provinces that make up Patagonia19 exhibited values above the national average, while the provinces of the NEA and the NOA presented a behavior below the average for this indicator. Compared to the previous report (data as of March 2019), improvements are evident in all provinces, with Neuquén and La Rioja presenting a greater increase in FLW per 10,000 adults, with increases of 1.3 and 1 FLW per 10,000 adults, respectively.

Figure 1.2 | Distribution by province of FLW and ADP per 10,000 adults

Note | Data as of December 2019.

Source | BCRA, networks and INDEC.

Just as there is a marked disparity in the distribution of FLW between provinces, the same phenomenon is recorded within each one, with clear differences between the levels of FLW in the departments that compose them. As an example, the province of Buenos Aires agglomerates districts such as San Isidro or Vicente López with 19.2 and 18.3 PDA per 10,000 adults, respectively, which more than double the national indicator, and others such as Florencio Varela or José C. Paz with 3 and 2.3 PDA per 10,000 adults, respectively, with a third or less of the national value. These disparities between departments or parties are observed in all Argentine provinces.

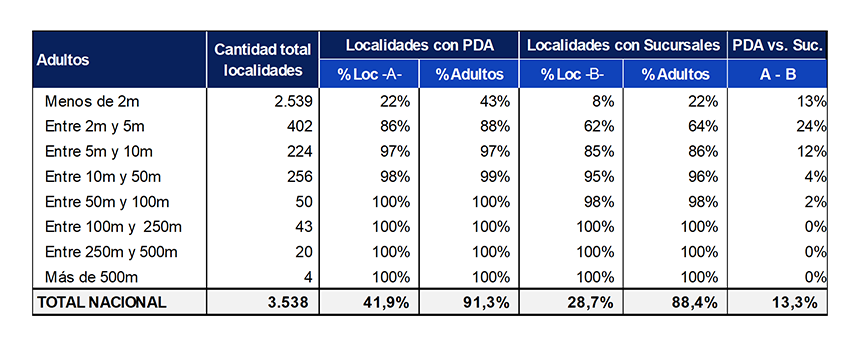

In relation to FLW coverage, 41.9% of Argentine localities had at least one FLW as of December 2019, showing a small improvement in recent years, from 39.6% in December 2016. However, while the percentage of localities covered may seem low, it is appropriate to consider the population of each locality in order to determine the percentage of the population that has access to a PDA in the locality in which it resides. In this sense, as of December 2019, it is observed that 91.3% of the adult population lived in a locality that had at least one FLW, while the remaining population lived in rural areas (5.8% of the total adult population) or in localities without ADP (2.9%).

Along the same lines, considering the number of adults living in each locality, it is possible to segment the localities to perform a more precise analysis of PDA coverage. Thus, as of December 2019, all adults living in towns with more than 50 thousand adult inhabitants had at least one PDA in their locality. As the number of inhabitants is reduced, a decrease in the coverage index is observed. This is accentuated for localities with less than 2 thousand adult inhabitants, given that only 22% had at least one PDA, leading to only 43% of adults living in localities of this population size having at least one PDA in their locality.

The same analysis can be done to identify those localities that have at least one bank branch, which is the type of PDA that offers bank customers the most complete range of services. This analysis is particularly useful to determine the quality of coverage, since there are localities whose only PDA is an ATM in which to carry out certain operations (apply for a loan, for example) residents must move to another locality that has a branch.

Figure 1.3 | Coverage of localities by at least one PDA

Note | m = thousand. The national population also considers the dispersed rural population.

Source | BCRA, networks and INDEC.

Branch coverage is relatively lower, considering that 28.7% of the country’s localities had at least one bank branch in December 2019 compared to 41.9% if we consider all types of PDAs. The difference between the two indicators indicates that 13.3% of the localities are covered by a type of PDA other than bank branches. They obtain their coverage mainly through ATMs installed outside bank branches and, to a lesser extent, mobile branches.

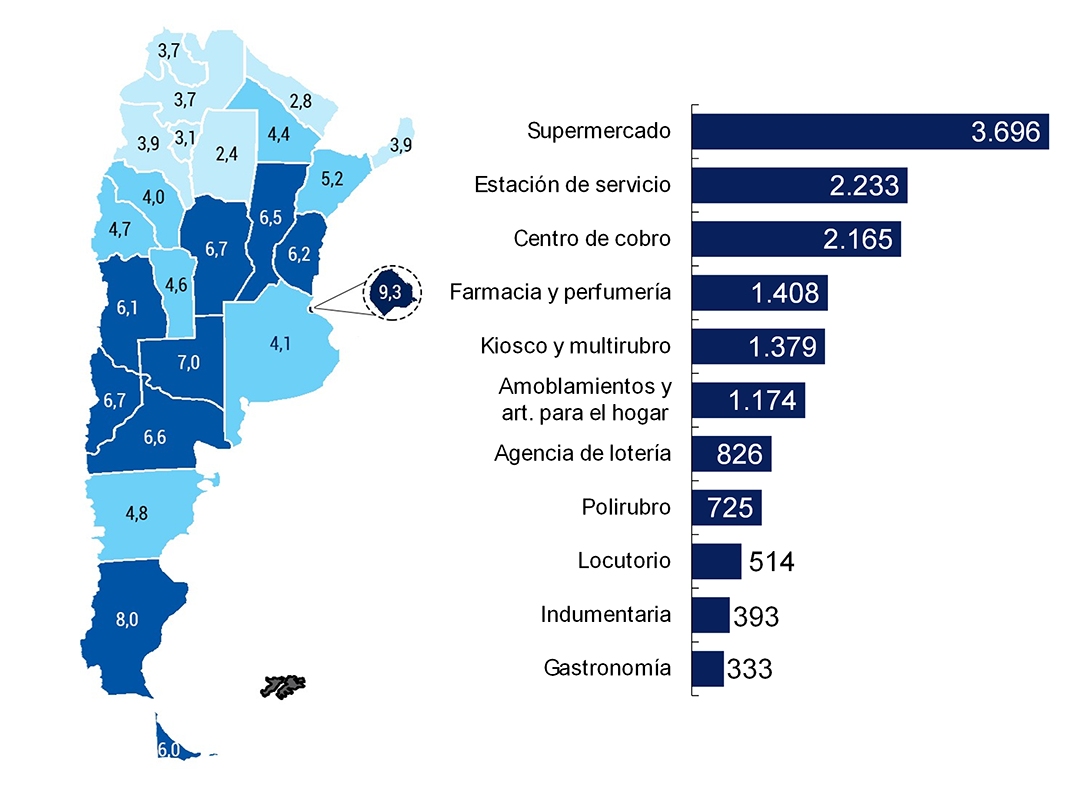

In addition to bank access points, there are other types of points in our country where the population can exclusively make cash withdrawals. These extra-bank withdrawal points include businesses such as supermarkets, pharmacies, service stations, among others, and extra-bank collection networks that offer the cash withdrawal service. Through the use of debit cards, customers can get cash that is debited from their bank account.

A survey carried out by the BCRA indicates that as of December 2019, a total of 17,483 non-bank withdrawal points were registered nationwide, with a notable growth in this type of points in recent years. The provincial distribution of non-bank withdrawal points is similar to that of the PDAs, with 44% concentrated between CABA and Buenos Aires and 65% considering Córdoba and Santa Fe.

The main items identified are supermarkets (21% of the total points), service stations (13%) and pharmacy and perfumery stores (8%). On the other hand, the collection centres for invoices and services comprise 13% of the extra-bank withdrawal points20. Although the non-bank withdrawal points do not offer the variety of financial services associated with the PDAs of the financial system, these extra-bank points are equivalent to the total number of operational ATMs, thus improving the population’s access to cash and contributing to financial inclusion.

Figure 1.4 | Number of non-bank withdrawal points per 10,000 adults and by main items

Note | Data as of December 2019. The breakdown by item shows the main items identified, but does not cover all the points.

Source | BCRA survey based on data from Mastercard, Cabal, Visa, Rapipago, Pagofácil, Plus Pagos, Pago24 and Bica Ágil.

2. Deposit accounts and payment and savings methods

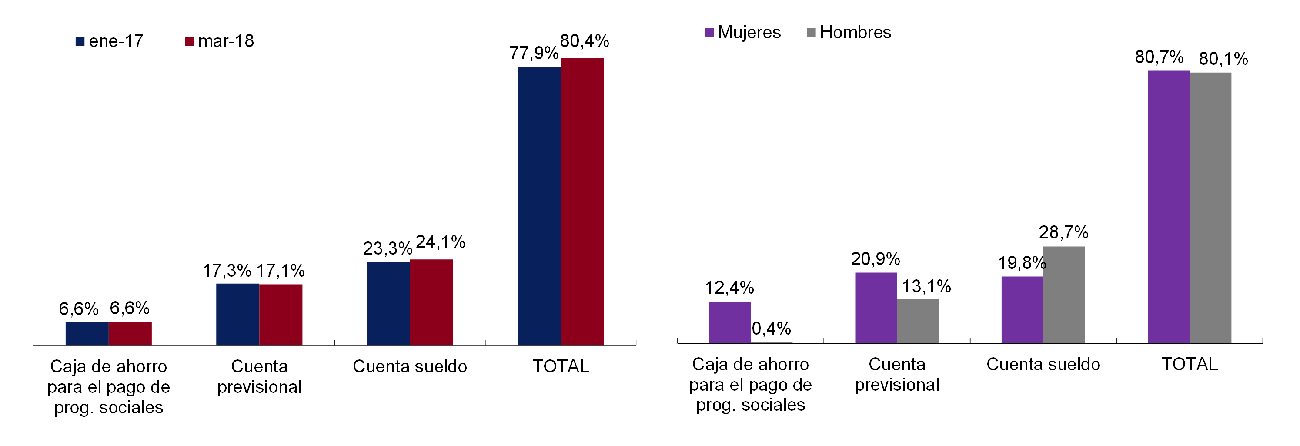

Bank accounts provide a secure way to store money and manage expenses and income, making it easy to pay for utilities, send and receive funds, build savings, and access credit. In Argentina, 80% of the adult population had at least one bank account as of March 2018, without any gender gap. The figure drops to 74% if the number of holders who receive the Universal Child Allowance (AUH), one of the main social assistance programs in our country, is subtracted. In this case, there is a gap of 11.5 p.p. to the detriment of women, given the high proportion of women in the AUH benefit (97%).

One of the most common uses of an account is to make payments. Electronic means of payment facilitate transactions for the population and, at the same time, contribute to reducing the use of cash. In each of the metrics of electronic means of payment in Argentina – purchases with debit, credit and prepaid cards and electronic transfers – there were increases relative to the population during the last time, despite the fact that economic activity has stagnated or fallen in the last five years. Thus, in 2019, for every 100 cash withdrawals per adult, almost twice as many transactions were carried out by electronic means of payment.

Accounts provide a way to generate savings for the future, although not the only way. Savings are the part of income that is not used for consumption and is intended to face unforeseen expenses or emergencies, buy goods and services in the future, and make investments to generate more wealth. According to the Survey for the Measurement of Financial Capabilities carried out in Argentina in 2017, approximately 1 in 3 people had saved money in the previous year, being more common in men (32%) than in women (26%). In the case of active savings, the use of fixed-term deposits (hereinafter, fixed-term) as a savings instrument was low in proportion to the number of deposit accounts in our country (6 fixed-term deposits per 100 deposit accounts, both in local currency), a ratio that remained practically constant over the last decade. which indicates that only a small number of deposit account holders would use this savings instrument.

2.1. Deposit

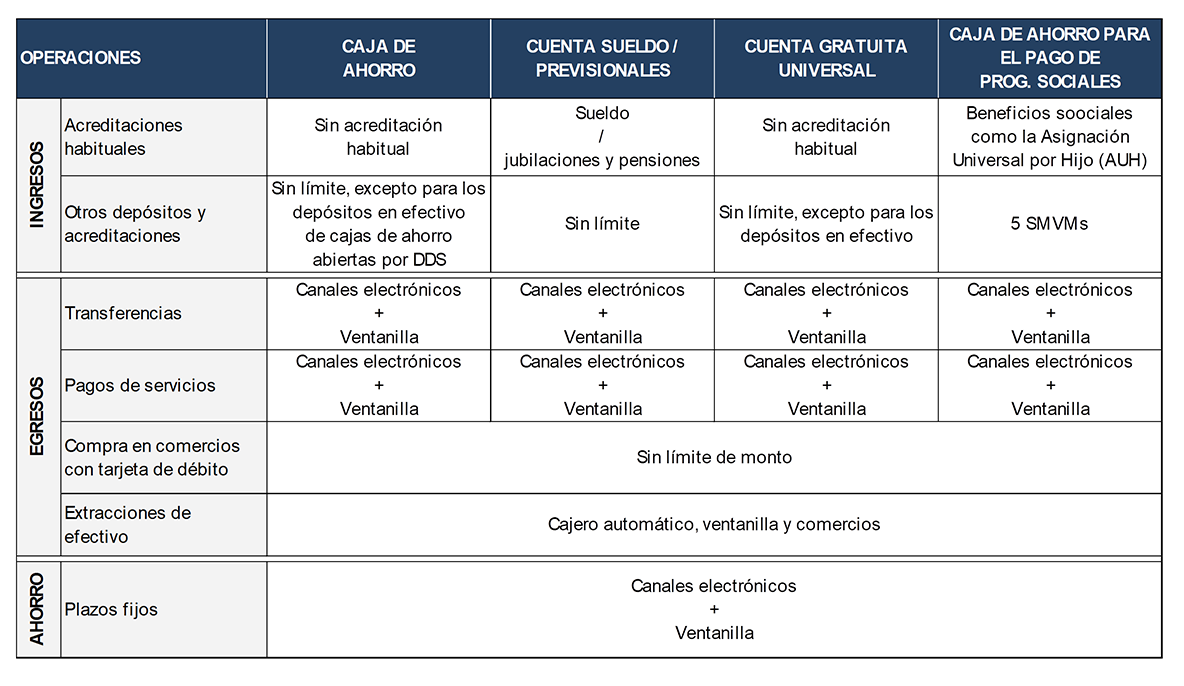

accounts In order to promote access to financial services by the population, the BCRA makes different types of bank accounts available. A bank account is a contract between the customer and the bank where the holder deposits an amount of money and the bank undertakes to safeguard it, in order to be able to use the money deposited for different purposes and at any time. In general, bank accounts are set up as checking accounts or deposit accounts, such as savings banks or salary accounts.

Current accounts are characterized by the possibility of withdrawing funds when you do not have enough balance. To do this, the holder must agree with the financial institution on a line of credit called an overdraft. On the other hand, deposit accounts in pesos have no opening or maintenance cost and the holder is granted a debit card free of charge. These accounts do not allow you to use more money than the one deposited and do not involve the provision of credit cards, although this product can be contracted additionally. All operations carried out with these accounts both remotely – through home banking, mobile banking or another channel – and those carried out at the branches of the financial institution that opened the account, whether by ATM, self-service terminal (TAS) or counter, have no cost for the account holder.

Deposit accounts in pesos are intended only for individuals and are made up of savings banks, salary accounts, social security accounts (hereinafter, pension accounts) and the recently relaunched Universal Free Account (CGU). There are also other types of deposit accounts, used for specific purposes, such as savings banks for the payment of social assistance plans or programs, among others.

Figure 2.1 | Basic Deposit Account Operations

Note | “DDS” stands for Simplified Due Diligence. For more details about the accounts, inquire about the following explanatory contents: CGU, salary account, pension accounts.

Source | BCRA.

The CGU21 was relaunched in order to advance in the full banking penetration of the population, especially the most vulnerable sectors. This account is available to all those who do not have another bank account in the financial system and its opening only requires the presentation of the DNI. This account admits all types of accreditations, including those originated in the sale of goods and services through the “Food Card” within the framework of the “Argentina Plan against Hunger”.

Deposit accounts share the largest number of basic transactions, with some differences in the minimum documentation required for opening, monthly balance limits and in the fee scheme for transactions carried out at ATMs and self-service terminals. Both in the CGU and in savings banks, when they are opened through the Simplified Due Diligence process, the balance of the account must be less than 25 Minimum Living and Mobile Wages (SMVM) and monthly cash transactions must not exceed 4 SMVM. In the same vein, savings banks for the payment of social programs have a monthly limit of 5 SMVM for accreditations other than social benefits.

On the other hand, operations carried out at ATMs and TAS through ATMs and TAS through salary, social security and social program payment accounts have no cost for the account holder, regardless of which financial institution the device belongs to or its location (inside or outside a bank branch). In the case of the CGU, up to eight operations are contemplated at no cost at ATMs of other financial institutions, but those carried out on devices of the financial institution itself located outside the branches -for example, in a supermarket-, may have a cost. On the other hand, in savings banks, transactions arranged on devices of other financial institutions and of the entity itself located outside the branches may have a cost for the account holder.

To measure the penetration of the different types of deposit accounts in the population, the percentage of adults who have at least one deposit account is analyzed. The opening of accounts for beneficiaries of social assistance programs and retirements or pensions has a favorable impact on this indicator, as well as the opening of salary accounts. To determine the impact of each account on the global indicator, the number of beneficiaries for each of the types of accounts was estimated based on the available information22. It should be clarified that for this exercise it was assumed that there is no overlap in account holding between these three categories and that people belonging to these groups do not have any bank account other than those mentioned.

The number of people with savings banks for the payment of social programs was estimated based on the sole holders of the Universal Child Allowance (AUH) social program. The AUH is one of the most important social assistance programs in the country, with more than 2 million unique holders23. Although it is the type of account with the lowest participation in the global indicator, its impact on it is significant, increasing its overall value. By not taking this group of accounts into account in the calculation, the percentage of adults with at least one account is reduced to 73.8%.

A little more than half of this value is explained by the set of salary and pension accounts, while the remaining part is related to holders of different types of savings banks, such as self-employed workers and beneficiaries of social programs other than the AUH – for example, unemployment insurance.

Figure 2.2 | Percentage of the adult population with at least one bank account in pesos

Discriminated by account type

Discriminated against by gender (March 2018)

Note | TOTAL column: percentage of the total adult population and of each gender corresponds to unique CUITs with at least one bank account.

Source | BCRA, COELSA, ANSES and INDEC.

Thus, the indicator of holding at least one net deposit account for pension accounts and for the payment of social programs shows a final figure of 54% as of January 2017, approaching the value obtained by the Global Findex survey24, with only 48% of the sample answering affirmatively about the holding of bank accounts by the adult population. In the previous IIF, it was mentioned that this could reflect the ignorance of many people regarding the possession of accounts in the financial system, given that another survey found that 39% of the population responded that same year that they did not own any financial product. The 54% obtained here, as an approximation, could indicate that this lack of knowledge about account ownership could come to a greater extent from the segments that receive retirements and/or pensions and the payment of social programs; although this is not corroborated from the available data.

If the gender breakdown of account holders is carried out as of March 2018, it is observed that there is no gap at the global level, a fact probably explained in large part by the participation of women in the AUH (97% is headed by women)25. If we subtract savings banks for the payment of social programs from the calculation, the gender gap in the possession of deposit accounts amounts to 11.5 p.p. to the detriment of women.

In turn, the number of pension accounts amounted to 3.6 million for women and 2.1 million for men26. Thus, if we also subtract the pension accounts, the result would indicate that 8.2 million women had an account (47.4% of the adult female population) compared to 10.8 million men (66.7% of the adult male population), resulting in a gap of 19.4 p.p.

At the same time, the holding of salary accounts shows a gap of 9 p.p. to the detriment of women, in line with their lower participation in the formal labor market. As noted in the section on credit to individuals, women have a lower rate of activity in the labor market (49% vs. 70% of men) and a lower employment rate of 44% vs. 64% of men27.

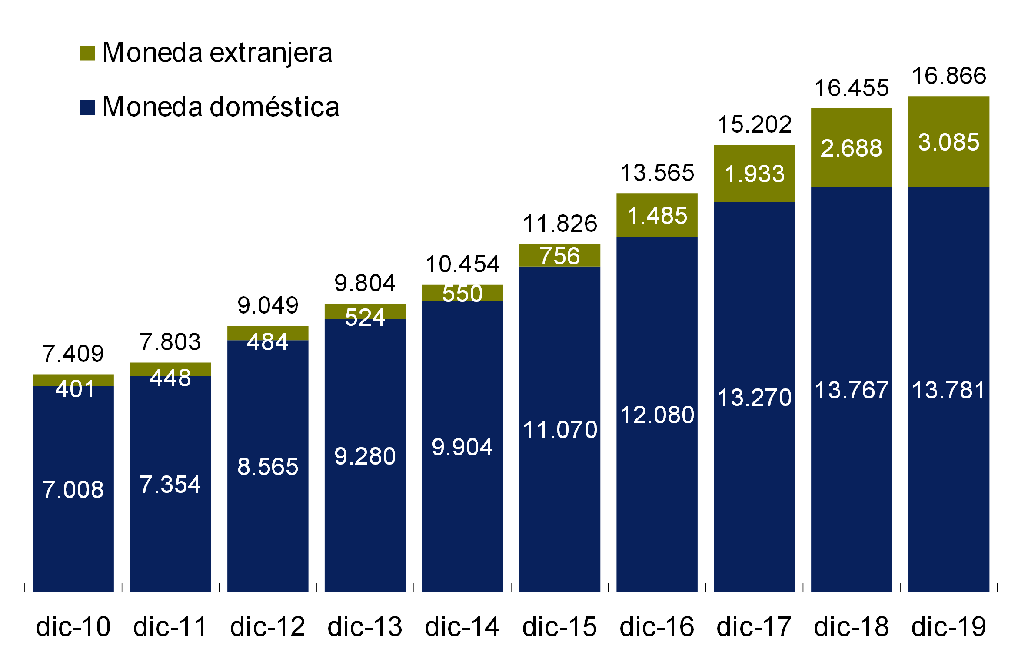

A complementary indicator, used as a proxy variable in countries that do not have individualized data on deposit account holding, is the number of deposit accounts per 10,000 adults. As of December 2019, 16,866 deposit accounts were registered per 10,000 adults, which is equivalent to 1.6 deposit accounts per adult, registering an average year-on-year growth of 9.6% over the last decade. If we consider deposit accounts in local currency, which represent 82% of the total, there are approximately 1.4 deposit accounts per adult.

Figure 2.3 | Deposit accounts per 10,000 adults

Source | BCRA and INDEC.

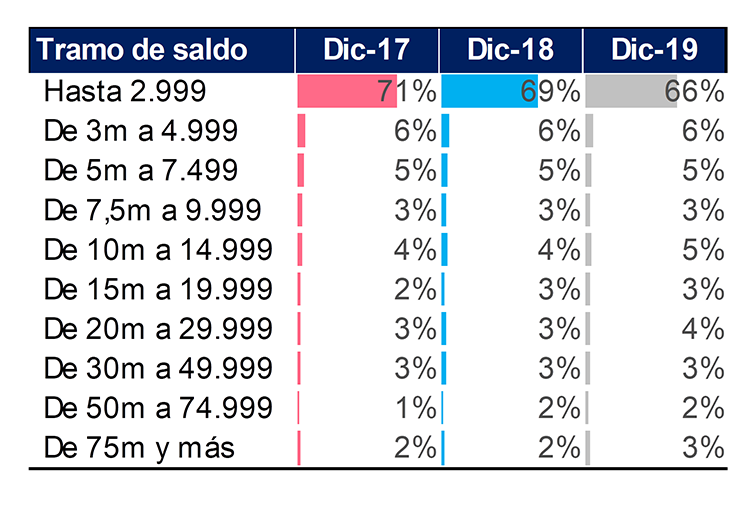

The information provided by financial institutions allows for grouping deposit accounts in local currency according to their balance level (monthly average)28. Based on this information, the distribution of the number of accounts according to different levels of balances is obtained, as well as the average balance in each of these groups.

The first range of information groups accounts with an average monthly balance of up to $2,999. This range brought together more than 30 million deposit accounts (out of a total of 46.8 million) for a total amount of almost $15 billion as of December 2019. This is equivalent to saying that 66% of deposit accounts in pesos were concentrated in the lower range, which, on average, registered a balance of $480. A similar distribution was verified for the months of December 2017 and 2018, with a slightly higher proportion in the first range, probably due to the effect of the nominal values of the balance brackets.

Leaving balances deposited in a deposit account could be considered passive savings. Only 1 in 3 people reported leaving balances in deposit accounts or checking accounts as a form of savings29, which would be in line with the information analyzed here.

Figure 2.4 | Relative Share of Deposit Accounts by Balance Tranche

Note | m = thousand. Local currency deposit accounts are considered, and the balance of each account corresponds to the average monthly balance.

Source | BCRA.

Deposit accounts that are assigned the receipt of some kind of income – salaries, retirements and pensions and social assistance – accounted for 64% of the total deposit accounts in local currency as of December 2019, with pension accounts registering the highest participation (28%). This behavior has remained constant over the last 6 years. The fact that the rest of the savings banks have a 35% share of the total could be indicating that a large part of the population has a savings account in addition to the one they receive their income. This would be related to the aforementioned metric that in Argentina there are 1.4 deposit accounts in pesos per adult.

2.2. Transactions by electronic means of payment and cash

withdrawals In line with the objectives set by the BCRA, electronic means of payment facilitate transactions for the population and, at the same time, contribute to reducing the use of cash. They make it possible to overcome geographical barriers, making it easier to send and receive money, simplify transactions of goods and services and contribute to a better management of available resources.

In this framework, the operations carried out by individuals through credit, debit, prepaid and electronic transfersare analyzed 30. In particular, debit, credit and prepaid card purchases, transfers of funds originating in bank accounts through electronic channels and cash withdrawals at ATMs made using cards or other alternative systems are considered in the analysis. Both the number of operations and the amounts involved are measured in relation to the adult population.

In each of the metrics of electronic means of payment, there were increases relative to the population, both in the number of operations and in the amount operated31 in real terms, despite the fact that economic activity has stagnated or contracted during the last five years. The existence of a regulatory framework aimed at the expansion of these means of payment may partially explain their continued growth. The obligation for merchants to accept payments with debit cards and the progressive reduction of interchange fees for debit and credit card transactions32, added to regulatory innovations such as payments through quick response codes (QR codes33) – including payment through different types of cards by this means – are factors that, from the sellers’ side, they help explain the growth of electronic means of payment.

On the other hand, the extension of the electronic transfer system through different modalities, types of accounts (bank and provided by Payment Service Providers -PSP), as well as the simplification adopted to identify the recipient (Alias-CBU34), among others, have contributed to a greater offer and greater adhesion by the population.

2.2.i. Debit, credit and prepaid card payments. Electronic payments, which facilitate transactions and help reduce the use of cash, can be executed from different technological environments such as cards, computers and cell phones. In 2019, electronic card payments grew 12% in average number of transactions per adult and thus consolidate several years of growth.

In Argentina, the debit card was the most used electronic means by the population to make payments during 2019, slightly surpassing the credit card by 7%. In previous years, the latter had been the instrument most chosen by the population to make payments, considering that it has the possibility of providing financing.

Both means of payment have maintained their growth path in 2019, although in the case of debit cards there was evidence of an acceleration. Taking into account the moving average of the number of monthly transactions per adult, it can be seen that in recent months debit card payments raised their usual growth range from 8% to 12% per year. From lower levels, the use of the prepaid card grew steadily and, like the debit card, experienced an acceleration in recent months. As mentioned in the previous IIF, prepaid cards, powered by PSPs, support the same operations as debit cards. In addition, these cards are linked to a payment account that, through the Uniform Virtual Key (CVU) launched by the BCRA, allows the interoperability of PSPs and bank accounts to be streamlined.

In order to strengthen the protection of financial services users, new regulations for PSPs were established in 2020. The funds of customers credited to payment accounts must be in demand accounts, in pesos, in financial institutions in the country and, at all times, immediately available upon request35. It was also established that it was mandatory for PSPs to register in the “Register of Payment Service Providers Offering Payment Accounts” and to report the corresponding information36 to the BCRA.

Figure 2.5 | Electronic Payment Per Adult Transactions

Amounts

Amounts

Note | Quantity and average monthly amount of the period (Base Price Index January 2019).

Source | BCRA and INDEC.

As for the amounts traded relative to the adult population, all electronic means of payment verified – in real terms – positive variations throughout the period, except for credit cards, which registered a slight drop. The latter could be explained by the adverse macroeconomic conditions in which the economy operated, in particular, the persistence of high interest rates in a context of contraction in economic activity. As observed in relation to the amounts, the amount of prepaid cards registered the highest relative increase from the lowest levels (monthly average per adult $21, $31 and $60 for 2017, 2018 and 2019, respectively).

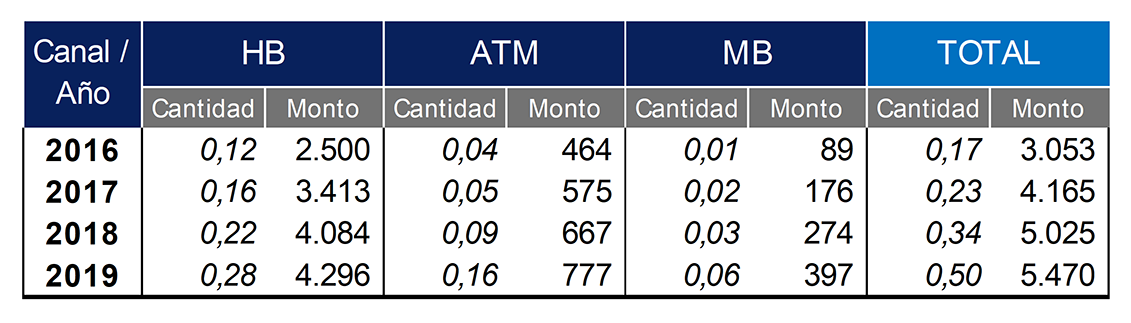

2.2.ii. Transfers of funds originating from bank accounts through electronic channels. Electronic transfers have been consolidating their growth in recent years, growing the number of operations at rates close to 47% in the last two years and almost doubling the average monthly amount operated from 2016 to 2019. In addition, this amount exceeded the amount operated with credit cards by 40% and by 2.5 times the amount of debit cards in 2019. In recent years, various regulations have been issued to improve the user experience, a pseudonym (Alias-CBU) was created to facilitate the identification of accounts and limits were temporarily increased at the request of customers37, among others.

Both in terms of amounts and amounts transferred, the channel most used by adults in recent years has been HB, followed by ATM and in third place by MB. HB transfers, with significant growth in the period, doubled the amounts made by ATM and exceeded those of MB by 5 times in 2019.

As for the amounts, they were 6 and 11 times higher than those channeled by ATM and MB, respectively. From relatively lower values, MB led the growth of these channels during this period, both in quantities (increase of 500%) and volumes (increase of more than 300%). This would be in line with a trend in favor of the adoption of cell phones for carrying out financial operations, since they offer a practical and agile alternative to operate through an account.

Notes | Quantity and average monthly amount of the period (Base Price Index January 2019). Only operations of human persons are contemplated.

Source | BCRA and INDEC.

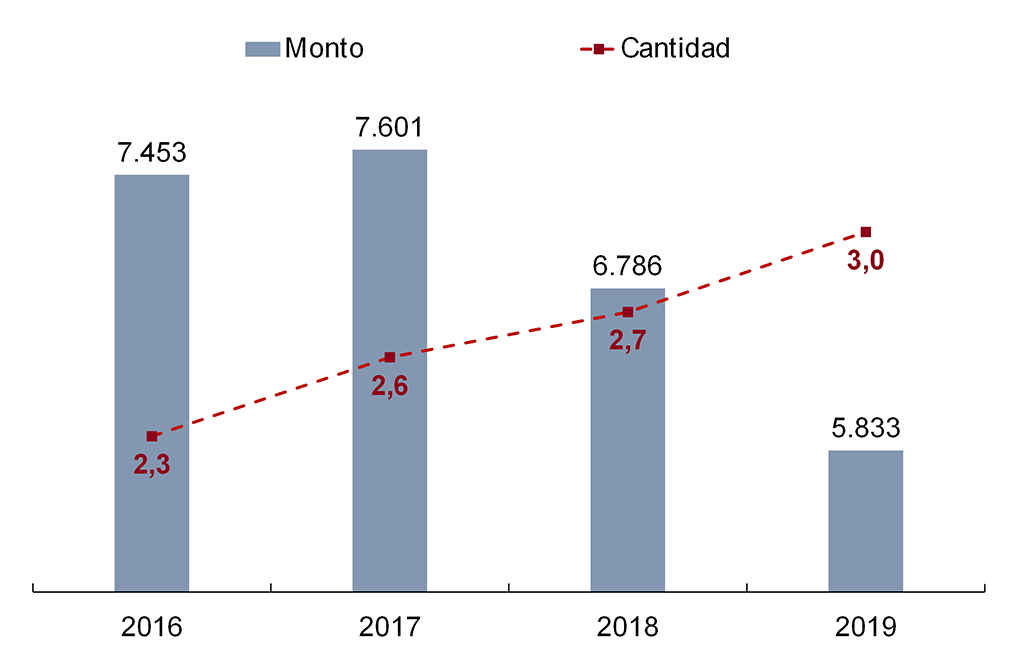

2.2.iii. ATM cash withdrawals per adult. From 2016 to 2019, ATM cash withdrawals increased by 29%, while average amounts withdrawn decreased by 22% in constant values. This could be due to the evolution of the financial infrastructure and the aforementioned increase in the use of electronic means of payment. The greater the availability of physical points, both PDAs and alternative cash withdrawal points, the possibility of carrying out these operations at any time is facilitated, without the need to withdraw large sums of money at each opportunity.

On the other hand, by encouraging the greater use of electronic means of payment, the adoption of these instruments is quickly incorporated into the new payment habits of the population. In this way, it is verified that in 2019, for every 100 withdrawals per adult, almost twice as many transactions were carried out by electronic means of payment (191), which are broken down into 89 with debit card, 82 with credit card, 17 transfers and 3 with prepaid cards.

Figure 2.7 ATM cash withdrawals per adult Amount Quantity

Note | Amount and average monthly amount for the period (base January 2019)

Source | BCRA and INDEC.

2.3. Savings modalities

The modalities of passive and active savings are channeled by the population through different instruments of the financial system. In the case of active savings, which involves the choice of a specific savings product, fixed terms are one of the main tools for channelling household savings and obtaining remuneration.

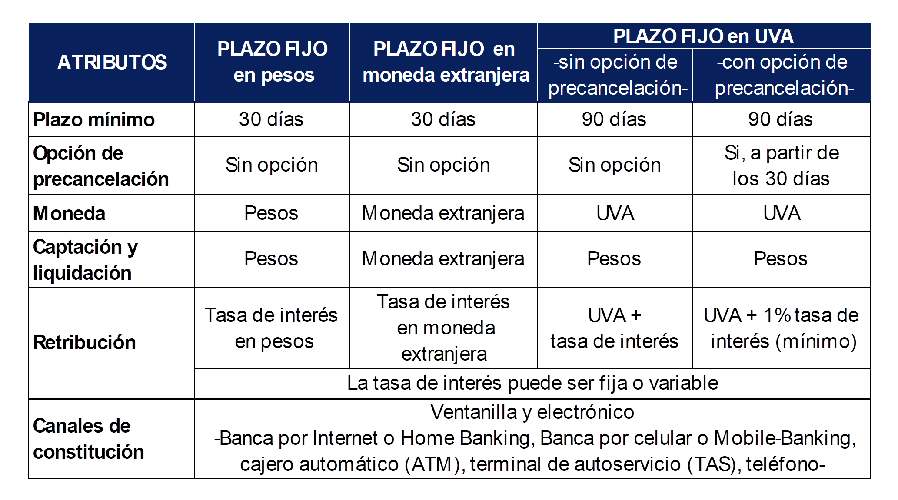

Fixed terms are placements in which the depositor delivers a sum of money to the financial institution for a certain period, in exchange for a future remuneration agreed between the parties. They can be made in pesos, UVA (Purchasing Value Units) or foreign currency (mainly dollars or euros), have a fixed or variable remuneration and be carried out in person or remotely (electronic channels). Its minimum term is 30 calendar days and some of them can be canceled before its expiration date (pre-cancellation option). They also have the possibility of being constituted without having a bank account, although they are usually made through them.

Fixed terms in pesos and in foreign currency have similar characteristics except for the currency of collection and settlement. On the other hand, fixed terms in UVA have the UVA as the unit of account, which is updated by the Reference Stabilization Coefficient (CER), which follows the evolution of the Consumer Price Index. This instrument constitutes an alternative for savings in pesos that is adjustable to the evolution of prices, maintaining the purchasing power of the capital saved.

Figure 2.8 | Main characteristics of fixed terms

Source | BCRA.

Fixed Terms in UVA require a minimum term of 90 calendar days, but offer an alternative that includes the possibility of early cancellation from 30 days of its constitution38. The interest rate of the early exit will be fixed at the time of contracting the fixed term for those who opt for the term of 90 days, plus 1% nominal per annum, guaranteeing a positive real interest rate.

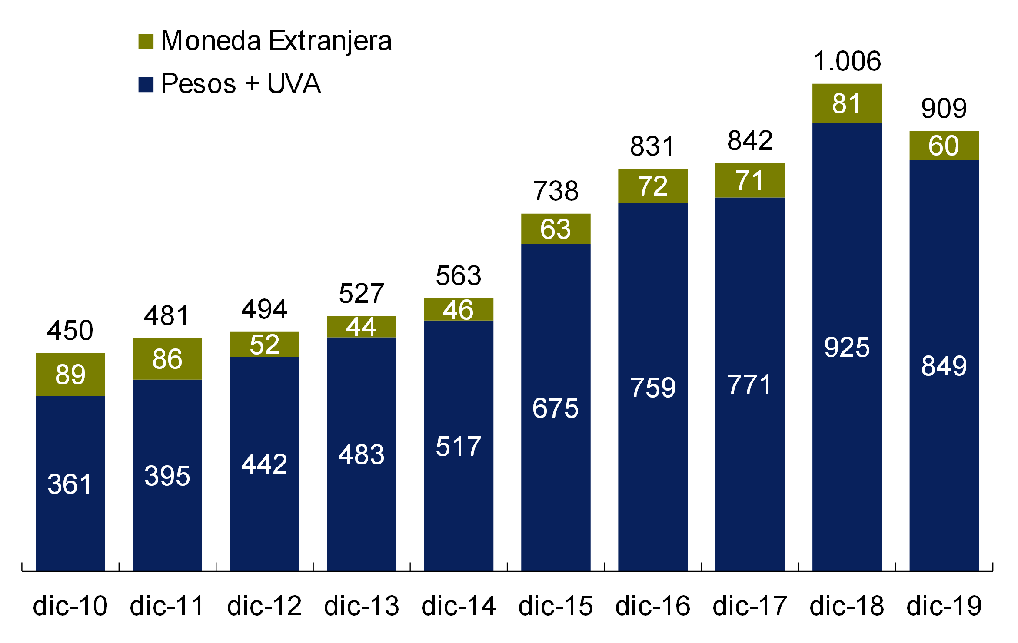

One of the basic indicators for measuring the use of this savings instrument is the number of fixed terms made by individuals39 in relation to the country’s adult population. As of December 2019, the number of fixed-term loans per 10,000 adults was 909, falling 10% compared to a year ago. A stylized reading of this value indicates that, on average, 1 in 10 adults had a fixed term as of December 2019. Between December 2010 and 2019, the number of fixed-term loans in pesos per 10,000 adults more than doubled, registering an average year-on-year increase of 10%.

During the period analyzed, the share of fixed-term deposits in local currency registered a slight but sustained increase, standing at 93% as of December 2019. Various regulatory changes have made it easier to set up fixed terms in domestic currency – through electronic channels without the need to be a customer of the financial institution – and respond to the specific needs of users – to maintain purchasing power. Also, the conditions that governed the foreign exchange market may have influenced the selection of the population’s savings products.

Figure 2.9 | Number of fixed terms per 10,000 adults

Source | BCRA and INDEC.

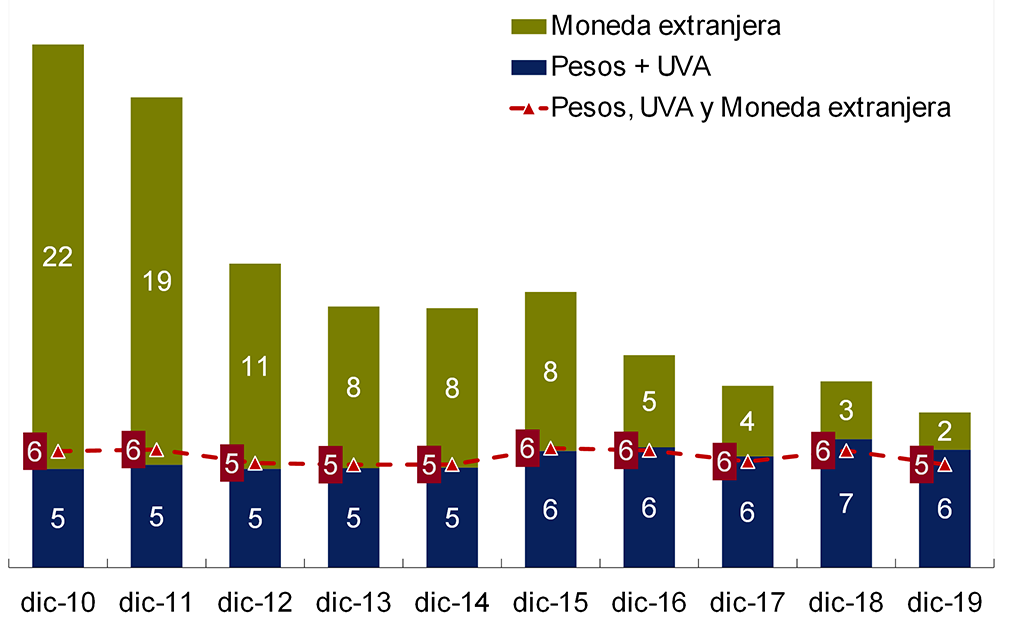

Another indicator that allows us to measure the intensity of use of fixed terms is the relationship between the number of fixed terms and the number of deposit accounts. Over the last decade, the number of fixed terms per 100 deposit accounts in foreign currency has been substantially reduced as a result of the massive opening of deposit accounts in that currency. In contrast, the metric in local currency maintained an average value of 6 fixed terms per 100 deposit accounts.

Figure 2.10 | Number of fixed terms per 100 deposit accounts

Source | BCRA.

The performance of this indicator indicates that only a small proportion of deposit account holders would use this savings instrument, which is in line with the low number of fixed-term deposits in relation to the adult population and with the results of the survey mentioned at the beginning of the section. The average balance per adult in real terms grew by only 4% between December 2010 and December 2019. Taking into account the SMVM as of December 2019, the average balance per adult on that date represented 1.6 times the SMVM. The geographical distribution of the real balance of fixed terms per adult was not homogeneous between the different provinces. It is observed as a trend that the Central and Patagonia regions presented the highest values of fixed terms per adult, while the NOA and NEA regions exhibited the lowest values.

As of December 2019, CABA led the ranking, surpassing Tierra del Fuego, which was in second place, by 1.7 times, and Misiones, located in last place, by 8 times. However, CABA presented a significant drop in real terms in the balance of fixed terms (13%) compared to December 2010. On the other hand, it is highlighted that Formosa and Catamarca were the provinces with the highest growth between December 2010 and December 2019, with 89% and 67% respectively. This implies a reduction in the differences in fixed-term balances per adult at the provincial level.

Figure 2.11 | Real balance of the fixed terms of human pesos. Provincial distribution by adult.

Note | It contemplates fixed terms in pesos, UVA and foreign currency. Price index (base January 2019).

Source | BCRA and INDEC.

One of the elements to encourage the use of savings products such as fixed-term savings is to facilitate their constitution as much as possible. Electronic channels such as HB and MB have many advantages in relation to the face-to-face modality. Based on the information on the balances of the fixed terms constituted by the non-financial private sector, it can be stated that the electronic channel has been the most chosen by individuals and companies over the last 10 years, ranging between 92% and 97% of the total balance.

Box / Regional comparison of the regulatory framework for basic accounts

Basic accounts seek to promote financial inclusion while protecting the integrity of the financial system40. Especially for people in vulnerable situations, it is important to have a policy for admitting new customers to the financial system that is not too restrictive and thus avoid financial exclusion41. Likewise, without access to the formal financial system, these people turn to cash and unregulated channels, which limits transparency and increases the risk of crime and money laundering, undermining financial integrity42.

Basic or simplified accounts refer to accounts that, based on specific regulatory provisions, require the request for reduced information and documentation requirements (know-your-customer policy). A large part of the vulnerable population is not in a position to present the documentation that is normally required to open standard bank accounts, such as proof of address and/or sources of income.

Generally, the regulations for basic accounts contemplate their opening through non-traditional channels, such as banking correspondents, or remote ones, through electronic means such as computers and cell phones, in order to facilitate the incorporation into the financial system of historically excluded people. These channels contribute to reducing transaction costs associated with the provision of formal financial services in remote populations, especially in rural areas, and in those localities where the provision of services through traditional infrastructures, such as branches and ATMs, is not sustainable.

In line with the lower requirements and simpler opening processes, transactional and balance limits are usually established for this type of account, in order to reduce their potential use for the management of resources of illicit origin and/or financing of terrorism.

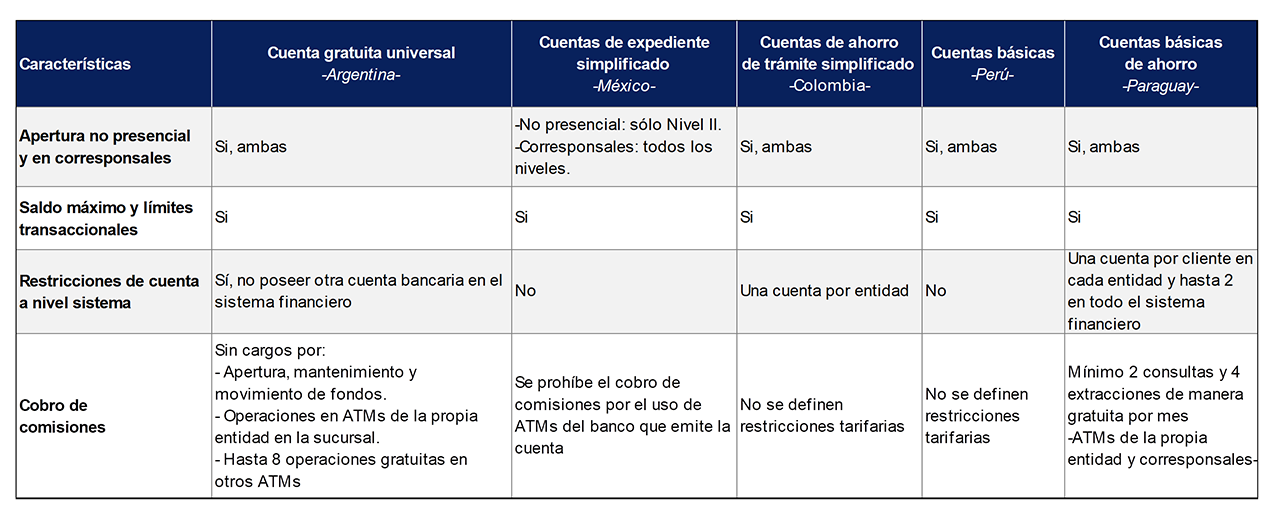

Several countries in the region have regulatory frameworks that define simplified openness fundraising products, focused on improving financial inclusion conditions for the underserved population. This is the case in countries such as Mexico, Colombia, Peru and Paraguay, where this type of account has a specific name that allows them to be identified and differentiated from the rest of the deposit accounts, having been implemented in 2012, 2009, 2011 and 2013, respectively.

Except for Mexico, the rest of the countries mentioned only contemplate the opening of these accounts for individuals. Another common factor is the possibility of opening through correspondents and by electronic means and the imposition of transactional limits. In contrast, regulatory frameworks differ in the policy of charging fees and in terms of restrictions on account holding at the system level.

Figure R1 | Regional comparison of the regulatory framework for basic accounts43

In the case of Argentina, in January 2020 the Universal Free Account (CGU), which had been discontinued in 2016, was restored. This bank account is aimed at unbanked people and is opened with the sole presentation of the DNI, having no opening and maintenance cost. All banks are obliged to offer and open it at the request of individuals. Starting in June of this year, banks will have to offer the remote opening of GUCs, reducing geographical barriers to access to financial services.

In this regard, it should be noted that although the proportion of the population living in localities without bank branches is relatively low (11.6%), in most cases these access points are located in urban centers, which implies that a large part of the population must travel considerable distances to access them. Likewise, the number of branches per locality is very scarce to serve the population that lives in them, considering that 34% of the localities have less than one branch for every 10,000 adults.

Basic accounts are a key instrument in terms of financial inclusion, since they are the vehicle for vulnerable segments of the population to access the benefits of participating in the financial system. In this sense, it is highlighted that the possession of a bank account allows people to carry out cashless transactions, such as purchases in stores and payments for services electronically, send money -transfers- and channel savings, among others.

3. Credit

3.1. Credit to individuals

The analysis of access to credit is one of the key axes of the diagnosis of financial inclusion in a country, since it makes it possible to determine the degree of use by individuals and companies of the financing provided by the financial system. In Argentina, there are different institutions that grant credit to individuals and companies.

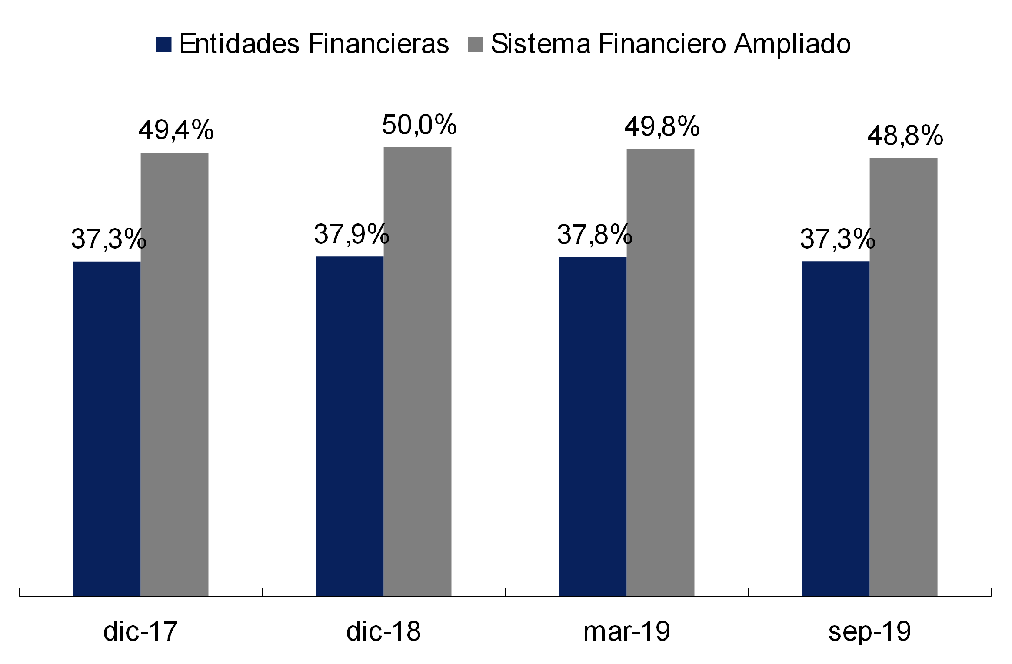

The main difference between those who provide credit lies in the origin of the funds used for it. Institutions that take funds from the public and then lend them to third parties, which is known as financial intermediation, are called financial institutions and are regulated by the BCRA in accordance with the provisions of the Financial Institutions Law. As of September 2019, 37% of Argentine adults had at least one financing granted by these entities.

On the other hand, those that lend with funds or own capital are not under this regulatory framework. Within this group, there are non-financial companies that issue credit and/or purchase cards (ETCNB) and other non-financial credit providers (OPNFC)44. As of September 2019, the ETCNBs provided financing to 16% of adults in our country, while the OPNFCs reached 9%. These two groups of institutions make up the group of Non-Financial Credit Providers (NFCPs), while the Extended Financial System (SFA) is defined as the group that includes financial institutions and NFPs.

In this context, all financial institutions and PNFCs registered in the respective registries report to the BCRA on the financing they grant to their customers. This credit information system is called the Central Bank of Debtors of the Financial System (CENDEU), whose data are available for individual consultation with CUIT, CUIL or CDI for the general public on the BCRA website.

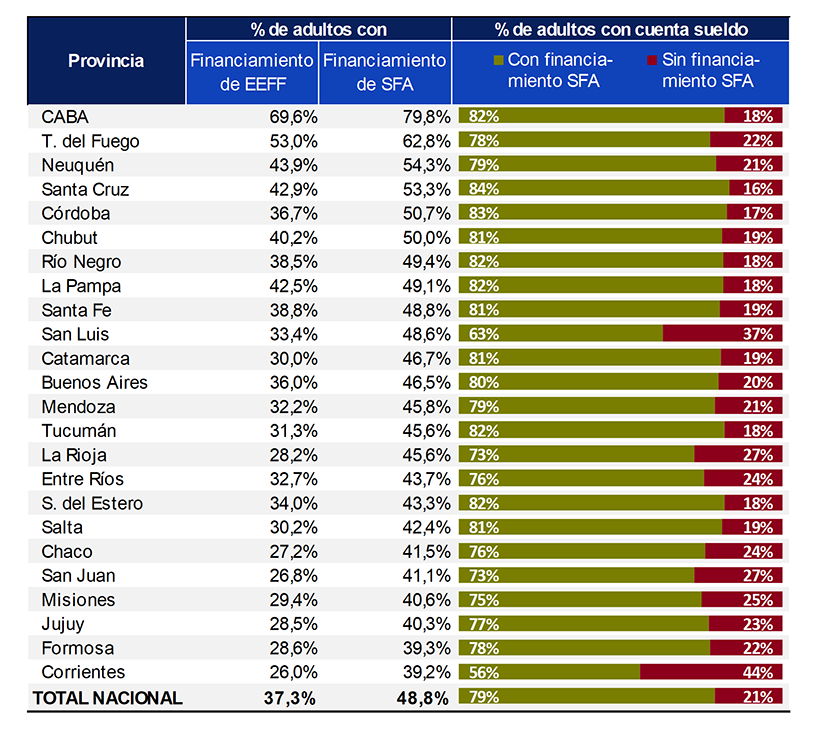

3.1.i. Adults with at least one financing per set of providers and per province. According to data reported to CENDEU, as of September 2019, 37% of adults in our country had at least one financing granted by financial institutions. On the other hand, this indicator amounted to 49% in the SFA.

The temporal evolution of the indicator, both for financial institutions and for the SFA, shows a relatively stable performance, registering a small increase in 2018 and, with the information available, a contraction during 2019. The percentages observed remained almost unchanged in recent years, showing certain limits in the inclusion of new people in credit products.

Figure 3.1| Percentage of adults with ale minus one financing.

Source | BCRA and INDEC.

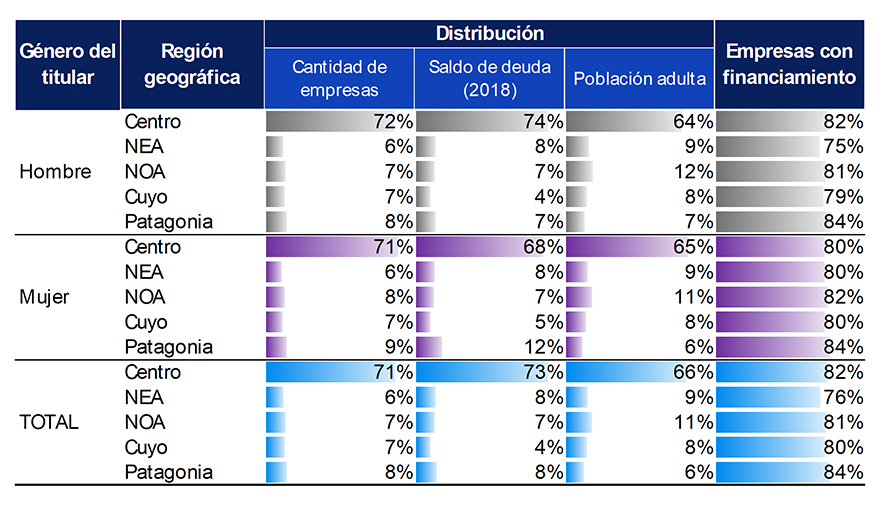

The distribution by province45, both for the financing of financial institutions and for that of the SFA, shows that CABA was the province with the highest proportion of debtors over its adult population, while Corrientes was at the opposite extreme. In all provinces, there is a considerable contribution of the PNFC to the percentage of debtors, with La Rioja being the province with the highest participation of this group (17.3% of the adult population), followed by Catamarca (16.7%), while La Pampa registered the lowest magnitude (6.6%).

In regional terms, as with the indicators of PDA and credit of individuals with business activity, a better performance is recorded for the Central and Patagonia regions, with a 51% and 52% percentage of debtors in the SFA, respectively, while the NEA, the NOA and Cuyo verified a lower proportion of adults with financing (40%, 44% and 45% respectively).

For the purpose of analyzing explanatory factors of access to financing, the relationship between participation in the formal labor market and access to financing is considered, taking as an indicator the possession of a salary account46. Nationally, 25% of adults had such an account as of September 2019. Within this group, 79% of people had at least one financing granted by the SFA.

There is a considerable improvement in the indicator of access to financing for people with a salary account, taking into account that there is a difference of 30 percentage points (p.p.) between the total percentage of adults who access financing and the percentage of adults with a salary account who access it. Again, there are great disparities at the provincial level, with Corrientes being the province with the least access to financing for its population with a salary account (56%) and Santa Cruz the one with the greatest access (84%).

Figure 3.2 | Debtors by province and accreditation of remuneration in bank account

Note | EEFF: Financial Institutions. Data as of September 2019.

Source | BCRA and INDEC.

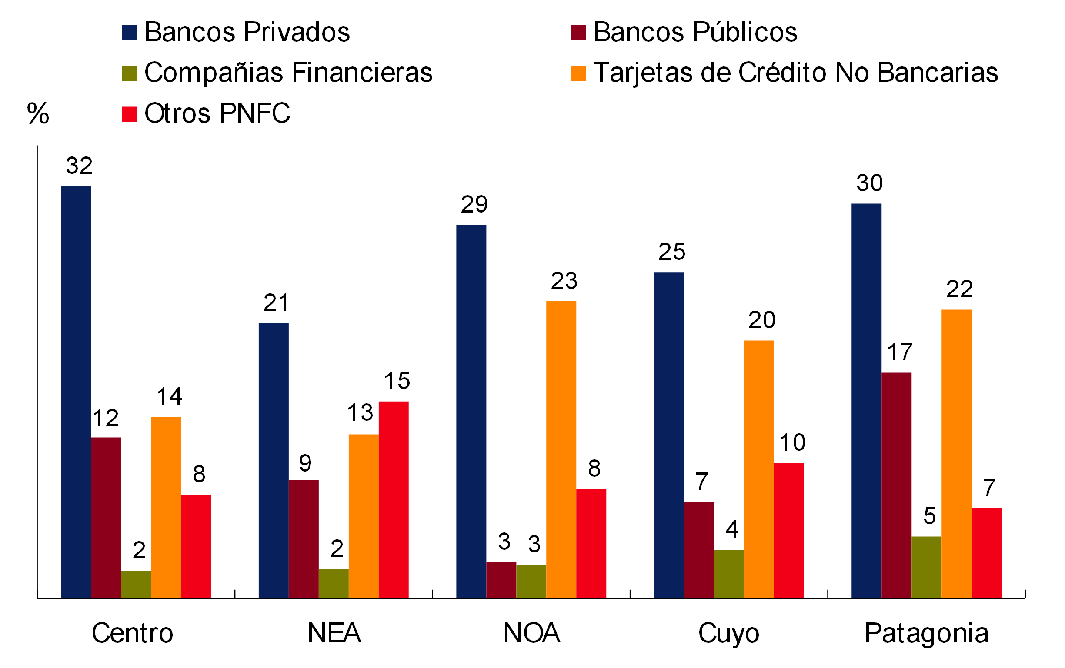

3.1.ii. Adults with at least one funding per provider type, funding type, and age group. Financial institutions can be classified into different main institutional groups: private banks (50 entities), public banks (13) and financial companies (15). On the other hand, if we consider the PNFCs that report to CENDEU, we find the ETCNB and the OPNFC47. Based on this classification, 30% of the adult population had at least one financing with a private bank as of September 2019. Public banks, on the other hand, accounted for 11% of adults, while ETCNBs and OPNFCs accounted for 16% and 9%, respectively48.

Both at the national level and in each of the regions, private banks are the institutional group that financed a higher percentage of the population, followed by the ETCNBs – with the exception of the NEA region where the OPNFCs take on greater relevance than the latter.

Although at the national level, public banks demonstrate a greater reach than OPNFCs, this performance is not homogeneous throughout the territory, with marked differences between regions. It is observed that in the Central and Patagonia regions, public banks grant financing to a higher percentage of adults than the OPNFCs, while in Cuyo, the NEA and the NOA this behavior is reversed.

An aggregate comparison of financial institutions on the one hand, and OPNFCs plus ETCNBs on the other, shows that while in the Central region the former had a higher relative share (ranging from a minimum of 32% to a maximum of 42%), the participation of the latter was relatively low (between 14% and 22%). On the other hand, OPNFCs and ETCNBs are more relevant in the NEA, NOA and Cuyo regions, where banks decrease their relative participation. In Patagonia, the percentage of adults with financing is high in relative terms relative to the other regions for all institutional groups, highlighting that it is the region where public banks have the greatest reach.

Figure 3.3 | Percentage of adults at least one funding per institutional group

Note | Data as of September 2019.

Source | BCRA and INDEC.

On the side of the type of financing, as of September 2019, 38% of the adult population had at least one credit card financing (both bank and non-bank). For that period, financial institutions and ETCNBs reported that there were a total of 28 million credit cards in Argentina that registered activity49. Taking into account this amount in relation to the adult population that registered credit card assistance, it appears that each debtor had an average of 2 credit cards.

In second place are personal loans, which were accessed by 25% of the adult population. For both types of financing, a slight reduction in the percentage of adults is observed between December 2018 and September 2019. On the other hand, longer-term loans that require collateral reached a much smaller percentage of the adult population. Only 1.3% of adults had a title loan, while for mortgages the percentage was only 0.7%.

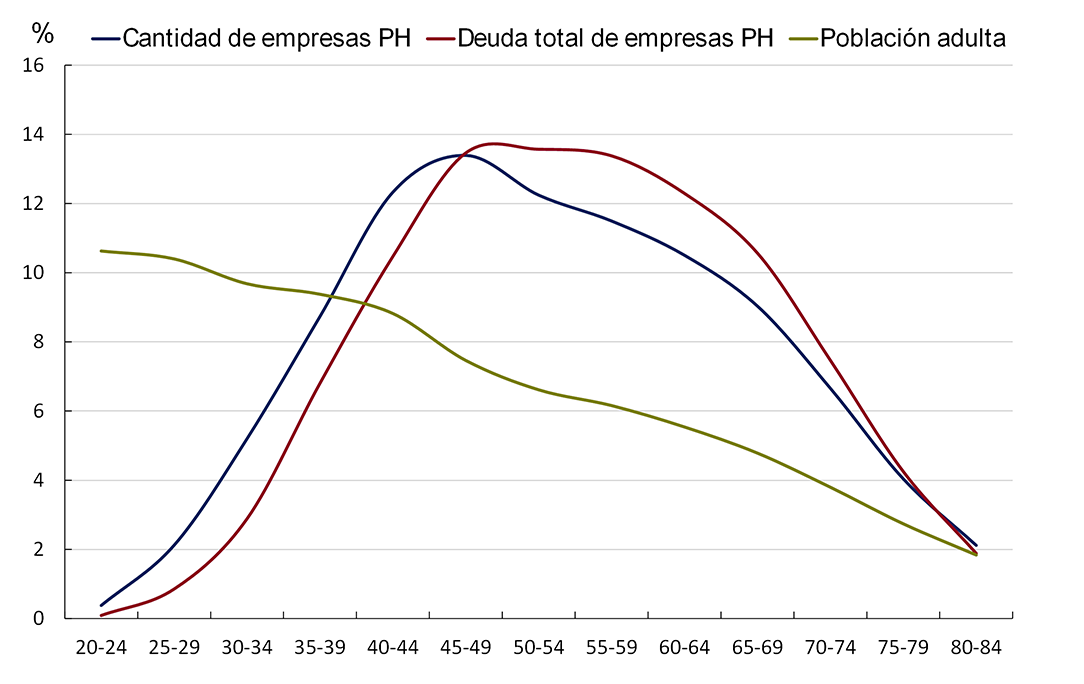

With regard to the age of the debtors, in all age ranges, the most used type of assistance was the credit card. From the age of 65, the percentage of the population that accesses personal loans increases considerably. This phenomenon could be associated with the existence of lines of credit offered by financial institutions to retirees and pensioners who receive retirement benefits or pensions in bank accounts.

Figure 3.4 | Percentage of adults with at least one SFA funding by type of assistance and age group

Note | Data as of September 2019. Source | BCRA and INDEC.

Mortgage loans were more prevalent in the population between 35 and 54 years of age, which could be related to a higher and more stable income level in these age groups, as well as a greater preponderance of the constitution of independent households and the acquisition of their own home. On the other hand, title loans registered a relatively longer scope until the age of 64.

3.1.iii. Financing situation of debtors. Financial institutions and PNFCs classify debtors according to the ability to pay their debt. The regulations provide for the existence of levels of grouping (“situations”) of debtors in decreasing order of quality, with Situation 1 being the one in which the debtors are able to adequately meet all their financial commitments (even though they may be late in payment) and Situations 5 and 6 those in which the debt is considered uncollectible50.

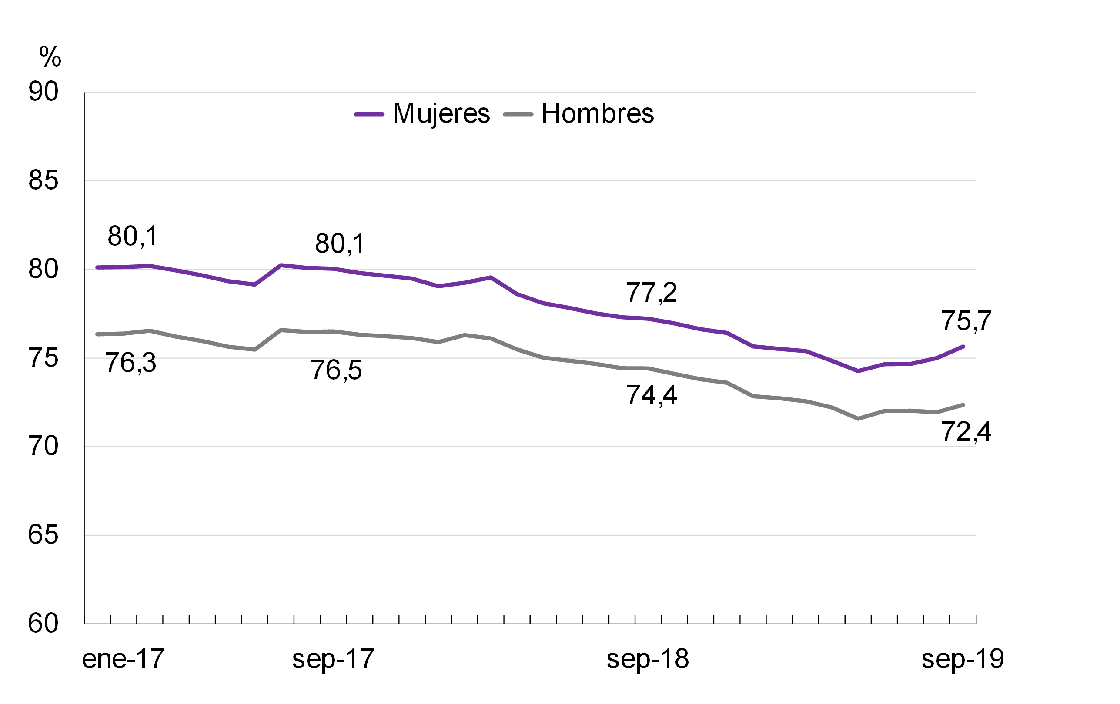

Debtors classified in Situation 1 and 2 are grouped in the regular situation, i.e. they can meet all their financial commitments, and all other debtors are considered under the category of irregular situation. As of September 2019, 74% of SFA debtors were in a regular situation. The temporal evolution of this indicator shows a reduction in the percentage of debtors who adequately meet their obligations, having fallen 4 p.p. and 2 p.p. compared to the same month in 2017 and 2018, respectively.

Figure 3.5 | Percentage of SFA debtors in a regular situation by gender

Note | Debtors whose financing has been assigned to financial trusts are included.

Source | BCRA and INDEC.

The disaggregation of this indicator according to the gender of the debtors denotes a difference in repayment behavior between men and women: while of all women with at least one financing in the SFA, 75.7% adequately fulfilled their obligations, in the case of men, this percentage was reduced to 72.4%. A similar difference is maintained over time, indicating that women as a group tend to have better debt payment behavior than men. The deterioration in the repayment situation shows a different performance between both genders, with a greater drop for women than for men, which were 4.4 p.p. and 4.1 p.p. in the last 24 months, respectively.

In terms of age, the percentage of debtors in a regular situation is lower in young people than in older ones, evidencing a positive relationship between the age of debtors and repayment behavior. As of September 2019, 69% of debtors between 20 and 40 years of age were in a regular situation, while for debtors between 40 and 65 years of age that percentage rose to 74% and for those over 65 years of age to 82%. Likewise, it can be seen that the largest number of debtors who do not adequately comply with the repayment of their financial obligations is between 30 and 45 years old.

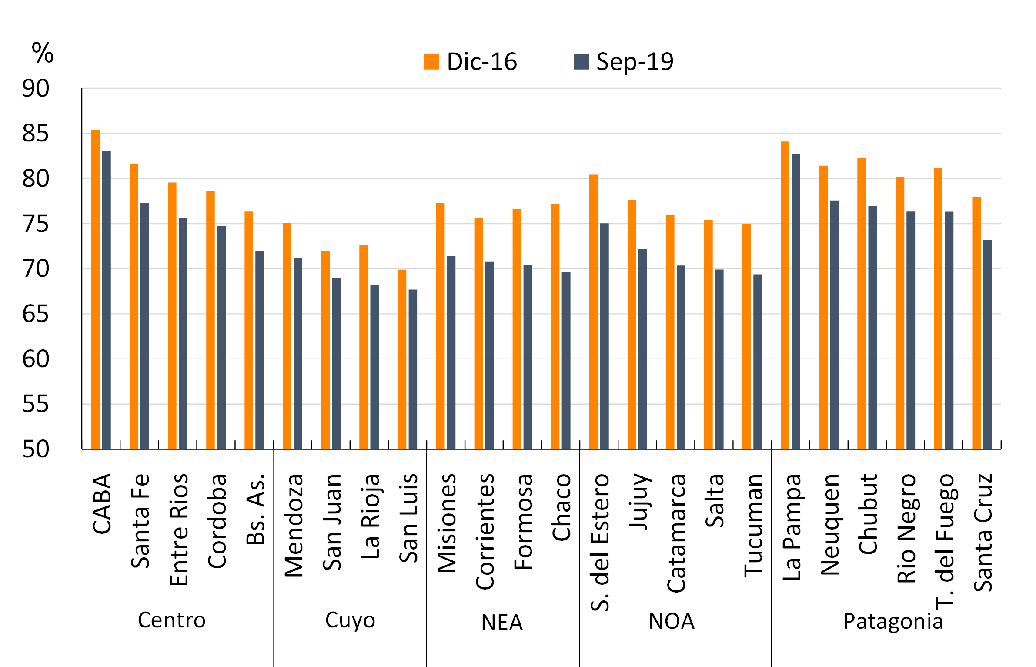

Geographically, the provinces of Patagonia had a higher proportion of debtors in a regular situation than the rest of the provinces, while the provinces of Cuyo had the lowest values. CABA and La Pampa were the jurisdictions in our country with the highest percentage of debtors in a regular situation, while La Rioja and San Luis were the ones with the lowest percentage.

Figure 3.6 | Percentage of SFA debtors in a regular situation by province

Note | Debtors whose financing has been assigned to financial trusts are included.

Source | BCRA and INDEC.

The evolution of the indicator over the last few years shows that all Argentine provinces have suffered a reduction in the proportion of debtors that regularly meet their commitments, this decrease being greater for the provinces that make up the NEA and the NOA. In particular, Chaco and Formosa show steep falls of 7.5 and 6.2 p.p. respectively which, compared to the falls in CABA and La Pampa (2.4 and 1.4 p.p. respectively), show that the deterioration in the indicator has had a very heterogeneous impact throughout the territory.

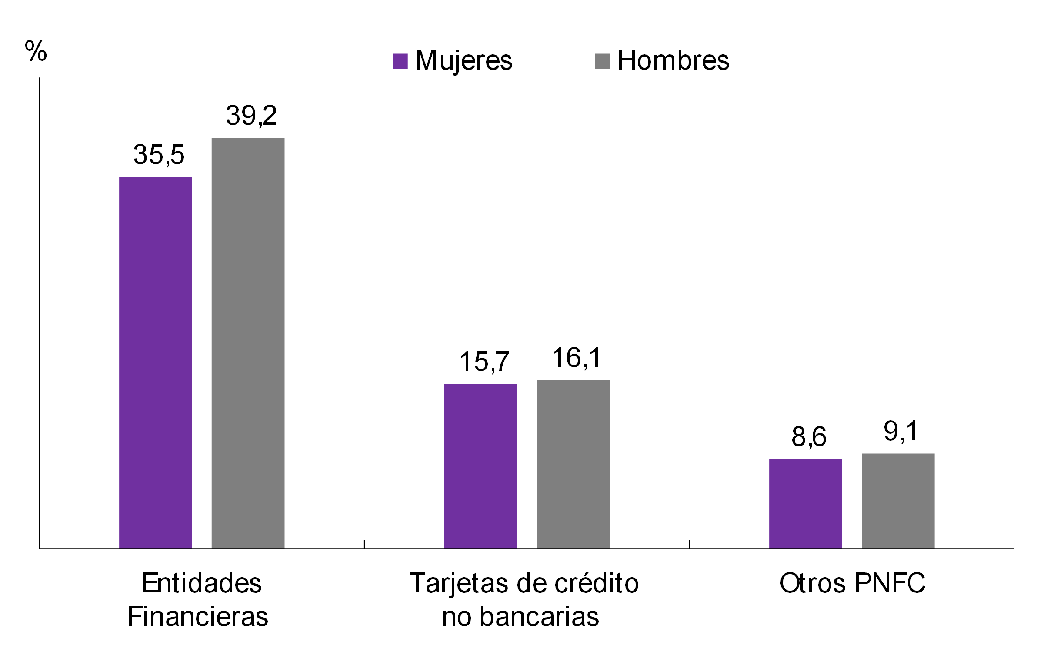

3.1.iv. Gender gaps by institutional group, type of financing and age group. As of September 2019, 46.0% of women and 51.8% of men had at least one financing in the SFA. These two values show the existence of a gender gap in access to financing that reached 5.8 p.p. Disaggregating the indicator, it is verified that the gap is mainly explained by the financing granted by financial institutions, with the gap for this subset reaching a value of 3.7 p.p. Within the subset of NFCPs, the gap is considerably smaller, with a difference of 0.4 p.p. for ETCNBs and 0.5 p.p. for NFPOs.

Figure 3.7 | Percentage of adults with at least one financing by gender and group of credit providers

Note | Data as of September 2019.

Source | BCRA and INDEC.

The evolution of the percentage of debtors by gender shows that, during 2018, the percentage of women who had at least one financing in the SFA increased by 0.8 p.p., while in the case of men the increase was 0.4 p.p. During 2019, however, there was a decrease in the percentage of adults who accessed financing, being 1 p.p. for women and 1.2 p.p. for men. These changes show a slight reduction in the gender gap in access to credit, a trend that has also been observed in previous years.

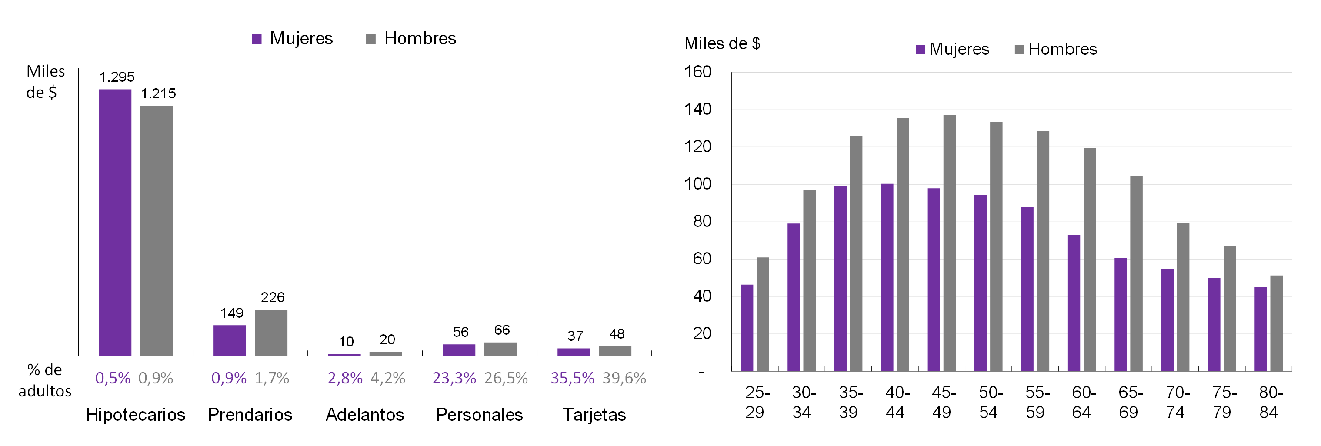

In all types of funding, the percentage of men was higher than that of women in the SFA. Although the difference between the percentage of men and women was greater in the case of credit cards and personal loans (4.1 p.p. and 3.1 p.p. respectively), for the types of loans that require greater collateral and a longer repayment period (pledge and mortgage loans) the difference between men and women was greater in relative terms (bearing in mind that there were almost twice as many men as women who had access to these types of financing). However, since title and mortgage loans cover considerably smaller percentages of the population, the impact of the disparity is relatively more limited. It should be clarified at this point that CENDEU registers loans in the name of a single debtor, so that, when a loan is taken out by more than one person (for example, a married couple who receive a mortgage loan), the financing is registered in CENDEU only in the name of one of them.

The gender gap is not only observed in the number of men and women who access credit, but also in the financing balances of each gender. In all types of financing, except for mortgage loans, there is a difference in balances to the detriment of women. In credit cards, the most widely used financing instrument, the difference between the average balance of men and women reached 30% in favor of men. For every $1,000 of financing balance that men had, women registered $769.

On the other hand, in terms of age of debtors, it can be seen that as of September 2019 the highest average debt balances for both genders were between 35 and 49 years old. From the age of 20, for all age ranges, there are higher balances for men than for women. One of the factors that could explain the gender gap observed in access to credit is participation in the labor market. According to INDEC51 data, women had an activity rate52 of 49.2% and an employment rate53 of 43.9% in the third quarter of 2019, while for men these values amounted to 70.2% and 64% respectively.

Figure 3.8 | Average balance by type of care, gender and age group

Data as of September 2019. Debtors and SFA balances.

Source | BCRA and INDEC.

Taking the possession of a salary account as an indicator of registered work, as of September 2019, 21% of women had at least one salary account, while for men the percentage rose to 28%. Within this group, 78% of women had at least one financing in the SFA, while for men this value rose to 80%. Thus, it is observed that considering the universe of adults who participate in the formal labor market, the gender gap in access to credit, although reduced, is still present. This would indicate that there are other factors, in addition to participation in the formal labor market, that affect access to credit for men and women.

3.2. Credit to productive

units In the first IIF, the financial inclusion of the country’s companies in terms of their use of financing was analyzed. On that occasion, a static study was carried out, characterizing the situation at a moment in time. In this report, based on historical series, the temporal dimension of the metrics already presented is incorporated, considering the evolution of around 600,000 productive units between 2007 and 2018.

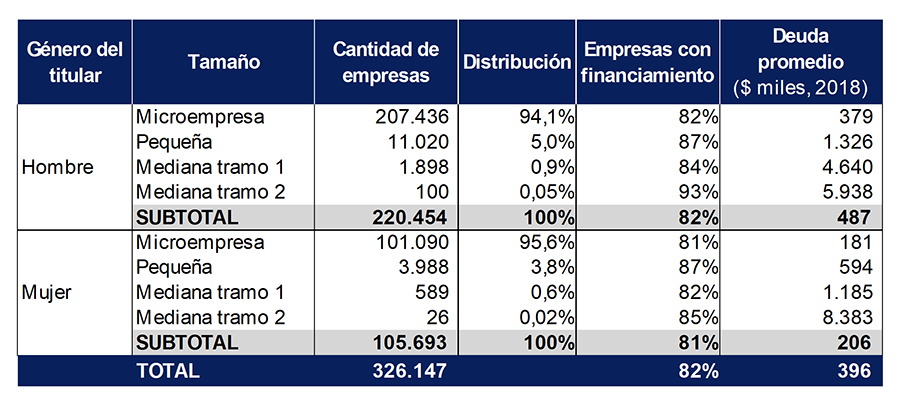

The temporal analyses include both the financing of companies incorporated as legal entities (PJ companies) and those individuals that carry out a productive and/or commercial activity without being incorporated as companies or legal entities (PH companies). It should be noted that the analyses of PH companies may be influenced by the fact that it is not possible to distinguish precisely financing for productive purposes from lines of credit for consumption. For this reason, in some passages of the section, PH companies are excluded from the analyses, as well as analyses excluding large and medium-sized companies section 2 in order to focus the study on MSMEs54, which are of greater interest for financial inclusion.

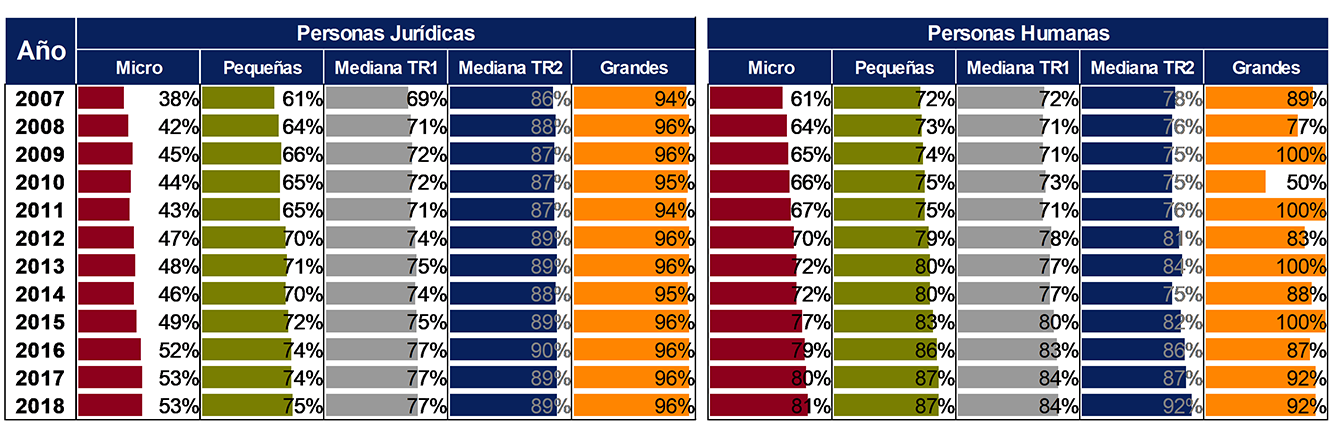

Figure 3.9 | Evolution of the percentage of companies that took out a loan with the SFA discriminated by company size and type of person

Note | Companies with financing for any month of the year considered.

Source | BCRA and Ministry of Productive Development.

The first credit indicator presented in the previous IIF consisted of the percentage of companies that took out some financing with the expanded financial system (SFA)55. It emphasized the disparities observed at the level of company size; in the case of PJ companies, only 53% of microenterprises took financing during 2018, while for large companies this proportion was 96%. Analyzing the historical evolution, it is found that these gaps tended to narrow, especially until 2016.

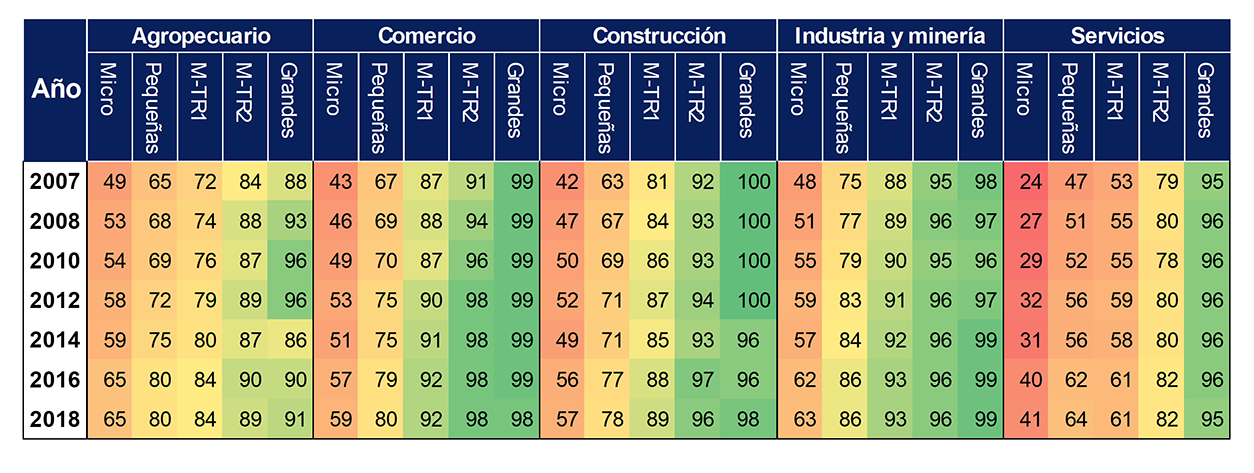

Analyzing the evolution of this same indicator by sector of activity for PJ companies, and focusing on smaller units, it is observed that the general trend of increase in the proportion of companies with financing is verified at all levels and sectors, with very slight differences in magnitude. Considering the performance of this indicator in absolute terms, it appears that the gaps between sectors were reduced, given that the sectors with less access to financing increased by a greater amount.

In particular, the evolution of the services sector stands out, which expanded the percentage of coverage between 2007 and 2018 from 24% to 41% for microenterprises and from 47% to 64% for small companies. However, in relative terms of the number of excluded companies, the agricultural, industry and mining sectors, which were already starting from higher values, were the ones that registered the best performance between 2007 and 2018. In the agricultural sector, the indicator of microenterprises with financing increased by 16 p.p., and that of small enterprises by 15 p.p., representing 31% and 46%, respectively, of the number of unfinanced enterprises in 2007.

Figure 3.10 | Evolution of the percentage of PJ companies that took out a loan with the SFA discriminated by company size and economic sector

Note | Companies with financing for any month of the year considered. M-TR1 and M-TR2 means medium tranche 1 and tranche 2, respectively.

Source | BCRA and Ministry of Productive Development.

In the industry and mining sector, the behavior was similar, registering a 15 p.p. increase for microenterprises and 11 p.p. for small companies, values that represented 29% and 44% of companies without financing in 2007. For its part, the services sector, which showed the highest absolute increase (17 p.p. for microenterprises and small enterprises), was the one with the worst final performance in relative terms, given the low initial level, incorporating 22% and 32% of microenterprises and small enterprises, respectively, without financing in 200756.

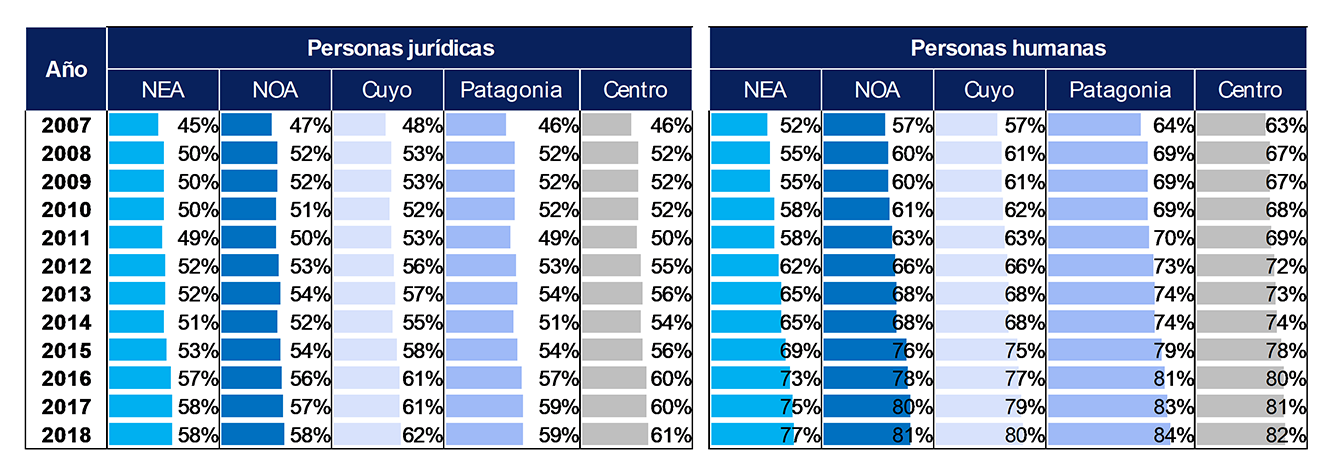

At the regional level, there are very slight differences in the percentages of companies with financing. Considering MSMEs, the largest increases in absolute terms occurred in the NOA and NEA for PH MSMEs, with growth of 25 p.p. and 24 p.p. between 2007 and 2018, respectively, thus reducing the gap with the regions that had a higher percentage with financing, such as Centro and Patagonia. In the case of PJ MSMEs, the increase in the indicator was more moderate and the gaps between regions tended to widen, with a greater incorporation of companies in Centro and Cuyo, although regional differentials remained at insignificant values (4 p.p. difference between the region with the highest and lowest percentage).

Figure 3.11 | Evolution of the percentage of MSMEs that took out a loan with the SFA discriminated by type of person and geographical region

Note | Companies with financing for any month of the year considered. Source | BCRA and Ministry of Productive Development.

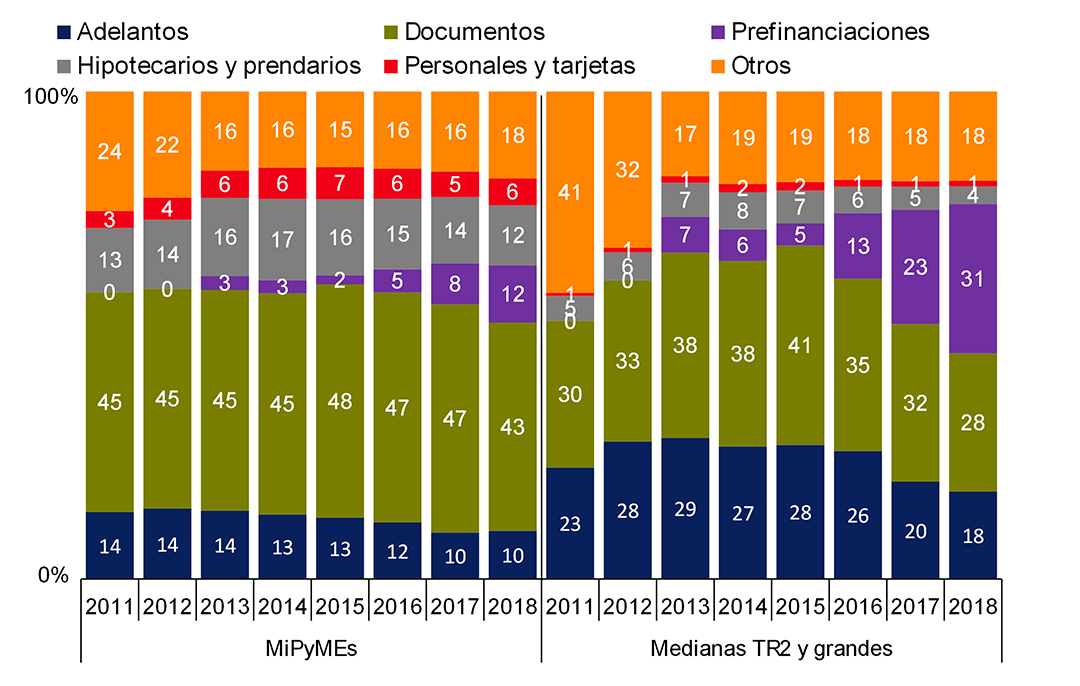

Within the universe of companies that took financing in the period analyzed, not all used the same type of financing. PJ MSMEs resorted to a greater extent to secured loans, such as mortgages and pledges, which may express a stricter collateral requirement on the part of financing providers towards this type of companies compared to larger ones.

On the other hand, PJ MSMEs also used document discounting to a greater extent, while medium-sized companies tranche 2 and large companies resorted relatively more to advances. Although both types of financing are usually short-term and oriented to working capital, it can again be deduced that PJ MSMEs require some additional support to obtain financing (a document to be discounted, such as a check).

On the other hand, in terms of evolution, the marked growth of export pre-financing from 2016 onwards stands out, becoming the main type of financing for larger companies. This was in line with the increase in foreign currency deposits in financial institutions57, which allowed for an increase in credit to exporting companies. Although it was the largest companies that were able to take advantage of this context to a greater extent, the reach it had for PJ MSMEs was also significant, reaching 12% of financing in 2018.

Figure 3.12 |Distribution of the debt balance of PJ companies by type of assistance and company size

Note | It is calculated based on the sum of the monthly balances in real terms.

Source | BCRA and Ministry of Productive Development.

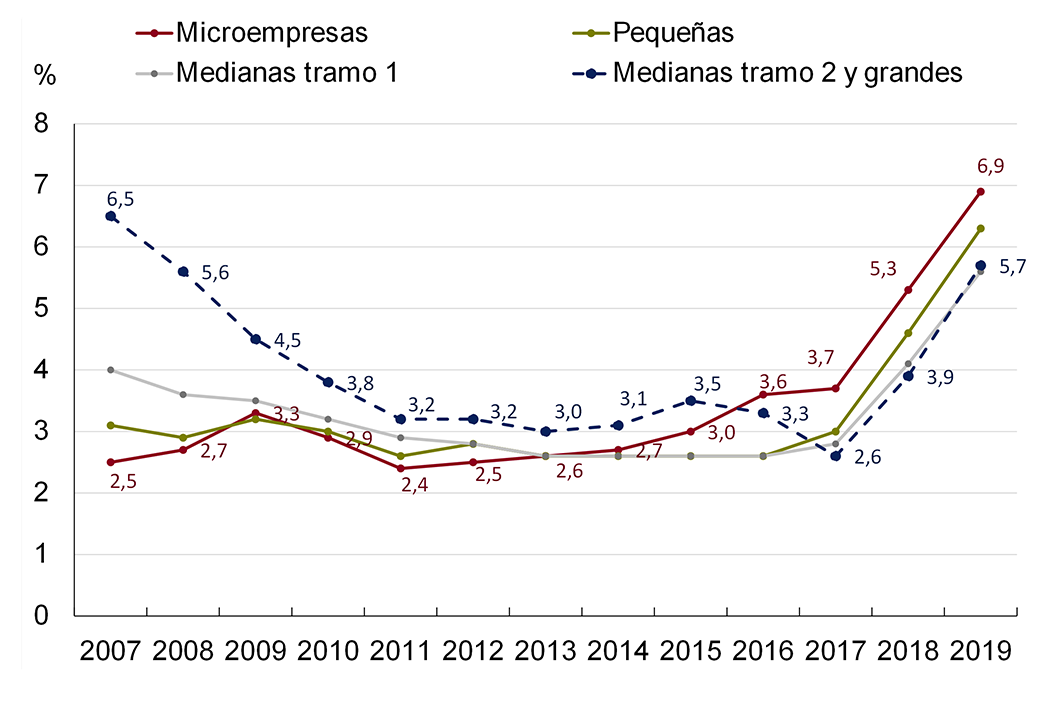

Another dimension from which the financial inclusion of companies can be measured, in addition to considering how many have access to financing, is to evaluate the extent to which they can afford to repay these loans. In this case, the indicator used consists of the percentage of companies – including both PH and PJ – that had some financing in an irregular situation58 (in relation to the total number of companies with financing). This indicator showed a markedly differentiated evolution for different sizes of companies.