I. Recent measures2

With the aim of continuing to expand access to banking services for the population, as well as to develop and improve the quality of the services provided, in November the BCRA enabled banking operations to be carried out through complementary agencies, commonly called banking correspondents.3

Recently, (i) the pledge or assignment as security (including fiduciary) of the bills of sale on future functional units to be built or under construction, with respect to which possession cannot be exercised due to their current non-existence, and (ii) the naval mortgage or pledge registered in the first degree on ships or naval artifacts —enabled or under construction—were incorporated as preferred “B” guarantees. 4

In line with the international standards established by the Basel Committee on Banking Supervision (BCBS), the BCRA recently approved the rules on “Large exposures to credit risk” that replace the rules on “Fractionation of credit risk” in the private sector as of January 1 of next year. 5 This criterion, which complements the minimum capital standard by protecting financial institutions from losses that would result from the default of a large debtor, was already implemented in the country with the aforementioned credit fractionation regulations, incorporating some nuances on the new international standards.

II. Activity

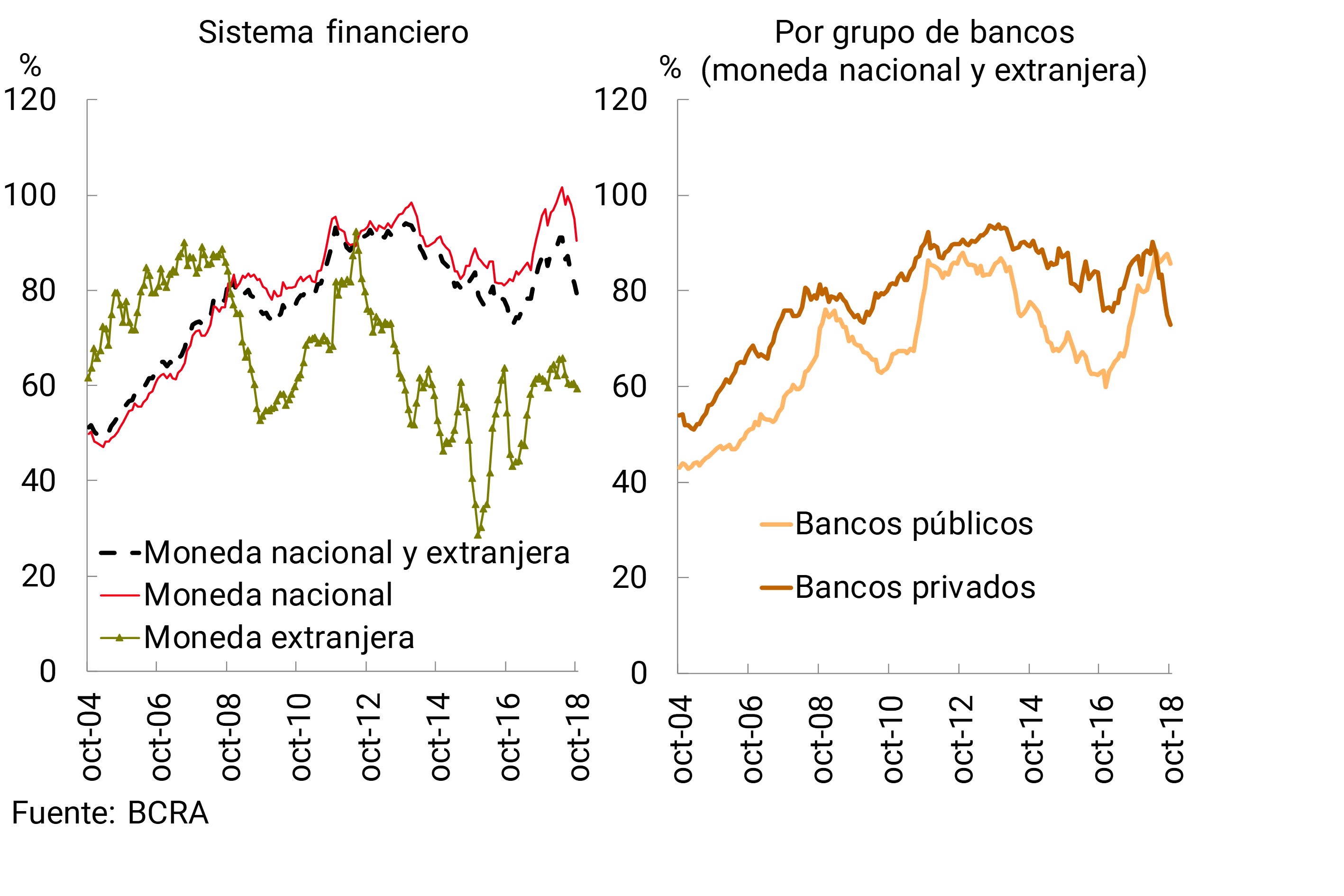

In line with recent performance, in October the changes in banks’ financial intermediation with the private sector were limited, with a reduction in deposit and credit balances in real terms compared to the previous month. Since the decline in lending was relatively greater than that in deposits, the ratio between the two fell again (see Chart 1), especially in private banks. The net assets of the financial system also fell in October (1.3% nominal or 6.3% real). 6

Graph 1 | Loans in Deposit Terms – Balance Sheet Balances – Private Sector

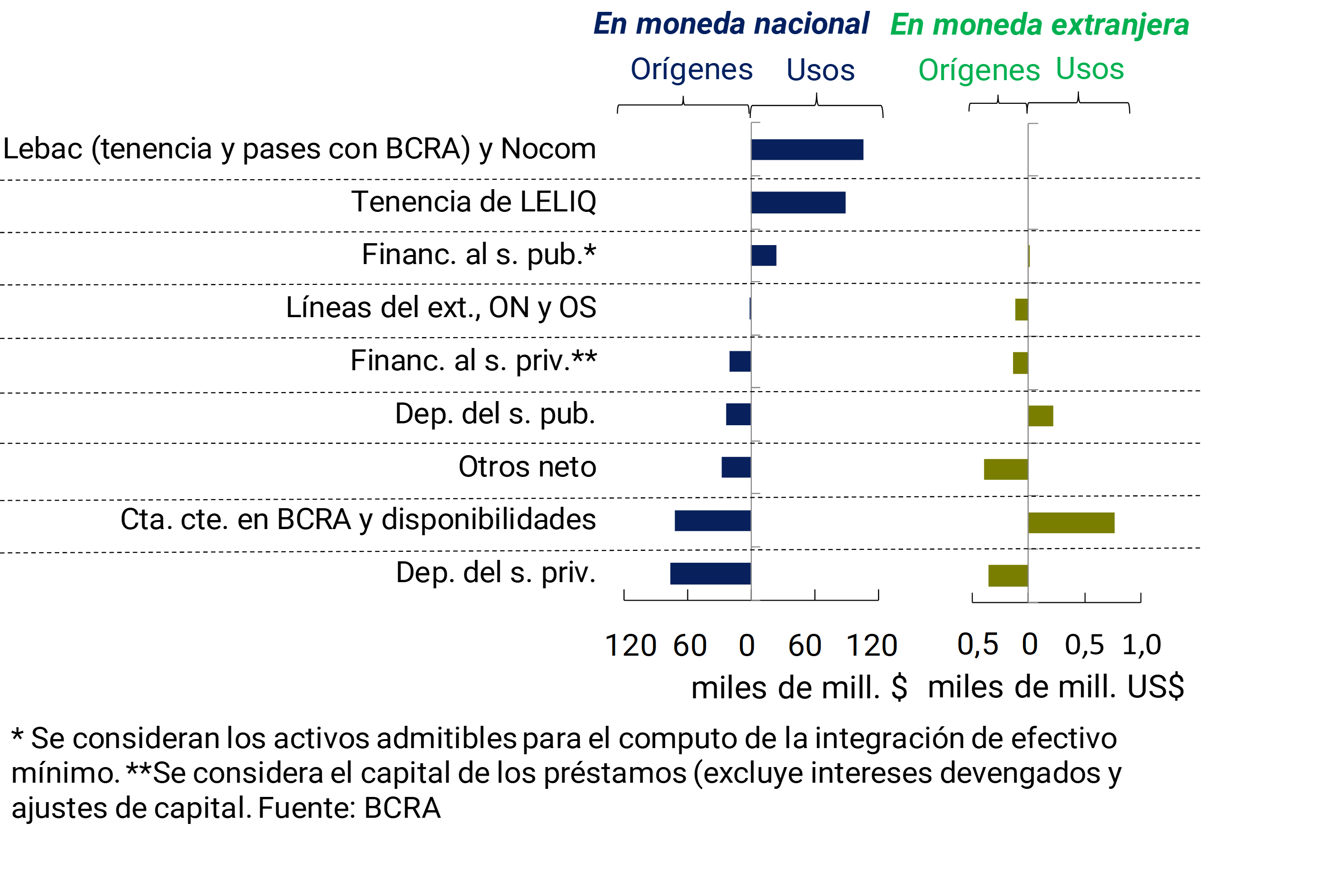

Based on the estimated monthly cash flow for the national currency items of the financial system, in October the nominal increase in private sector deposits ($76,000 million) and the reduction in the balance in the current accounts that banks have in the BCRA ($72,000 million) were the main sources of resources (see Graph 2). 7 These funds were mainly channeled to increase the holding of BCRA instruments ($89,000 million in LELIQ and $72,100 million in passes). For foreign currency items, the monthly increases in private sector deposits and liquidity were respectively the most relevant source and application of funds for banks as a whole.

Graph 2 | Oct-18 Cash Flow Estimate – Financial System – By Source Currency

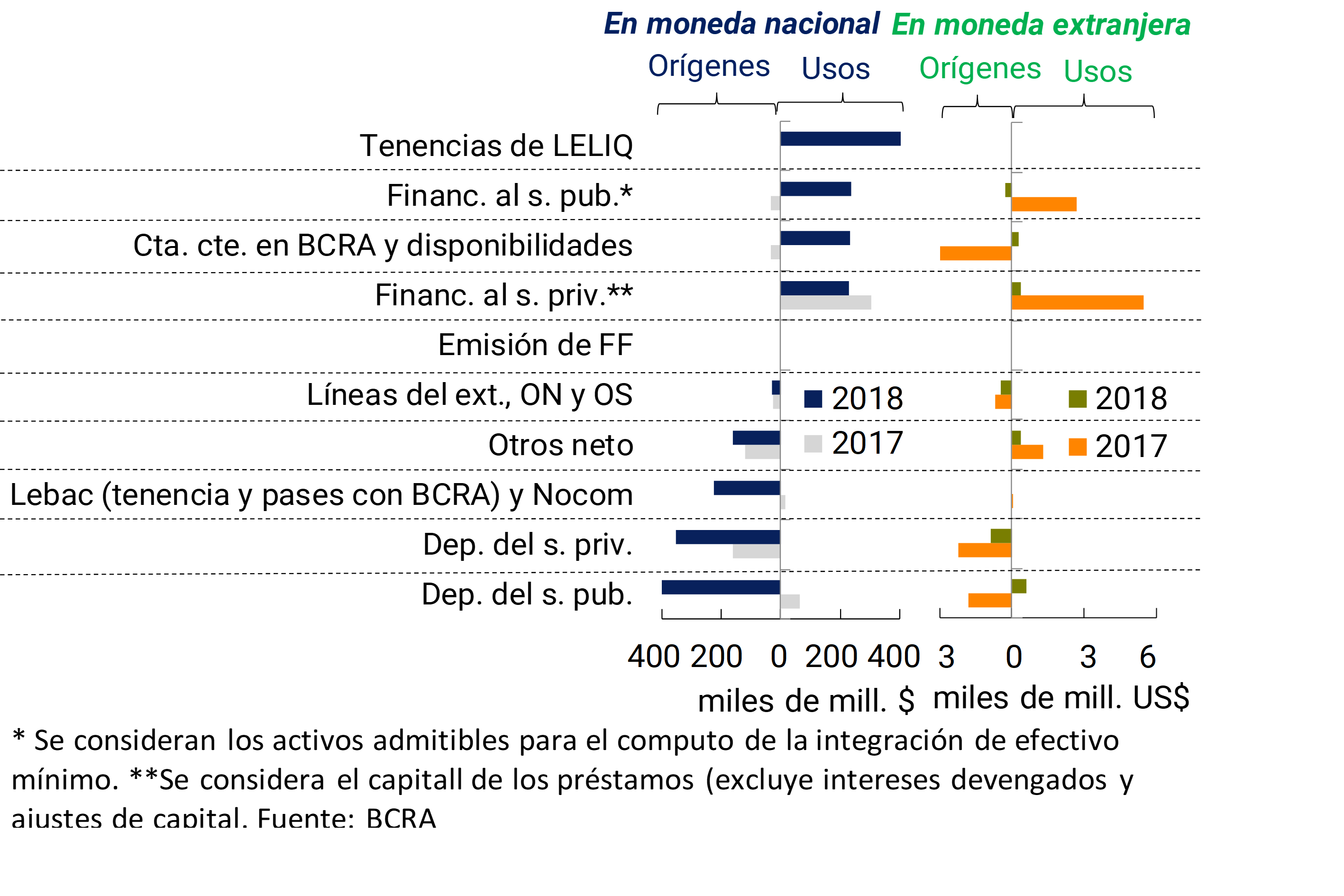

Considering the estimate of the flow of funds from the financial system for items in national currency in the accumulated ten months of the year, the increase in deposits ($402,000 million from the public sector and $351,000 million from the private sector) and the reduction in LEBAC holdings ($226,000 million) were the most important sources of resources (see Graph 3). These funds were used to increase the holdings of LELIQ ($478,000 million), credit to the public sector ($237,000 million), the balance of the current accounts of the entities in the BCRA ($231,000 million) and financing to the private sector ($229,000 million). On the other hand, the evolution of items denominated in foreign currency for the year as a whole showed less dynamism in relation to the same period last year (see Graph 3). The increase in private sector deposits and foreign credit lines were the most relevant sources of funds in foreign currency, while the decrease in public sector deposits and the increase in financing to the private sector and liquidity were the most important applications of resources in dollars for banks in the period.

Graph 3 | Estimated 10-Month Cumulative Cash Flow – Financial System – By Source Currency

In October, the mismatch of foreign currency assets for the financial system fell slightly, to 17.6% of the computable patrimonial responsibility (CPR). The monthly performance occurred in the context of the reduction of the nominal peso-dollar exchange rate. 8 Within the framework of the macroprudential policies established by the BCRA, banks as a whole currently have a limited foreign currency mismatch when compared to the peaks observed in previous years (see Chart 4).

Figure 4 | Foreign Currency (EM) Mismatch – EM Assets – EM Liabilities + Net Forward Purchases of EM without delivery of underlying* – As % of the financial system’s PRC

For its part, in October the active mismatch of items adjustable by CER in the financial system also fell slightly to a total of 48.1% of regulatory capital. The decrease in the spread was mainly explained by the significant growth in UVA deposits and by the placement of a negotiable obligation by a public bank in UVA, effects that were tempered by the granting of loans – more moderate than in previous months – and by the capital adjustment on the active mismatch. 9

Considering the operations of the National Payment System – the latest information available as of October 2018 – the amount in real terms (and the amount) of cleared checks increased slightly compared to September, although it accumulated a reduction of 9.9% YoY (-2.2% YoY). The ratio of check rejections due to lack of funds in relation to the total compensated also increased in the month, totaling 1.2% in amounts and 1.7% in amounts.

Bank transfers with instant credit increased compared to September – the latest information available as of October 2018 – both in amounts (adjusted for inflation) and in amounts. Immediate transactions mostly associated with individuals (through ATMs, home banking and mobile banking) continued to drive the performance of transfers.

III. Deposits and liquidity

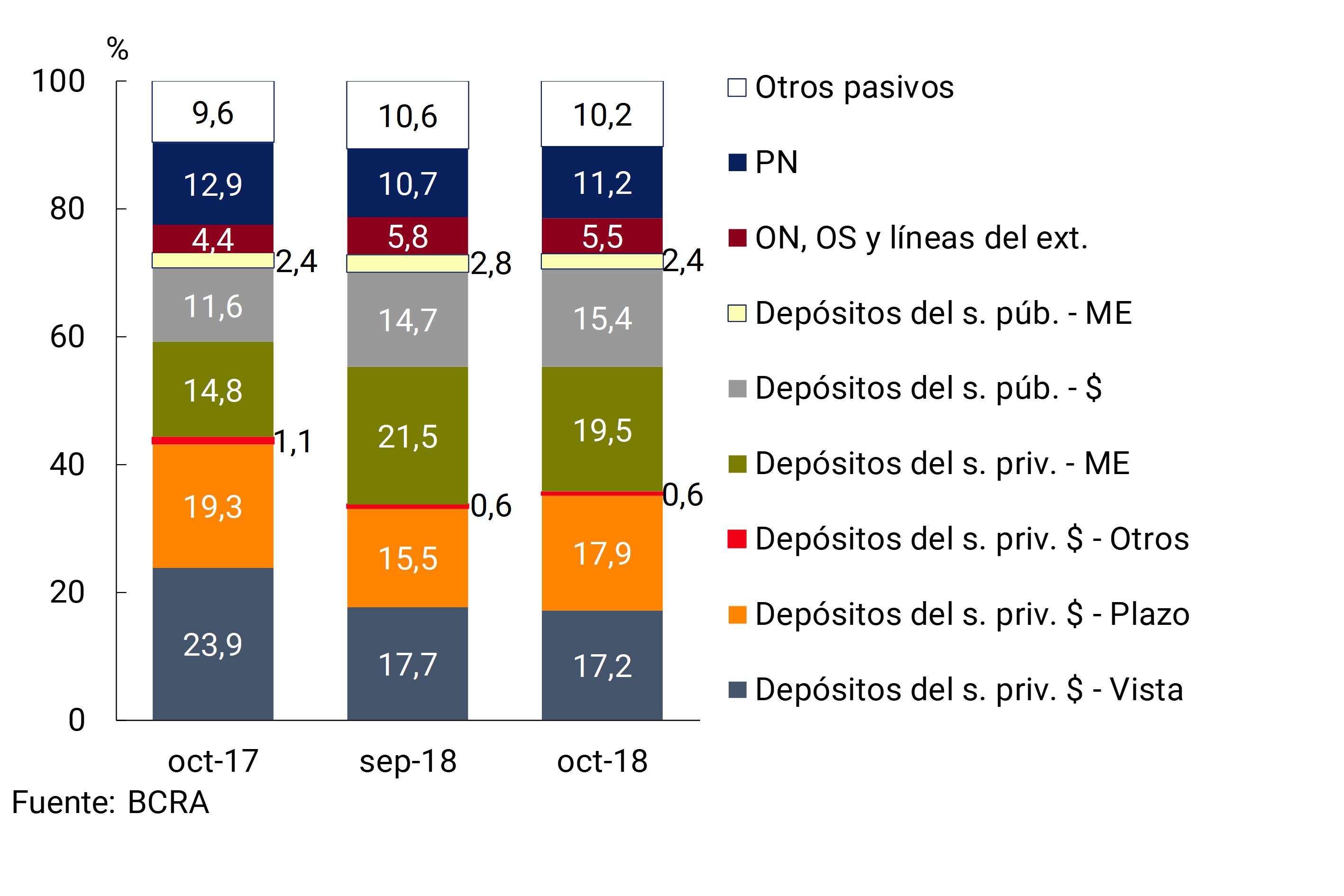

Considering the sources of funding of the financial system, in October the share of private sector deposits in the total (liabilities and net worth) did not show significant variations, standing at 55.3%. Among these deposits, it is worth highlighting the monthly performance of term placements in national currency, which increased their relative importance in total funding by 2.4 p.p., to 17.9% (see Graph 5). On the other hand, in the month, deposits in pesos on demand and those arranged in foreign currency decreased their weighting in total funding. 10

Graph 5 | Total Funding (Liabilities + NP) – Sistema Financiero

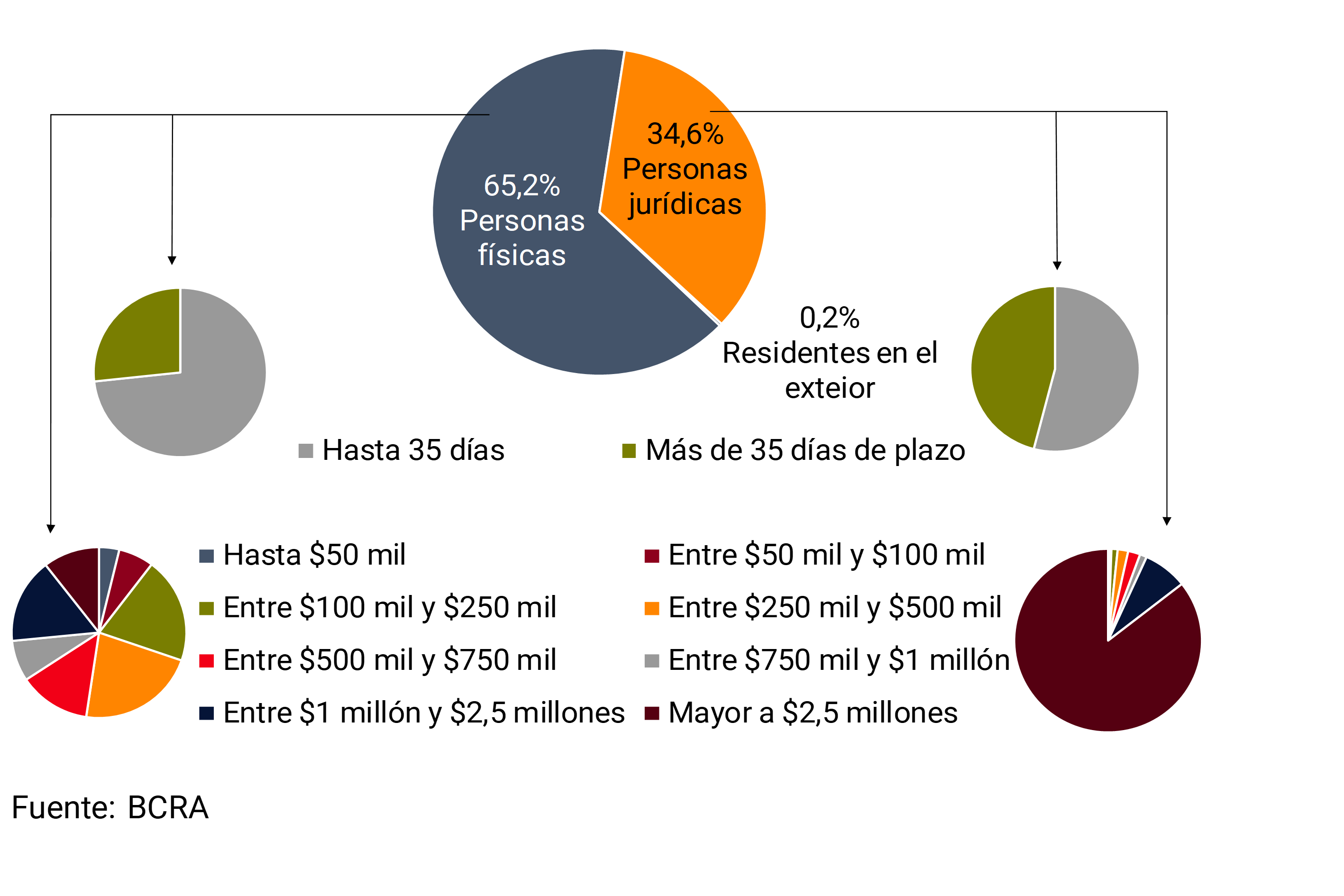

Total deposits in national currency fell 1.1% when adjusted for inflation in the month (+4.2% nominal), with a similar performance in public and private sector placements. Within the latter segment, the monthly drop was explained by demand accounts, as time deposits grew 8.1% in real terms between peak times of the month. This increase would be mainly explained by deposits made by individuals (see Graph 6), with two-thirds of the total traded in the month. 11 In the case of transactions involving natural persons, fixed terms of up to 35 days prevailed, while deposits made by legal persons in the month were made for relatively longer contractual terms. Meanwhile, total deposits in foreign currency increased slightly in the month (0.5% in foreign currency), driven by private sector placements.

Graph 6 | Private Sector Time Deposits in Pesos – Amounts Traded in October – Financial System

In a year-on-year comparison, total deposits in pesos accumulated an increase of 8.8% in real terms, driven by public sector placements. The balance of private sector deposits in national currency fell 5% in the last 12 months when adjusted for inflation. On the other hand, total deposits in foreign currency increased 7% in foreign currency compared to the same month of the previous year, driven by private sector placements (+10.5% y.o.y. in source currency).

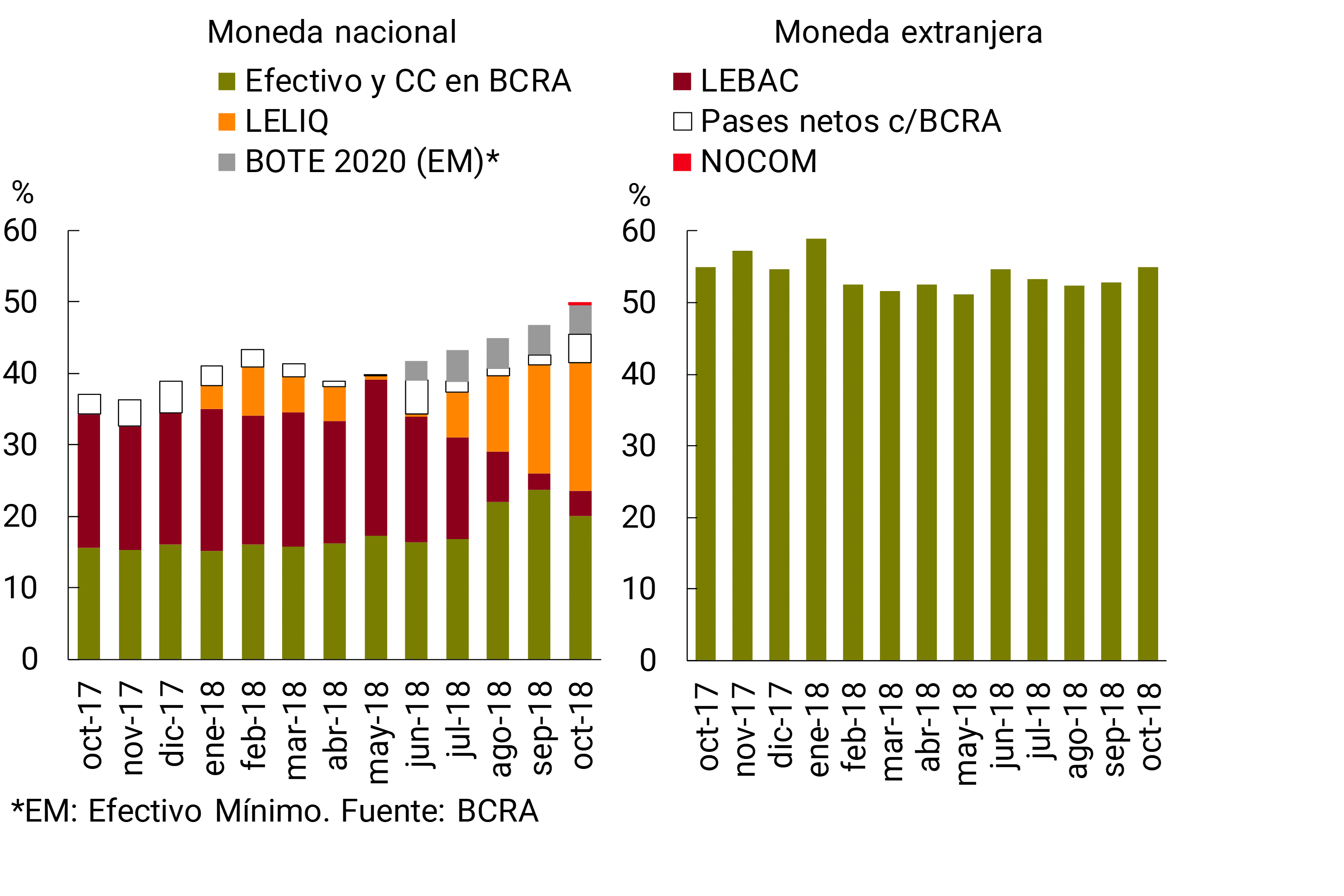

The liquidity of all financial institutions increased again in October. The broad liquidity ratio – integration of minimum cash, BCRA instruments and availabilities, in domestic and foreign currency – represented 51.3% of total deposits in the month (49.7% considering only items in pesos), increasing 2.5 p.p. (2.8 p.p.) compared to September. In line with the increase in reserve requirements – and the possibility of integrating part of it with LELIQ – 12, the composition of bank liquidity was modified in favor of LELIQ holdings and with a lower weighting of balances in the current accounts of financial institutions at the BCRA (see Chart 7). 13 In a year-on-year comparison, ample liquidity increased by 10.2 p.p. of deposits.

Figure 7 | Composition of Bank Liquidity – As % of Deposits

The interest rates that banks operated with the private sector for fixed-term deposits in pesos increased in October, reaching 46.9% nominal annual on average (+8.1 p.p. compared to September). This performance was in line with the trajectory of the benchmark interest rate and with the regulations that modified the remuneration of reserve requirements. In this context, the estimated funding cost for private sector deposits in pesos increased in the month.

IV. Exposures and Credit Quality

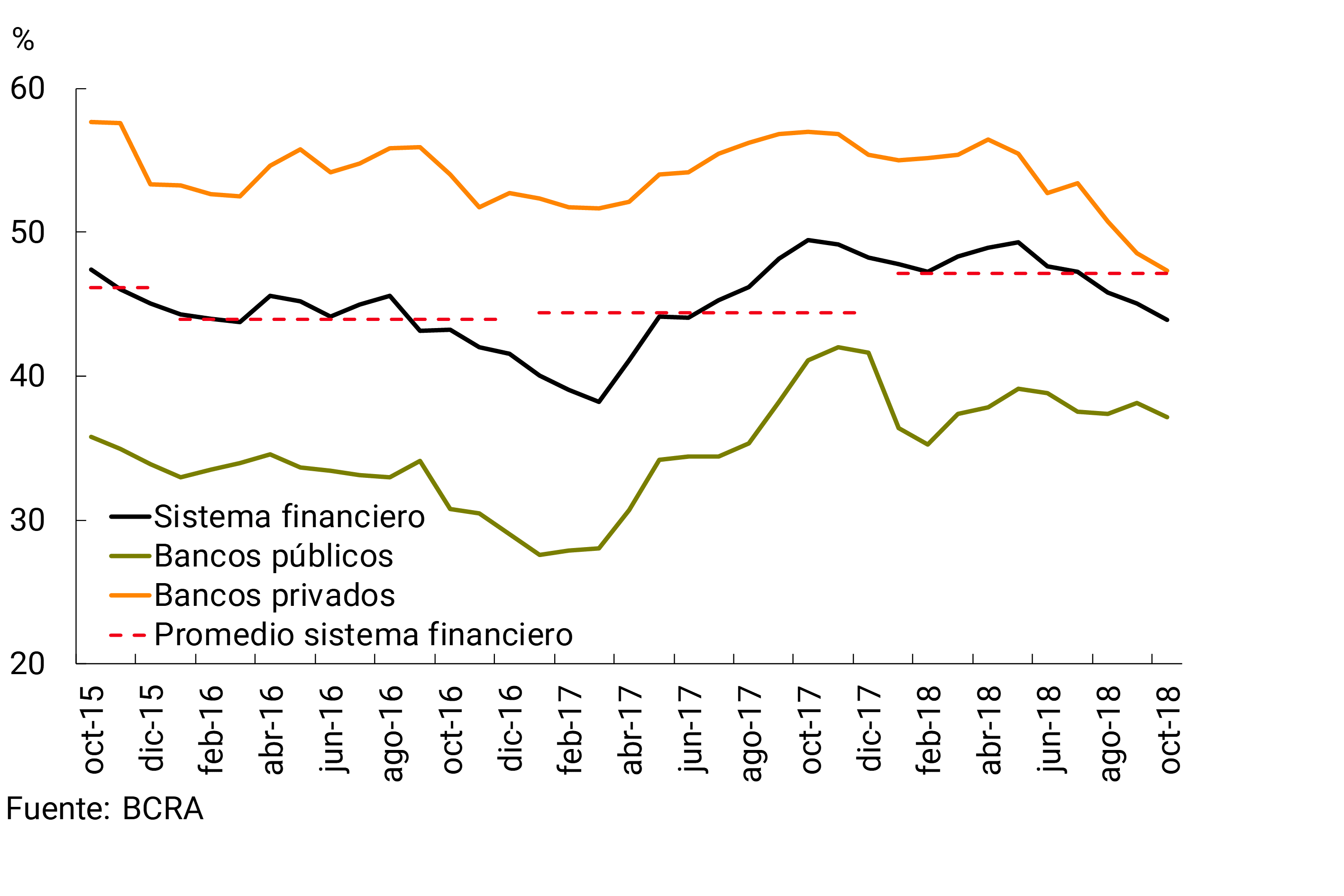

In October, the exposure of all financial institutions to the non-financial private sector continued to decline, accompanying the performance of the economy. Bank financing to the private sector in terms of assets fell 1.2 p.p. compared to the previous month, to represent 43.9% (see Chart 8). This decline was widespread among the different groups of financial institutions, with a greater relative decline observed in private banks.

Figure 8 | Gross Exposure to the Non-Financial Private Sector – Private Sector Financing as % of Net Assets

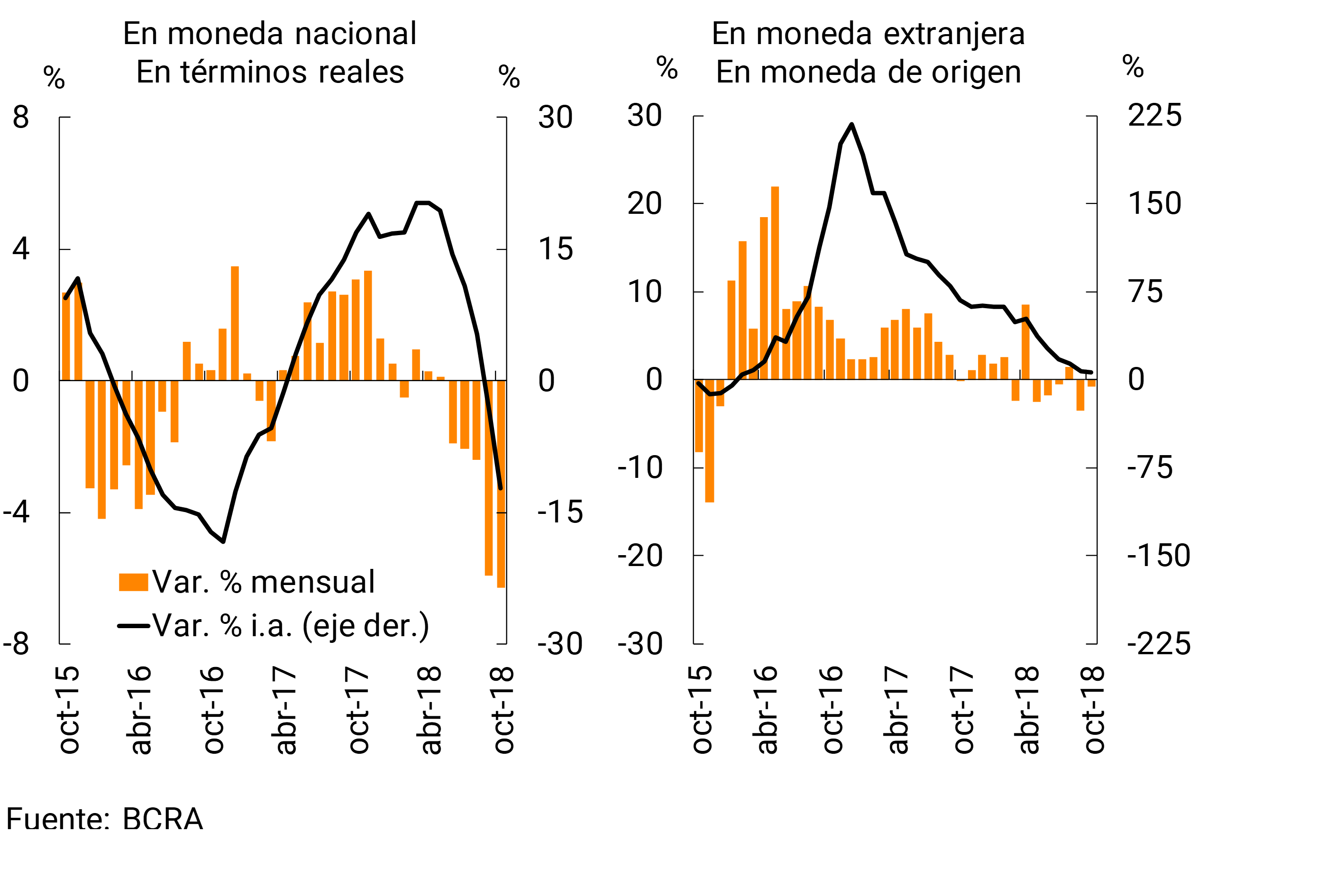

In the month, the balance of credit in pesos to the private sector contracted 6.3% when adjusted for inflation (-1.2% in nominal terms) (see Chart 9), mainly due to the performance of private banks. 14 All credit lines were reduced in real terms compared to September, with commercial lines (advances and documents) showing the largest relative falls. For its part, the balance of loans in foreign currency decreased 0.8% compared to September, mainly explained by the dynamics of public banks. 15 In this context, taking into account the effect of the monthly appreciation of the peso against the dollar, the total balance (including both domestic and foreign currency) of loans to the private sector expressed in pesos showed a fall of 8.8% in real terms (-3.9% nominal).

Figure 9 | Private Sector Credit Balance by Currency

In year-on-year terms, in October financing in pesos to companies and families accumulated a reduction of 12.3% in real terms (see Graph 9), driven mainly by documents and pledges. 16 Financing in foreign currency continued to register a slowdown in its year-on-year growth rate, reaching a variation of 6.3% YoY in October. 17

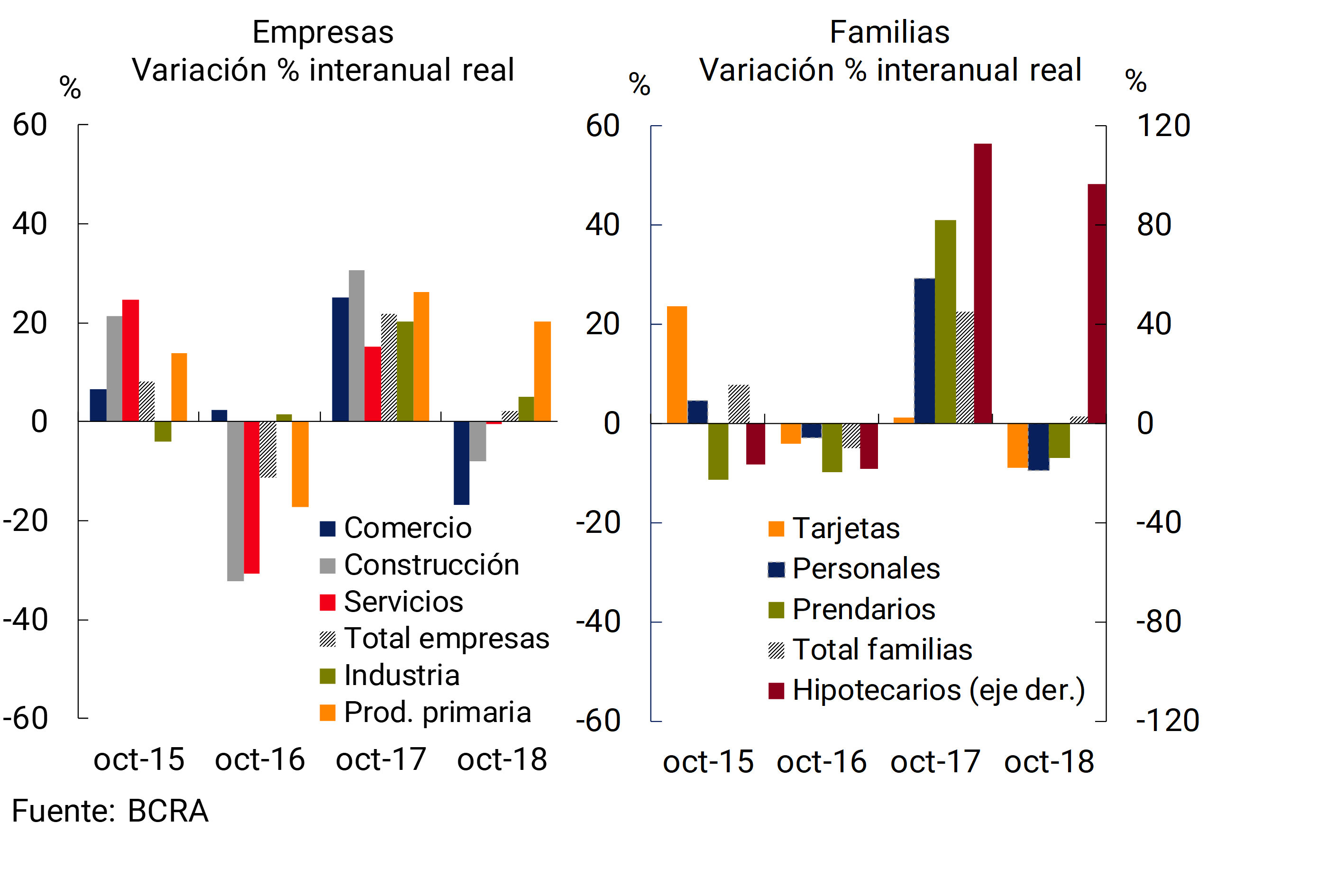

Differentiating by segment, in the month total bank financing (in domestic and foreign currency) to companies fell 13.7% compared to September in real terms (-9.1% nominal),18 influenced in part by the effect of the appreciation of the peso against the dollar. 19 Loans to industry and commerce showed the largest relative monthly falls. In this context, in October the total credit balance to companies in real terms remained practically unchanged compared to the level of the same month in 2017 (+2.1% real y.o.y., see Chart 10).

Figure 10 | Total Credit Balance by Segment

Financing to families fell by 2.8% in real terms in October (+2.5% nominal), with pledges and personal loans showing the most significant losses in the period. In a year-on-year comparison, the total credit balance to households when adjusted for inflation remained at a level similar to that observed a year ago (1.5% real YoY, see Chart 10). 20

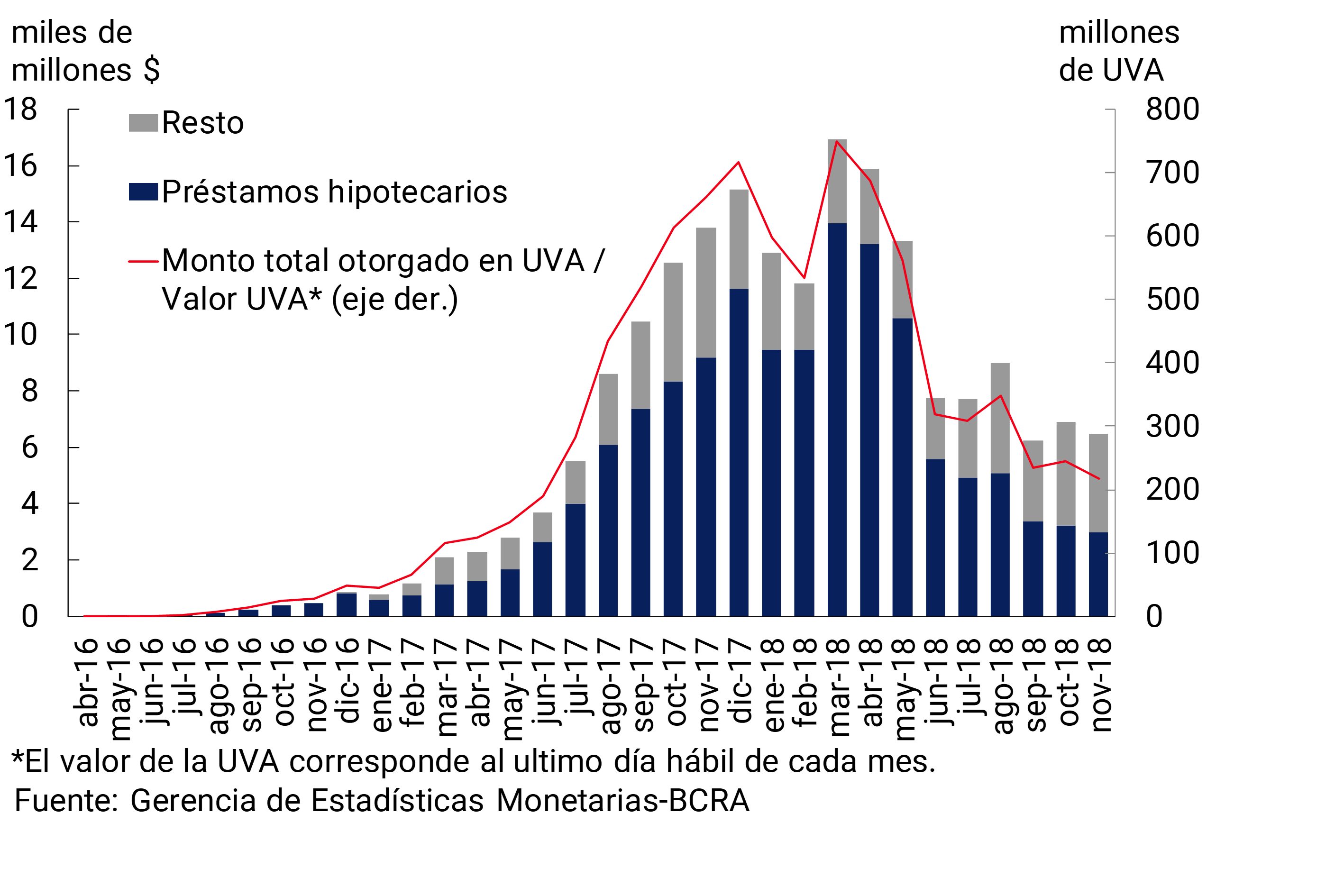

In November, financing granted in UVA reached $6,471 million (217 million UVA), below last month (see Graph 11). 21 A little less than half of the amount granted was channeled to mortgage loans (46%), while 38% was allocated to personal loans and the rest to pledges. Considering the information from the balance sheet of all financial institutions, in October the balance of credit in UVA to the private sector stood at $237,039 million (73% corresponded to mortgage loans), which represents 10.6% of the total financing portfolio to the private sector. 22

Figure 11 | UVA Financing – Amounts Granted

In October, the lending rates of the aggregate financial system operated in national currency with the private sector increased, a performance mainly explained by national private banks and public banks. 23 On the other hand, in the month, the average interest rates operated in UVA increased in personal and pledge loans, while in mortgages they fell slightly.

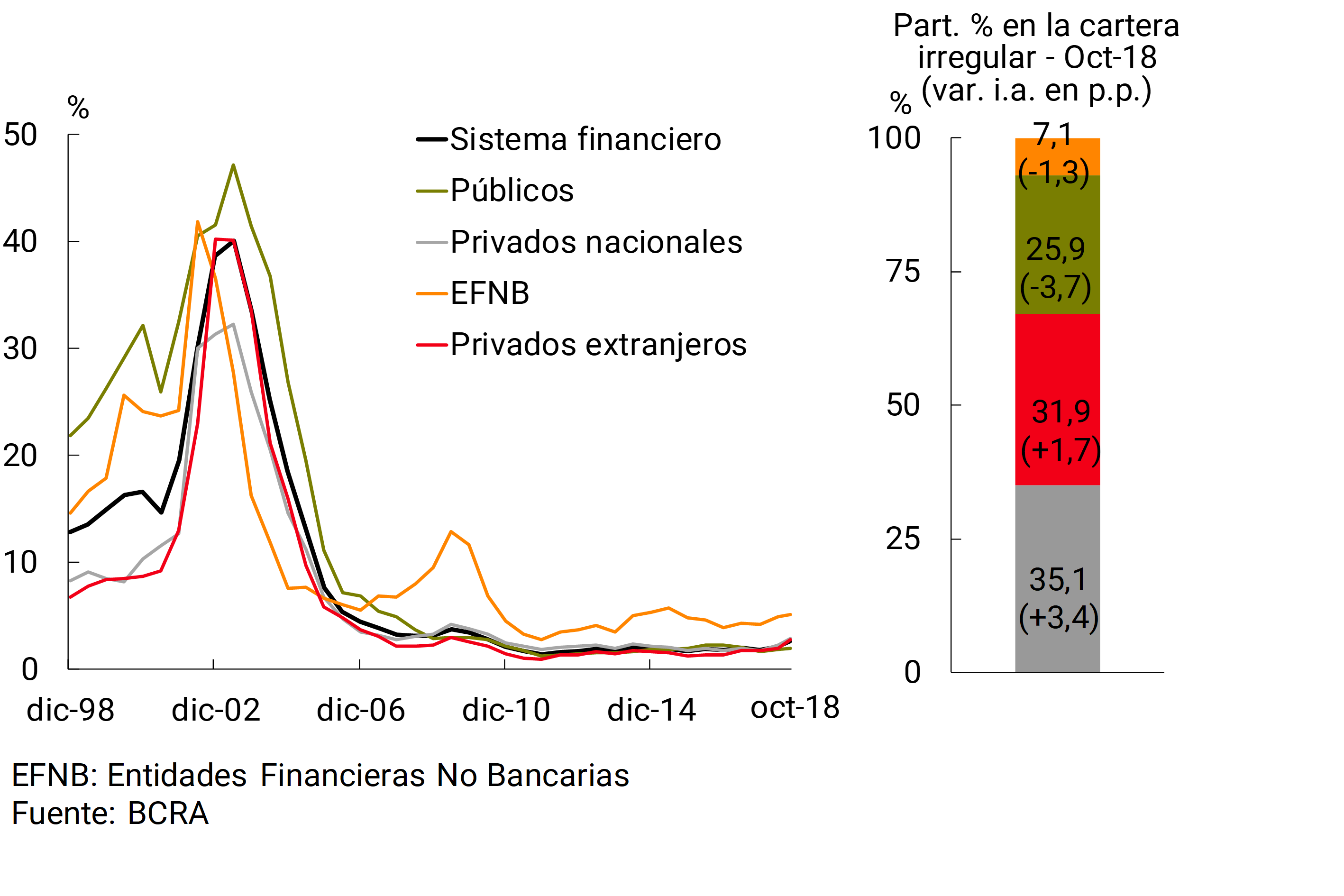

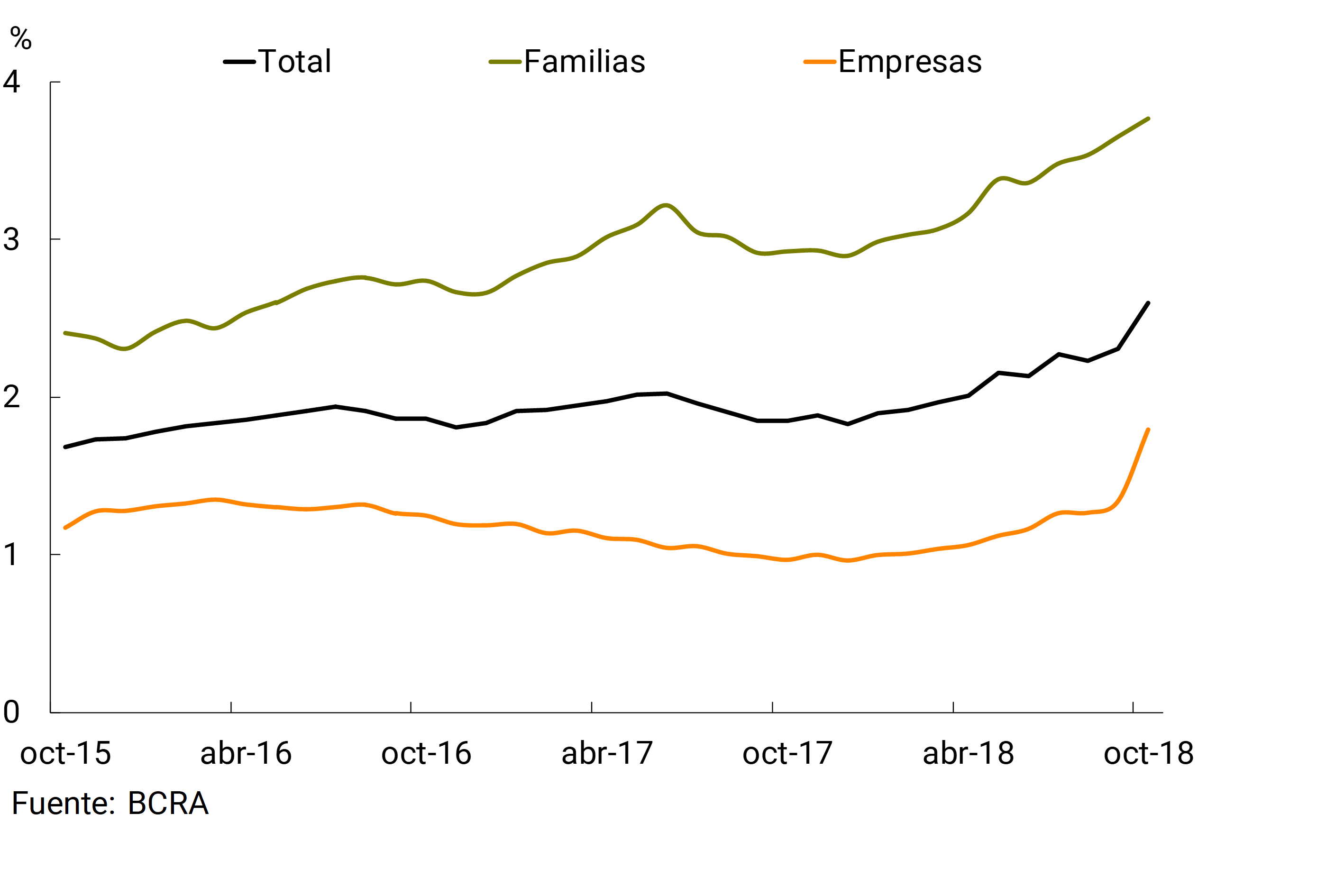

In a context of a fall in the nominal balance of total credit to the private sector and an increase in the nominal balance of financing in an irregular situation, in October the NPL ratio of financing to the private sector reached 2.6%, increasing 0.3 p.p. compared to last month’s value and 0.8 p.p. compared to the level of a year ago. The monthly performance was explained by private banks and, to a lesser extent, by non-bank financial institutions. For its part, the irregularity coefficient of financing to the private sector by public banks remained unchanged in magnitude in the period. It should be noted that, despite the increase observed in recent months, this indicator still remains at low levels compared to those observed years ago (see Graph 12) and to other economies in the region.

Figure 12 | Irregularity of Credit to the Private Sector – Irregular financing / Total financing (%)

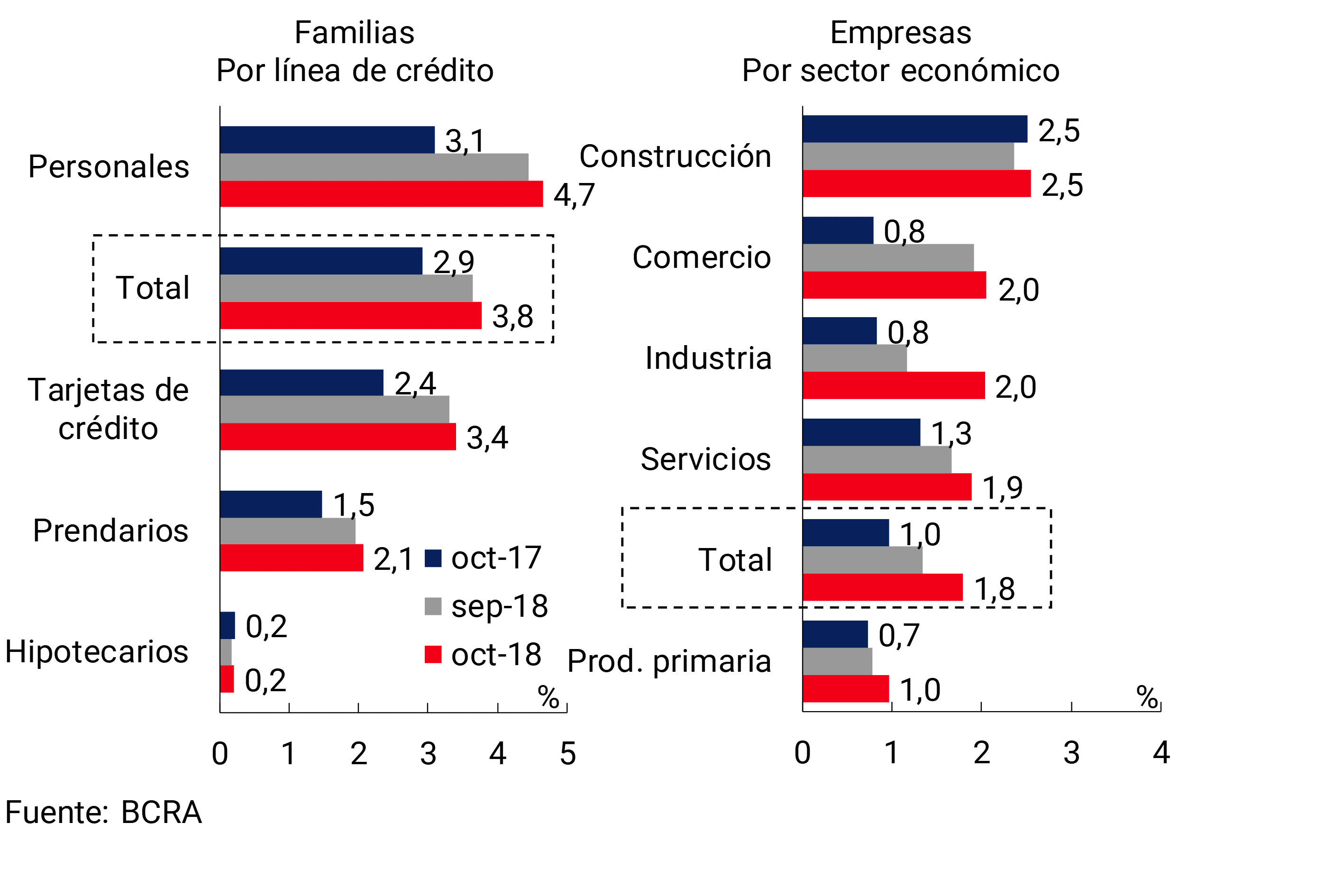

In the month, the non-performing loan ratio to companies increased by 0.5 p.p. compared to September, reaching 1.8% in the month (see Chart 13). The monthly increase was mainly explained by the performance of financing to industry (see Graph 14). Distinguishing by credit line, the advance delinquency indicator showed the highest relative increase with respect to the values observed in September. In year-on-year terms, the level of this coefficient increased by 0.8 p.p., driven mainly by loans to trade and industry.

Figure 13 | Irregularity of Credit to the Private Sector – Irregular financing / Total financing (%)

Figure 14 | Irregularity of Credit to the Private Sector – Irregular financing / Total financing (%)

NPLs on loans to households stood at 3.8% of the total portfolio to this sector in October (see Graph 14), slightly increasing compared to the previous month (+0.1 p.p.). In a year-on-year comparison, this indicator accumulated a rise of 0.8 p.p., explained by the performance of consumer lines (personal and credit cards), and to a lesser extent, of pledges. Meanwhile, mortgage loans maintained their levels of irregularity unchanged at 0.2% in the period. Within this segment, the NPL ratio of those denominated in UVA stood at 0.14%.

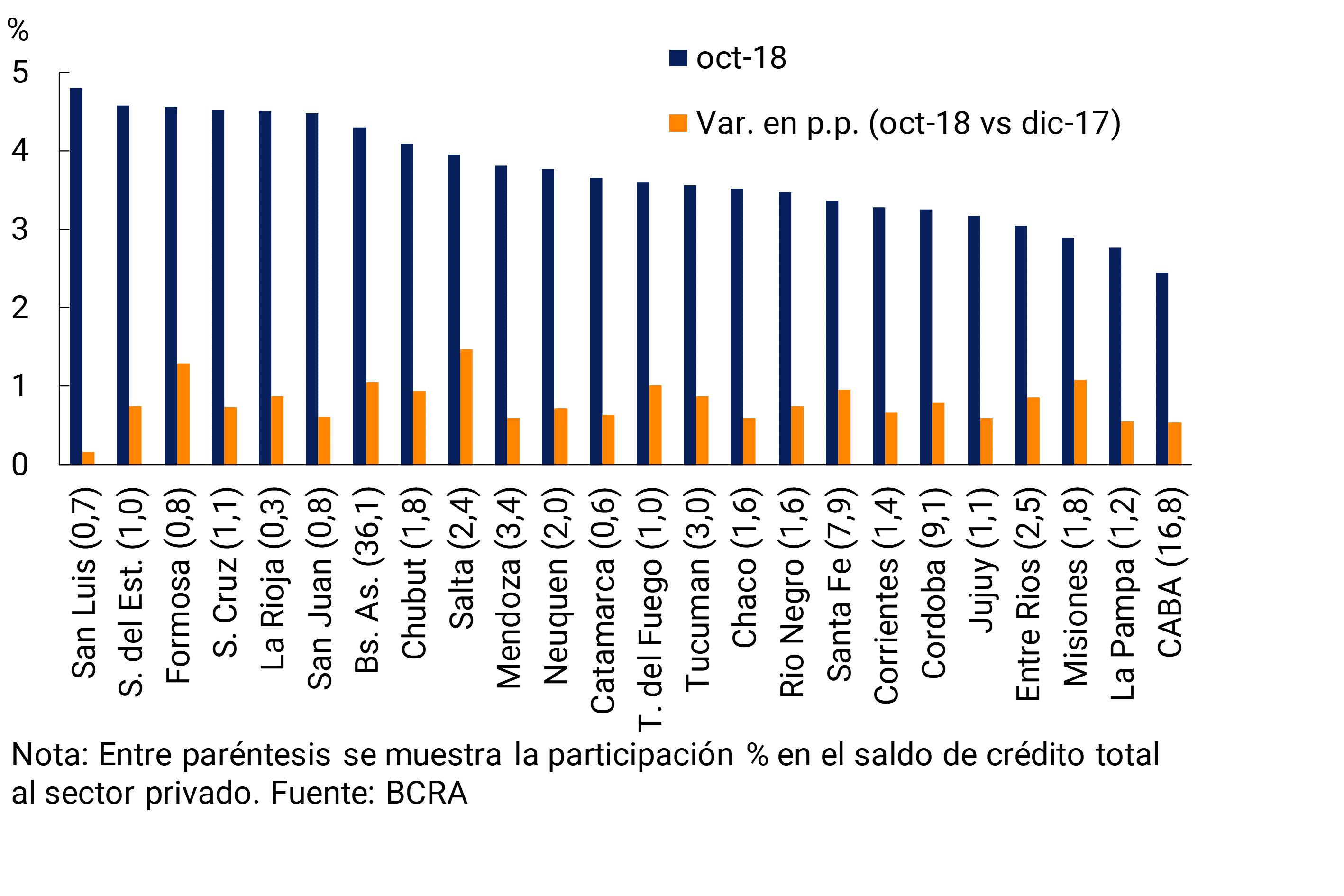

Considering the non-performing loan ratio of loans to individuals registered in each of the country’s provinces,24 in October, CABA, La Pampa, and Misiones had the lowest relative levels of this indicator, while San Luis, Santiago del Estero, and Formosa recorded the highest (see Graph 15). The increase in irregularity in a year-on-year comparison has been widespread between jurisdictions.

Figure 15 | Irregularity of Credit to Individuals – Irregular Financing / Total Financing (%)

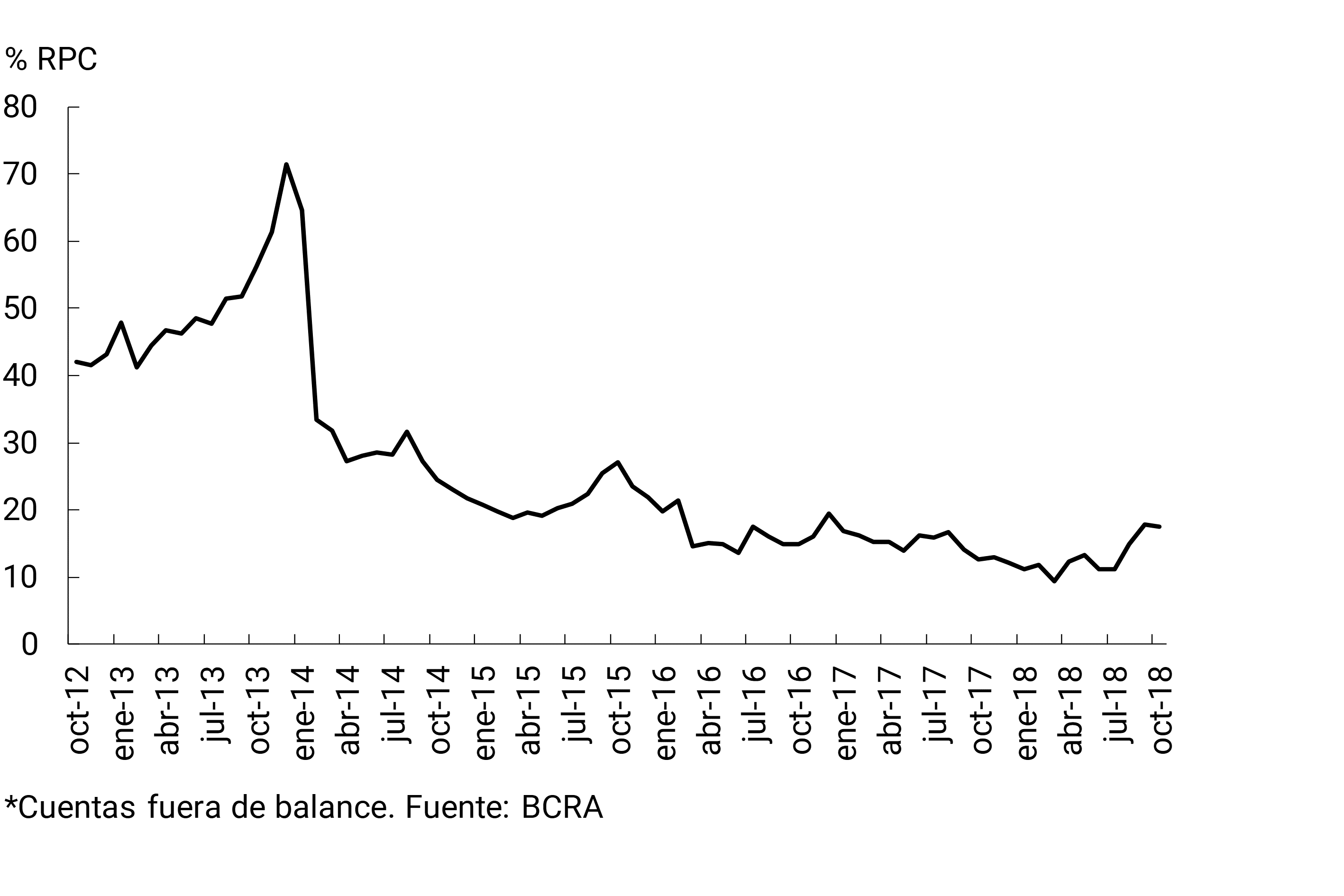

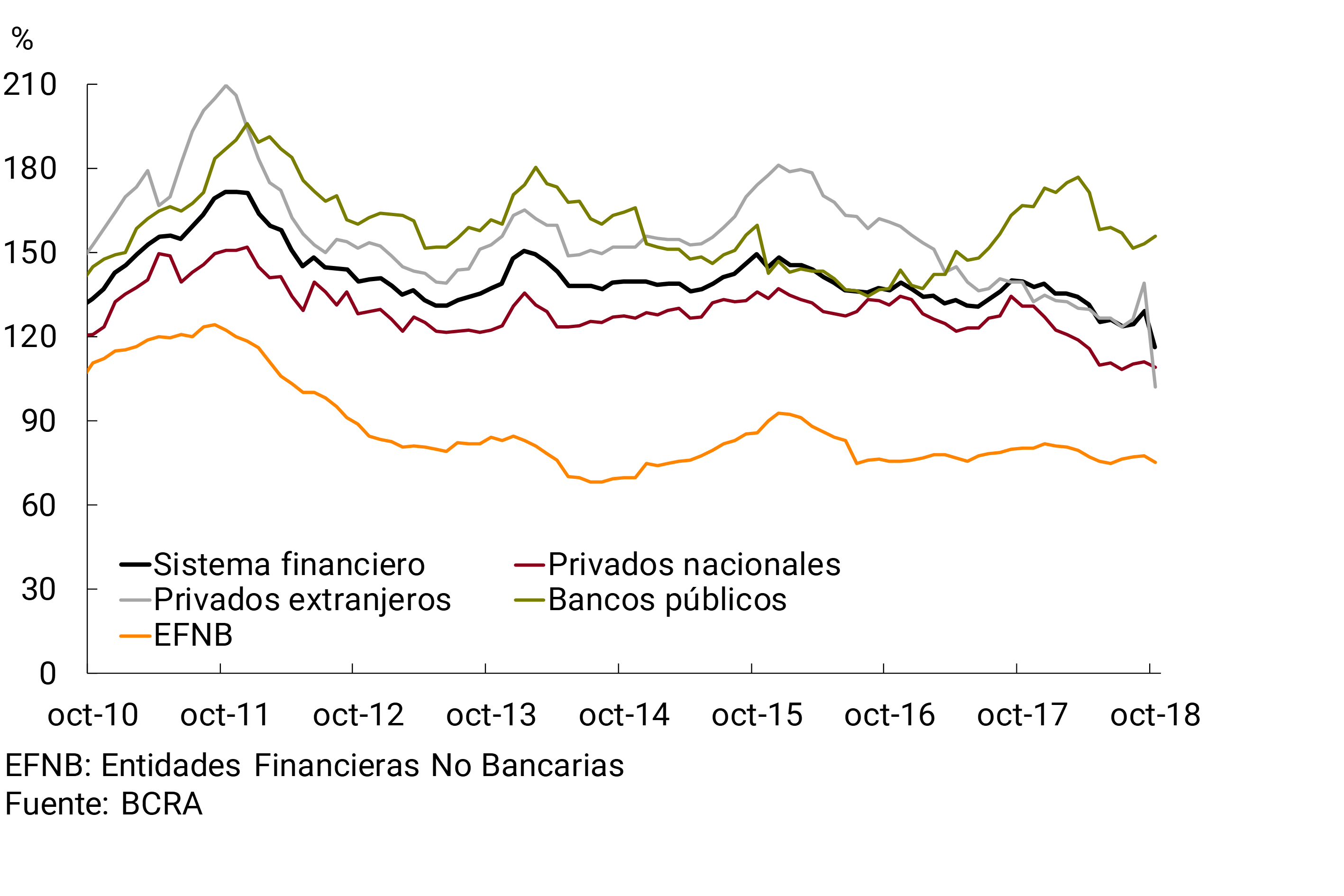

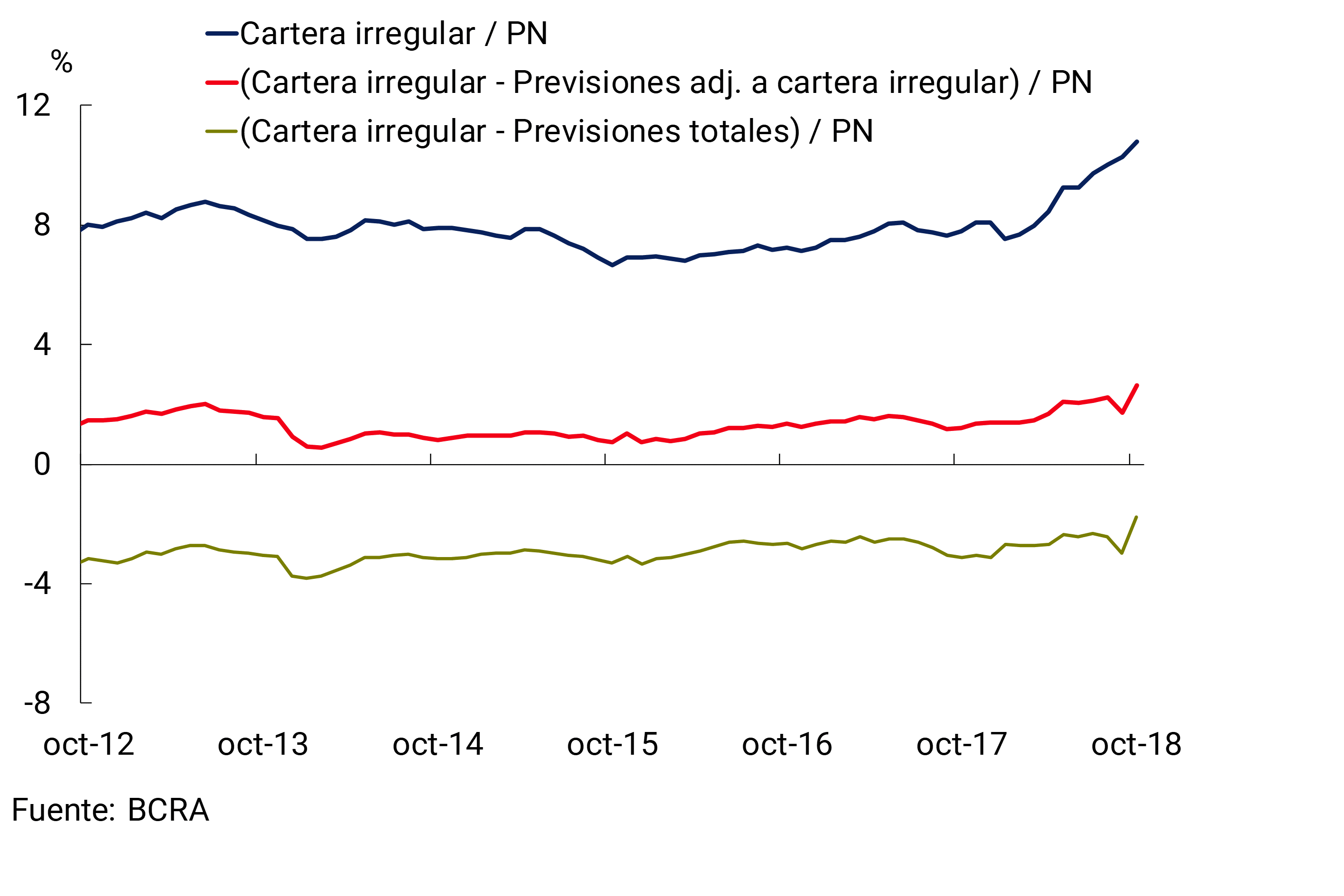

In October, the accounting forecasts of the aggregate financial system showed a balance equivalent to 117% of the private sector’s irregular portfolio, below the levels of previous months (see Chart 16). All bank groups continued to exhibit high levels of coverage with forecasts, which exceed the minimum regulatory requirements in force. In particular, public banks continued to have the highest degree of foresight in the sector. It should be considered that, if the minimum forecasts for the portfolio in regular status are excluded, this ratio would stand at 76% in the month, slightly lower than the value of a year ago.

Figure 16 | Forecasting of the Financial System – Forecasts / Irregular portfolio to the private sector (%)

In this context, the equity exposure of all financial institutions to the private sector continued to be at negative and moderate levels (see Chart 17). 25 Taking into account the forecasts allocated only to the non-performing portfolio, the financial system’s equity exposure would stand at 2.6% in October, above the values observed in previous months.

Figure 17 | Equity Exposure to the Private Sector – Financial System

V. Solvency

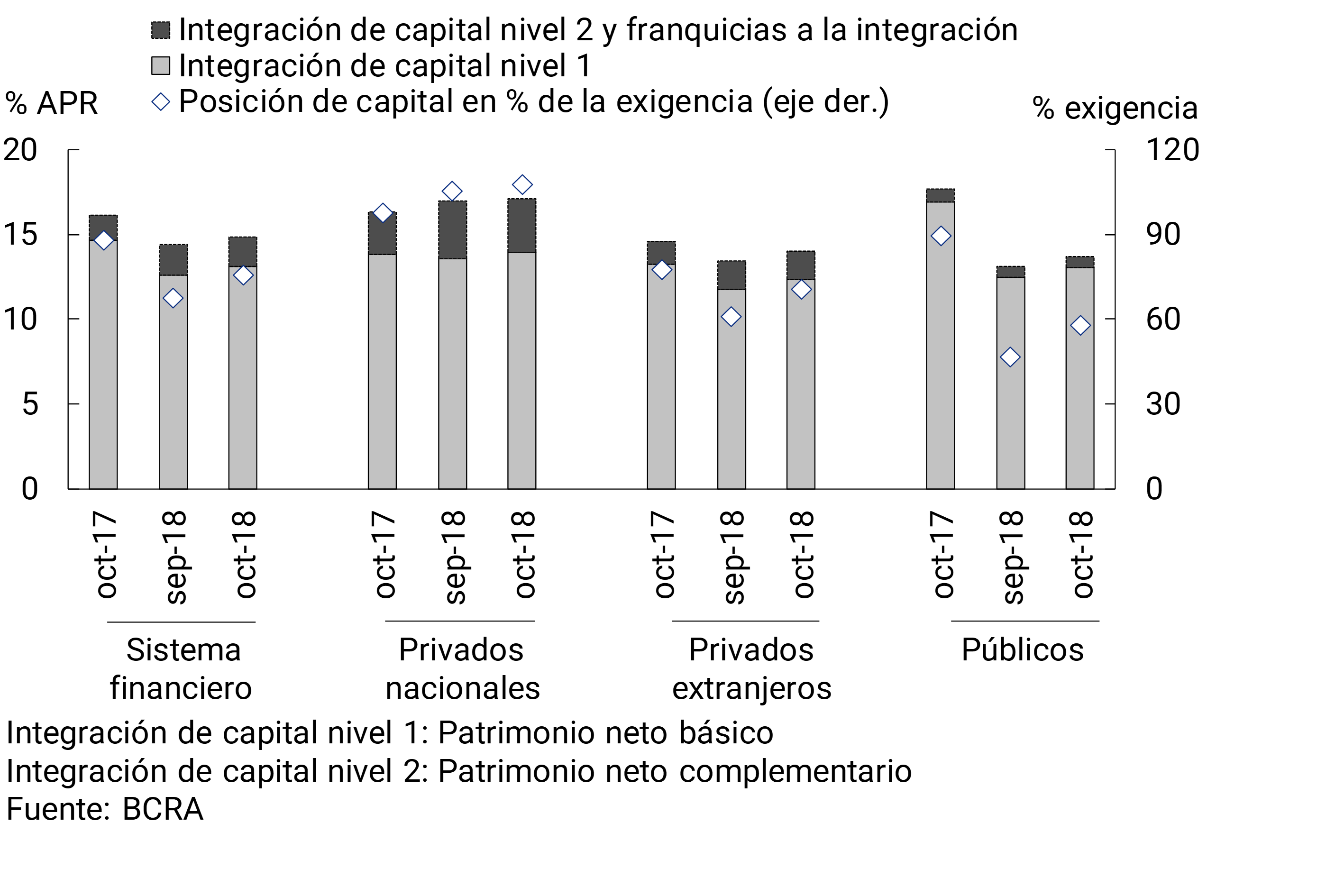

In October, the solvency ratios of the financial system increased slightly. In the month, the regulatory capital integration of the banks as a whole represented 14.9% of risk-weighted assets (RWA) (see Chart 18). 88% of the integrated capital continued to be accounted for by the segment with the greatest capacity to face unexpected losses (Tier 1 capital). The excess of integrated capital was equivalent to 76% of the regulatory requirement for the aggregate financial system.

Figure 18 | Capital Integration and Regulatory Capital Excess

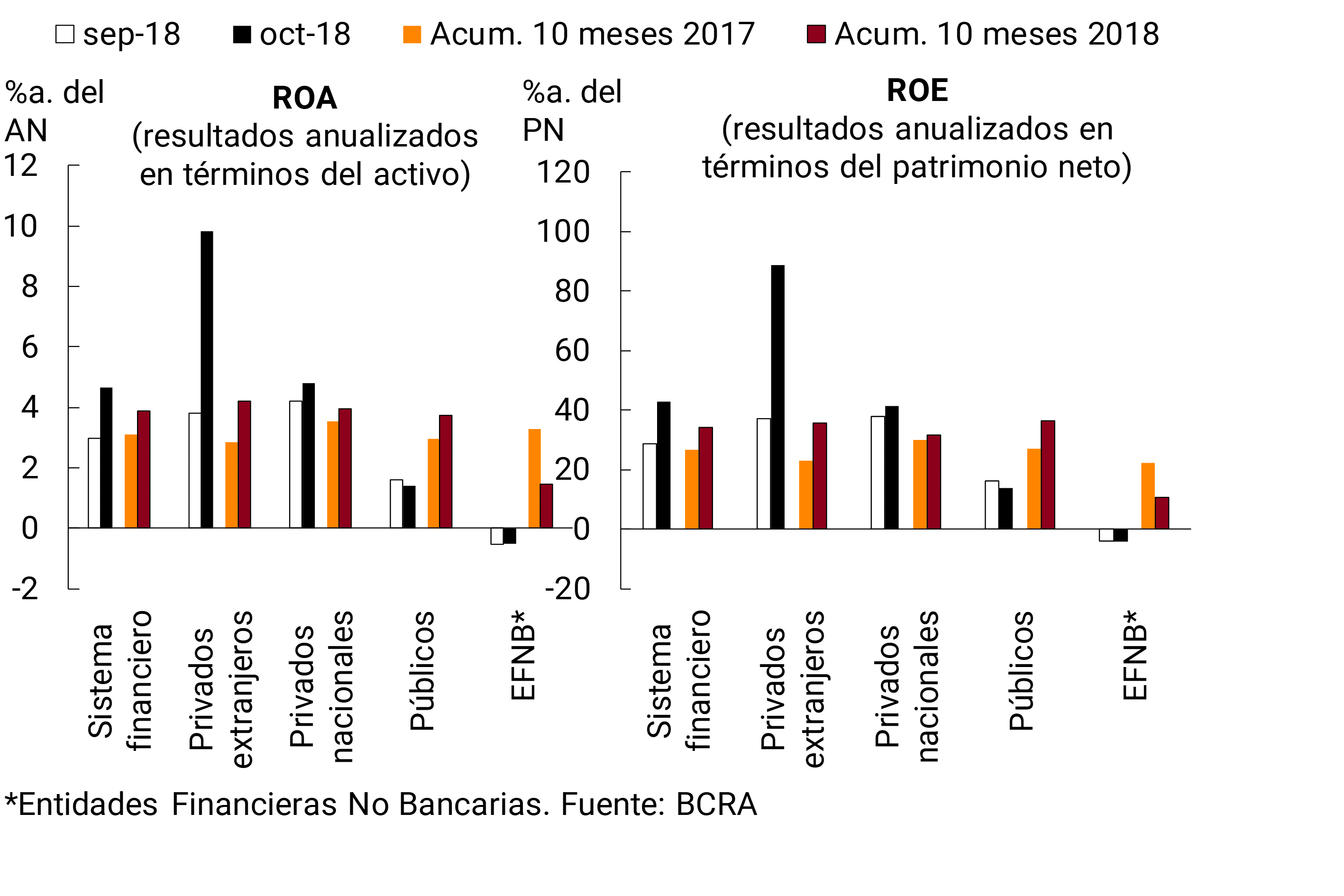

The nominal accounting results of the financial system in October represented 4.7% annualized (y.) of assets and 43% y. of net worth. These profitability indicators were higher than those evidenced in September, mainly due to the performance of private banks. For their part, public banks slightly reduced their profitability in the month. Considering the cumulative nominal flow of results for ten months of 2018, the financial system accrued an ROA of 3.9%a. and an ROE of 34.1%y. (see Graph 19), increasing 0.8 p.p. y.a. and 7.5 p.p. y.a., respectively.

Figure 19 | Profitability by Group of Financial Institutions

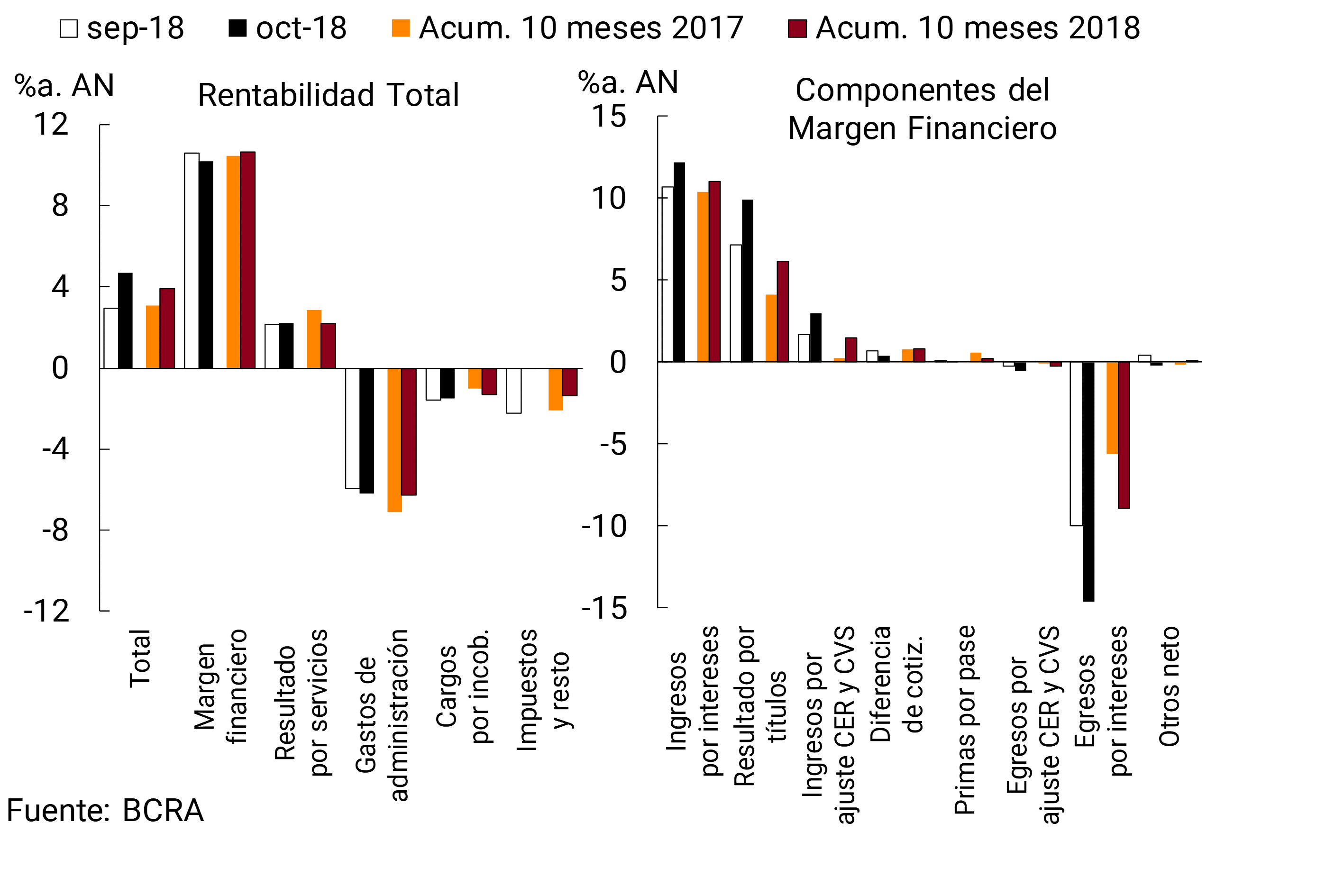

In October, the financial margin of the banks as a whole fell 0.4 p.p. of assets, to 10.2%y. (see Graph 20). The increase in interest outflows – in the context of the renewed dynamism of time deposits in pesos – was partially offset by higher earnings from securities, higher interest income and CER adjustment. In the cumulative ten-month period of 2018, the financial margin represented 10.6% y/y of assets, 0.2 p.p. more than in the same period of 2017. The year-on-year increase in securities gains, income from CER adjustments and interest income was tempered by the increase in interest and CER expenses and by the fall in pass premiums.

Figure 20 | Income Table – Financial System

Taking into account the group of private banks, in October the financial margin increased by 2.1 p.p. of assets. This increase was mainly due to higher gains on securities, higher interest income and positive share price differences, effects partially offset by higher interest expenses. In the cumulative ten months of 2018, the financial margin of private banks totaled 12% of assets, 0.7 p.p. more than in the same period last year.

In the month, the results for services of the financial system represented 2.2% of assets, slightly higher than in the previous month. In the cumulative period between January and October, these net income also reached 2.2% of assets, falling 0.7 p.p. of assets in a year-on-year comparison (see Chart 20).

Charges for uncollectibility of the financial system were slightly reduced compared to September, reaching 1.5% y/y of assets in the month. These levels are higher than those recorded in recent years and occur in the context of the increase in credit delinquencies (see Section IV). In October, such charges increased in the group of private banks and were reduced in public banks. Considering the accumulated in ten months of the year, charges for uncollectibility of the aggregate financial system totaled 1.3% of assets, increasing 0.3 p.p.i.y.

Administrative expenses of the banks as a whole represented 6.2% y/y of assets in October, 0.2 p.p. higher than last month. In the accumulated ten months of 2018, such expenditures reached 6.3% of assets, 0.8 p.p. less in a year-on-year comparison.

Regulations

Summary of the main regulations of the month, implemented by the BCRA, related to financial intermediation activity. The date of publication of the standard is taken as a reference.

Communication A6579 – 05/10/18 | The rules on “Time deposits and investments” are adapted, reducing to 30 days the term for the option of early cancellation of non-transferable nominative certificates in pesos corresponding to holders of the public sector.

Communication A6586 – 12/10/18 | The rules on “Minimum capital of financial institutions” are modified, increasing to the equivalent in pesos of €1 million the maximum exposure limit for an MSME to be framed as a retail portfolio. The rules on “Liquidity Coverage Ratio” modify the conditions of unsecured wholesale funding provided by MSMEs, establishing that the total aggregate funding must be less than the equivalent amount in pesos of €1 million.

Communication A6589 – 19/10/18 | The rules on “Authorization and composition of the capital of financial institutions” are adapted, increasing to $10 million the amount from which second-degree public banks can take time deposits. The requirement that these public banks be entities oriented to medium- and long-term financing for productive investment and foreign trade is abolished.

References

1 For more details, see Press Release.

2 Reference is made to those measures adopted since the date of publication of the previous Report on Banks.

4 Communication A6605. The “B” preferred guarantees are constituted by the rights in rem over assets or commitments of third parties that, reliably instrumented, ensure that the entity will be able to dispose of the funds as a cancellation of the obligation contracted by the client, previously complying with the procedures established for their execution.

5 Communication A6599. In line with the BCBS standard “Supervisory framework for measuring and controlling large exposures”.

6 Throughout the Report, the series are deflated using a consumer price index (CPI). As of 2017, the CPI of national coverage prepared by INDEC is taken into account (in October 2018 it presented a monthly variation of 5.4% and 45.9% year-on-year). Until December 2016, the index calculated from the CPIs of the City of Buenos Aires, San Luis and Córdoba weighted according to the National Household Expenditure Survey corresponding to the period 2004-2005 is being worked on.

7 Considering balance sheet differences.

8 The nominal peso-dollar exchange rate fell 11.5% between the peak of the month.

9 The balance of UVA deposits – in the public and private sectors – almost doubled in October, although they still represent only 1% of total deposits.

10 The effect of the reduction in the nominal peso-dollar exchange rate observed in the month had an impact on the composition of funding measured in national currency, mainly with a reduction in the weighting of the components in foreign currency and an increase in that of the segments in pesos.

11 This participation is in line with what has been observed in the balances of time deposits in the private sector in pesos in recent months (with data as of September, this participation represented 64.7% of deposits for individuals and 35.3% for legal entities).

12 An increase of 3 p.p. in the reserve ratios on deposits in pesos, which can be integrated with LELIQ, was provided, and the possibility of integrating the total marginal reserve requirement – corresponding to the net increase – of time deposits in pesos with LELIQ.

13 In addition, as of October, financial institutions have the possibility of using their cash balances in pesos not affected by the interbank clearing to purchase Cash Clearing Notes (NOCOM). See Communication A6575 and Communication B11760.

14 Excludes principal adjustments and accrued interest. If these concepts are incorporated, the monthly fall in credit in pesos to the private sector would be 5.6% in real terms (-0.5% nominal).

15 Variation in currency of origin. It does not include principal adjustments or accrued interest. If these concepts are incorporated, the monthly decrease in credit in foreign currency would reach 0.7%.

16 Excludes principal adjustments and accrued interest. If these concepts are incorporated, the year-on-year fall in credit in pesos to the private sector would be 10% in real terms.

17 Variation in currency of origin. It does not include principal adjustments or accrued interest. If these concepts are incorporated, the monthly decrease in credit in foreign currency would reach 6.7%.

18 Information extracted from the Central Debtors (includes both national and foreign currency). Loans to residents abroad are not included. Adjustments in principal and accrued interest are considered. Business financing is defined here as that granted to legal entities and commercial financing granted to individuals. On the other hand, loans to families are considered to be those granted to individuals, unless they are for commercial purposes.

19 The wholesale peso-dollar exchange rate (Com. “A” 3500) went from $40.9 at the end of September to $36.2 at the end of October. In this context, part of the monthly fall in corporate credit is explained by the re-expression of foreign currency balances at the new exchange rate.

20 Adjustments of principal and accrued interest are considered.

21 The value of the UVA is that corresponding to the last business day of October.

22 Includes capital and adjustment of capital for the evolution of the CER.

23 Includes transactions at a fixed and repacable interest rate.

24 According to the debtor’s tax domicile.

25 Equity exposure to the private sector is defined as the ratio of the private sector’s irregular portfolio net of total forecasts to the private sector and the consolidated net worth of the aggregate financial system.

Glossary

%a.: annualized percentage.

% YoY: Year-on-year percentage.

Liquid assets: availabilities (integration of “minimum cash” in current accounts at the BCRA and in special guarantee accounts and other concepts, mainly cash in banks and correspondent offices) plus the net credit balance for transfer operations of financial institutions against the BCRA using LEBAC and NOBAC.

Consolidated assets and liabilities: those arising from deducting transactions between entities in the system.

Net Assets (NA): Assets and liabilities are net of accounting duplications for pass-through, forward and spot transactions to be settled.

APR: Total Risk Weighted Assets.

BCBS: Basel Committee on Banking Supervision (BCBS).

Irregular portfolio: portfolio in situation 3 to 6, in accordance with the “Classification of Debtors” regime.

Credit to the public sector: Position in public securities (without LEBAC or NOBAC) + Loans to the public sector + Compensation to be received + Debt securities and Certificates of participation in financial trusts (with underlying public securities) + Miscellaneous credits to the public sector.

Credit to the private sector: loans to the non-financial private sector including accrued interest and CER and CVS adjustment and leasing.

Contribution differences: Results from the monthly update of assets and liabilities in foreign currency. The item also includes the results originated by the purchase and sale of foreign currency, which arise as a difference between the agreed price (net of the direct expenses originated by the operation) and the book value.

Miscellaneous: miscellaneous gains (including, but not limited to, gains on permanent interests, recovered loans and unaffected provisions) minus miscellaneous losses (including, but not limited to, losses on permanent interests, loss on the sale or impairment of goods in use and amortization of business keys).

Equity exposure to counterparty risk: irregular portfolio net of provisions in terms of equity.

Administration expenses: includes remunerations, social charges, services and fees, taxes and amortizations.

IEF II-17: BCRA Financial Stability Report.

IPCBA: Consumer Price Index of the City of Buenos Aires.

CSF: Liquidity Coverage Ratio (LCR).

LEBAC and NOBAC: bills and notes issued by the BCRA.

LELIQ: BCRA liquidity bills.

LR: Leverage Ratio (LR).

Financial margin: Income minus financial expenses. It includes interest and securities earnings, CER and CVS adjustments, exchange rate differences and other financial results.

Mill.: Million or million, as appropriate.

IFRS: International Financial Reporting Standards.

ON: Negotiable Obligations.

ORI: Other comprehensive results.

OS: Subordinated Obligations.

Other financial results: rental income from financial leases, contribution to the deposit guarantee fund, interest on availabilities, charges for loan depreciation, premiums for the sale of foreign currency and other unidentified items.

PN: Net Worth.

p.p.: percentage points.

SME: Small and Medium Enterprises.

Consolidated profit: Results from permanent holdings in local financial institutions are eliminated. Available since January 2008.

Income from securities: includes results from public securities, temporary shares, negotiable obligations, subordinated obligations, options and other credits for financial intermediation. In the case of public securities, it includes the results accrued in terms of income, differences in share price, exponential increase based on the internal rate of return (IRR) and sales, in addition to the charge for forecasts for the risk of impairment.

Interest income: interest charged minus interest paid for financial intermediation, following the accrual criterion (balance sheet information) and not what is received. It includes interest on loans and deposits of government securities and premiums for passes.

Result for services: commissions charged minus commissions paid. It includes fees related to obligations, credits, securities, guarantees granted, the rental of safe deposit boxes and foreign and exchange operations, excluding in the latter case the results from the purchase and sale of foreign currency, the latter being accounted for in the “Differences in quotation” account. Expenses include commissions paid, contributions to the ISSB, other contributions for income from services and charges accrued from the gross income tax.

ROA: Final result as a percentage of net assets. In the case of referring to accumulated results, the average of the NA for the reference months is considered in the denominator.

SWEE: Final result as a percentage of equity. In the case of referring to accumulated results, the average net worth for the reference months is considered in the denominator.

RPC: Computable Patrimonial Liability. For more details, see Ordered Text “Minimum Capitals of Financial Institutions”.

TNA: Annual nominal rate.

US$: US dollars.

UVA: Unit of Purchasing Value.

ICU: Housing Units.

Share on