I. Recent measures1

In order to generate a firmer control of liquidity in the money market – essential to minimize volatility in the foreign exchange market and reinforce the anti-inflationary commitment – the BCRA recently adopted a set of measures2. On the one hand, bank reserve requirements were increased in stages (3 p.p. as of June 21, an additional 3 p.p. as of July 2 and 2 p.p. more since July 18) for demand and time deposits – both in pesos – with certain exceptions such as those denominated in UVA. Part of this increase may be integrated through National Treasury Bonds in pesos at a fixed rate maturing in November 2020 valued at market price. On the other hand, the limit of the positive net global position of foreign currency computed in daily balances was reduced from 10% to 5% of the computable equity liability (CPR) or liquid capital (whichever is lower) of the entities.

To give dynamism to the secondary market of National Treasury Bills in Foreign Currency (Letes in dollars), the requirements for financial institutions to acquire these instruments in the secondary marketwere relaxed 3. Financial institutions were authorized to increase their net global position in foreign currency above 5% admitted and up to 30% of their RPC, as long as the excess is integrated with dollar Letes.

In order to facilitate financing for micro, small and medium-sized enterprises (MSMEs), the BCRA recently implemented a series of measures aimed at strengthening the credit channel and reducing the level of interest rates applied to this segment, without neglecting the prudential criteria recommended by the Basel Committee4. In particular, the minimum capital requirement that entities must have integrated if the funds are channeled to MSMEs was relaxed. In addition, reserve allowances linked to credit lines for MSMEs and the “Ahora 12” plan were increased. Additionally, the current limit of 15% of the Computable Patrimonial Liability (RPC) was eliminated to consider a preferred guarantee to the discount of documents. In this way, banks will be able to apply lower forecasts to this type of operation.

In order to continue strengthening the security measures of the financial system, in June it was established that the transporters of securities must have a comprehensive process for the management of the risk of committing crimes – which involves their identification, evaluation, monitoring, control and mitigation – to safeguard the integrity of people, as well as the values transported. considering, among other aspects, the amounts to be transported, the distances to be traveled, and the geographical areas in which it will be operated5.

II. Activity

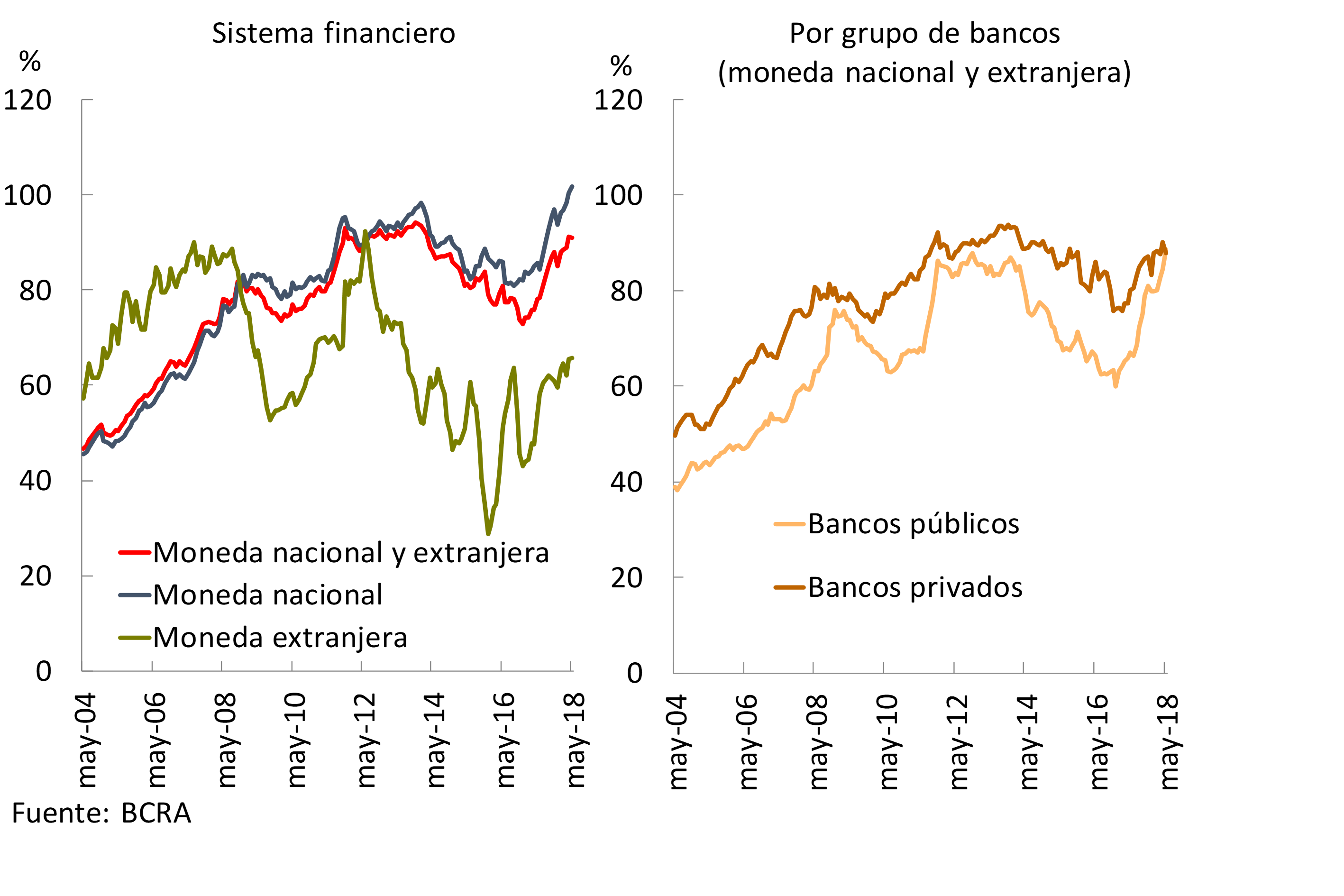

In May, the growth rate of banks’ financial intermediation with the private sector moderated. As in recent months, the ratio between loans and deposits in pesos in the private sector increased during the period (see Graph 1). When considering the items in domestic and foreign currency, loans to companies and families accounted for 91% of private sector deposits. In this context, in May the net assets of the financial system increased 2.8% in real terms and accumulated an increase of 20.9% year-on-year (y.o.y.).

Graph 1 | Loans in Deposit Terms – Balance Sheet Balances – Private Sector

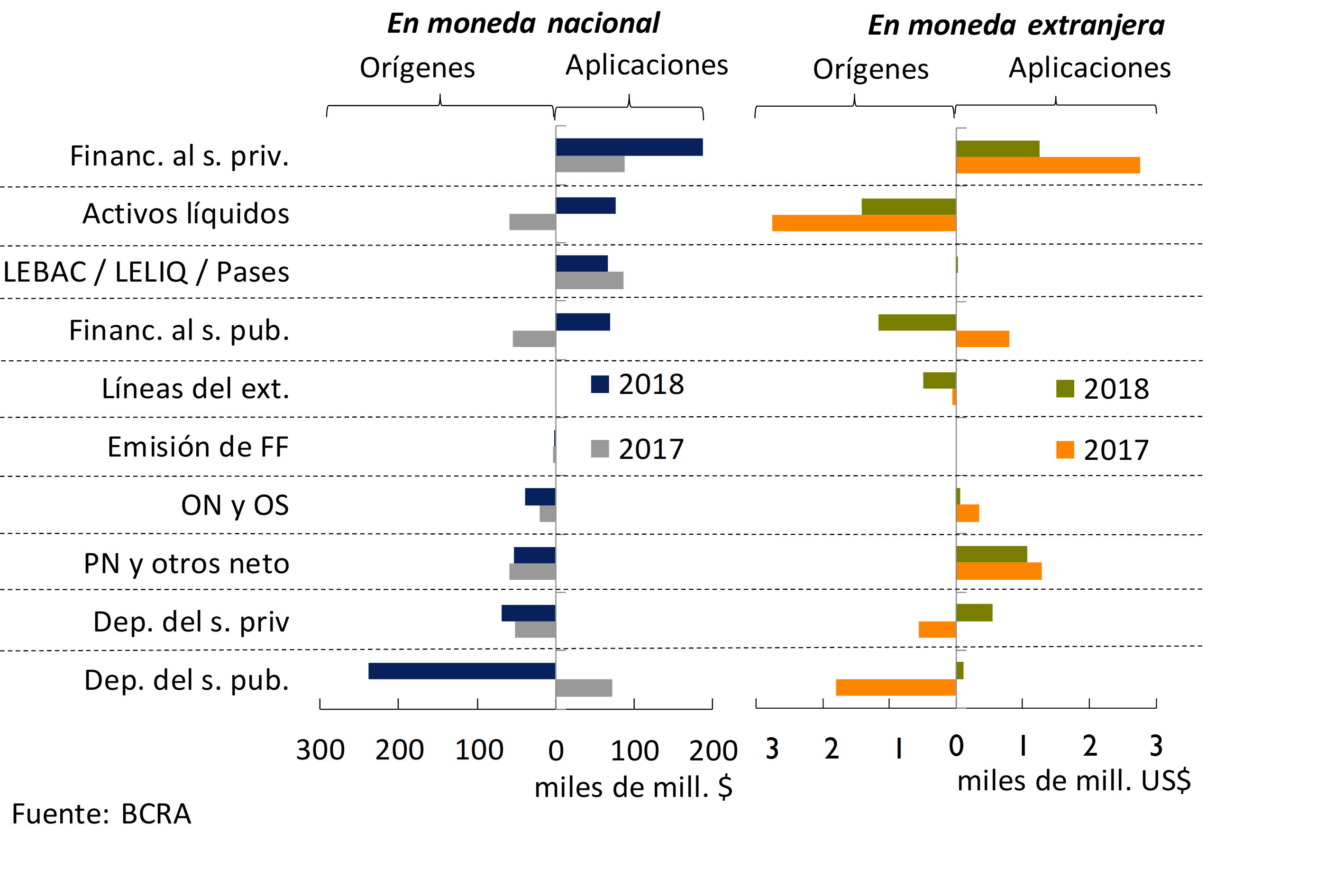

Taking into account the estimate of the flow of funds6 per currency for the banks as a whole, in May the increases in deposits from the public and private sectors were the main sources of funds in pesos. These resources in national currency were used to increase financing to the private sector and the balance of liquid assets. On the other hand, considering the monthly flow of funds from the financial system in foreign currency, the reduction in liquid assets (source of resources) and private sector deposits (application of funds) were the main movements in May.

In relation to the flow of funds in national currency for the first 5 months of the year, the increase in public sector deposits ($237,000 million) was the main source of resources (see Graph 2). In addition, the increase in private sector deposits and the placement of negotiable obligations (ON) were other sources of funding highlighted in the period. These resources were used to increase financing to the private sector ($188,000 million) and the balance of liquid assets ($77,000 million). The increase in the holdings of monetary regulation instruments and financing to the public sector were other uses of funds so far in 2018. On the other hand, according to the flow of funds for items denominated in foreign currency, the reduction in liquid assets (US$1,400 million) and the increase in credit to the private sector (US$1,300 million) were the most relevant origin and application of funds so far this year, respectively.

Graph 2 | Estimated Cash Flow for the First 5 Months – Financial System – By Source Currency

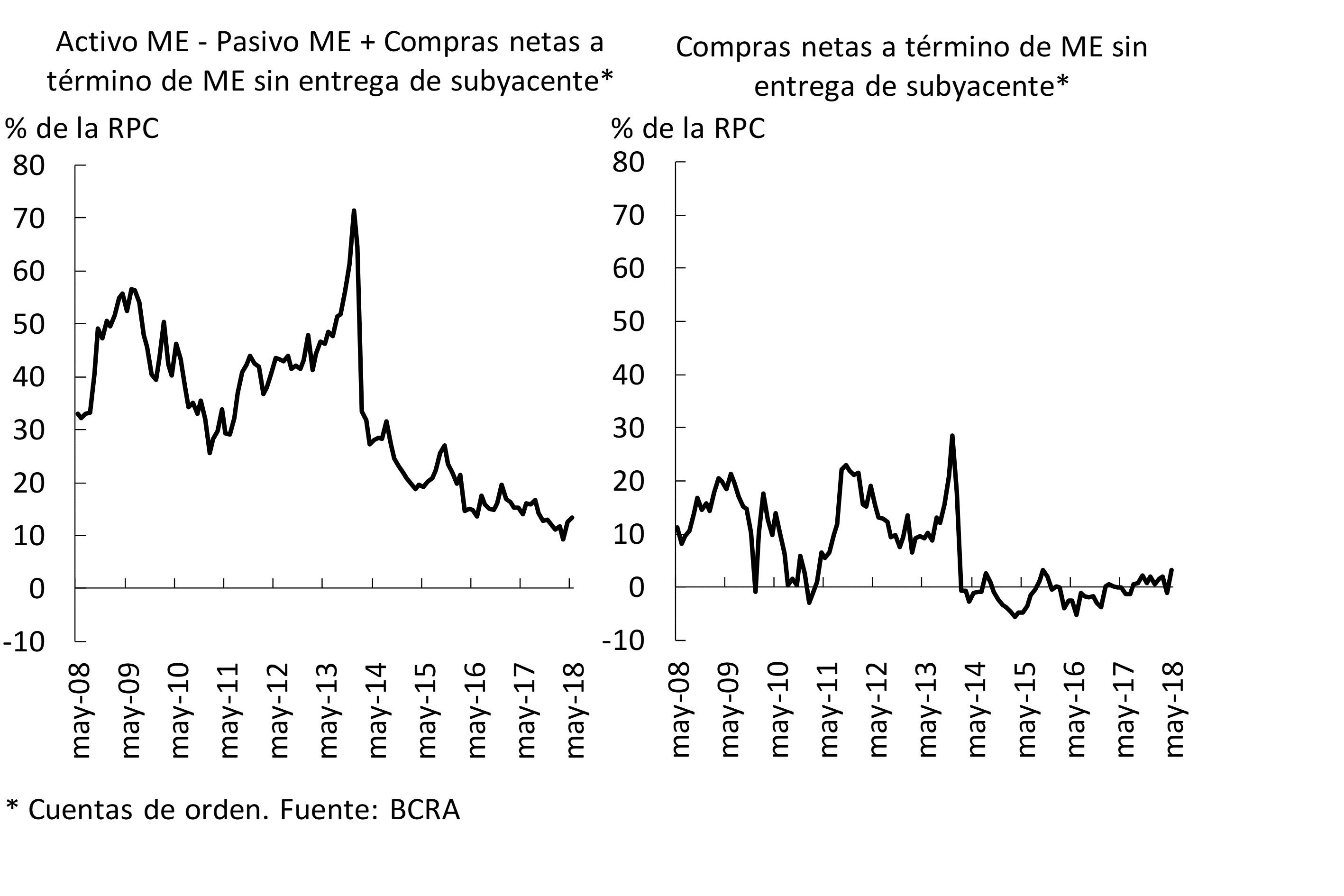

Considering the different equity mismatches to which the financial system is exposed, in May the difference between assets and liabilities in inflation-adjusted pesos was around 43% of the computable equity liability (CPR), 2.1 p.p. more than the level of April. For its part, the foreign currency mismatch of the banks as a whole was equivalent to 13.3% of the PRC in the month, 0.8 p.p. more than in April. The monthly increase in this indicator was explained by the forward operations of foreign private banks and by the effect of the increase in the exchange rate. In a year-on-year comparison, this indicator fell by 0.6 p.p. of the PRC, remaining in a range of low values (see Graph 3).

Graph 3 | Foreign Currency Mismatch of the Financial System

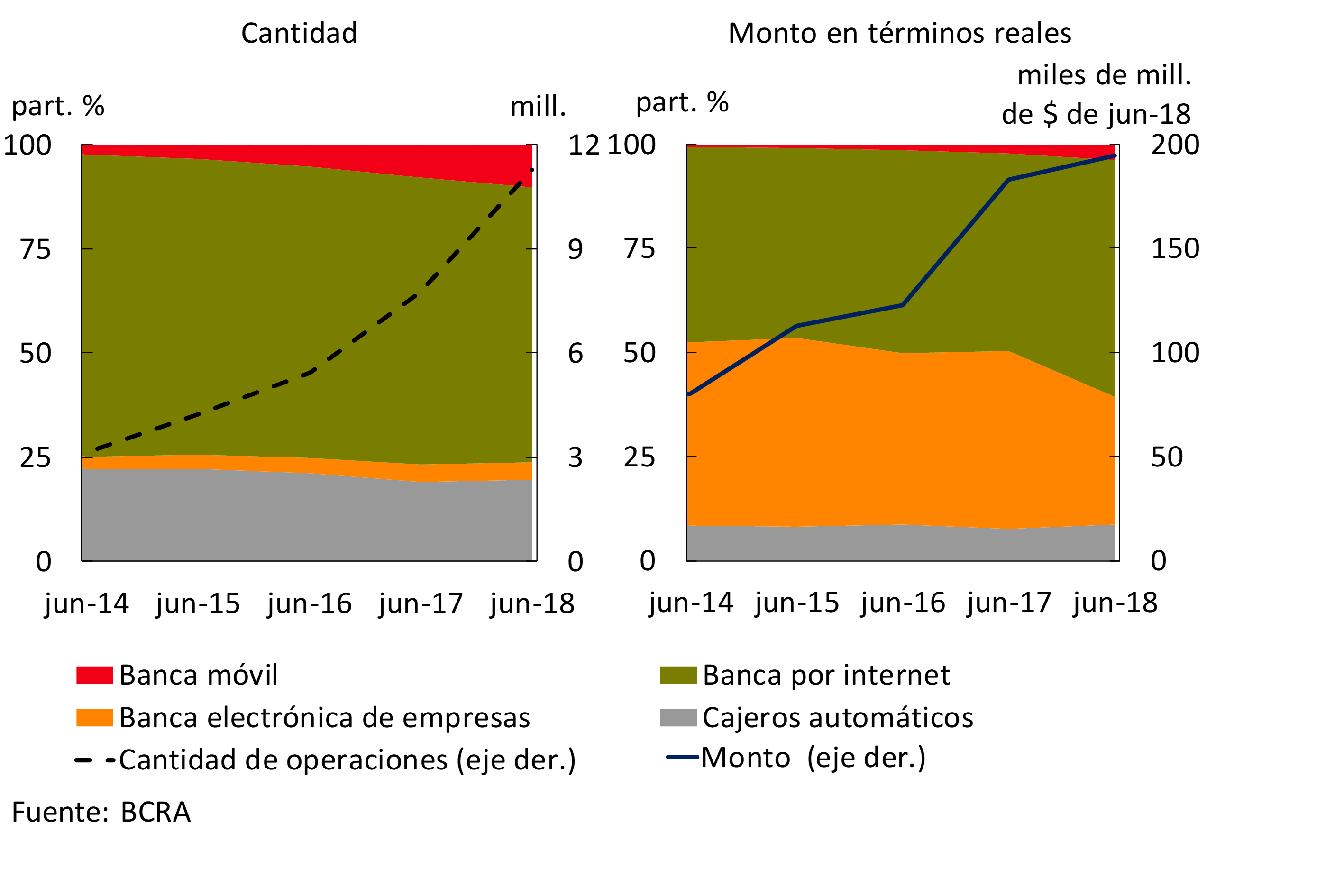

In relation to the operations of the payment system, transfers of funds to third parties continued to grow, mainly driven by those of immediate credit. The latter type of operations increased 6.2% YoY in real values and 45.3% YoY in quantity as of June (latest information available). As for the channels through which immediate transfers are made, the use of mobile platforms is gradually gaining participation (see Graph 4), to the detriment of those channeled via ATMs and internet banking. Thus, 10.3% of immediate transfers made during June were made through mobile banking.

Figure 4 | Immediate Channel Transfers of Funds

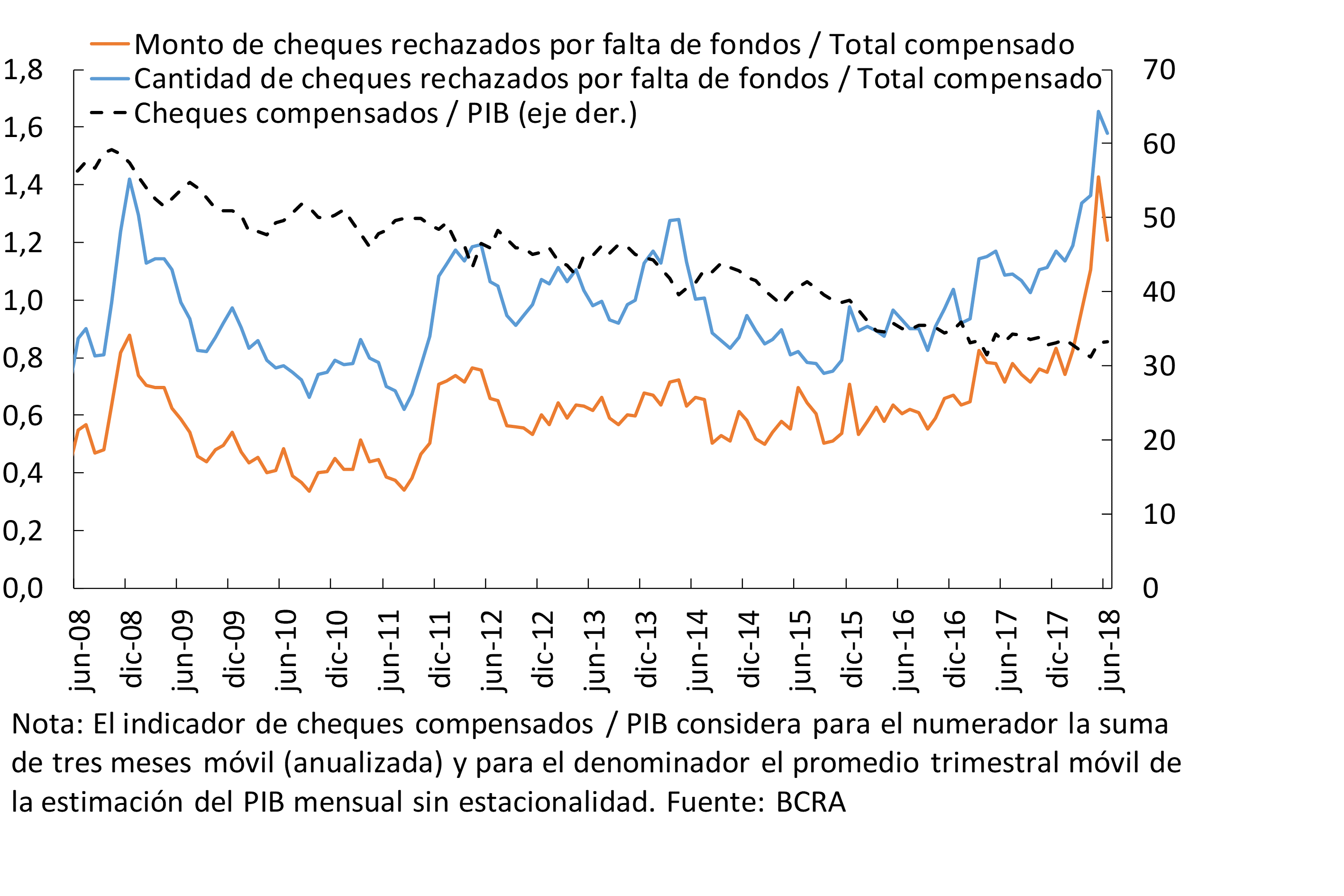

For its part, the amount of cleared checks continued to show a decrease in terms of the size of the economy measured by GDP (see Graph 5). In this context, the ratio of rejected cheques due to lack of funds increased in May and then decreased during the month of June, standing at around 1.21% for amounts issued and 1.58% for amounts.

Graph 5 | Cleared and Bounced Checks

III. Deposits and liquidity

In the month, the total balance of deposits in national currency did not show any changes in real terms with respect to April (-0.2%), reflecting an increase in public sector accounts (1.2%) and a decrease in private sector placements (-0.9%). This last movement was made up of a fall in demand accounts (-2.7%), partially offset by an increase in time deposits (+1.4%). Meanwhile, deposits in foreign currency of the private sector fell 2.6% monthly – in currency of origin.

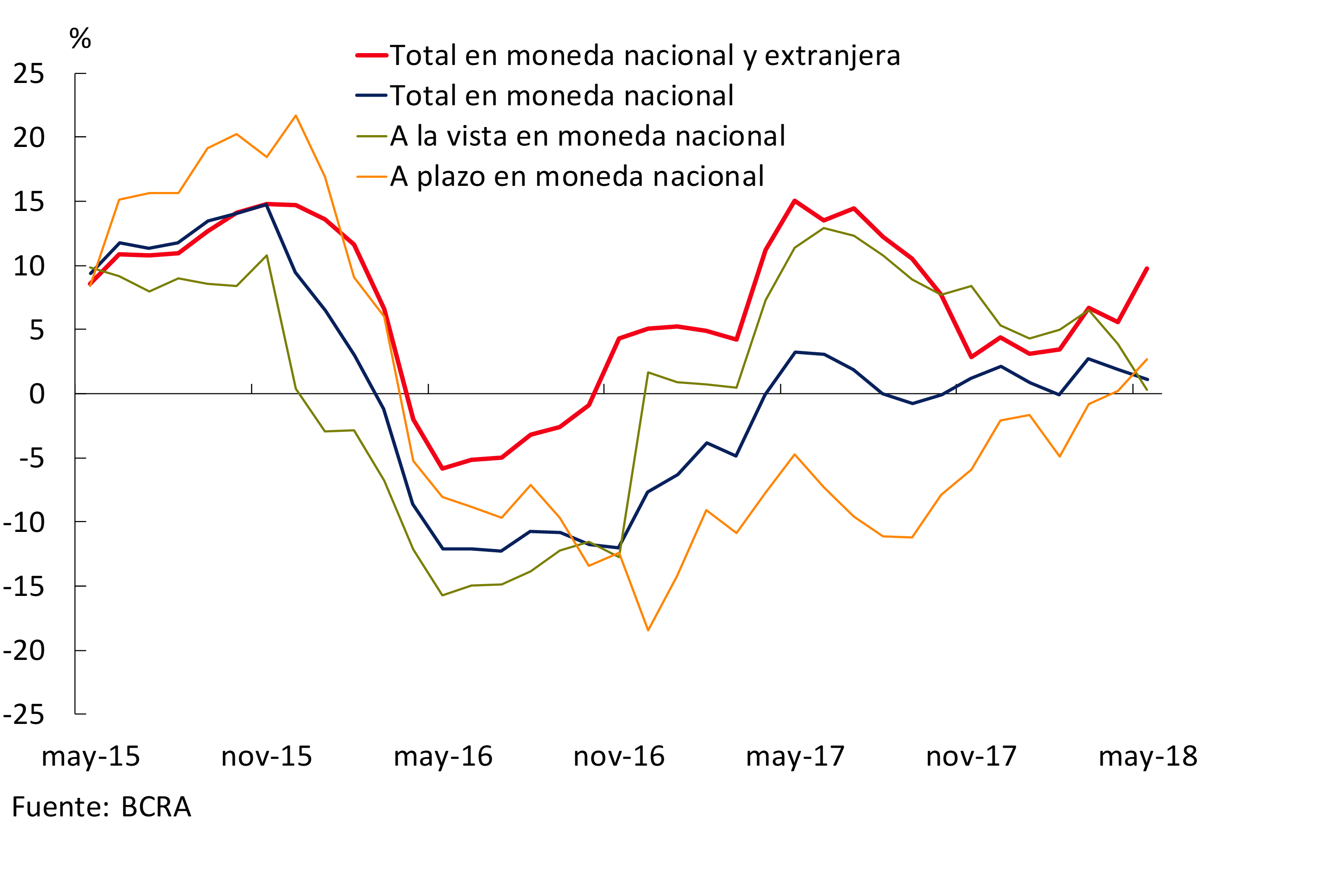

In year-on-year terms, total deposits in national currency in the banks as a whole grew 11.3% adjusting for inflation. Public sector deposits drove this increase (+46.8% real YoY), while private sector placements showed no significant changes (+1.2% Real YoY). Within the latter segment, time deposits grew relatively more year-on-year than demand accounts, a situation that had not been observed since the beginning of 2016 (see Chart 6). For their part, foreign currency deposits of the private sector grew 12.3% – in source currency – in the last twelve months.

Graph 6 | Total Private Sector Deposits – Var. A.I. of the balance in real terms

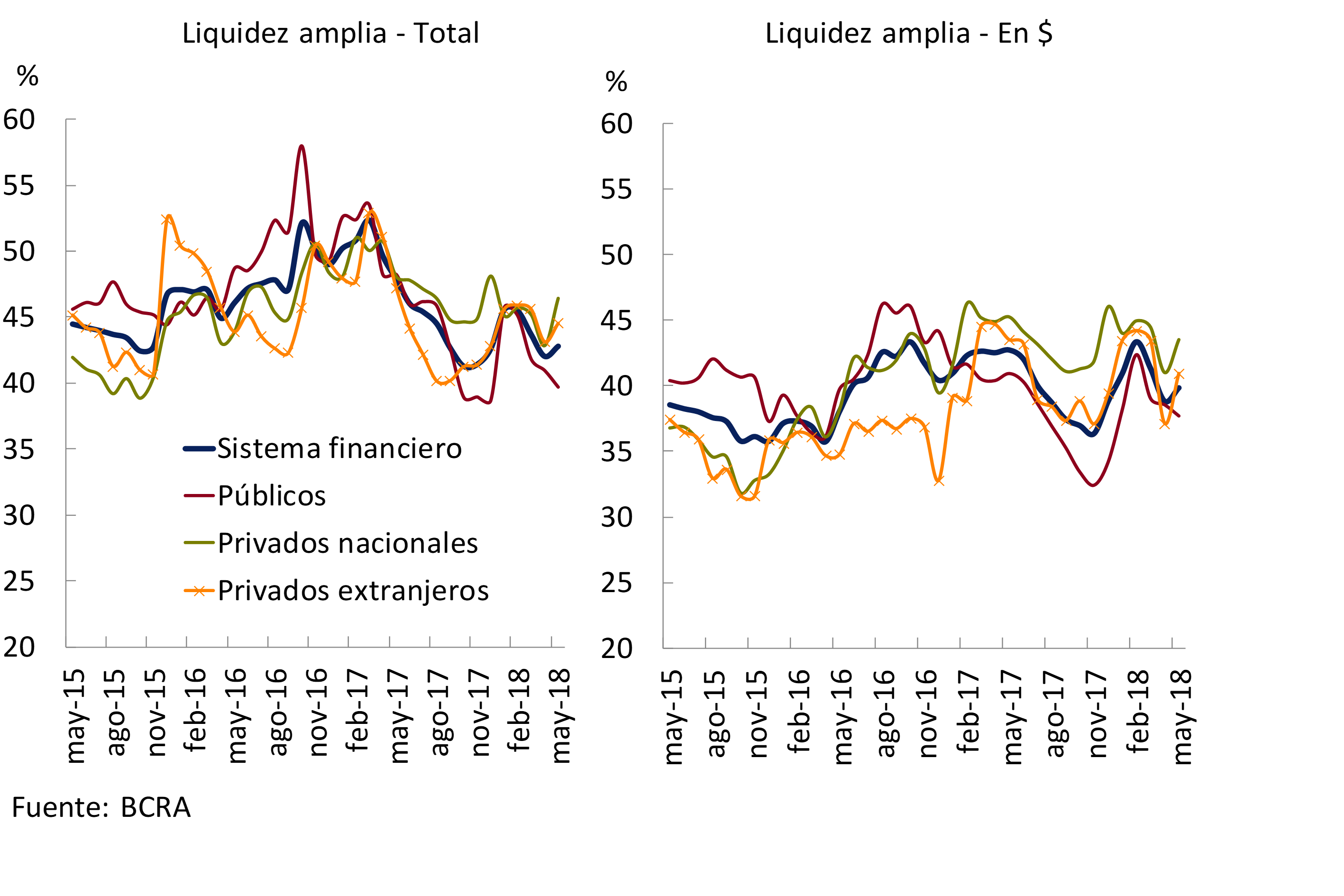

In May, the broad liquidity indicator – in domestic and foreign currency, including monetary regulation instruments – of the financial system totaled 42.8% of total deposits (39.9% in peso items), increasing 0.8 p.p. (1 p.p.) compared to last month. This increase was driven by private banks (see Figure 7). The greater liquidity was due to the increase in the accounts that banks have in the BCRA. It should be remembered that in mid-May a change in the minimum cash rule7 came into force, which established a quarterly period (May/July) for the calculation of the requirement and integration. In this context, the strictest indicator of liquidity – in domestic and foreign currency, taking into account only the balance of availabilities and current accounts at the BCRA in terms of deposits – increased by 1.4 p.p. of deposits to around 26%.

Figure 7 | Ample Liquidity of the Financial System

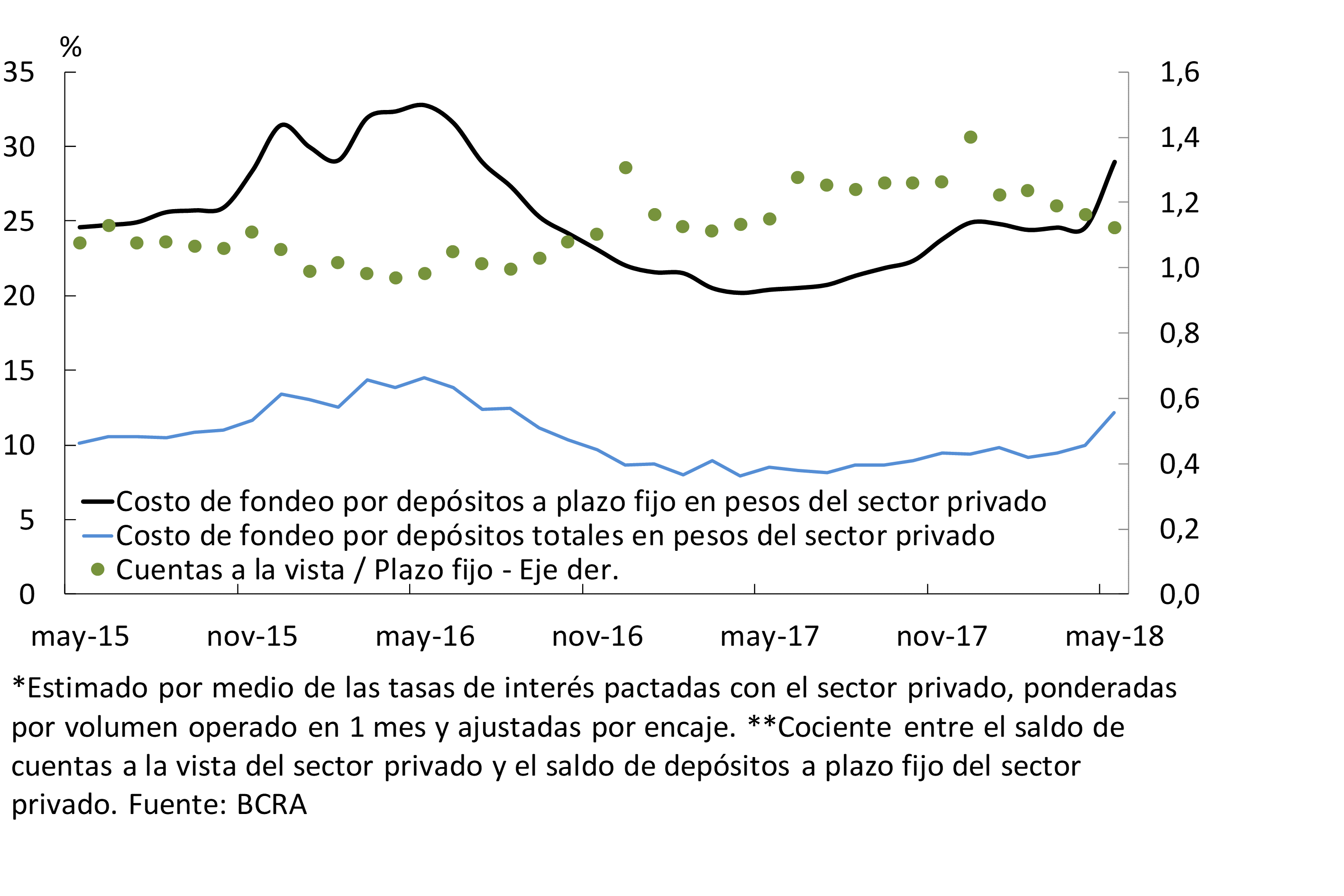

In line with the monetary policy interest rate hike established by the BCRA throughout May – a process that began at the end of April – the return that banks offered for fixed-term deposits increased 3.4 p.p. in the month, to 25.6%. In this context, and given the greater weighting of time deposits in total private sector deposits in pesos, the total funding cost for private sector deposit operations in national currency increased compared to April (see Chart 8).

Figure 8 | Estimated Funding Cost for Private Sector Deposits in Pesos* and Ratio between Demand and Time Deposits**

IV. Financing

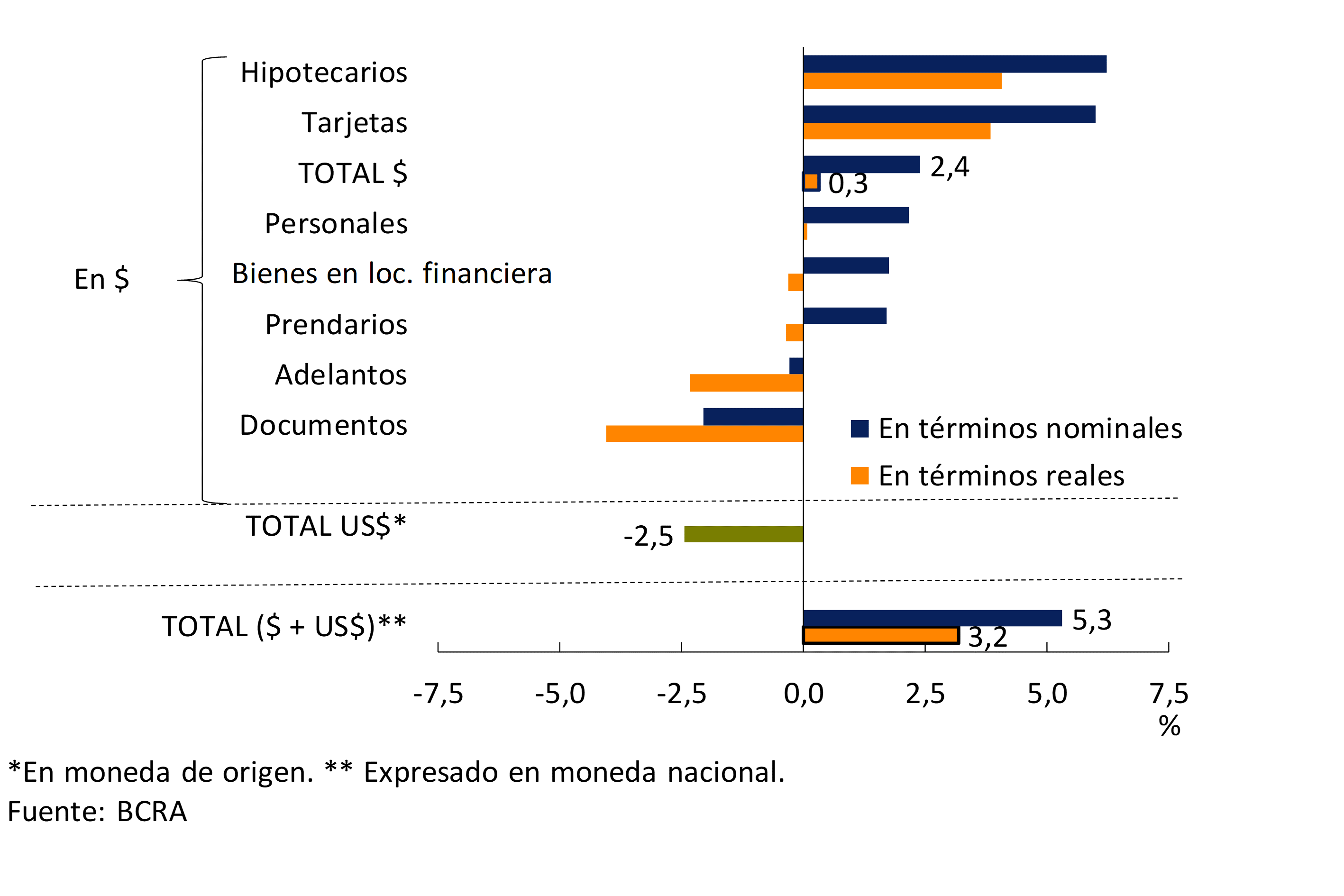

In May, the balance of financing in pesos from banks to the private sector in real terms remained practically unchanged compared to April (+0.3%). In this segment, monthly increases were recorded in mortgages, cards and personal loans (see Graph 9), which were offset by decreases in the remaining credit lines. On the other hand, in the period, loans in foreign currency fell by 2.5% – in the currency of origin – mainly explained by the performance of pre-financing for exports. Considering the total balance of credit to the private sector expressed in pesos (of items denominated in both domestic and foreign currency), this concept verified a monthly increase of 3.2% in the balance adjusted for inflation8.

Figure 9 | Total Credit Balance to the Private Sector – Monthly % Change – May 2018

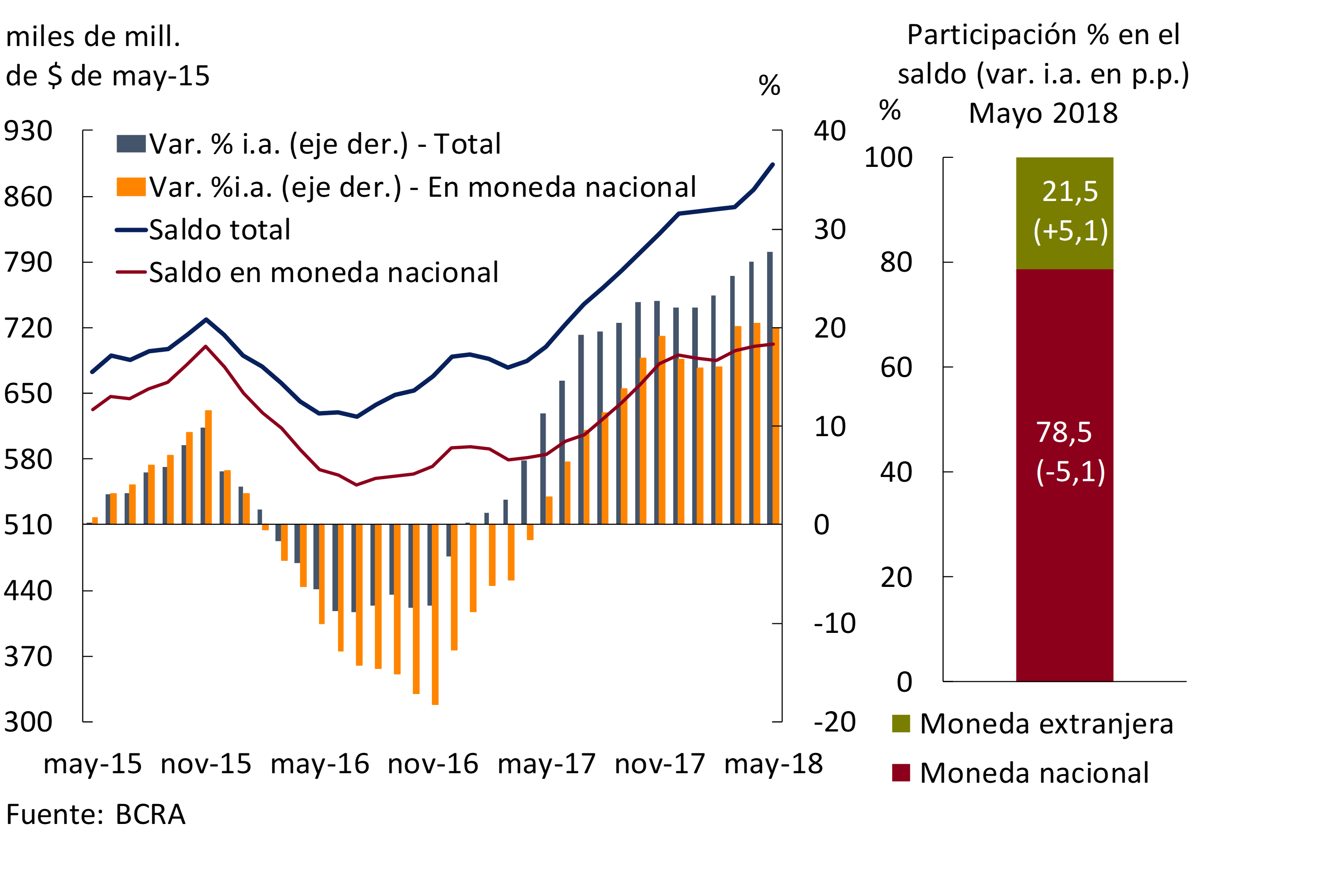

In a year-on-year comparison, loans in pesos to the private sector grew by 20% in real terms (see Graph 10), slightly lower than the variation recorded in April. On the other hand, foreign currency lines accumulated a growth of 36.7% y.o.y. in May, increasing their share of the total credit balance to the private sector by 5.1 p.p. in the last year, to a level of 21.5%. In this context, the balance of total financing to the private sector increased by 27.7% YoY in real terms. Loans with real collateral (mortgages and pledges) continued to show the greatest relative year-on-year dynamism (see Chart 11).

Figure 10 | Total Credit Balance to the Private Sector in Real Terms

Figure 11 | Total Credit Balance to the Private Sector

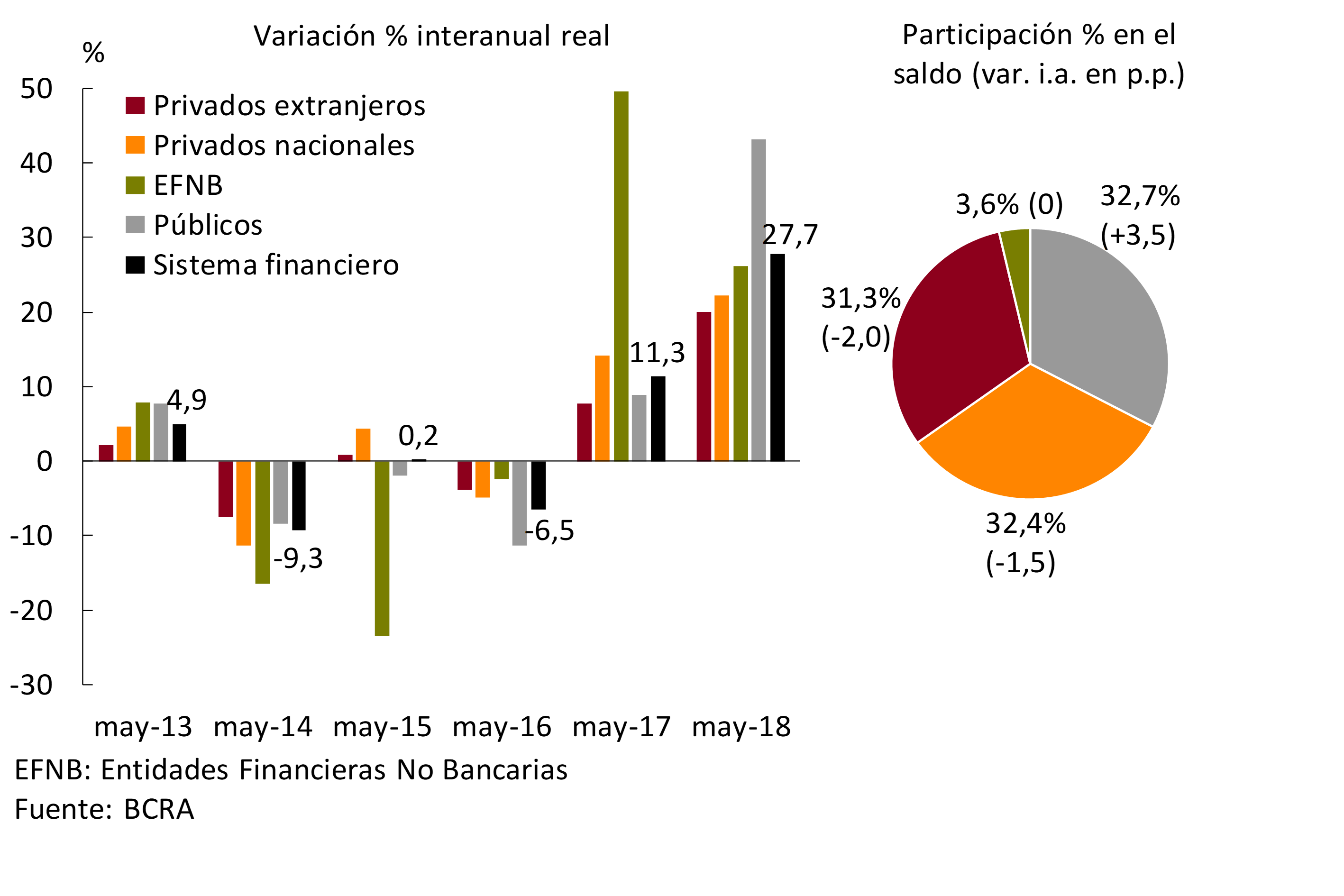

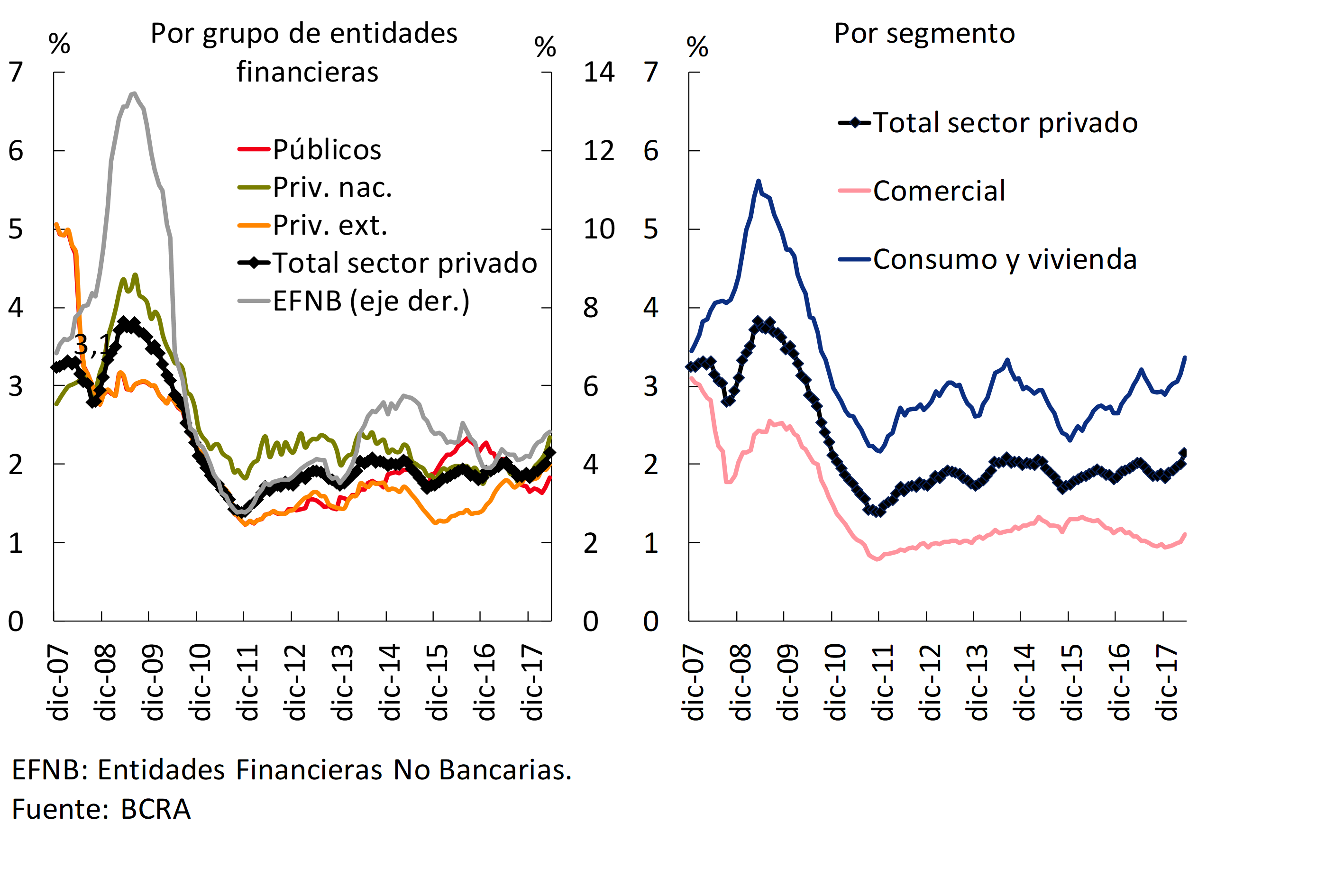

In May, the real year-on-year increase in total financing to companies and households was widespread among all groups of financial institutions. In particular, loans to the private sector channeled by public banks showed the highest relative real increase, equivalent to 43.1% as of May (see Chart 12). In this way, this group of banks increased its proportion in the balance of total loans to the private sector to 32.7%, to the detriment of private banks.

Figure 12 | Total Credit Balance to the Private Sector – By Group of Financial Institutions

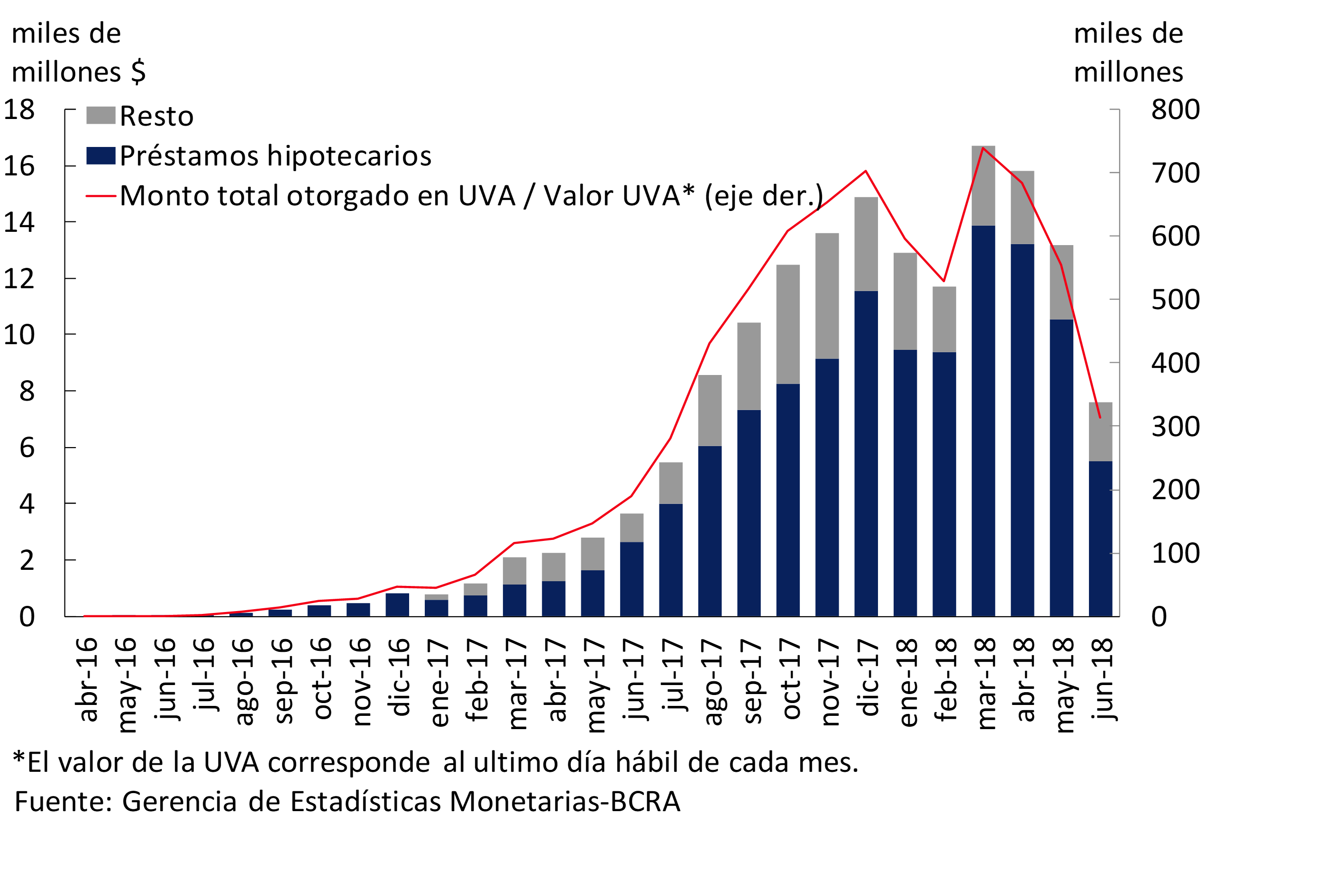

In June, the volume of loans to the private sector in UVA totaled more than $7,600 million, down from previous months (see Chart 13). 72.6% of the amount traded corresponded to mortgage loans. According to the latest available information, in May, 8.7% of the total balance of financing to the private sector corresponded to UVA lines —almost $173,300 million9—. In particular, the balance of mortgage loans in UVA to companies and families in the financial system stood at $128,980 million (65.6% of the total balance of mortgage lines).

Figure 13 | UVA Financing – Amounts Granted

Nominal interest rates operating with companies and families in national currency10 increased in May in almost all lines of credit. The monthly performance was mainly explained by private banks and, to a lesser extent, by public banks. Also the average interest rates operated in UVA for mortgages, personal and pledges increased slightly compared to April.

In May, the irregularity ratio of credit to the private sector stood at 2.1%, slightly above last month’s value and the level of a year ago. It should be considered that the current levels of delinquency are moderate, both in relation to the record of the last 10 years (average of 2.2%, see Graph 14), and in a comparison with the countries of the region. According to the latest available information (IMF Financial Soundness Indicators), credit delinquencies in Brazil amount to 3.5%, in Colombia to 4.7%, in Chile to 2%, Peru 4.7%, Uruguay 2.4%. Disaggregated by segment at the local level, the NPL ratio for consumer and housing credit increased slightly in the month, to 3.4%. For its part, the non-performing loan ratio of commercial loans stood at 1.1% in the period, just above the value of April and in line with the record of a year ago. In the period, the balance of accounting forecasts of the financial system represented 126% of loans in an irregular situation, reducing both in a monthly and year-on-year comparison.

Figure 14 | Irregularity of Credit to the Private Sector

V. Solvency

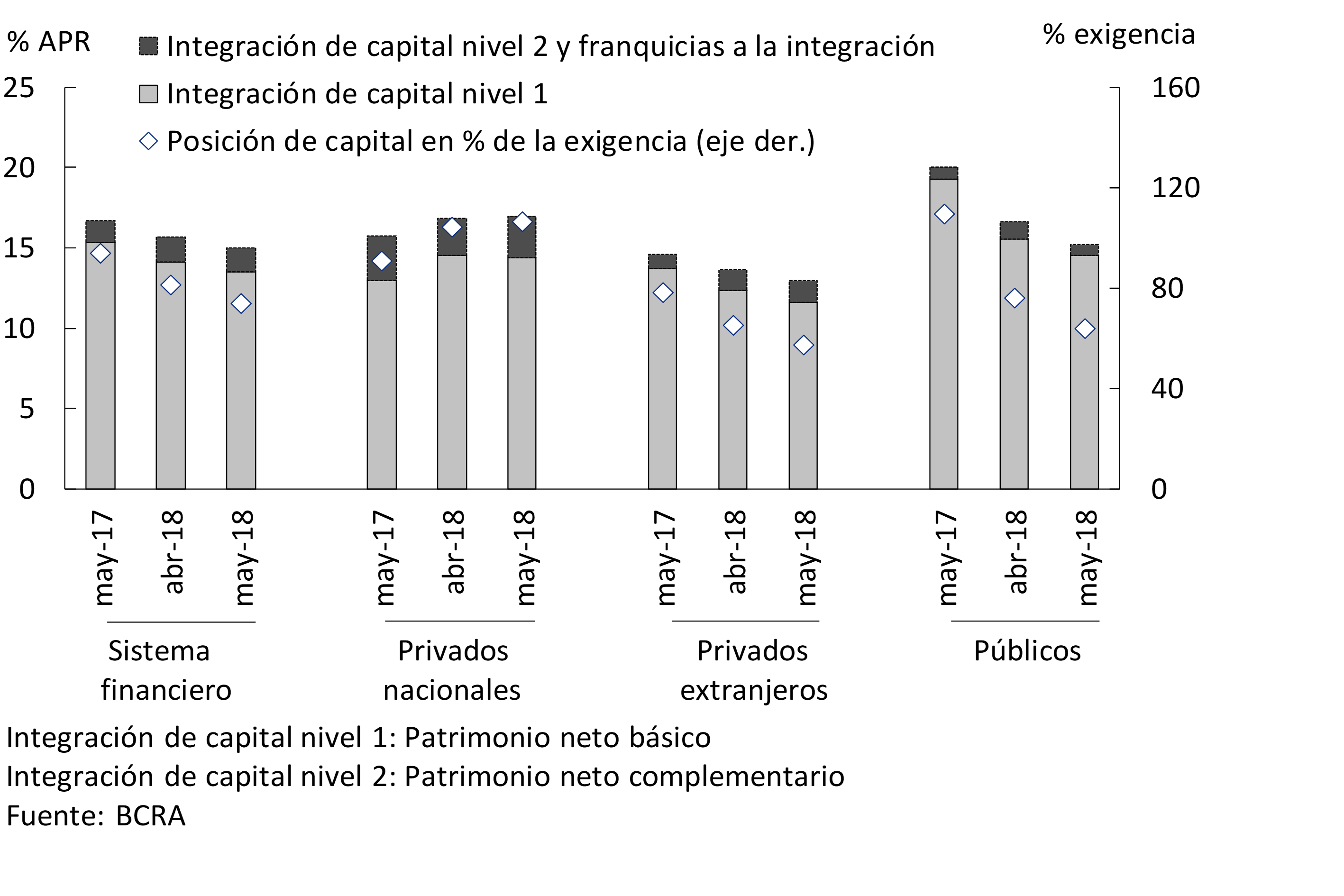

From high levels, in May the solvency indicators of the financial system were slightly reduced. The monthly increase in capital was relatively smaller than the increase in risk-weighted assets (RWAs) and the increase in the minimum regulatory requirement. For the aggregate of financial institutions, regulatory capital integration accounted for 15% of RWAs in the month (see Chart 15). Tier 1 capital, with the greatest capacity to absorb losses, totaled 13.5% of RWAs. For its part, the regulatory capital position – excess integration – stood at 74% of the minimum regulatory requirement. The net worth of the consolidated financial system grew in real terms by 0.8% compared to April and by 19.7% in the last twelve months. The monthly increase was mainly explained by the profits accrued, being tempered by the decision to distribute dividends by some banks.

Figure 15 | Integration and Excess Regulatory Capital (Position)

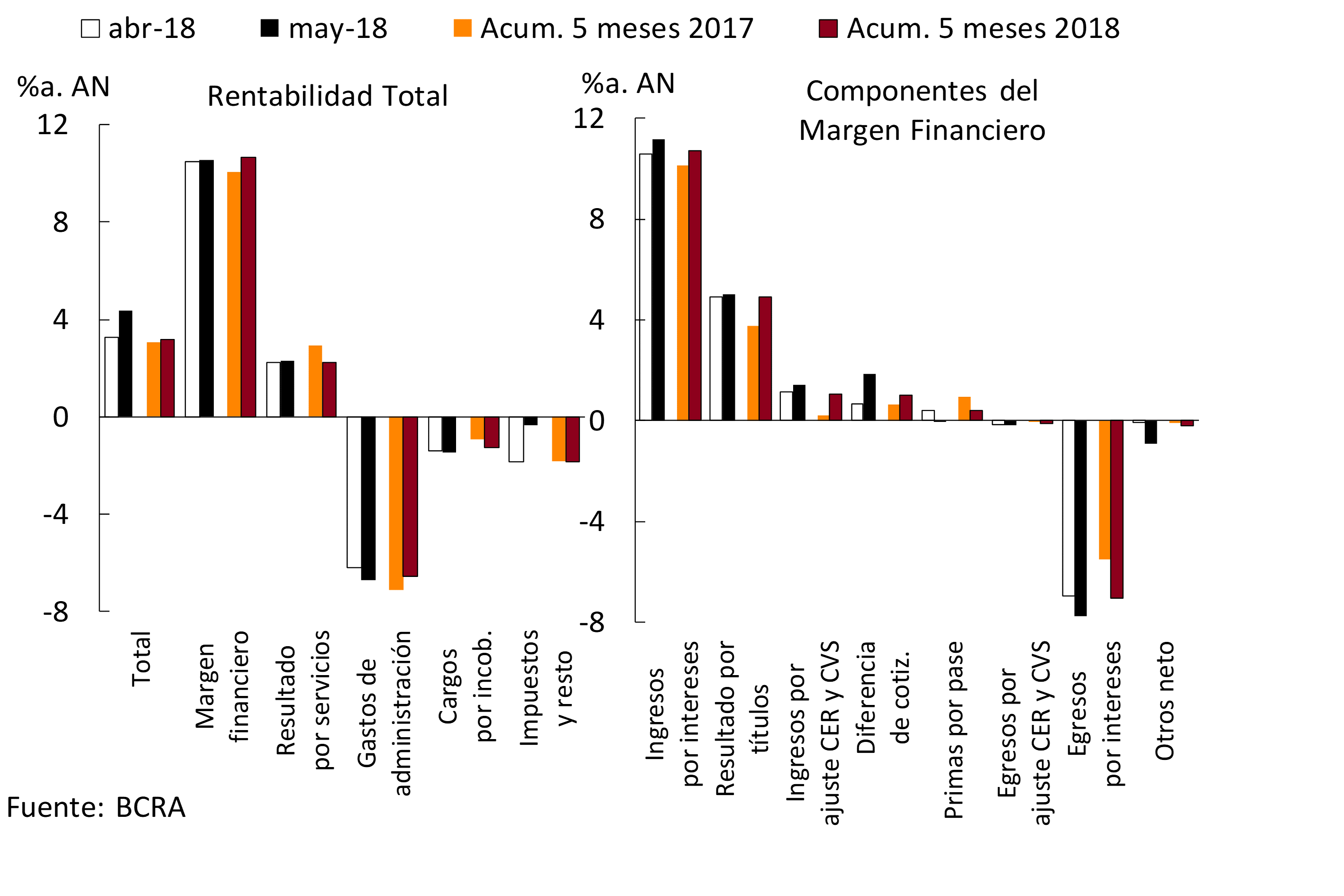

The monthly earnings accrued in May by the financial system totaled 4.4% annualized (y) of assets (37% y. of net worth -ROE), increasing 1.1 p.p. compared to last month (see Chart 16). This increase was mainly explained by the effect of the increase in the nominal exchange rate on the balance sheet of all entities, reflected in greater differences in the share price of private banks and an increase in the gains recorded in “other comprehensive income” (ORI) in public banks11. In May, private banks obtained profits of 3.8% y/y of assets (+1.1 p.p. compared to April), while public banks recorded profits of 5.3% y/y of assets (+1.3 p.p. compared to April).

Figure 16 | Income Statement by Financial Institution Group

In the first five months of the year, the financial system accrued profits of 3.2% of assets or 26.4% of net worth, with no significant changes in a year-on-year comparison.

In May, the financial margin totaled 10.6% of assets, slightly higher than in April. The increase was mainly driven by higher share price differences, higher interest income and CER12 adjustment results, effects partially offset by an increase in interest expenses and a decrease in pass premiums (see Chart 17). Considering the cumulative figure for the first five months of 2018, the financial margin represented 10.6% of assets, being 0.6 p.p. higher than in the same period of 2017. The year-on-year increase was due to higher gains on securities, CER13 adjustments, interest income and share price differences. These variations were partially offset by an increase in interest expenses and a reduction in pass premiums.

Figure 17 | Components of the Income Table – Financial System

Net income from services in the financial system represented 2.3% of assets in May, increasing slightly compared to April. In five months of 2018, these results by services represented 2.2% of assets, falling 0.7 p.p. in a year-on-year comparison (see Chart 17).

On the expenditure side, in the month charges for uncollectibility represented 1.5% of assets, slightly higher than those of April. Between January and May 2018, bad debt charges accounted for 1.3% y/y of assets, 0.3 p.p. higher in a year-on-year comparison (see Chart 17). In May, administrative expenses totaled 6.7% y/y of assets, increasing 0.5 p.p. compared to April. In the first five months of the year, administrative expenses reached 6.6% of assets, 0.5 p.p. less in a year-on-year comparison.

Regulations

Summary of the main regulations of the month, implemented by the BCRA, related to financial intermediation activity. The effective date of the regulation is taken as a reference.

Communication A6501 – 04/05/18

As of 05/07/18, the limit of the positive net global position of foreign currency was reduced to 10% of the computable equity liability or liquid equity, whichever is lower, and it is established that its measurement must be carried out on a daily basis.

Communication A6504 – 08/05/18

The rules on “Net global position of foreign currency” are modified, admitting an excess with respect to the limit to the positive net global position that financial institutions verify as of 05/07/18, which may not exceed its position in National Treasury Bills in U.S. dollars, both measured on that date. This excess must be recalculated daily, reducing the negative difference registered by the aforementioned position between the day of calculation of the net global position of foreign currency and that verified on 05/07/18.

Communication A6507 – 10/05/18

It is provided that for the calculation of the limits provided for in the rules on “Net global position of foreign currency”, the balances must be converted into pesos at the reference exchange rate at the end of the month prior to the calculation of this relationship.

Communication A6508 – 14/05/18

The rules on “Minimum cash” are modified, unifying the calculation of the position for the months of May, June and July 2018, and eliminating the minimum daily integration for the month of May.

Communication A6517 – 24/05/18

Adjustments are introduced to the rules on “Authorization and composition of the capital of financial institutions”, providing that the promoters and founders of financial institutions and those who, directly or indirectly, exercise their control, may not have their income concentrated, directly or indirectly, in more than 75% in concession contracts and/or provision to the national governments. provincial, municipal and the Autonomous City of Buenos Aires. Financial institutions are required to inform the Superintendence of Financial and Exchange Institutions if their shareholders are covered by this provision.

References

1 Reference is made to those measures of relevance to the financial system that were adopted since the date of publication of the previous Report on Banks.

2 Communication A6526, Communication A6532, Press Release of 18/06/18 and Press Release of 02/07/18.

3 Communication A6526 and Press Release of 18/06/18.

4 Communication A6531 and Press Release of 28/06/18.

6 Based on balance sheet balance.

8 This variation is mainly explained by the re-expression in pesos of the balance of loans in foreign currency, within the framework of the monthly increase in the peso-dollar exchange rate.

9 Includes capital and adjustment of capital for the evolution of the CER.

10 It includes a fixed and repacable interest rate.

11 Fundamentally associated with the exchange difference due to the conversion of financial statements of foreign business carried out by a bank of magnitude.

12 This concept is made up of an increase in income, partially offset by higher expenditures.

13 Same as previous article.

Glossary

%a.: annualized percentage.

% YoY: Year-on-year percentage.

Liquid assets: availabilities (integration of “minimum cash” in current accounts at the BCRA and in special guarantee accounts and other concepts, mainly cash in banks and correspondent offices) plus the net credit balance for transfer operations of financial institutions against the BCRA using LEBAC and NOBAC.

Consolidated assets and liabilities: those arising from deducting transactions between entities in the system.

Net Assets (NA): Assets and liabilities are net of accounting duplications for pass-through, forward and spot transactions to be settled.

APR: Total Risk Weighted Assets.

BCBS: Basel Committee on Banking Supervision (BCBS).

Irregular portfolio: portfolio in situation 3 to 6, in accordance with the “Classification of Debtors” regime.

Credit to the public sector: Position in public securities (without LEBAC or NOBAC) + Loans to the public sector + Compensation to be received + Debt securities and Certificates of participation in financial trusts (with underlying public securities) + Miscellaneous credits to the public sector.

Credit to the private sector: loans to the non-financial private sector including accrued interest and CER and CVS adjustment and leasing.

Contribution differences: Results from the monthly update of assets and liabilities in foreign currency. The item also includes the results originated by the purchase and sale of foreign currency, which arise as a difference between the agreed price (net of the direct expenses originated by the operation) and the book value.

Miscellaneous: miscellaneous profits (including, but not limited to, gains on permanent shares, recovered loans and unaffected provisions) less miscellaneous losses (including, but not limited to, losses on permanent shareholdings, loss on sale or disposal of goods for use and amortization of business keys).

Equity exposure to counterparty risk: irregular portfolio net of provisions in terms of equity.

Administration expenses: includes remunerations, social charges, services and fees, taxes and amortizations.

IEF II-17: BCRA Financial Stability Report.

IPCBA: Consumer Price Index of the City of Buenos Aires.

CSF: Liquidity Coverage Ratio (LCR).

LEBAC and NOBAC: bills and notes issued by the BCRA.

LELIQ: BCRA liquidity bills.

LR: Leverage Ratio (LR).

Financial margin: Income minus financial expenses. It includes interest and securities earnings, CER and CVS adjustments, exchange rate differences and other financial results.

Mill.: Million or million, as appropriate.

IFRS: International Financial Reporting Standards.

ON: Negotiable Obligations.

ORI: Other comprehensive results.

OS: Subordinated Obligations.

Other financial results: rental income from financial leases, contribution to the deposit guarantee fund, interest on availabilities, charges for loan depreciation, premiums for the sale of foreign currency and other unidentified items.

PN: Net Worth.

p.p.: percentage points.

SME: Small and Medium Enterprises.

Consolidated profit: Results from permanent holdings in local financial institutions are eliminated. Available since January 2008.

Income from securities: includes results from public securities, temporary shares, negotiable obligations, subordinated obligations, options and other credits for financial intermediation. In the case of public securities, it includes the results accrued in terms of income, differences in share price, exponential increase based on the internal rate of return (IRR) and sales, in addition to the charge for forecasts for the risk of impairment.

Interest income: interest charged minus interest paid for financial intermediation, following the accrual criterion (balance sheet information) and not what is received. It includes interest on loans and deposits of government securities and premiums for passes.

Result for services: commissions charged minus commissions paid. It includes fees related to obligations, credits, securities, guarantees granted, the rental of safe deposit boxes and foreign and exchange operations, excluding in the latter case the results from the purchase and sale of foreign currency, the latter being accounted for in the “Differences in quotation” account. Expenses include commissions paid, contributions to the ISSB, other contributions for income from services and charges accrued from the gross income tax.

ROA: Final result as a percentage of net assets. In the case of referring to accumulated results, the average of the NA for the reference months is considered in the denominator.

SWEE: Final result as a percentage of equity. In the case of referring to accumulated results, the average net worth for the reference months is considered in the denominator.

RPC: Computable Patrimonial Liability. For more details, see Ordered Text “Minimum Capitals of Financial Institutions”.

TNA: Annual nominal rate.

US$: US dollars.

UVA: Unit of Purchasing Value.

ICU: Housing Units.

Share on