About the use of inclusive language in this publication

The use of language that does not discriminate and that makes all gender identities visible is an institutional commitment of the Central Bank of the Argentine Republic. This publication recognizes the influence of language on ideas, feelings, ways of thinking and evaluation schemes.

This document has sought to avoid sexist and binary language. However, for ease of reading, resources such as “@” or “x” are not included.

Executive summary

• At the beginning of 2021, the financial system maintained high liquidity and solvency coverage, in a context in which financial intermediation with the private sector was reduced in part due to the influence of seasonal factors. Despite the performance observed in January, a year-on-year comparison (y.a.) shows real growth rates of the balances in national currency of credit to the private sector and deposits in this sector, reversing the records of the same month in 2020 and 2019.

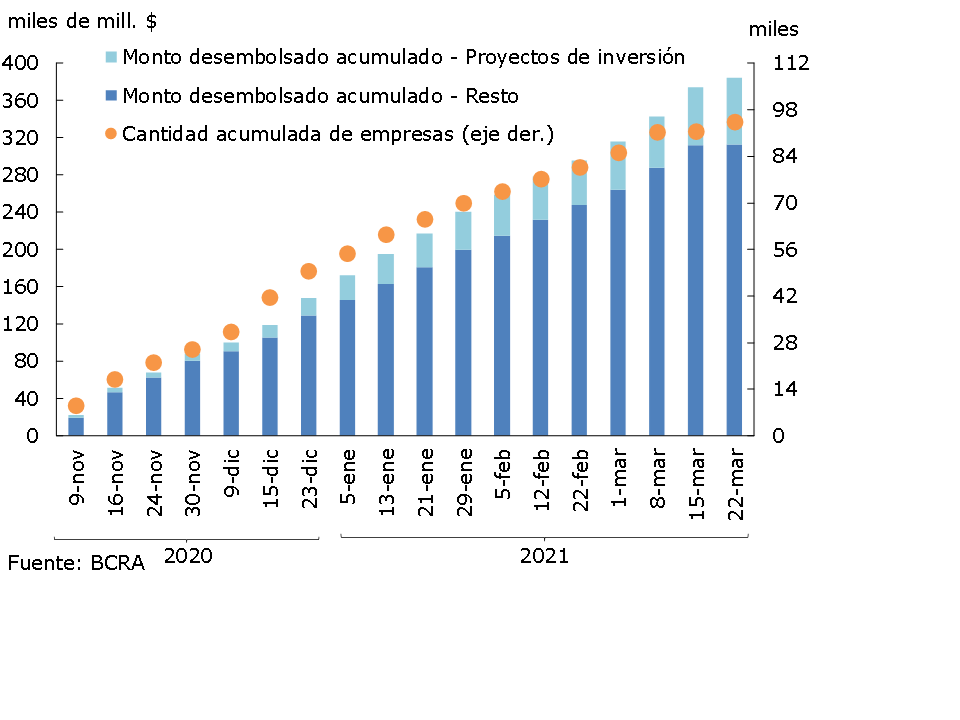

• As usual in the first month of the year, financing to the private sector in national currency fell in real terms, although it accumulated an increase of 10.6% YoY. This year-on-year performance contrasts with what was evidenced in the same month of previous years (-17% YoY and -20.6% YoY in 2020 and 2019, respectively). This year-on-year increase in credit in pesos was generated within the framework of the set of measures promoted by the BCRA and the National Executive Branch aimed at mitigating the adverse economic effects of the pandemic scenario. In this sense, through the Financing Line for Productive Investment (LFIP) of MSMEs, the financial institutions covered generated disbursements of $384,566 million until March 22, 2021 (19% to investment projects), destined for 94,329 companies. In order to continue stimulating credit to MSMEs and contribute to productive investment, economic reactivation and job creation, the validity of this instrument was recently extended, setting a new quota until September 2021 under similar financial conditions.

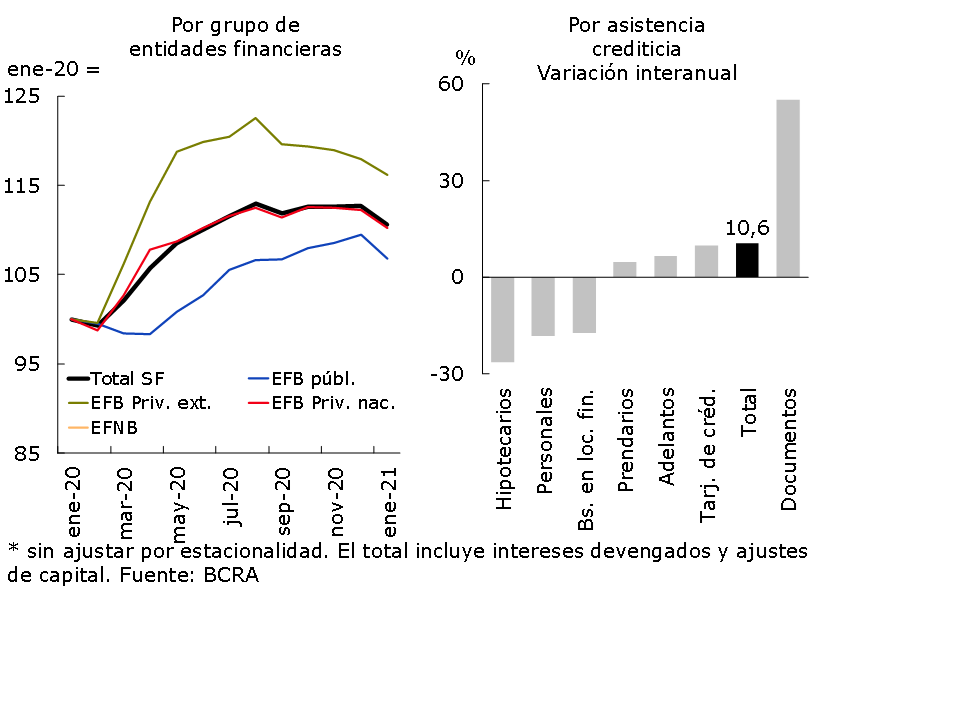

• The irregularity ratio of credit to the private sector for the aggregate financial system continued to fall at the beginning of 2021 to 3.8% (-2.2 p.p. y.o.y.), in a context of the transitory modification on the parameters for classifying debtors and the possibility of transferring unpaid installments at the end of the life of the credit.

• Financial institutions as a whole continued to preserve comfortable levels of forecasting. The forecast balance represented 5.8% of credit to the private sector in January, slightly below the previous month and 0.5 p.p. higher in a year-on-year comparison. The total forecasts in terms of the irregular portfolio stood at 153.2% in the month, accumulating an increase of 65.8 p.p. y.o.y.

• Also following the typical pattern of the beginning of the year, the balance of deposits in pesos of the private sector fell in real terms. This performance was explained by demand accounts, while time deposits in pesos increased in real terms in the period, with an outstanding monthly dynamism in the UVA segment. Given the performance at the beginning of 2021, the real balance of private sector deposits in pesos expanded 23.1% YoY, with increases in both demand and term segments. The year-on-year dynamics of the real balance of deposits in pesos in the private sector also differ considerably from those evidenced at the beginning of previous years (-4.1% YoY in January 2020 and -2.1% YoY in January 2019).

• From high levels compared to recent years, the broad liquidity of the financial system declined slightly in January. The broad liquidity indicator totaled 64.7% of total deposits. This indicator increased by 2.5 p.p. y.o.y.

• At the beginning of the year, the sector’s solvency ratios increased. Capital integration (RPC) of the aggregate of entities totaled 24.4% of risk-weighted assets (RWA) in January, 1.2 p.p. above last December and 3.4 p.p. more than in January 2020.

• In January, the financial system accrued slightly positive comprehensive results in homogeneous currency, lower than those at the end of 2020, thus continuing the trend of gradual decline verified in recent quarters. Comprehensive income in the last twelve months represented 1.9% of assets (ROA) and 12.6% of equity (ROE).

I. Financial intermediation activity

Partly as a reflection of seasonal factors typical of the beginning of the year, in the first month of 2021 the financial intermediation of all entities with the private sector was reduced. In relation to the estimated cash flow in homogeneous currency on the segment of items in pesos,1 the reduction in liquidity in the broad sense and in credit to the private sector were the main sources of resources for the financial system in January. Among the most outstanding fund applications in the month was the decrease in deposits from the private sector and the public sector. 2

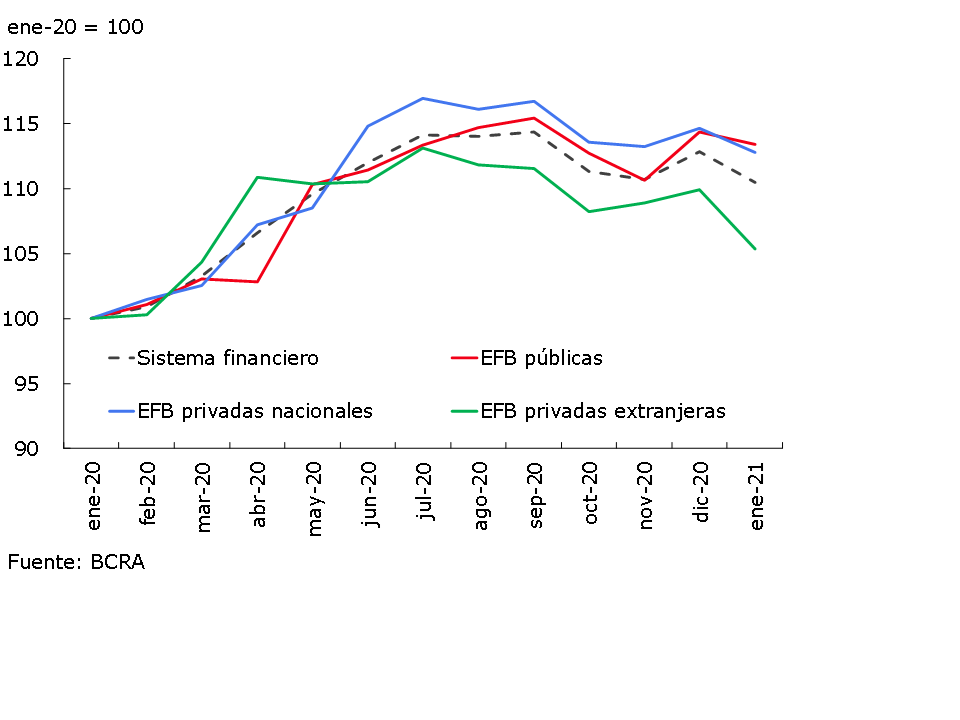

In January, the balance of credit to the private sector in pesos fell 1.9% in real terms between the peak of the month (+2.1% nominal). 3 With the exception of advances and pledges, the monthly decrease in the real balance of financing was verified in all credit assistance. Despite this performance, the year-on-year variation (y.a.) of the real balance of credit in pesos to the private sector continued to be positive and increased at the beginning of 2021, reaching 10.6% at the end of January (well above the year-on-year performances of -17% and -20.6% in the same month of 2020 and 2019 respectively). The year-on-year increase in credit in pesos at the beginning of 2021 was disseminated among the different groups of financial institutions (see Graph 1),4 with greater relative dynamism in foreign private institutions. Among credit assistance, documents had a notable real year-on-year increase within the framework of the boost generated by the BCRA’s measures, while credit cards, advances and pledges also registered positive variations in real terms compared to January 2020.

Graph 1 | Credit to the private sector in pesos

In real terms*

Since the emergence of the COVID-19 pandemic, the BCRA has implemented and promoted different credit assistance to meet the financial needs of the most affected sectors of the population. In relation to credit for smaller companies, the Financing Line for Productive Investment (LFIP) for MSMEs5 became the main financing channel for this segment in the context of the emergency. This line sought a lengthening of the terms of the loans, as well as a certain adequacy of the interest rates with respect to the rates of the previous programs. Through this program, since its implementation and until March 22, 2021, $384,566 million were disbursed, of which 19% corresponded to investment projects (See Graph 2). The number of beneficiary companies has already risen to 94,329. Domestic private banks accounted for the largest disbursements (39% of the total), while the rest were distributed in practically equal parts between public and foreign private banks.

Graph 2 | Financing Line for Productive Investment (LFIP) of MSMEs

It should be noted that, in order to continue stimulating credit to MSMEs to contribute to economic reactivation and job creation, the BCRA recently established a new LFIP quota, maintaining conditions similar to those in force. In particular, for this 2021 quota, the entities reached6 must maintain, between April 1 and September 30, an amount of financing equivalent to 7.5% of the balance of their non-financial private sector deposits in pesos7. 8

In addition, firms enrolled in the “Emergency Assistance Program for Work and Production” (ATP)9 have a line of financing at a subsidized interest rate. With data up to March 22, 20,929 loans were granted through this line for a cumulative amount of $14,240 million. The number of employees who have received part of their salary with these resources amounted to 607,789 since the beginning of the financing program.

People who carry out their activity in the form of self-employed and/or monotributistas have special lines of loans. On the one hand, through the program called “zero-rate credit line”10 since its inception (mid-May 2020) and until March 22, 2021, $66,478 million have been granted. As a result of this program, 249,325 new credit cards were issued, thus being a mechanism that favors financial inclusion. On the other hand, through the program called “line of credit at zero culture rate”11 , $308 million were granted, in a total of 2,924 loans.

In January, credit in foreign currency to the private sector fell by 6% – in the currency of origin. Consequently, the total real balance (in domestic and foreign currency) of financing to the private sector decreased 2.5% compared to last December (-2.1% YoY).

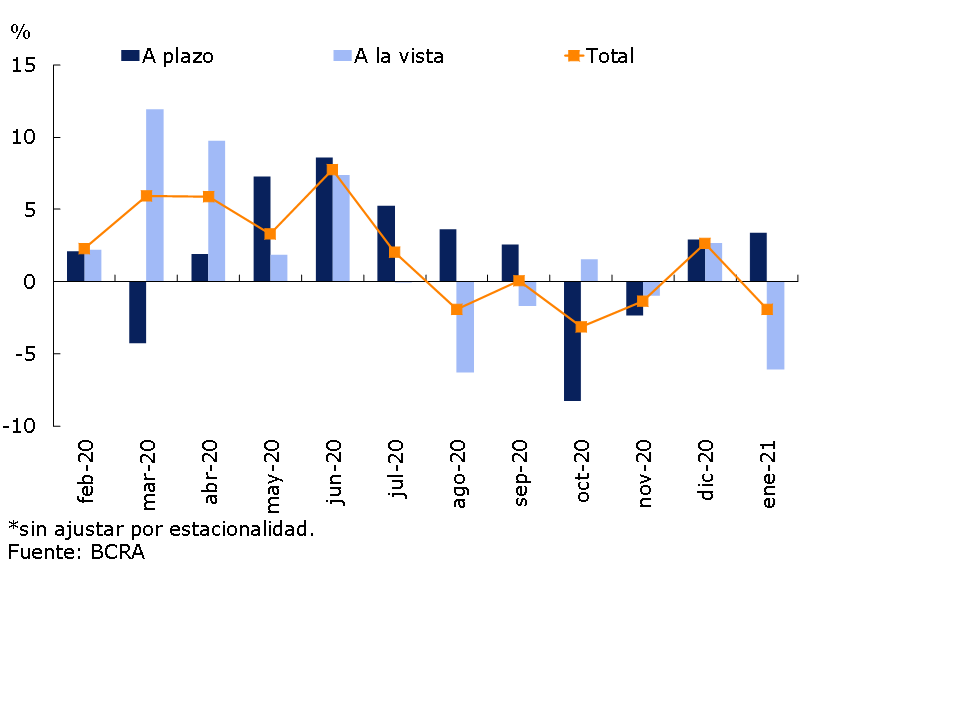

When considering the funding of the financial system, in January the balance of deposits in pesos of the private sector fell by 1.9% in real terms (+2.1% nominal), a variation that was verified within the framework of the seasonality of the period. This performance was explained by demand accounts, which decreased 6.1% in real terms in the month (-2.3% nominal). On the other hand, time deposits in pesos increased 3.4% in real terms in the period (7.6% nominal) (see Chart 3), with a notable monthly dynamism in the UVA segment (+17.4% real for those with early cancellation and 12.7% real for traditional ones).12

Graph 3 | Balance of private sector deposits in pesos

Monthly change – In real terms*

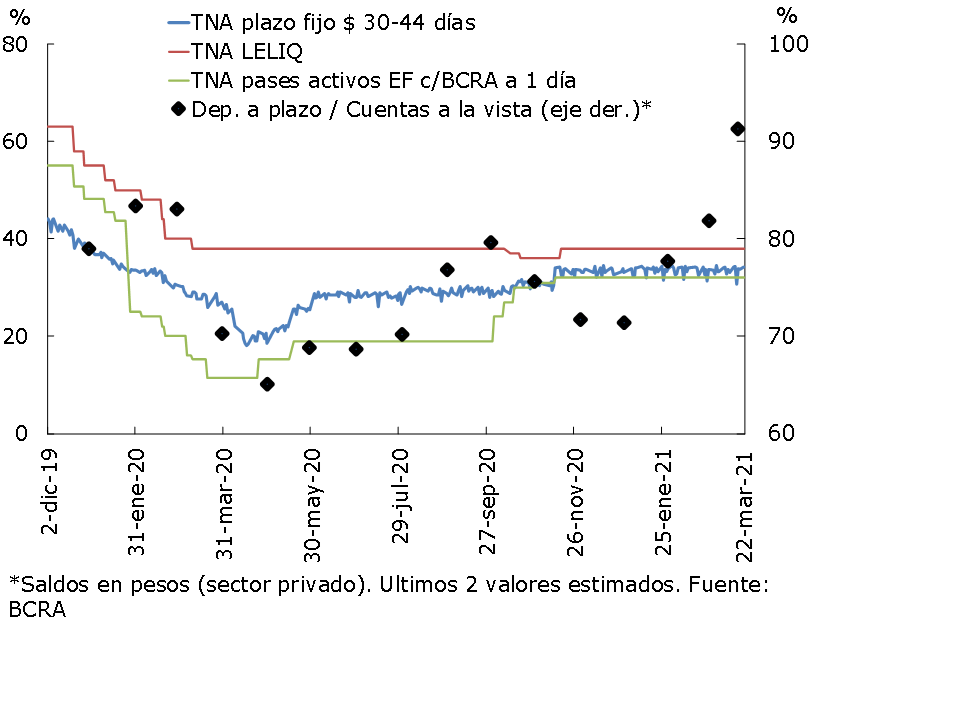

As a reflection of this monthly performance, at the beginning of 2021 the ratio between the balance of time deposits and the balance of private sector demand accounts in national currency increased (see Chart 4) in a context in which monetary policy interest rates remained stable. as well as the nominal passive interest rates operated.

Figure 4 | Interest rates and deposits in pesos*

For their part, private sector foreign currency deposits fell 1.9% – in source currency – in January. Thus, the balance of total private sector deposits (in domestic and foreign currency) decreased by 2% in real terms compared to December, although it accumulated an increase of 13.6% YoY.

Taking into account a year-on-year comparison, the real balance of deposits in pesos in the private sector expanded 23.1% (+70.5% nominal y.o.y.), while the real balance of deposits in the same denomination in the public sector increased 40.8% y.o.y. in real terms (+95.1% y.o.y. nominal). Thus, deposits in total pesos (including the public and private sectors) grew 25.1% YoY in real terms (+73.4% YoY nominal). Finally, the real balance of total deposits in the financial system (all sectors and currencies) increased by 16.3% YoY in January.

II. Aggregate Balance Sheet Composition

In January, the total assets of the financial system fell by 2.1% in real terms (+1.9% nominal), with a similar performance in the different groups of entities (see Chart 5). In a year-on-year comparison, the sector’s assets accumulated an increase of 10.4%, with greater relative dynamism in public and national private banking entities.

Graph 5 | Total Asset Balance

In real terms*

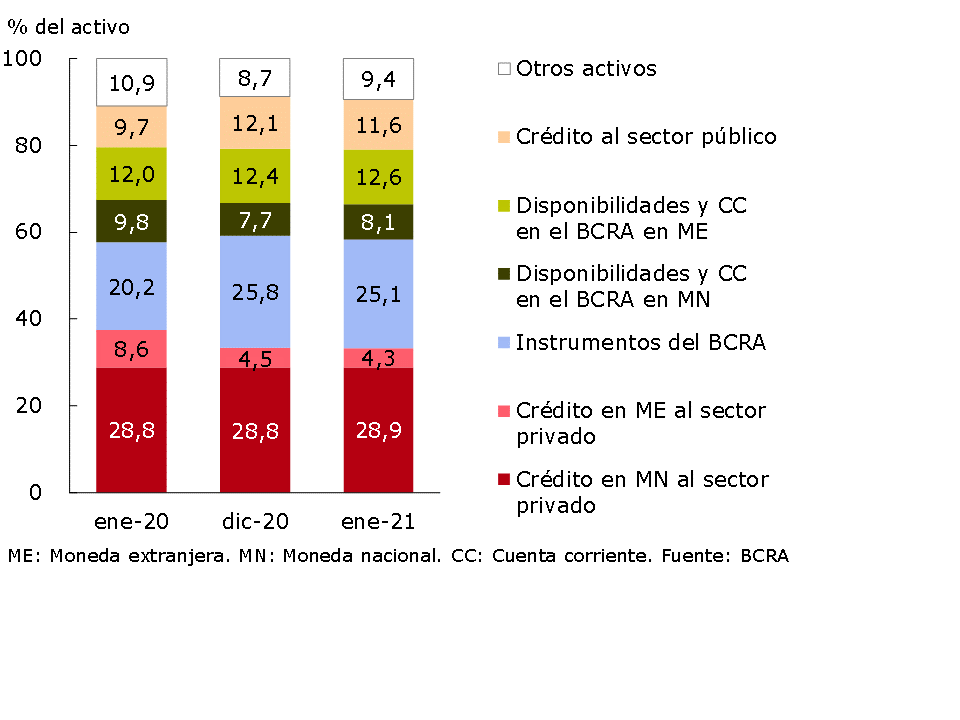

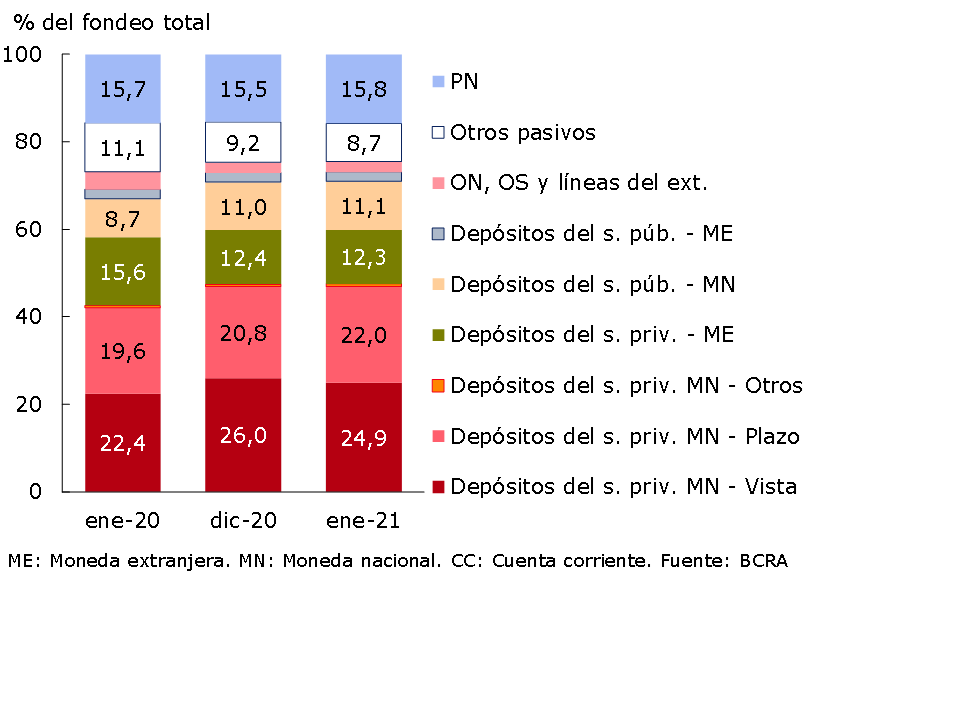

In terms of the components of the total assets of the financial system, in January the most notable was the increase in the relevance of the balance of current accounts in the BCRA in both domestic and foreign currency (see Chart 6). On the other hand, compared to the end of 2020, the relative importance in total assets of the holding of BCRA instruments and credit to the public sector was reduced. With regard to the sector’s funding, in the first month of the year, the private sector’s time deposits in national currency and net worth increased their weighting in the total (see Chart 7), while the private sector’s demand accounts in pesos reduced their relative participation.

Graph 6 | Composition of total assets

Financial system – Share %

Figure 7 | Total system funding composition

In % of total funding (liabilities + equity)

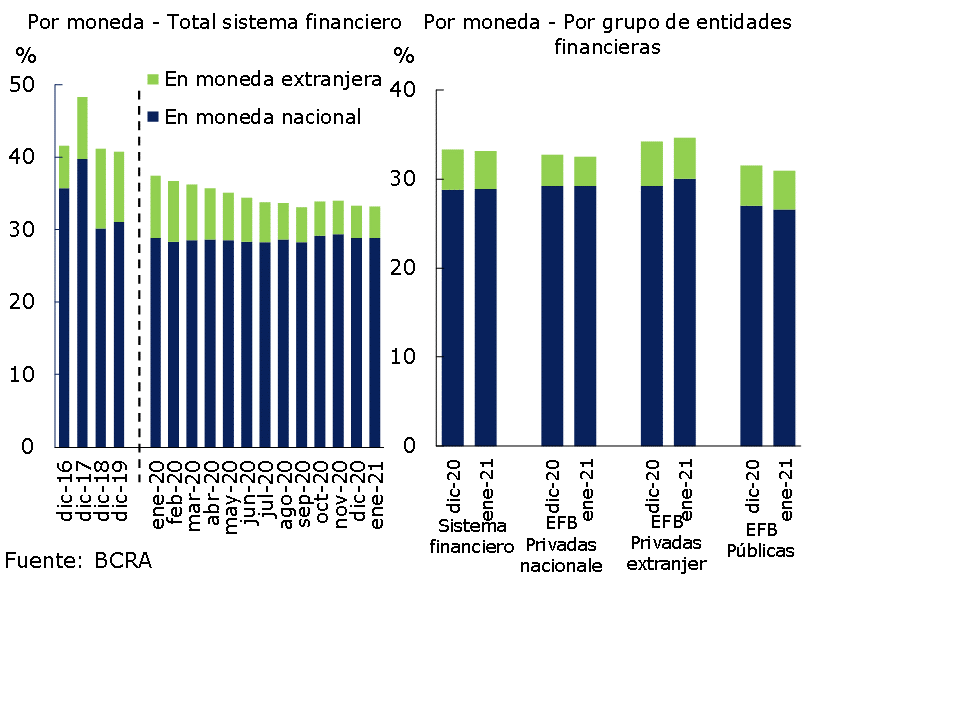

In the first month of 2021, the foreign currency assets of the financial system represented 19.6% of total assets, with no significant changes compared to the end of 2020 and 4 p.p. less than in January 2020. On the other hand, liabilities in the same denomination totaled 17.7% of total funding (liabilities and equity), remaining unchanged in magnitude with respect to the level of December 2020 and accumulating a reduction of 4.6 p.p. y.o.y. When additionally considering the forward purchase/sale of foreign currency – off-balance sheet – carried out by financial institutions as a whole, the spread between assets and liabilities in this denomination reached 12.3% of the regulatory capital integration in January, falling 1.3 p.p. compared to the level of December 2020. Thus, within the framework of the macroprudential regulations in force, this differential remains below the average evidenced in recent years (see Chart 8).

Figure 8 | EM Assets – EM Liabilities + EM Forward Position (Financial System)

III. Portfolio quality

In January, the gross exposure of the financial system to the private sector (including domestic and foreign currency) stood at 33.2% of total assets, slightly below the value of the previous month. 13 The ratio totaled 28.9% when considering only financing in pesos, slightly above December and without significant changes with respect to the same month of the previous year (see Graph 9). On the other hand, credit to the private sector in foreign currency continued to decrease its weighting in total assets, in line with the performance observed in recent years.

Figure 9 | Private Sector Credit Balance / Assets

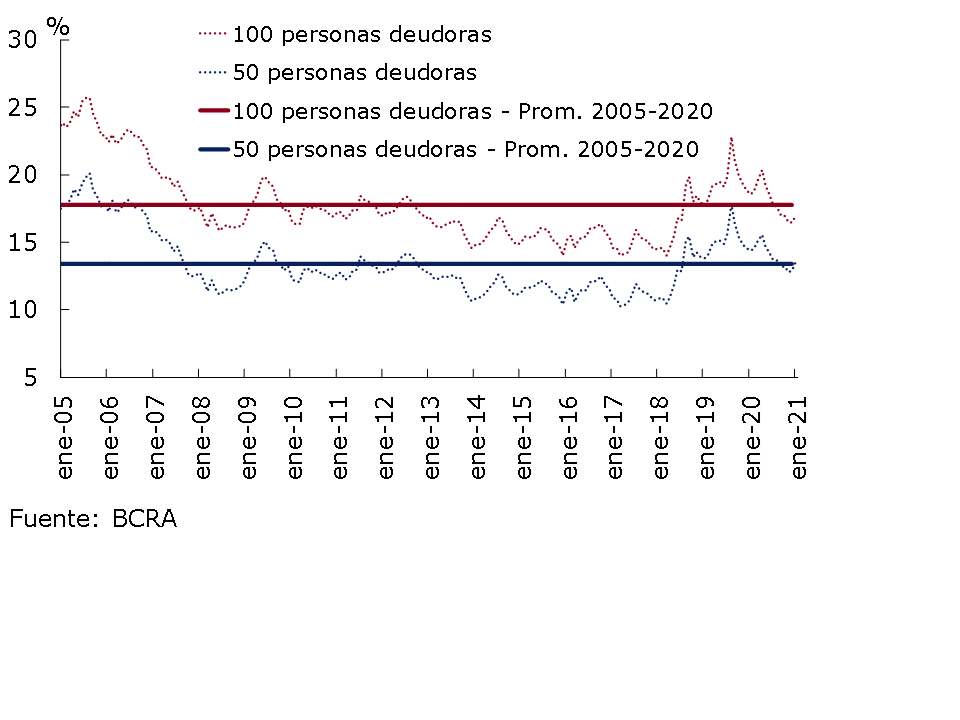

The concentration of private sector debtors in the financial system remained moderate at the beginning of 2021. 14 The share of the main debtors (legal and human) in the total portfolio gradually declined,15 after the peak reached in August 2019. In particular, the top 100 and 50 private sector debtors in the financial system aggregate accounted for 17% and 13.6% of the total credit balance as of January (see Chart 10), 1.5 p.p. and 0.8 p.p. below the same month of the previous year, respectively.

Figure 10 | Share of the total balance of credit to the private sector of the main debtors

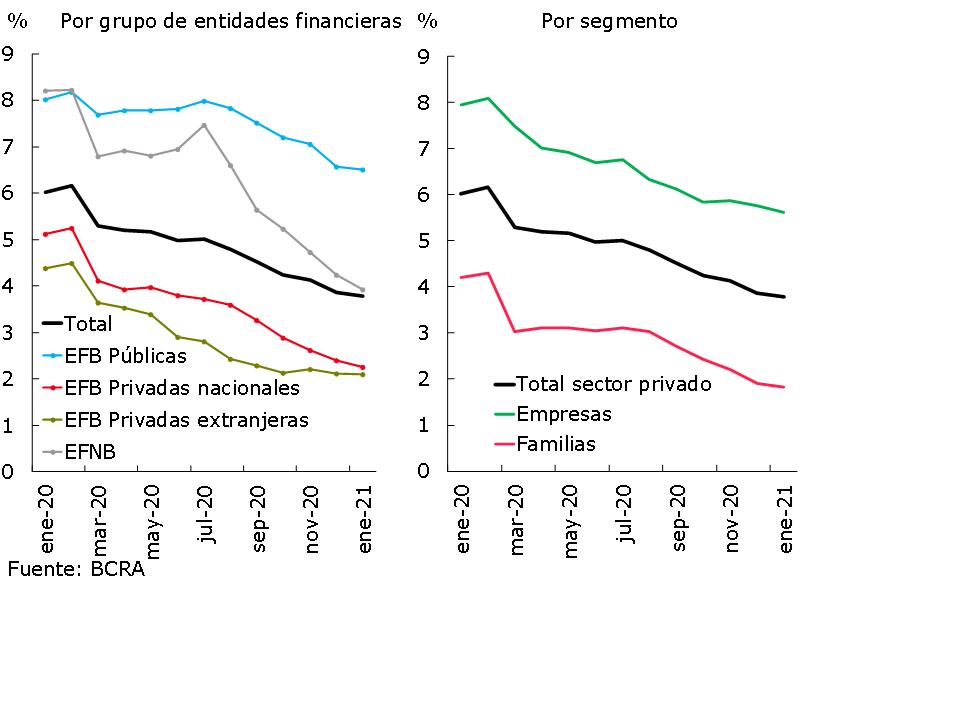

In a scenario in which the transitory modification of the parameters for classifying debtors and the possibility of transferring unpaid installments at the end of the life of the credit – accruing onlycompensatory interest 16 – to alleviate the financial burden of people in the face of the pandemic scenario is maintained, the irregularity ratio of credit to the private sector for the aggregate financial system continued to fall to 3.8% in the month, 0.1 p.p. less than at the end of the previous year (-2.2 p.p. y.o.y.) (see Graph 11). This fall continues to be widespread among the different groups of financial institutions.

Figure 11 | Irregularity of credit to the private sector

Irregular financing / Total financing (%)

Non-performing loans to households stood at 1.8%, slightly below the previous month (-2.4 p.p. y.o.y.), with a reduction in the irregularity ratio of all credit assistance except credit cards (see Graph 12). As for credit to companies, irregularity stood at 5.6% of the total, with a monthly decrease similar to that verified in the segment to families (-2.3 p.p. y.o.y.). As has been happening in recent months, the decrease in the non-performing loan indicator was widespread among credit lines, with the exception of pre-financing for exports.

Figure 12 | Irregularity of credit to the private sector

Irregular financing / Total financing (%)

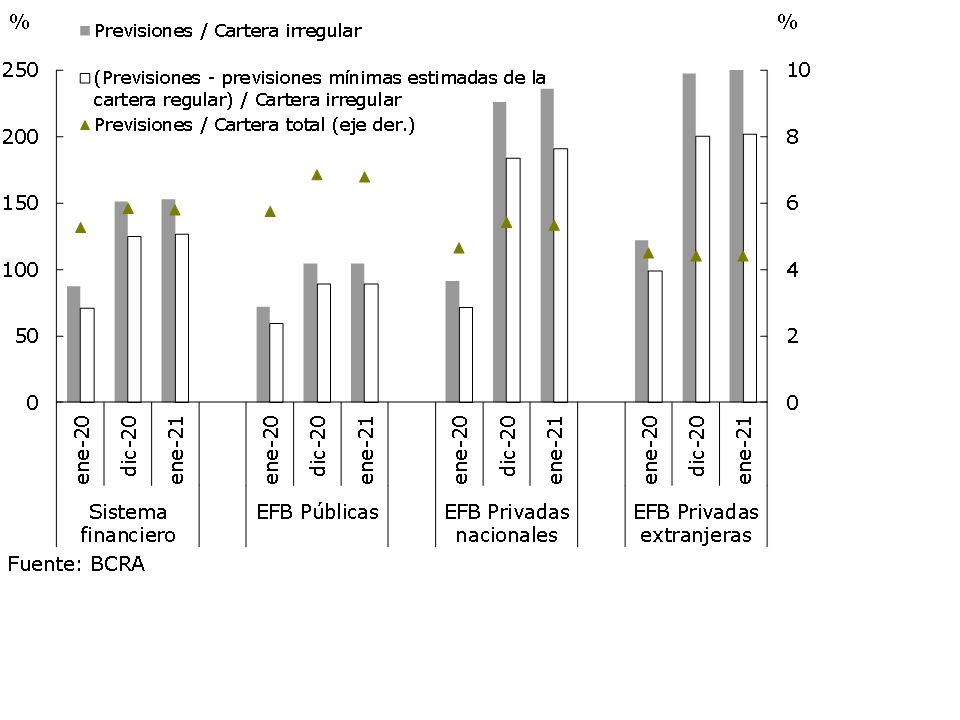

Financial institutions as a whole continued to preserve comfortable levels of forecasting. The forecasts represented 5.8% of total credit to the private sector in January, slightly below the previous month (+0.5 p.p. y.o.y.). The total forecasts in terms of the non-performing portfolio stood at 153.2% in the month, 2.1 p.p. more than in December (and +65.8 p.p. y.o.y.) (see Graph 13). In turn, the balance of regulatory forecasts attributable to the non-performing portfolio (following the criteria of the minimum regulatory forecasts for bad debt risk) totaled 126.4% of said portfolio in January.

Figure 13 | Credit to the private sector and forecasts

By Entity Group

The relationship between regulatory capital and credit to the private sector net of forecasts provides a general idea of the level of resilience of the sector in the face of possible scenarios of counterparty risk materialization. This ratio stood at 43.4% at the systemic level in January (3.1 p.p. more than in the previous month and 8.2 p.p. y.a.), being a high figure compared to the average of the last 10 years (25.5%).

IV. Liquidity and solvency

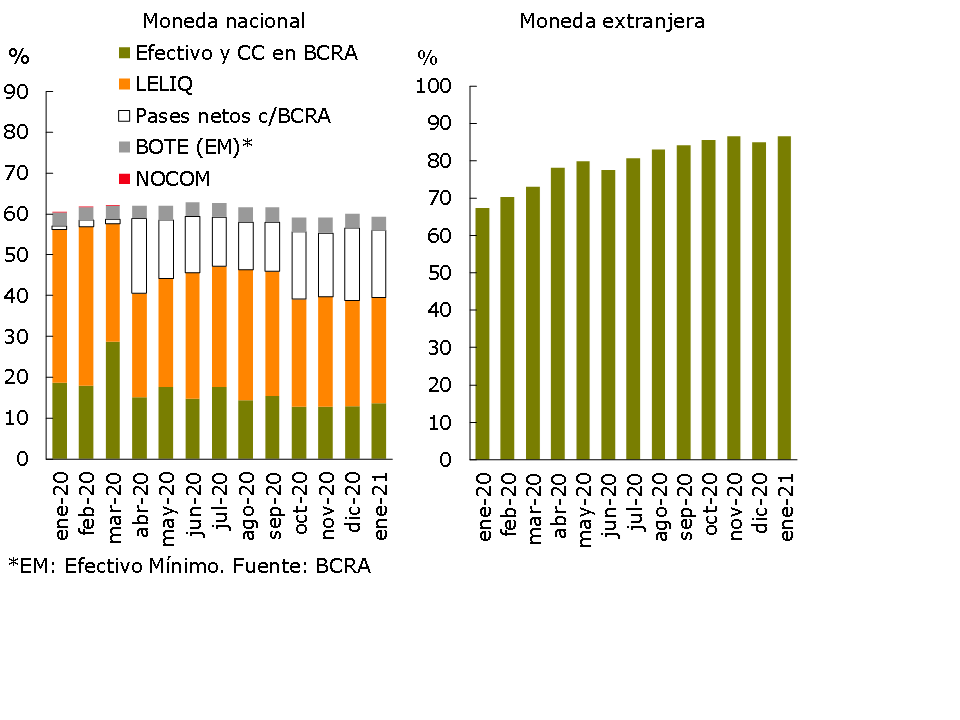

From relatively high levels compared to the last 15 years, the ample liquidity of the banks as a whole fell slightly in January. The broad liquidity ratio17 stood at 64.7% of total deposits (59.4% for the segment in pesos and 86.5% for items in foreign currency), 0.3 p.p. less than at the end of the previous year (-0.7 p.p. and +1.5 p.p. for items in local currency and foreign currency, respectively) (see Chart 14). Within the segment in pesos, the share of net passes with the BCRA decreased during the month, and the relevance of the current account balance that entities have in this Institution increased. In the last 12 months to January, the broad liquidity indicator increased by 2.5 p.p. in deposits, with a dissimilar behavior by currency: an increase of 19.1 p.p. y.o.y. in the foreign currency segment and a decrease of 1.1 p.p. y.o.y. in the peso segment.

Figure 14 | Liquidity of the financial system

In % of deposits

At the aggregate level, at the beginning of the year the local financial system continued to comfortably exceed international standards in terms of liquidity. The Liquidity Coverage Ratio (LCR, with information as of January 2021) and the Stable Net Funding Ratio (NSFR, as of September 2020)—18.19 stood at levels that are practically double the minimums required for the group of locally obligated entities (Group A).

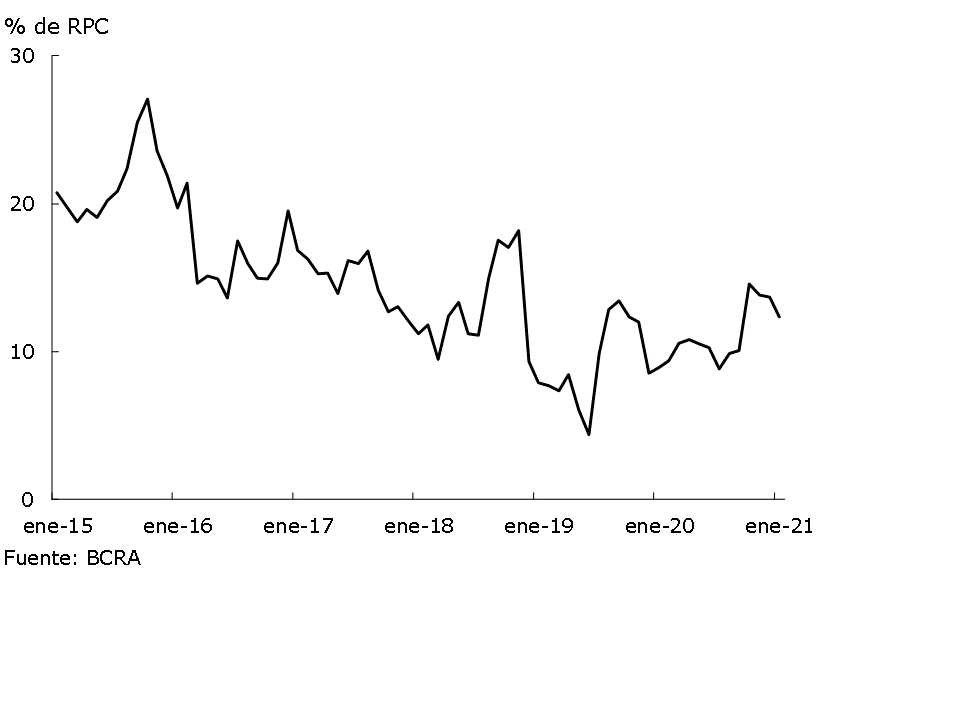

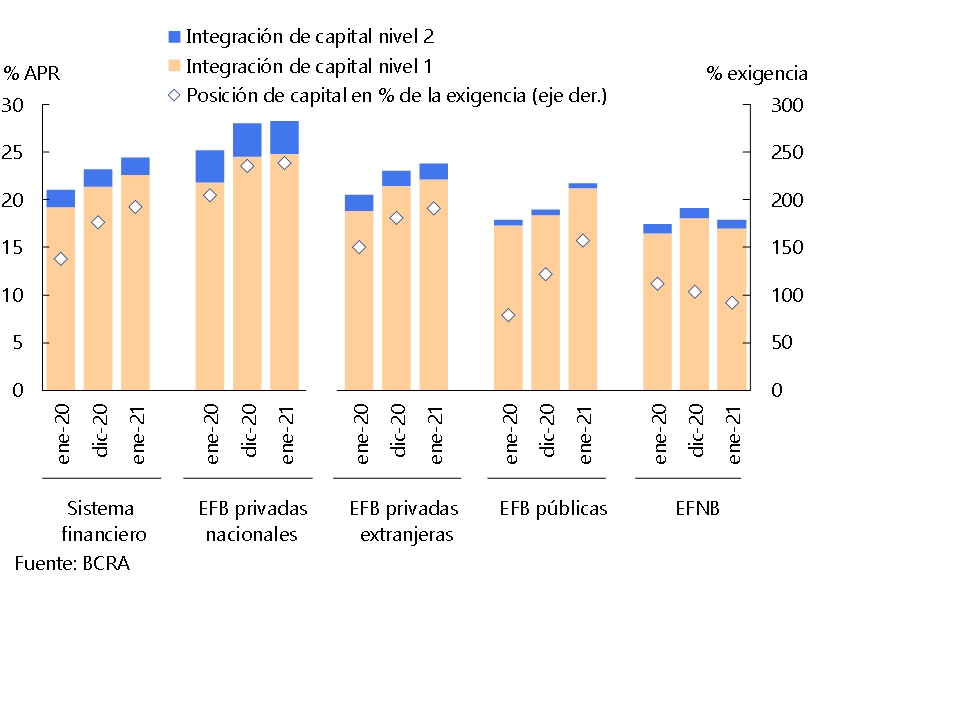

With regard to the solvency ratios of financial institutions as a whole, capital integration (CPR) increased in January in terms of risk-weighted assets (RWA) (see Chart 15). With the exception of the EFNBs, all groups of institutions increased this ratio in the month, amounting to 24.4% for the entire system (+1.2 p.p. monthly). The sector’s capital position (RPC net of regulatory requirements) increased 16 p.p. of the requirement in the month to 192%. In year-on-year terms, the regulatory capital and capital position of the aggregate financial system expanded by 3.4 p.p. of RWAs and 54 p.p. of regulatory requirements, respectively.

Figure 15 | Integration of regulatory capital

By financial institution group

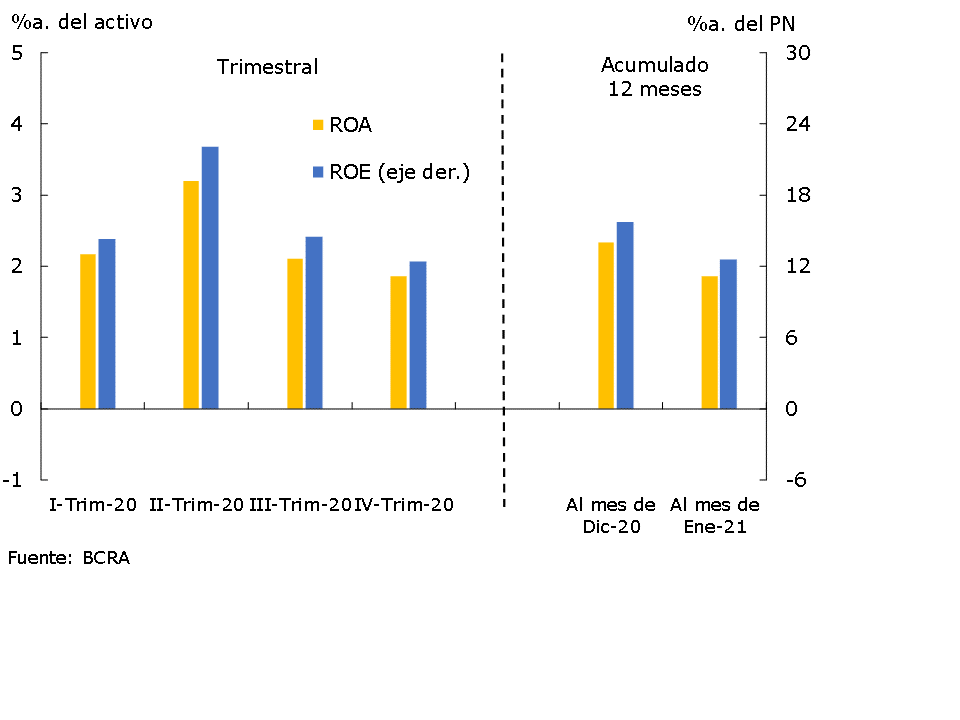

Regarding the profitability ratios of the financial system, in January the total comprehensive results in homogeneous currency were slightly positive and lower than those recorded at the end of 2020, continuing a trend of gradual decline that has been observed in recent quarters (see Chart 16). For its part, in the accumulated twelve months to January, the total comprehensive results in homogeneous currency were equivalent to 1.9% of assets (ROA) and 12.6% of equity (ROE).

Figure 16 | Comprehensive total profit in homogeneous currency of the financial system

The financial margin of the aggregate of entities reached 11% of assets in the cumulative period between February 2020 and January 2021. As has been the case in recent months, interest income from loans and results from securities were the most relevant items of the financial margin (8.3% and 8.2% of assets, respectively). Interest paid on deposits continues to be the main financial expenditure of the sector in the period (9% of assets). On the other hand, among the non-financial items, the results for services as generators of resources (1.8% of assets) stood out, while administrative expenses (6.6% of assets) and charges for uncollectibility (1.6% of assets) were the main expenditures in the accumulated twelve months.

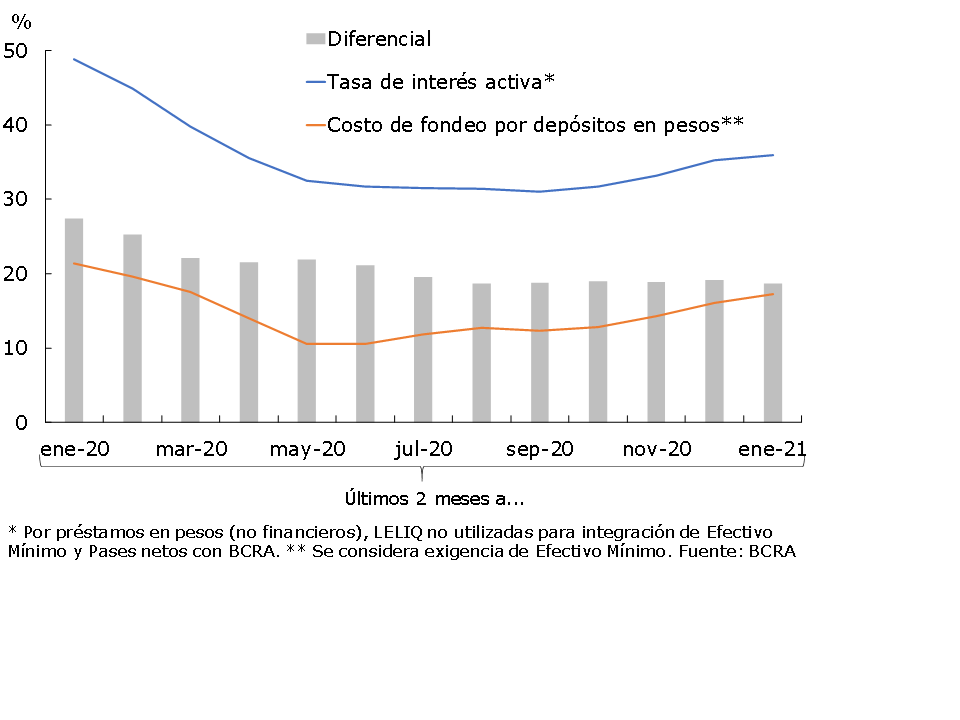

According to the estimate of nominal implicit interest rates arising from the main assets and liabilities in national currency,20 21 in the last two months (taking December 2020 and January 2021) the increase in the cost of funding for deposits was slightly higher than the increase in the lending rate (see Chart 17). As a result, the differential between the two concepts narrowed slightly in the period. In a year-on-year comparison, a decrease in the implicit spread of nominal interest rates in national currency is also estimated. The trajectory of implied interest rates occurred in different inflationary contexts. When the estimated effect of the rise in the general price level was separated, the differential between the lending rate and the cost of funding also showed a pattern of decrease.

Figure 17 | Estimated (annualized) implied nominal interest rates for the financial system

V. Payment system

At the beginning of 2021, electronic means of payment continued to gain relevance in the usual transactions of companies and families. In particular, total transfers in pesos (immediate and with credit in 24 hours) made during February 2021 (latest available information), although they decreased compared to the previous month within the framework of seasonal factors, continued to register significant growth in a year-on-year comparison (66.6% in quantities and 31.9% in real amounts, see Graph 18). This dynamic of total transfers was reflected in the greater weight they had in the economy’s usual transactions: it is estimated that the amount operated through total transfers was equivalent to almost 44% of GDP in February 2021, growing 15.4 p.p. in a year-on-year comparison. It is worth mentioning that in February, 88% of the number of operations and 76% of the value in real amounts of total transfers in pesos was explained by the segment that is carried out with immediate accreditation.

Figure 18 | Total transfers in pesos (immediate and with credit in 24 hours)

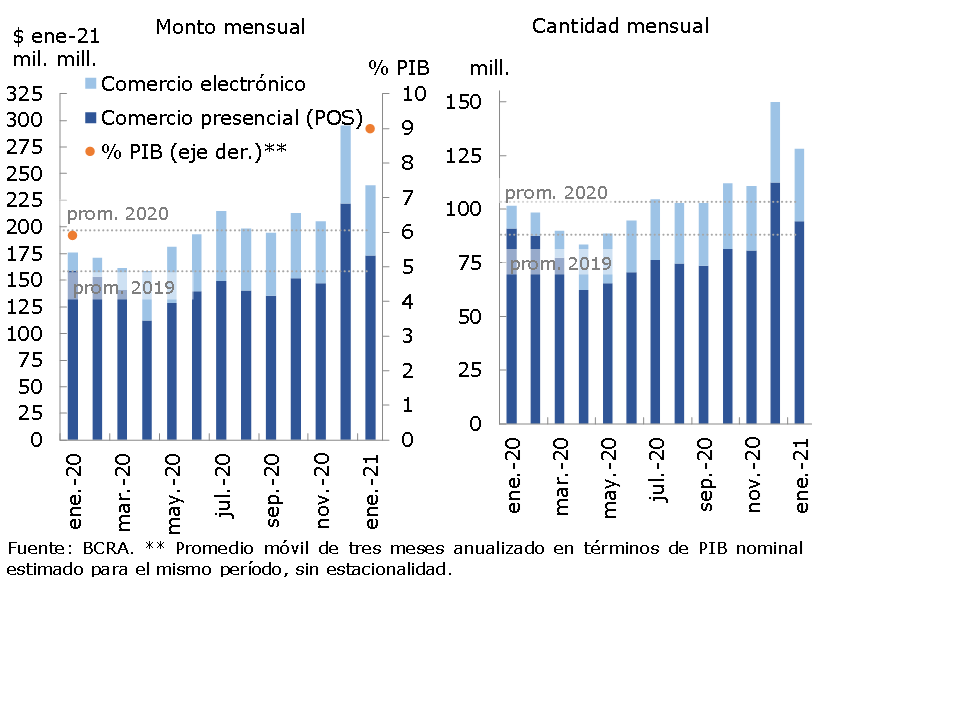

Debit card operations also presented a certain seasonality as of January (latest available information) by decreasing compared to December 2020. Compared to the same month of the previous year, debit card transactions increased 26% in amounts and 35.8% in real amounts (see Graph 19), both in person and electronically. It is worth highlighting the dynamism evidenced in the electronic format: +219% YoY in amounts to account for 26.3% of the total operations and +280% YoY in real amounts to cover 27.4% of the total amount. Thus, it is estimated that the amount of debit card operations represented 9% of GDP at the beginning of the year, increasing 3.1 p.p. compared to the same month in 2020.

Figure 19 | Debit card transactions

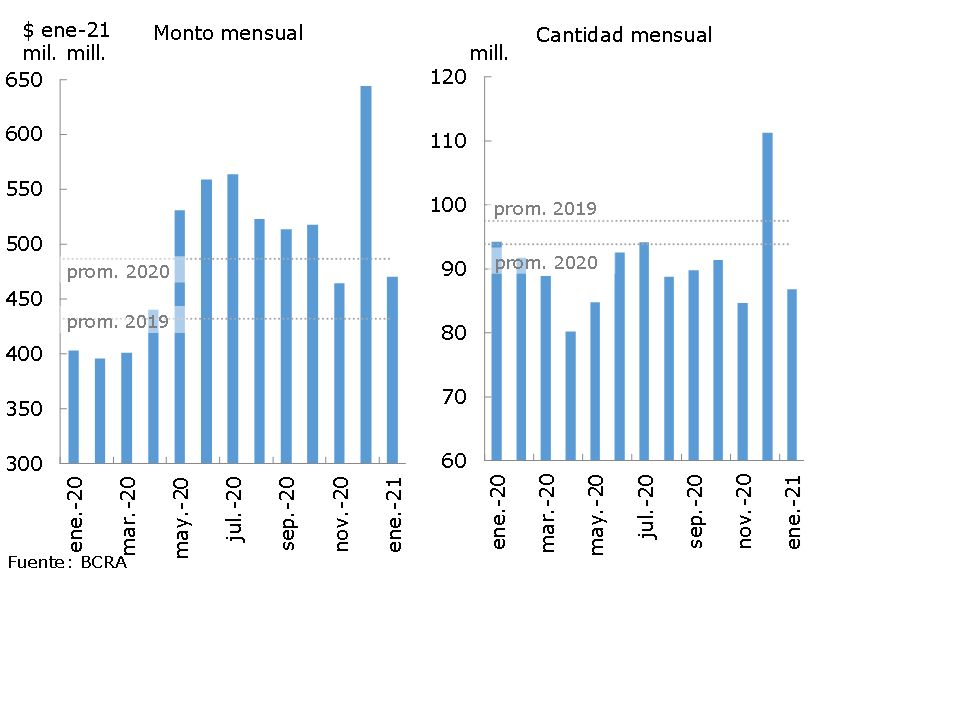

Regarding cash withdrawals through the use of ATMs, in January (latest available information) there were fewer operations than last December (-22% in amounts and -27% in real amounts), in line with the seasonality that usually shows each year-end (see Graph 20). It should be recalled that the BCRA timely ordered the free use of ATMs at the same time as the beginning of the mandatory and preventive social isolation (ASPO). In addition, at that time, the availability of cash at ATMs was expanded, establishing that they had to admit withdrawals of at least $15,000 accumulated per day per user. These measures were in line with a set of actions that sought at that time to reduce the movement of people by limiting the distance and the times they had to go to an ATM to get cash. The use of ATM networks is free until March 31 for all users of the financial system. From that date, only holders of debit cards associated with salary accounts, pension payments or social plans will be able to continue using any ATM at no cost, regardless of which bank or network they belong to. Compared to the average of the last 12 months, cash withdrawals through ATMs remained below this record in January (-4% in amounts and -6.3% in real amounts). Compared to the same month of the previous year, withdrawals decreased in quantities (-8%) and increased in real amounts (16.7%), increasing the average amount of each withdrawal measured in constant currency (+$1,145, to $5,418 per withdrawal at January 2021 prices).

Figure 20 | Cash withdrawals

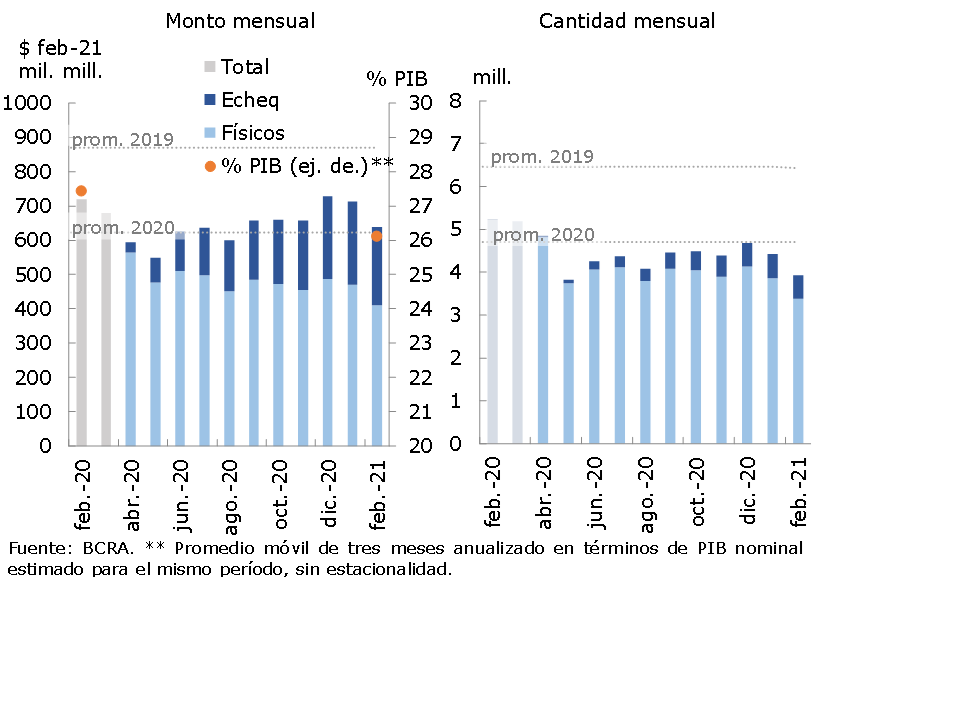

With respect to check transactions, during February (latest available information) the total compensation was reduced compared to the previous month. Compared to the same month of the previous year, the clearing of checks also decreased in amounts (-25.2%) and in real amounts (-11.2%). In this way, the weighting of the use of the check as a means of payment continued to decrease. It is estimated that the amount cleared from checks during February 2021 was equivalent to 26.1% of GDP, falling 1.3 p.p. in a year-on-year comparison (see Chart 21). Within this segment, the Echeqs gradually gained share to account for about 36% of the total amount compensated during February.

Figure 21 | Check clearing

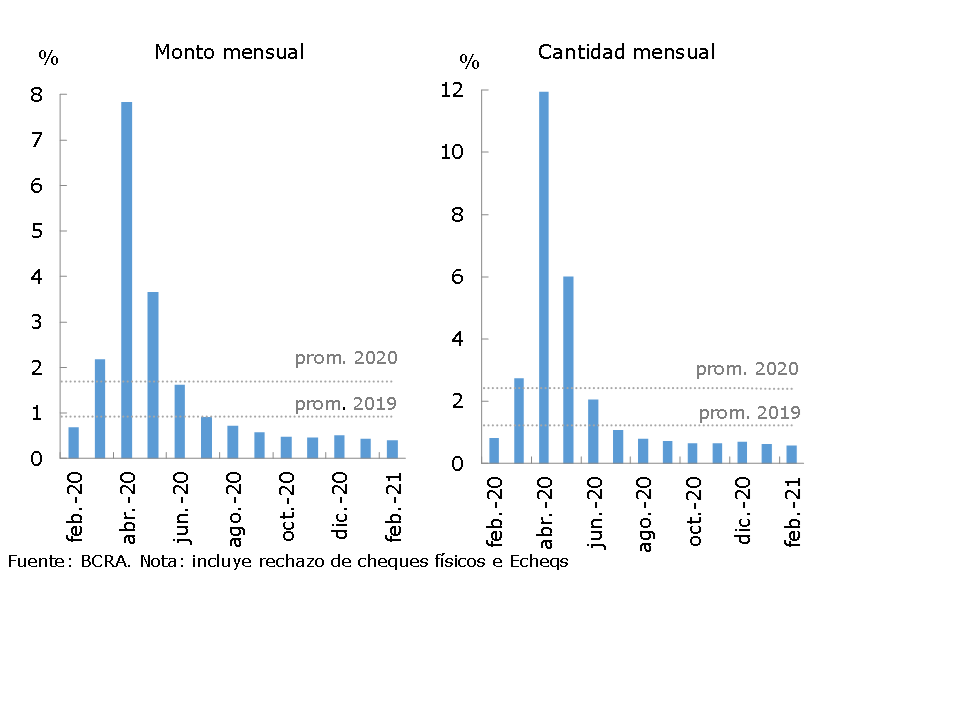

In February, the ratio of check rejections due to lack of funds in terms of the total compensated decreased compared to the previous month both in quantities (-0.04 p.p., with a level of 0.59%) and in amounts (-0.02 p.p., with a level of 0.41%), being below the levels corresponding to the same month of the previous year (with a fall of 0.23 p.p. and 0.27 p.p. in quantities and amounts respectively, see Figure 22).

Figure 22 | Bounce checks due to insufficient funds

References

1 Differences in balance sheet balances expressed in homogeneous currency.

2 Taking into account the segment of items in foreign currency —expressed in currency of origin—, in January the decrease in financing to the private sector was the most important source of resources for all financial institutions. On the other hand, the reduction in private sector deposits was the most prominent application of funds in the period.

3 Includes principal adjustments and accrued interest.

4 Throughout the Report, when reference is made to groups of private (national and/or foreign) and public financial institutions, it corresponds to banking entities. Non-bank entities will be referred to as “EFNBs”.

5 For more details, see Communication “A” “7140” and amendments.

6 The entities covered are those included in group “A” as of April 1, 2021 and those that – not included in said group – operate as financial agents of the National, provincial, Autonomous City of Buenos Aires and/or municipal governments.

7 This percentage is reduced by 25% for those financial institutions that do not make up group A.

8 See Communication “A” “7240”

9 For more details see Communication “A” “7082” and Communication “A” “7102”.

10 For more details, see Communication “A” “6993”.

11 For more details, see Communication “A” “7082”.

12 It should be considered that, despite this dynamism, the balance of UVA time deposits in the private sector still has a low relevance at the aggregate level, reaching only 1.5% of the total balance of deposits in national currency of the private sector.

13 The ratio is 2 p.p. lower when the total forecasts for the balance of credit to the private sector are netted

14 It should be considered that the local regulatory framework has a set of rules that seek to promote the diversification of the debtor portfolio of financial institutions. In this way, the aim is to avoid situations of excessive exposure of a bank to individual customers that could markedly increase the levels of credit risk assumed and, potentially, adversely affect its capital. See Consolidated Text on “Large exposures to credit risk” and Section 5 of the “IEF” for the second half of 2019.

15 Considering the credit balance of debtors throughout the financial system.

16 Communication “A” “6938”, Communication “A” “7107”, Communication “A” “7181”, and Point 2.1.1. of the Ordered Text “”Financial Services in the Framework of the Health Emergency Provided for by Decree No. 260/2020 CORONAVIRUS (COVID-19)””.

17 Considers availability, integration of minimum cash and BCRA instruments, in national and foreign currency.

18 The LCR considers the liquidity available to deal with a potential outflow of funds in the event of a possible stress scenario in the short term. See Ordered Text —TO— “”Liquidity Coverage Ratio””.

19 The NSFR takes into account the availability of stable funding of the entities, in line with the terms of the businesses to which it applies. See TO “Stable Net Funding Ratio””.

20 For the calculation of implicit interest rates, concepts such as administrative expenses, tax expenses, cost of capital or other components associated with hedging for risks intrinsic to financial intermediation operations are not considered.

21Implied interest rates are estimated by accumulating the flows of the last 2 months and annualized. For more details on the calculation methodology, see previous editions of the Banking Report.

Share on