1. Executive Summary

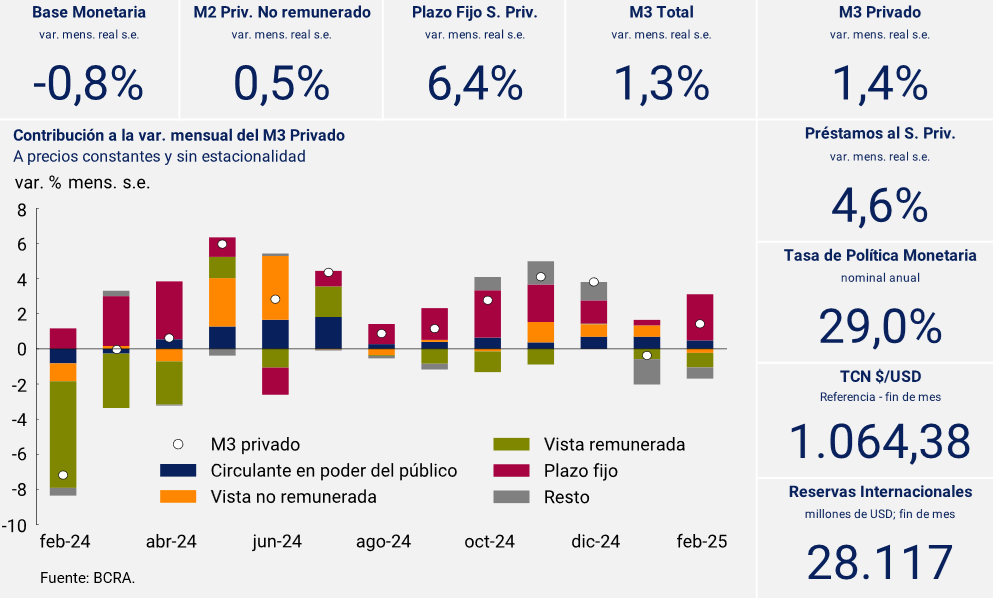

The broad monetary aggregate (private M3) registered an increase of 1.4% in real terms and without seasonality. Thus, the demand for money continued to recover from historic lows. The component most closely linked to means of payment (private transactional M2) grew more moderately, 0.5% s.e. in real terms. The greatest contribution to its growth came from fixed-term deposits, with increases in the holdings of legal entities and, to a lesser extent, individuals.

On the side of the factors that explain this money creation, credit to the private sector continued to stand out, which presented a monthly growth of 4.6% at constant prices and without seasonality. Although the increase was spread among the different lines of credit, those destined for consumption made a greater contribution to the growth of loans. With respect to the primary change in money, the Monetary Base contracted, at constant and non-seasonal prices (-0.8%), due to the effect of the displacement of fixed-term demand deposits, the latter having lower minimum cash requirements and can be integrated with public securities.

In the foreign currency segment, private sector deposits showed a decline, although they remain around maximum levels, while loans in foreign currency showed sustained growth. It should be noted that the BCRA decided to relax the conditions for granting loans in foreign currency, eliminating the prohibition on financial institutions from lending to customers who are not exporters to the extent that the funds come from Negotiable Obligations or lines of financing from abroad.

2. Demand for money

In February, the broad monetary aggregate M3 private1 registered a monthly increase of 1.4% at constant prices and adjusted for seasonality. Thus, the demand for money continued on a path of recovery from historic lows. In year-on-year terms, private M3 presented a real growth of 30.8% and as a percentage of GDP it would have stood at 12.6%, 0.6 p.p. above the February 2024 record.

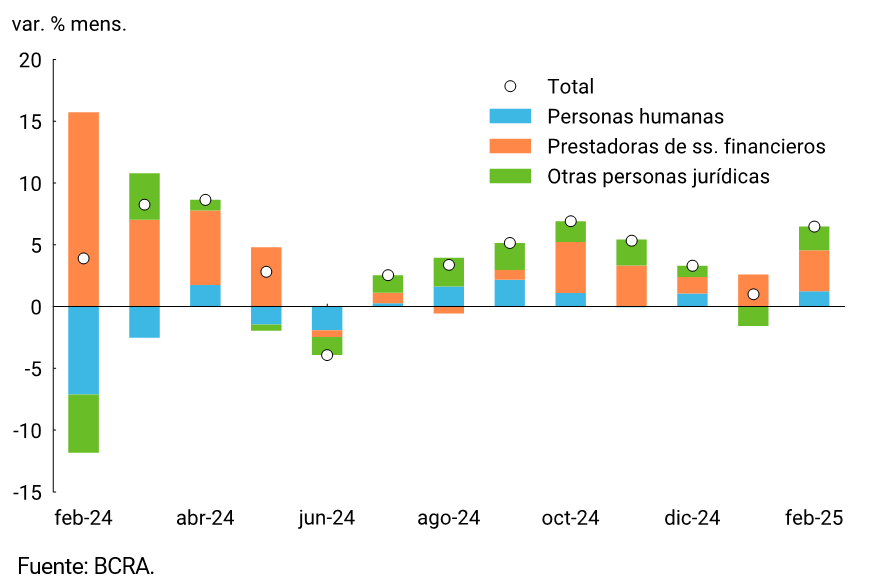

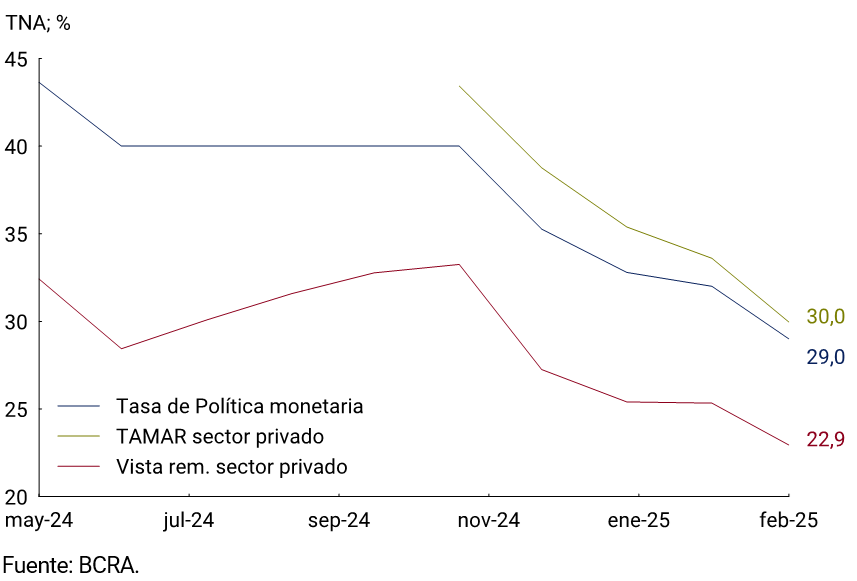

At the component level, means of payment (private transactional M2) moderated their pace of expansion, registering an increase of 0.5% s.e. in real terms. While the working capital held by the public expanded for the eleventh consecutive month (2.7% s.e.), transactional demand deposits contracted slightly (-0.8% s.e.). In the remunerated segment, fixed-term placements stood out with an average monthly growth of 6.4% s.e. at constant prices. The increase extended to all types of depositors, although the greatest impetus came from legal entities (see Figure 2.1). Within the “Financial Services Providers”, the main players are the Money Market Mutual Funds, whose assets increased 1.8% s.e. in real terms. The greater availability of funds was channeled towards fixed-term placements. Meanwhile, interest-bearing demand deposits experienced a monthly contraction in real terms of 8.1% s.e. The interest rate paid on fixed-term placements in the wholesale segment (TAMAR), in which legal entities mainly operate, stood at an average of 30.1% n.a. in the month, 7.2 p.p. above the rate at which demand deposits are remunerated (see Chart 2.2).

Figure 2.1 | Private sector

fixed-term Contribution to real and non-seasonal contributions

Figure 2.2 | Passive

Interest Rates Monthly Averages

3. Money Creation

3.1. Primary creation

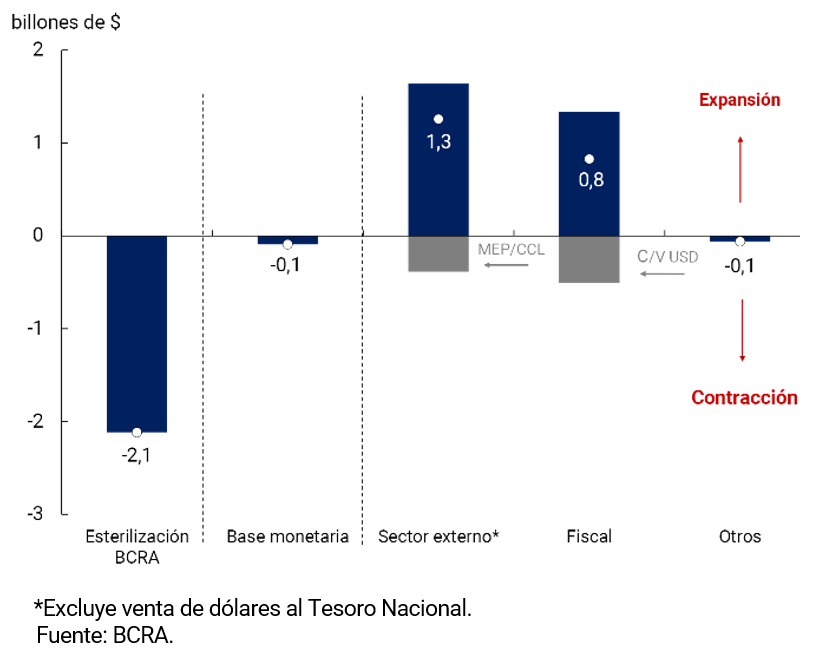

The Monetary Base registered an average monthly fall of $90.4 billion in February, which implied a decrease of 0.8% at constant prices and adjusted for seasonality (see Figure 3.1.1).

Regarding the factors of variation of the Monetary Base, the net purchase of foreign currency from the private sector and public sector operations were expansionary. Within the latter, the statistical drag left by the last auction of the National Treasury in January, in which it partially renewed the maturities of debt in pesos, had an impact. The monetary expansion of operations mentioned above was more than offset by the greater holding of LEFI by financial institutions (see Figure 3.1.2). It is worth mentioning that towards the end of the month a sale of dollars was made to the National Treasury, which will be used to pay obligations in foreign currency. The operation was carried out with funds from the Treasury account in pesos at the BCRA, so its monetary effect was neutral.

Figure 3.1.1 | Monetary Base

At constant prices and without seasonality

Figure 3.1.2 | Monetary Base and Factors of Variation from the Supply Side to

Var. of Monthly Average Balances

3.2. Sequential creation

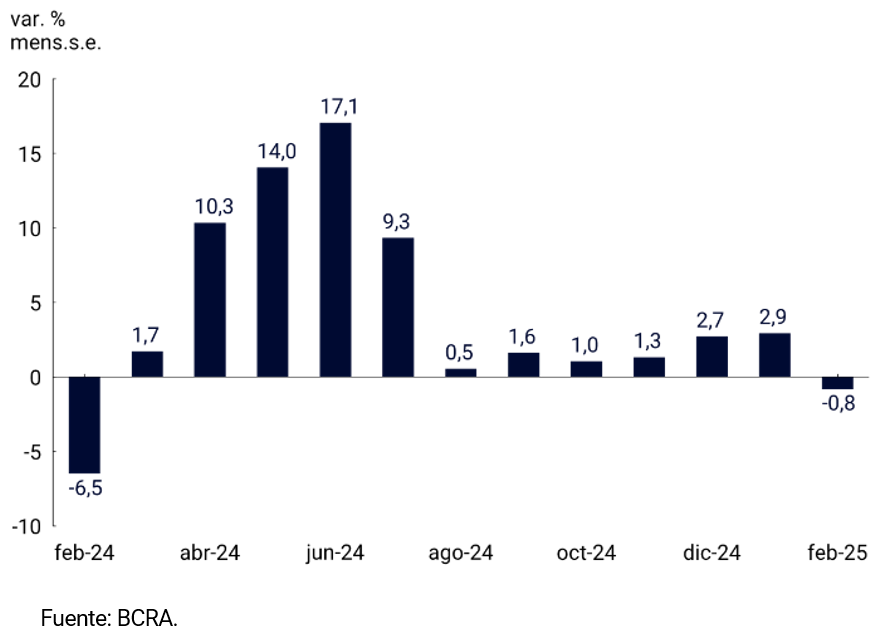

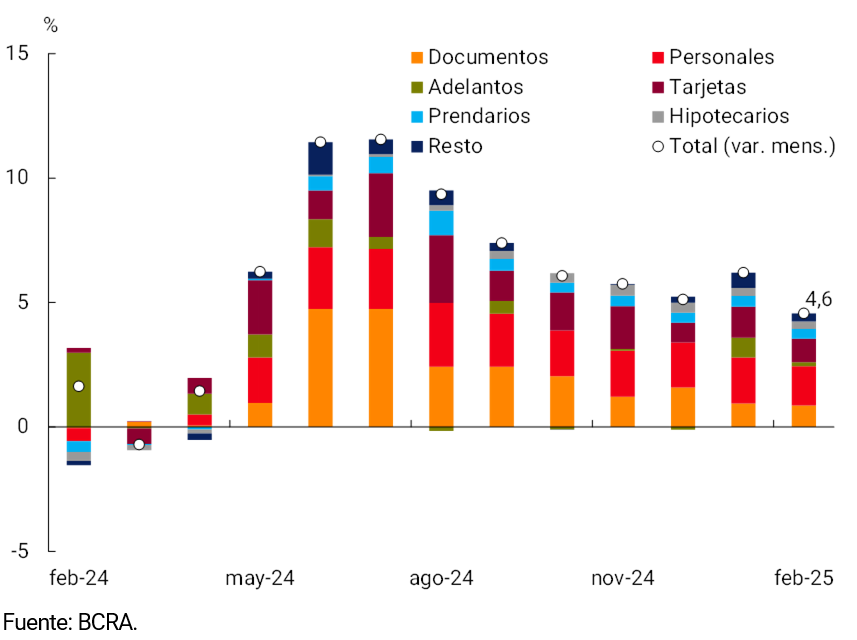

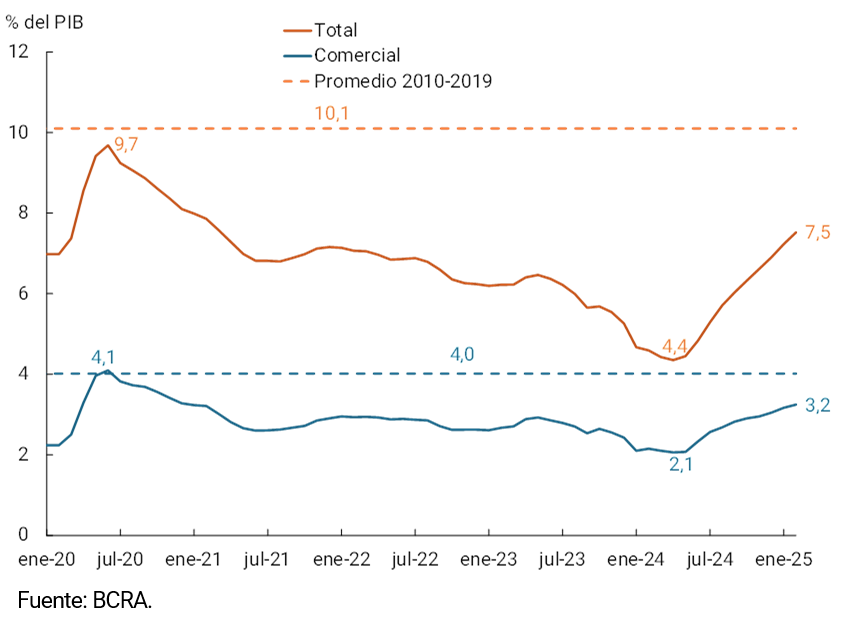

Loans in pesos to the private sector registered an increase of close to $2.8 trillion during February, consistent with a monthly growth of 4.6% s.e. at constant prices. Thus, credit to the private sector has now accumulated 11 consecutive months of growth and an increase of 108.0% s.e. compared to the lows of January 2024 in real terms. In a context of incipient reintermediation, credit to the private sector would have reached 7.5% of GDP, with an increase of 3.1 p.p. compared to the minimum recorded in 2024 and with a very high margin to continue on this path of recovery (see Figures 3.2.1 and 3.2.2).

Figure 3.2.1 | Contribution to var. monthly of loans in pesos to the private

sector At constant prices and without seasonality

Figure 3.2.2 | Loans to the private sector in terms of GDP

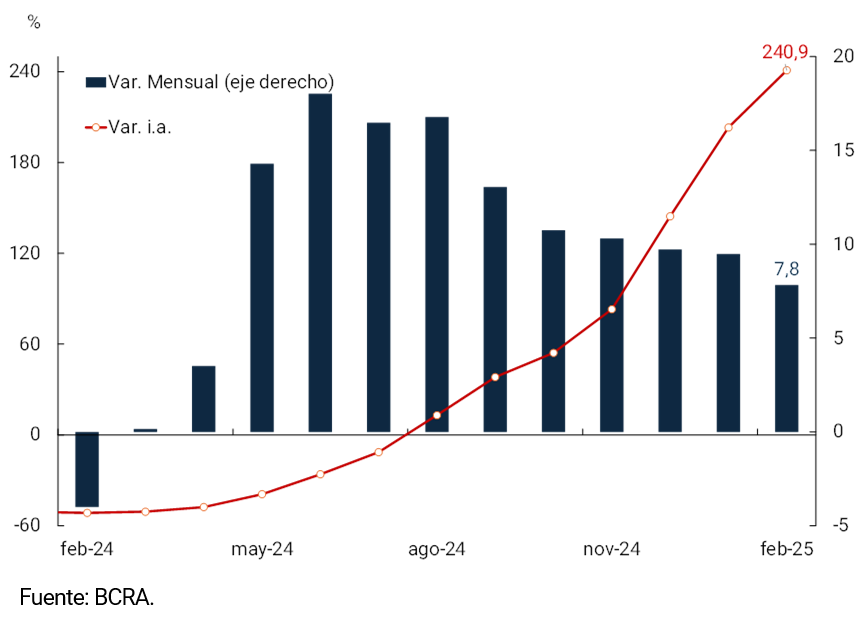

The growth of the month was generalized at the level of the different lines of credit, although the largest contribution came from consumer loans. Personal loans grew, in real terms, at a similar rate to that of previous months (7.8% s.e.) and in the last 12 months accumulated a growth of 240.9% (see Figure 3.2.3). On the other hand, credit card financing grew at constant prices by 3.5% per month and accumulated a year-on-year increase of 71.6%.

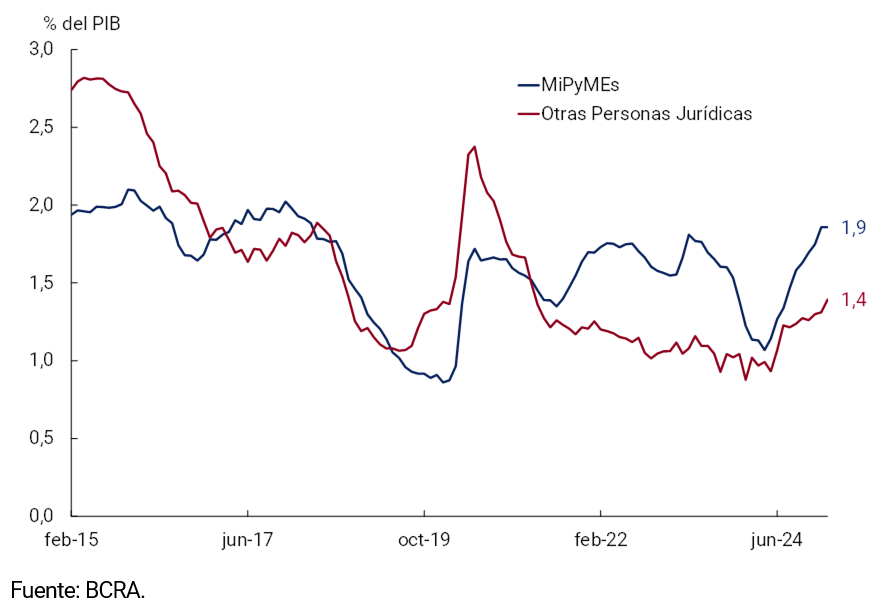

Commercial loans grew in real terms by 3.1% s.e. compared to January and have now grown for 13 consecutive months, standing 87.3% above their level a year ago. Those instrumented through documents grew 3.0% month-on-month s.e., with a similar increase in single-signature documents and discounted documents, which have a shorter average term. Advances, on the other hand, grew 1.6% month-on-month s.e. in real terms and are 39.1% above the level recorded in February 2024. When analyzing the evolution of commercial credit according to the type of debtor, it is observed that both credit for SMEs and for large companies grew in real terms again in February. Commercial credit to SMEs would have grown 0.5% s.e. and would have remained at a level of around 1.9% of GDP, the highest level in the last 7 years. Loans to large companies would have grown 6.7% s.e. and 70.3% y.o.y., to 1.4% of GDP (see Figure 3.2.4).

Finally, loans with collateral showed great dynamism, as in recent months. Although their contribution to growth is limited, they were the ones that showed a higher monthly expansion rate at constant prices. In fact, mortgages registered a monthly increase of 9.3% s.e. (124.0% y.o.y.) and pledges a monthly expansion of 6.5% real s.e. (122.0% y.o.y.).

Figure 3.2.3 | Personal

loans Var. monthly at constant prices and without seasonality

Figure 3.2.4 | Commercial loans per debtor

In terms of GDP

4. Foreign currency

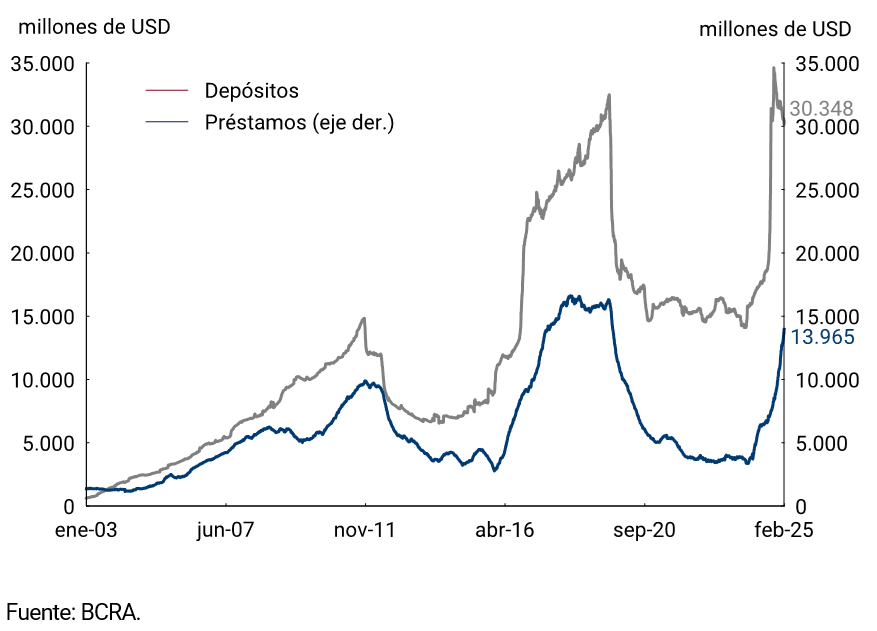

The main assets and liabilities in foreign currency of financial institutions showed dissimilar behaviors in January. On the one hand, private sector deposits continued to decline, recording a drop of USD840 million in February. However, the balance is at historically high levels (USD30,348 million; see Figure 4.1). On the other hand, loans to the private sector continued to show great dynamism, driven by commercial credit. The increase recorded in February was USD1,230 million, reaching the balance of USD13,965 million, the highest record since October 2019.

It should be noted that the BCRA decided to relax the conditions for granting loans in foreign currency. The prohibition on financial institutions from lending to customers who do not generate income in foreign currency to the extent that the funds come from Negotiable Obligations or lines of financing from abroadwas eliminated 2.

As of February, the new path of displacement of 1% per month for the exchange rate began to take effect. This adjustment continues to play the role of a complementary anchor to the fiscal one in the behavior of inflation expectations. Thus, the exchange rate ended the month at $1,064.38/USD.

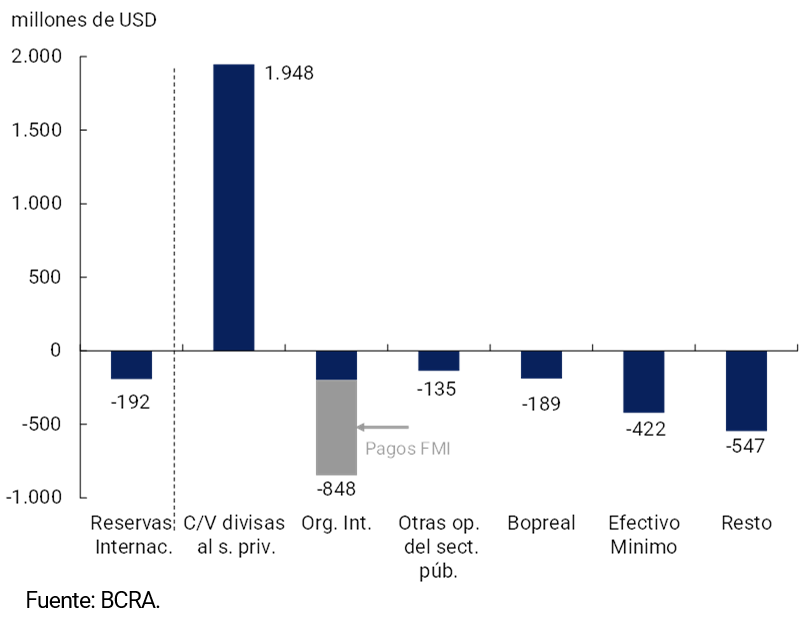

The BCRA’s International Reserves ended February with a balance of USD28,117 million, which implied a drop of USD192 million compared to the previous month. The effect of the net purchase of foreign currency from the private sector, which left a balance of USD1,948 million, was offset by the rest of the factors of variation in international reserves. In particular, payments to international organizations were highlighted, including the payment of interest and charges to the IMF for USD648 million (see Figure 4.2).

Figure 4.1 | Foreign currency loans and deposits to the private sector

Figure 4.2 | Factors of change in international

reserves Change between balances at the end of the month

Glossary

ANSES: National Social Security Administration.

AFIP: Federal Administration of Public Revenues.

BADLAR: Interest rate on fixed-term deposits for amounts greater than one million pesos and a term of 30 to 35 days.

BCRA: Central Bank of the Argentine Republic.

BM: Monetary Base, includes monetary circulation plus deposits in pesos in current account at the BCRA.

CC BCRA: Current account deposits at the BCRA.

CER: Reference Stabilization Coefficient.

NVC: National Securities Commission.

SDR: Special Drawing Rights.

EFNB: Non-Banking Financial Institutions.

EM: Minimum Cash.

FCI: Common Investment Fund.

A.I.: Year-on-year .

IAMC: Argentine Institute of Capital Markets

CPI: Consumer Price Index.

ITCNM: Multilateral Nominal Exchange Rate Index

ITCRM: Multilateral Real Exchange Rate Index

LEBAC: Central Bank bills.

LELIQ: Liquidity Bills of the BCRA.

LFIP: Financing Line for Productive Investment.

M2 Total: Means of payment, which includes working capital held by the public, cancelling cheques in pesos and demand deposits in pesos from the public and non-financial private sector.

Private M2: Means of payment, includes working capital held by the public, cancelling cheques in pesos and demand deposits in pesos from the non-financial private sector.

Private transactional M2: Means of payment, includes working capital held by the public, cancelling cheques in pesos and non-remunerated demand deposits in pesos from the non-financial private sector.

M3 Total: Broad aggregate in pesos, includes the current currency held by the public, cancelling checks in pesos and the total deposits in pesos of the public and non-financial private sector.

Private M3: Broad aggregate in pesos, includes the working capital held by the public, cancelling checks in pesos and the total deposits in pesos of the non-financial private sector.

MERVAL: Buenos Aires Stock Market.

MM: Money Market.

N.A.: Annual nominal.

E.A.: Effective Annual.

NOCOM: Cash Clearing Notes.

ON: Negotiable Obligation.

GDP: Gross Domestic Product.

P.B.: basis points.

PSP.: Payment Service Provider.

p.p.: percentage points.

MSMEs: Micro, Small and Medium Enterprises.

ROFEX: Rosario Term Market.

S.E.: No seasonality

SISCEN: Centralized System of Information Requirements of the BCRA.

SIMPES: Comprehensive System for Monitoring Payments of Services Abroad.

TCN: Nominal Exchange Rate

IRR: Internal Rate of Return.

TM20: Interest rate on fixed-term deposits for amounts greater than 20 million pesos and a term of 30 to 35 days.

TNA: Annual Nominal Rate.

UVA: Unit of Purchasing Value

References

1 The private M3 includes the working capital held by the public and the deposits in pesos of the non-financial private sector (demand, time and others).

2 Communication 8202.

Share on