Executive summary

• Financial service access points (PDAs) registered an increase of 4.8% between December 2021 and December 2022 and maintained the percentage of the adult population living in localities with PDAs at 92.5%.

• Bank and/or payment account coverage reached almost the entire adult population (99.3%) at the end of 2022. The number of individuals (PH) who had at least one account stood at 35.1 million compared to 34.6 million in June 2022 (98.5%). With values above 95%, the NOA, Cuyo and Patagonia regions were at account holding levels close to full coverage while the Center and NEA have already reached it.

• Joint bank and payment account tenure reached record levels in several segments of the population. In December 2022, joint tenure marked maximum coverage values in the age range of 25 to 29 years, reaching 76%. However, the holding of both types of accounts is relatively low in the age ranges of 15 to 19 years old and 60 to 64 years old.

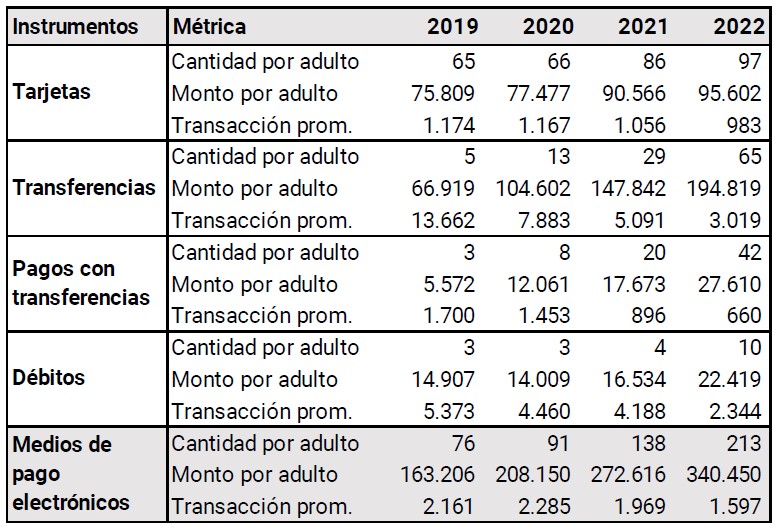

• Electronic means of payment (EMP) continued to set all-time highs. Each individual made an average of 17.8 monthly payments for MPE in 2022, a record value that practically triples the record prior to the COVID-19 pandemic. Those MPEs whose commissions are zero or reduced and the availability of the funds is immediate for the recipient (Transfers and Payments with Transfer) were highlighted.

• The use of mobile banking to carry out transactional operations in financial institutions (EEFF) grew significantly between 2019 and 2021. While around 10% of individuals with a bank account had carried out a transactional operation in the last quarter of 2019, the same indicator rose to 31% in the same period of 2021.

After the COVID-19 pandemic, a change in behavior is observed in the electronic channel chosen for transactions, with mobile banking gaining relevance over home banking.

• The average transaction with MPE fell for the second consecutive year (19% year-on-year in real terms in 2022). This performance, in a context where the real amounts operated by adults grew, indicates the advance of the use of electronic wallets and mobile banking in everyday payments since they involve payments for smaller amounts.

• Increases in returns had a positive impact on savings and investment products. In December 2022, the number of PH fixed terms in local currency was 6.9 fixed terms per 100 bank accounts in pesos, which represented a 53% year-on-year increase in this metric. Compared to 2021, there was a shift towards short- and medium-term products (mutual funds and fixed terms) and a contraction of account balances with immediate liquidity (account balances and money pools).

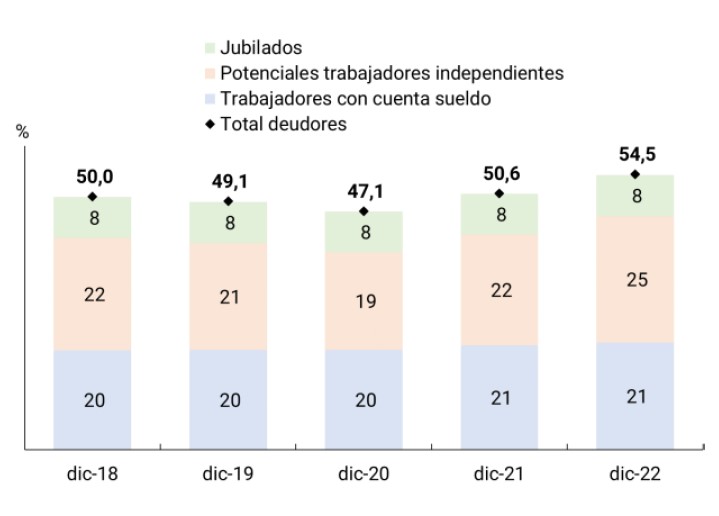

• As of December 2022, 54.5% of the adult population had financing from the expanded financial system (SFA). Consolidating two years of sustained growth, the number of PHs financed by the SFA had a net increase of 1.6 million during 2022 and reached 19.2 million in December. However, during the same period, the total PH financing balance in the SFA fell 13% in real terms, so the average balance per debtor continues on a downward path.

• The type of income significantly influences the level of the average debt balance of the PHs. As of December 2022, more than half of the PHs that registered credit products had a formal salary for their work in a dependent relationship or a retirement for having reached the corresponding age. PHs that have a salary register an average balance per debtor that doubles that of those debtors who would have an independent job.

• The number of MSMEs with SFA financing reached 1.04 million companies in December 2022, registering an increase of around 216,000 productive units compared to the same month in 2021. The financing balance registered a fall of 14% year-on-year at constant prices, due to the decrease in the average debt balance.

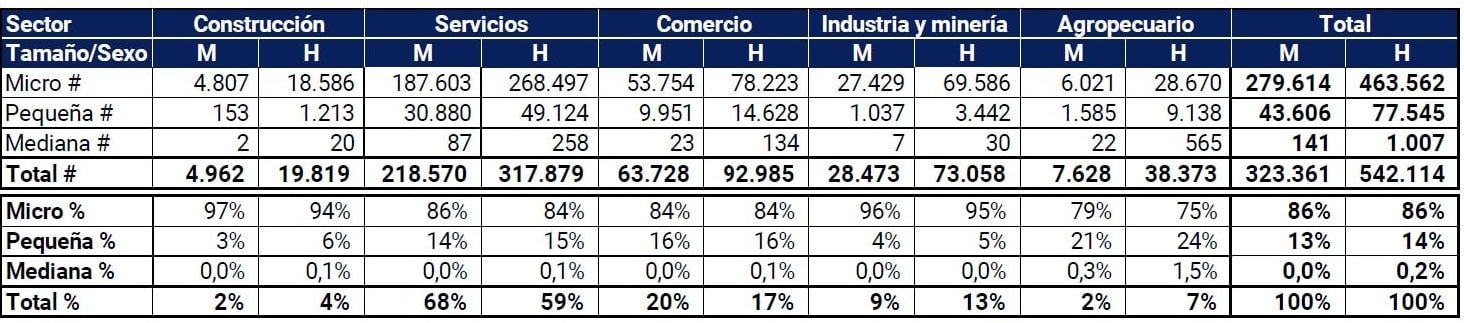

• The average balance of women’s MSMEs (MSMEs-M) is considerably lower than that of men’s MSMEs (MSMEs-H). As of December 2022, the average balance corresponding to PHs classified as MSMEs-M represented 47.6% of the average balance of an MSME-H, showing a gender gap in terms of the amount financed that remained at similar values during the last two years. The difference in average balance to the detriment of MSMEs-M is found in all sizes of companies (to a greater extent for the largest ones) and in all economic sectors.

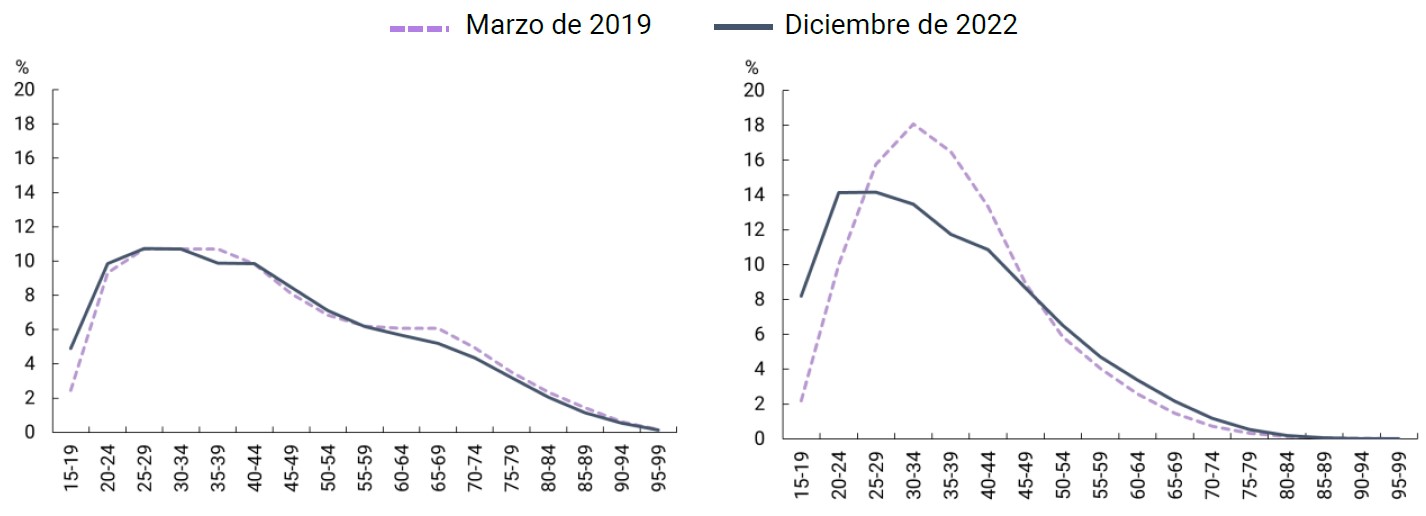

• Between 2019 and 2022, there was a deepening in the financial inclusion of young people (15 to 24 years old). The number of people with bank and/or payment accounts grew 27% between March 2019 and December 2022 (+7.6 million people). The age range of 15 to 24 years old was the one that contributed the most to this growth, accounting for 9.6 p.p. Information from the end of 2022 suggests that the number of young people opening their first account through an EEFF or a PSP is similar. In the case of access to financing, significant changes were observed between EEFF and PNFC. A greater inclusion of young age ranges is highlighted, mainly explained by the PNFCs.

Indicator Table | Financial inclusion in Argentina

Notes

(1) This includes access points for financial institutions (branches, mobile branches, ATMs, self-service terminals and complementary financial services agencies) and ATMs operated by non-financial institutions.

(2) Monthly average for each year.

Local context

In 2022, the financial inclusion process in Argentina was framed in a context of improved economic activity and the employment rate, a widespread use of mobile devices and, within the framework of the monetary policy implemented, a growing trend in reference interest rates.

Economic activity continued to improve during 2022 and reached levels higher than those of 2021. The Monthly Estimator of Economic Activity (EMAE) showed 5.2% annual growth for the year 2022 1 . Private consumption evolved along the same lines 2 , expanding by 9% in 2022 compared to the previous year.

In the labor market, the employment rate for the main urban agglomerations remained at historically high levels, reaching 44.6% in the fourth quarter of 2022. This mark is the highest since 2003, coinciding with the rate recorded in the second quarter of 2022. One of the features of this growth in the employment rate is that it is associated with the growth of the activity and employment rate of women to a greater extent than that of men3 . For its part, the income of salaried people showed a reduction of almost 3% in real terms in the second half of 2022 compared to the same period in 2021. However, differentiated behaviors were observed between those corresponding to registered and unregistered workers. Incomes in real terms contracted more for unregistered workers4.

For their part, the benchmark lending and passive interest rates showed an upward trend between June and September 2022, before stabilizing in the last quarter of the year. In the third quarter of 2022, the Central Bank of the Argentine Republic (BCRA) raised its monetary policy rate with the aim of preserving exchange rate and financial stability by bringing it to positive values in real terms. Between the end of June and September 2022, the monetary policy rate increased by 23 p.p., while the fixed-term rate increased by around 21 p.p. and the rate on signature document loans and personal loans rose by around 18 p.p. in the same period.

On the side of the perceived demand for financing, in the second half of 2022 financial institutions (FFSEs) continued to observe a reduction in the business segment (both small, medium and large)5. Regarding the demand for credit from households, the EEFF pointed to the support of the credit card segment and other consumer loans. Demand for collateral loans was relatively weak. At the same time, the BCRA maintained incentives for access to financing.

Access to digital infrastructure is essential to facilitate financial inclusion. Residential mobile internet accesses expanded by around 9% in the third quarter of 2022, reaching just over 32 million accesses6. In terms of cell phone subscriptions per 100 inhabitants, Argentina (130.5) was above the average for Latin America and the Caribbean (108) and for countries that share the same income category (upper middle, 123)7. The cost of fixed broadband services in Argentina, in terms of monthly gross national income per capita (GNI), was 14% above the average of a selection of Latin American countries and exceeds between 3 and 4 times the cost of developed countries such as Canada and the United States8. On the other hand, the cost of mobile broadband services in relation to the monthly GNI was 13% below the Latin American average and doubles the cost of developed countries such as Canada and the United States. For their part, users in Argentina spent an average of 3.9 hours per day on their cell phones, 8.3% more than the previous year9. In this sense, downloads of mobile banking applications and electronic payment wallets grew by 16% in 2022, reaching 42.8 million downloads10.

State of the situation. In this context, the state of financial inclusion stands out for an almost total coverage of the population in the holding of accounts, mainly bank accounts, and a greater participation of the population in electronic channels to carry out transactions (See Section 1). This increase is reflected in the dynamics of payments and transactions by electronic means, where the decrease in the average amount per transaction (in a context of an increase in the amounts operated per adult) indicates a greater penetration of digital payments in people’s daily lives. Likewise, in the last two years, the expansion of the PNFC as a source of financing for individuals (PH) was highlighted and, although to a lesser extent, contributions from public banks were also observed. Both providers explained the increase in PHs with financing, reaching the highest values in the series at the end of 2022. On the side of financing to MSMEs, the number of companies with financing experienced a significant increase in 2022, although credit balances fell in real terms.

During the second half of 2022, the BCRA and the National Government issued regulations that will contribute positively to financial inclusion. In the field of MSME financing, the extension of the Financing Line for Productive Investment of MSMEs was provided until September 2023. In connection with the initiatives to improve financing for MSMEs and with the aim of generating information on the use of digital products, the BCRA determined: (1) that unpaid MSME Electronic Credit Invoices (FCEM) be reflected in the Central Center for Electronic MSME Invoices Unpaid at Maturity (CenFIV), which seeks to provide information by generating a credit history in the use of this product11; and (2) the creation of the “Registry of platforms for MSME financing” in which all legal entities that offer tools, computer systems and platforms for carrying out operations with MSME electronic credit invoices must be registered12.

In terms of financing for households, the National Government included within the Ahora 12 Program, the purchase of nationally produced cell phones with financing of 10 installments and an APR of 48%. This measure has a positive impact on the use of digital financial services.

In order to protect depositors, the BCRA updated the upper limit of the coverage of the Deposit Guarantee Insurance System to $6 million per person, account and deposit in each EF. Fixed terms and balances in savings banks, among others, are covered by this coverage. In relation to savings, the Electronic Certificate for Time Deposits and Investments (CEDIP) was also created in order to expand the functionalities of time deposits and investments13. This new instrument will improve the liquidity of fixed terms since their ownership can be transferred by electronic means to cancel obligations, be traded on securities markets and be divided into amounts lower than the original amount. In this way, the average maturities of these placements could be extended, resulting in a greater availability of funds for longer-term loans by the EFSEs.

Finally, technological advances, the diversity of participants in the financial system and their interconnections, and the expansion of digital financial services, led the BCRA to update the standards on technology and information security risks with the aim of strengthening cybersecurity, fraud prevention and cyber resilience14, which are considered fundamental elements when it comes to adequately providing financial services to usersQuestion 15.

1. Financial infrastructure

The post-COVID-19 pandemic stage poses new challenges for the infrastructure for access to financial services. On the one hand, the growing adoption of digital channels transforms digital infrastructure into an indispensable element for access to financial services. In this context, the physical infrastructure works in a complementary way with digital channels to continue offering services in person, either due to the nature of the service or the population that demands it.

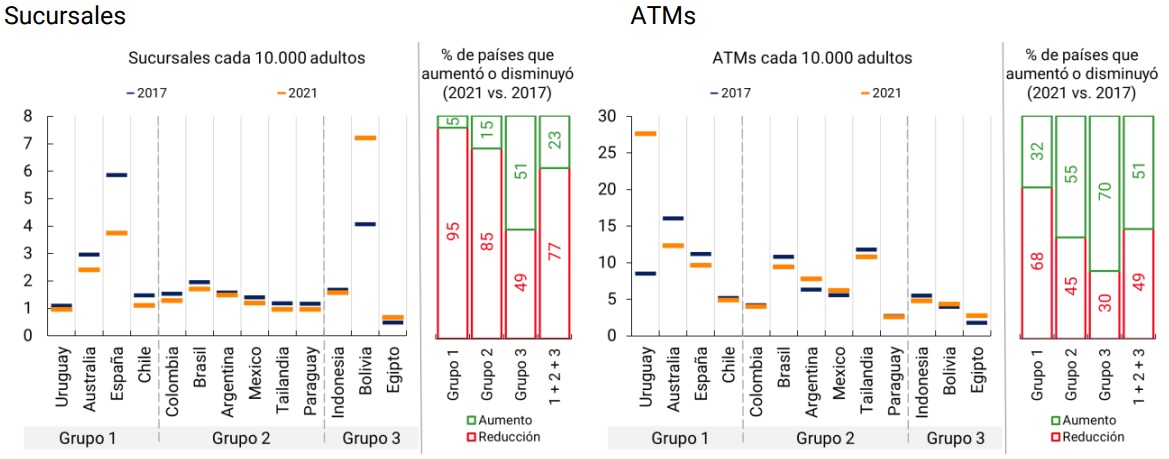

In relation to the adult population, the physical infrastructure at the global level registers a decrease in traditional financial service access points (PDAs). Branches experience notable declines in high- and upper-middle-income countries, while ATMs show the greatest reduction in high-income countries. In both cases, the reduction in costs by financial institutions (EFSE) and the greater progress of the digitalization of financial services, particularly in the area of payments, are some of the explanatory factors of this new scenario16 .

Graph 1 | Evolution of branches and ATMs

Note | Countries are grouped by their income level according to the World Bank’s classification. Argentina is among the group of upper-middle-income countries. Group 1: high-income countries; Group 2: medium-high and group 3: medium-low. “Increase” means that the metric per 10,000 adults increased between 2017 and 2021 and vice versa for reduction. For those countries that did not have records for the year 2021, the data corresponding to the year 2020 was taken.

Source | FAS, INDEC and BCRA.

Compared to the global trend and to upper-middle-income countries, branches in Argentina showed a very slight reduction and ATMs a significant increase (23% between December 2017 and 2021). In recent years, various regulations aimed to extend and modernize the ATM fleet17 and evaluate the impact on the coverage of branch closures prior to their implementation18.

On the other hand, cell phone ownership and internet use in Argentina are at levels very close to the average of high-income countries19, while mobile coverage20 almost reaches the entire population21. These values indicate that access to and use of information and communication technologies are widespread in our country, complying with one of the necessary conditions for access to and use of digital financial services. However, there are other factors, such as the quality of connection and the technological capabilities of the population, that must be considered to take advantage of and expand the potential of digital channels.

Graph 2 | Access to and use of information and communication technologies

Note | In all graphs, the 2022 data for Argentina repeat the values of 2021. The cell phone ownership graph shows the use of cell phones in our country (because there is no possession data). Mobile coverage: percentage of inhabitants within range of a mobile phone signal, regardless of whether they are users or not.

Source | INDEC and ITU.

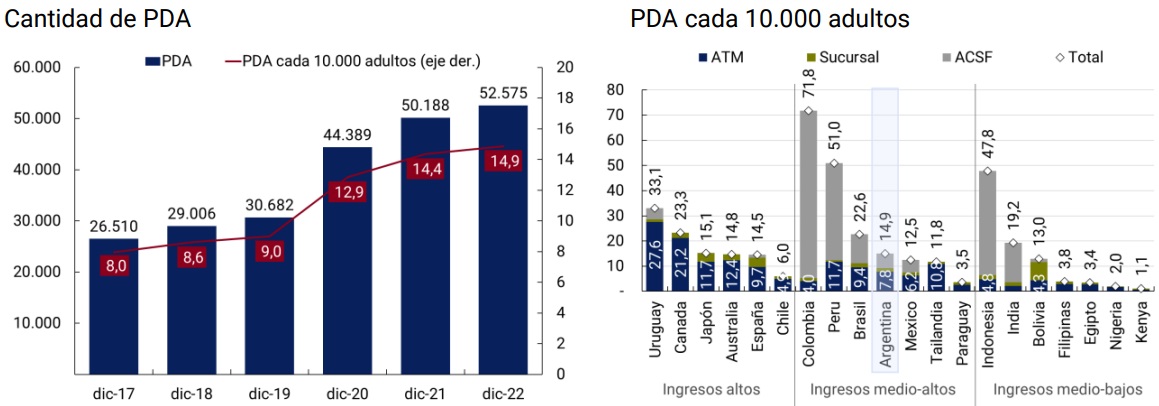

Physical infrastructure. Physical access points to financial services (PDAs) registered an increase of 4.8% compared to December 2021 and maintained at 92.5% the percentage of the adult population living in localities with PDAs. Likewise, the level of PDA per 10,000 adults is similar to values in high-income countries such as Japan and Spain, although in these countries ATMs predominate and the contribution of complementary financial services agencies (ACSFs) is marginal, while in Argentina the latter have greater relative weight, as in other Latin American countries.

However, the pace of growth of ADPs slowed compared to the previous two years (13% for 2021 and 45% for 2020) due to a decline in the growth of ACSFs and ATMs. This behavior could be explained by:

-

-

- (i) ACSF: these points rest mainly on existing extra-bank collection networks, where most of the service points are already enabled as ACSF. In 2022, the ACSF had a positive result with a 13% increase, although they registered a drop of 5.9% between June and December 202222.

(ii) ATMs: in general, the new equipment replaced existing units, generating a replacement of the device fleet, instead of an expansion. This replacement may have been prompted by the obligation for ATMs to offer biometric readers for user identification

-

- . ATMs slowed their growth from 4% in 2021 to 1% in 2022 in a context of greater use of electronic means of payment (EPM) and the expansion of alternative mechanisms for cash withdrawals.

Graph 3 | Financial Services Access Points

Note | Graph on the right: data to 2021 except Argentina to 2022.

Source | BCRA, FAS, networks and INDEC.

Likewise, the growth of payment accounts generated the need for an infrastructure that allows the holders of these accounts to make cash withdrawals and deposits. To do this, businesses that can be registered as ACSF and bank and non-bank ATMs are used. In this way, the physical infrastructure of financial services incorporates new use cases as interoperability between the different types of accounts and the application of technology is enhanced.

Finally, branches ended the year with a decrease of 1.5% compared to December 2021, cushioning the global trend 24. These closures occurred in localities where there was at least one other branch and other PDAs, so their inhabitants still have human service points and electronic devices to access financial services.

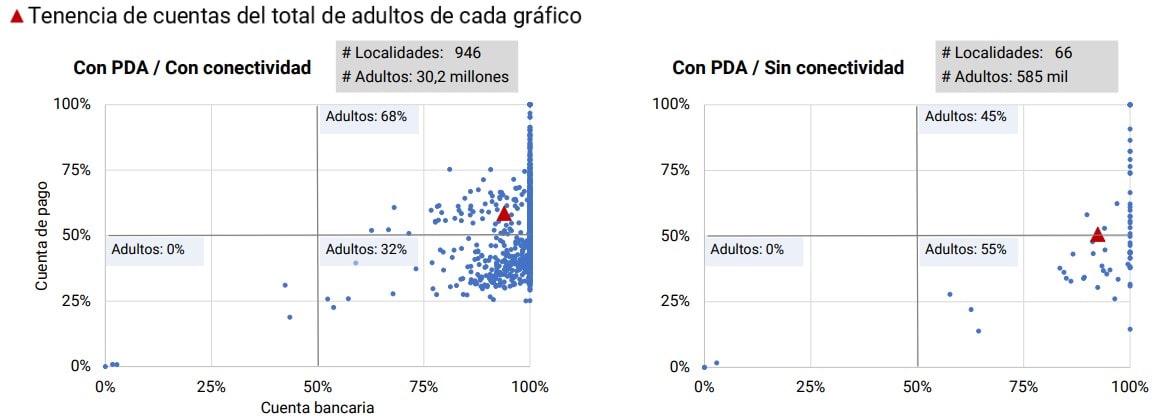

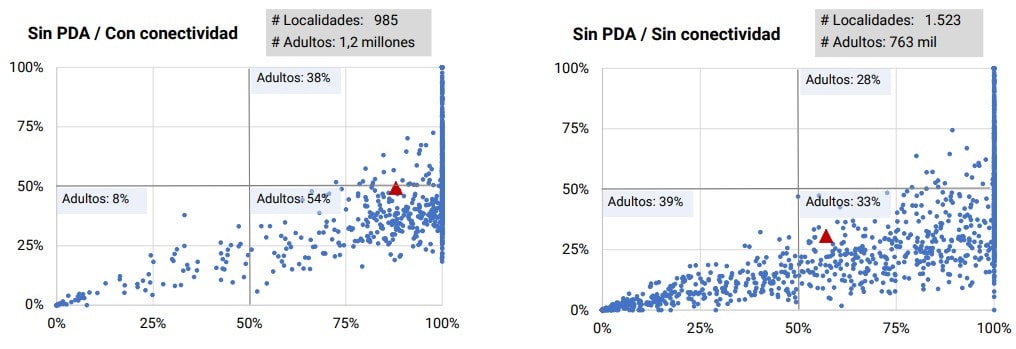

Availability of infrastructure by locality. The physical infrastructure of the financial system provides services for the different types of accounts: EEFF account holders can use all types of PDAs, while people with payment accounts mainly use ATMs, both bank and non-bank, as a cash withdrawal point 25. In this way, part of the physical infrastructure is shared by payment service provider (PSP) and EEFF customers, while another part is for the exclusive use of bank account holders. On the other hand, telecommunications infrastructure allows the use of digital financial services for both sets of users. In this context, the question arises as to whether the presence of infrastructure favors the possession and use of bank and payment accounts.

From the combination of availability of physical and telecommunications infrastructure, four subgroups of localities are obtained that present different configurations in terms of the possession of bank and payment accounts of their population. For the availability of physical infrastructure, those localities that have at least one branch and another type of PDA are counted, which implies that the locality has a full offer of face-to-face financial services26. In terms of availability of digital infrastructure, the localities that report both fixed and mobile Internet connectivity are counted, which allows the use of electronic channels from the computer and cell phone.

Localities with a full offer of face-to-face financial services and internet connectivity concentrate 87% of the country’s adults and show very high levels of bank and payment account ownership. The population that lives in these localities presents very favorable initial conditions for access to financial services both in terms of account ownership and infrastructure. Likewise, these conditions favor the acceptance of electronic means of payment by local businesses and the exchange of funds between its inhabitants (positive synergies). Also, it is expected that the possession of payment accounts will grow in these localities attentive to the availability of internet connection.

On the other side of the spectrum, localities without full offer of face-to-face financial services and that did not report the two types of connectivity group a significant number of localities, although with smaller populations that together account for 2% of the total adult population. This infrastructure configuration presents more localities with a smaller proportion of their population with bank accounts and payment accounts.

Another aspect shown in the graph is the association between the existence of PDA coverage in the localities, regardless of whether or not they have internet connectivity, and the percentage of the adult population with a bank account. While the point cloud tends to be distributed with variability within the entire range of bank accounts (0% to 100%) when localities do not have PDA, this same ratio becomes concentrated in higher percentages above 80%) when localities have PDA. With regard to connectivity, it is observed that localities with a fixed and mobile Internet connection tend to register a higher percentage of the population with a payment account.

Figure 4 | PDA & Internet Coverage & Account Holding

Note | PDA data as of Dec-22, accounts as of Sep-22 and connectivity as of Aug-22. With PDAs: at least one branch and another type of PDA. With connectivity: fixed and mobile connectivity. Bank account: percentage of the adult population with at least one bank account. Payment account: Percentage of the adult population with at least one payment account. The light blue boxes indicate the percentage of adults living in the localities of each quadrant (out of the total localities of the combination).

Source | BCRA, networks, ENACOM and INDEC.

Although there are several factors that can impact the holding of bank and payment accounts (such as the level of education and income, age, associated costs, among others), the availability of infrastructure is presented as a necessary condition for access to and use of financial services. Those localities that offer a more favorable physical and telecommunications infrastructure register greater account ownership.

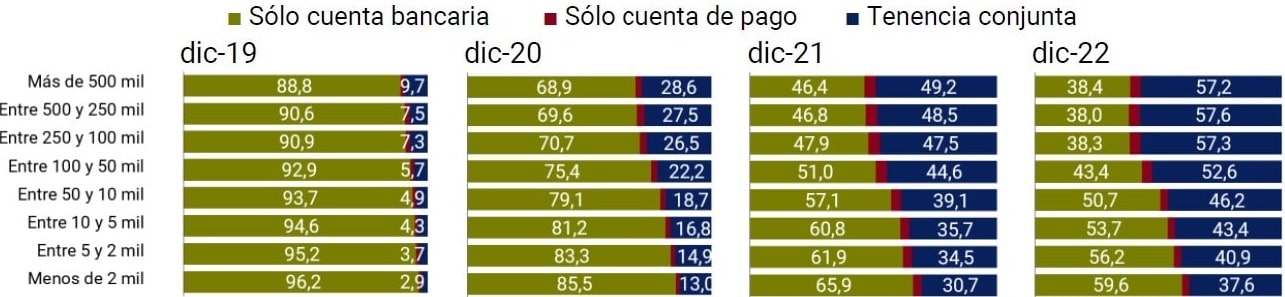

2. Account Holding

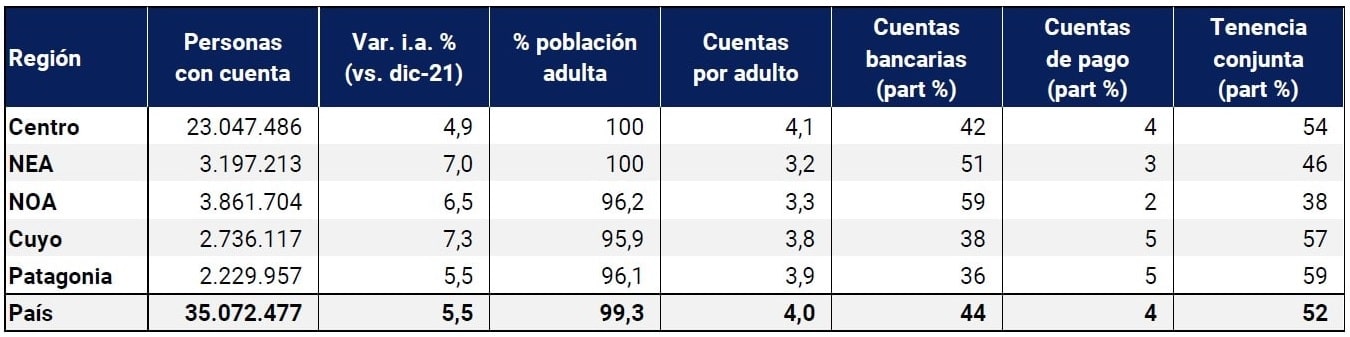

Account holding levels are approaching the total coverage of the adult population. The number of human persons (PH) who had at least one account stood at 35.1 million as of December 2022, which represented 99.3% of the adult population. With values above 95%, the NOA, Cuyo and Patagonia regions were at account holding levels close to full coverage while the Center and NEA have already reached it. This shows that widespread access to accounts is a federal phenomenon.

Table 1 | Bank and payment account holding metrics

Data as of December 2022

Note | Bank accounts: people who only have this type of account and do not have payment accounts; Payment accounts: people who only have payment accounts; Joint tenancy: people who have bank and payment accounts; Accounts per adult: considers accounts in Argentine pesos and foreign currency; % adult population: takes as a denominator the projections of the adult population made from the results of the 2010 National Census. Estimated growth rates may differ from actual rates and thus overestimate account holding levels.

Source | BCRA based on COELSA and INDEC.

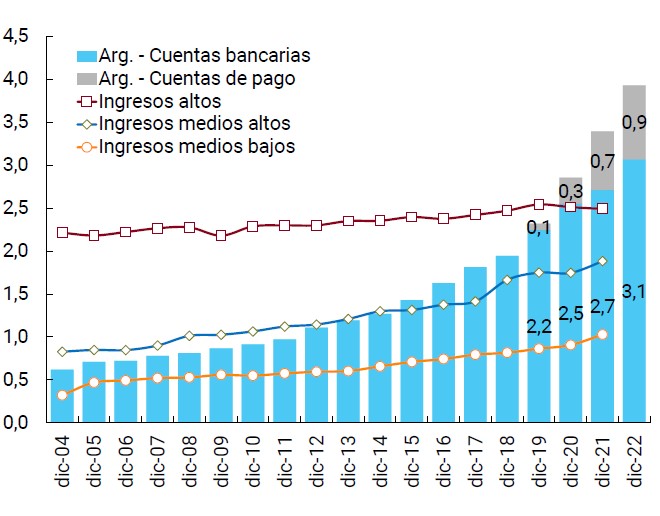

In terms of the number of accounts per adult, a metric commonly used internationally to compare account ownership between countries, Argentina has recorded continuous growth over the past 15 years, exceeding the average levels of high-income countries in recent years27. A particular characteristic of the Argentine economy is the existence of bi-monetary savings banks (i.e., in pesos and in foreign currency), thus providing accounts in foreign currency with an additional margin (about 0.6 accounts per adult) in the explanation of the value achieved.

Since the beginning of the COVID-19 pandemic, bank accounts have grown significantly, although starting from a high level of coverage (2.4 accounts per adult28), while payment accounts, being a more innovative product at that time, experienced a significant adherence in the adult population. This is reflected in the fact that more than half of the adult population simultaneously owns payment accounts and bank accounts.

The motivation to add a payment account (to the possession of bank accounts) usually lies in the use of specific services of this type of product such as e-commerce, the use of electronic means of payment offered by these accounts in stores and a simpler user experience for both opening and operating. Likewise, the distinctive feature of payment accounts is that they are opened and operated 100% digitally, from a computer or mobile device29. This requires internet connectivity and certain technological capabilities of users, as it does not have its own physical service points.

Graph 5 | International comparison of the number of bank accounts per adult

Note | Argentina: between 2019 and 2022, data from COELSA were used, while from 2004 to 2018, data from FAS (IMF) were used. Accounts in Argentine pesos and foreign currency are included. Other countries: Only bank accounts are considered.

Source | World Bank, BCRA and FAS (IMF).

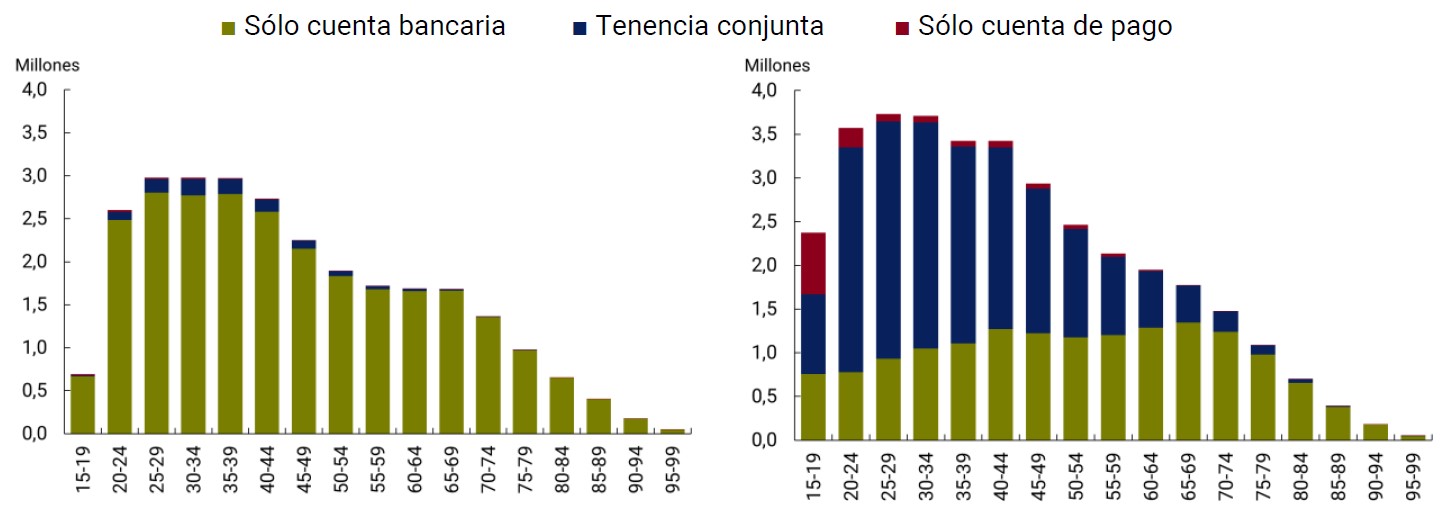

Characteristics of bank and payment account holders. Prior to the COVID19 pandemic, joint account holding comprised 8.5% of the adult population. Then, given the need to carry out transactions remotely, PHs with both accounts experienced significant growth and, currently, are at values greater than or close to 50% of the adult population, both nationally and regionally. Given the relevance of this phenomenon, it is interesting to know some attributes of the people who make it up.

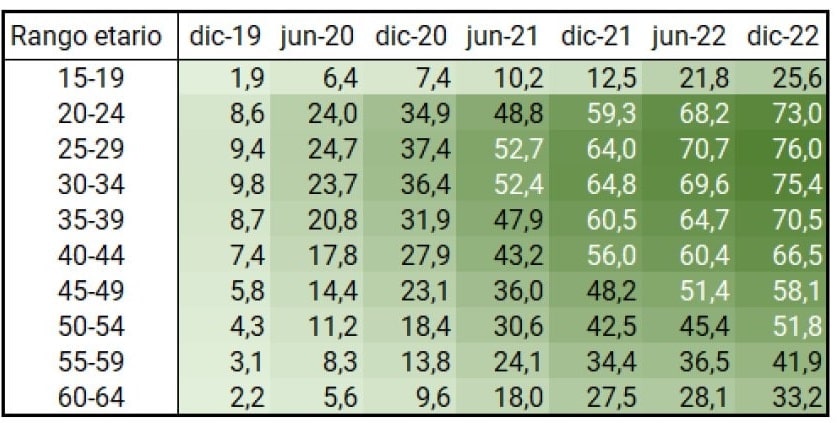

Age profile. The proportion of young people aged 20-29 and middle-aged 30-54) with joint tenure exceeds the proportion of people with only bank accounts. Conversely, in the very young (15-19 years) and older age (55 years or older) age ranges, the proportion of people who own both types of accounts is lower. While the holding of both types of accounts decreases as age increases, the levels of tenure are now high. Older people probably prefer to carry out financial transactions in environments where they feel comfortable and that eventually have the possibility of carrying out operations in person, an aspect that only bank accounts provide.

The latter is similar to the use of cell phones, computers and the internet, which is at high levels in all age ranges, but decreases as age increases. It is estimated that more than 90% of young and middle-aged people use the internet and mobile phones, while among people over 64 years of age only 59% use the internet and 74% use cell phones30. Thus, the gap of elderly people who use their cell phones without connecting to the internet amounts to at least 15 p.p31. In this way, the technological factor plays a fundamental role in explaining the differences in account ownership between age groups since, in order to open a payment account and carry out operations, cell phones with an internet connection are required.

Table 2 | Persons with joint account holdings in relation to the adult population

Expressed as % of the population of each age range

Note | The shades of green in the cells are determined by the minimum and maximum value in the table. The age range is expressed in years.

Source | BCRA, COELSA and INDEC.

When grouping the ages by five-year groups, three effects can be seen with respect to joint account keeping: (i) throughout the period of analysis, significant increases were recorded in all five-year groups. The changes experienced in the COVID-19 pandemic regarding interaction with financial services modified the habits of use of financial services of all population groups; (ii) people who are between 25 and 34 years of age have a clear preference for simultaneous possession of bank and payment accounts, as this would allow them to use the financial services of both accounts that are interoperable. Then, as age advances, the preference for joint account ownership is diluted and, from the age of 55, people prefer exclusive bank account ownership, although it is not as clear as it was years ago and iii) the evolution of the different age groups between December 2019 and the same month in 2022 was not uniform. The groups under 30 years of age grew in a similar way in 2020 and 2021; while the higher age groups tended to grow less during the first year of the pandemic and more in the following year32. Thus, the youngest were the ones who in relative terms adopted digital financial services the fastest.

Geographical profile. The growth of joint account tenure is a cross-cutting phenomenon for all localities, regardless of their population density. Although it became especially relevant in urban centers (greater than 50 thousand adult inhabitants), where the population with both accounts represented more than 50% of the PHs with accounts, localities with lower population density experienced significant increases, reaching participation levels between 30% and 40%. Thus, the percentage differences between urban centers and less populated localities narrowed over time.

Between December 2019 and 2022, the proportion of people with both accounts in localities with less than 10 thousand adults went from values close to 3.5% to values around 40%. Although the improvement in telecommunications infrastructure could have influenced this increase, this factor does not explain the differences between the localities with the highest and lowest population density, given that the availability of internet access in localities with less than 10 thousand adults is high33.

Likewise, as mentioned in the Financial Infrastructure section, cell phone ownership, internet use and mobile coverage in Argentina are at very high levels, close to the total coverage of the population. In this sense, access to technology would be covered in both localities with low population density and those with high population density.

Graph 6 | Distribution of people with accounts according to the size of the locality

Data expressed in %

Source | BCRA, COELSA and INDEC.

However, other factors associated with the locality, such as the quality of internet connection and the level of financial development, could influence the decision to open a payment account by its inhabitants. In the first case, localities with lower population density register average download speeds for fixed internet much lower than the most populated localities34. On the other hand, when analyzing the situation of the less populated localities in terms of their financial development, it is observed that as population density falls, the localities register weaker development indicators35. This could be linked to lower average incomes that make it difficult to pay for telecommunications services in line with digital financial services. Both aspects of localities discourage the use of digital financial services (and, therefore, the opening of a payment account), with people having as an alternative the use of financial services banking points such as branches or ATMs.

3. Electronic means of payment and savings and investment modalities

3.1. Electronic means of payment

The use of electronic means of payment (EMP) contributes to improving financial inclusion. MEPs make it possible to channel the different payment needs of the population and, indirectly, can make access to new financial services, such as savings or financing products, affordable for their users36. The BCRA, considering these aspects, has promoted through its regulation the creation of new means of payment, the adoption of technology, the reduction of commissions and the crediting times of funds for businesses.

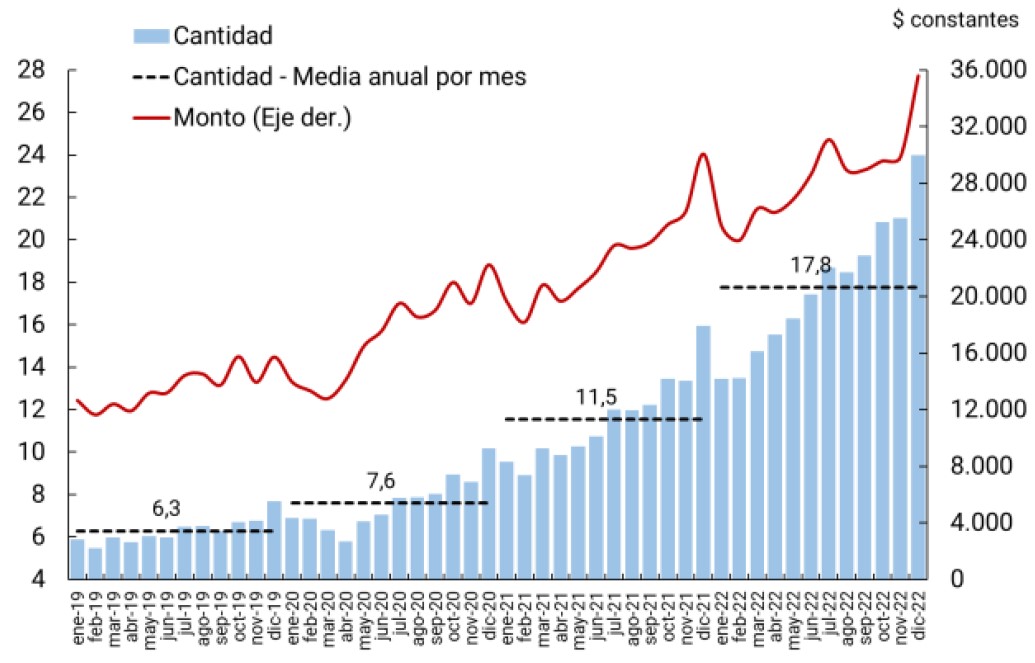

Volumes and amounts transacted. In this context, the amounts of operations carried out through MPE increased their participation in the Gross Domestic Product (GDP), from 54% in 2021 to 66% in 202237. Individuals (PH) continued to increase the use of MPE38 in the second half of 2022, particularly those whose commissions are zero or reduced and the availability of funds is immediate for the recipient (Transfers and Payments with Transfer -PCT-).

Figure 7 | Transactions with electronic

Year-on-year rates of change (YoY)

Year-on-year rates of change (YoY)

Note | “Avg. Transaction” corresponds to the quotient between the amount and the number of transactions. The “Payments with Transfers” category includes transactions initiated with cards. Amounts at constant prices of January 2019 (CPI January 2019 = 100).

Source | BCRA, INDEC and networks.

In 2022, the number of transactions per adult grew by 54% while the amount transacted per adult increased by 25% in real terms. Each individual made an average of 17.8 monthly payments for PEMs, which is a new record value and almost triple the pre-COVID-19 pandemic record39. The downward trend in the average transaction, which fell by 19% in 2022, shows, in a context where the amounts operated per adult grew, the advance of digitalization in the daily payments of PHs since they usually involve relatively smaller amounts to face their daily transactions. This dynamism is also reflected in the growing relationship between PEMs and cash withdrawals. In 2022, $5.1 was recorded through MPE for every $1 of cash withdrawal, compared to a ratio of $3.5 to $1 in the previous year40.

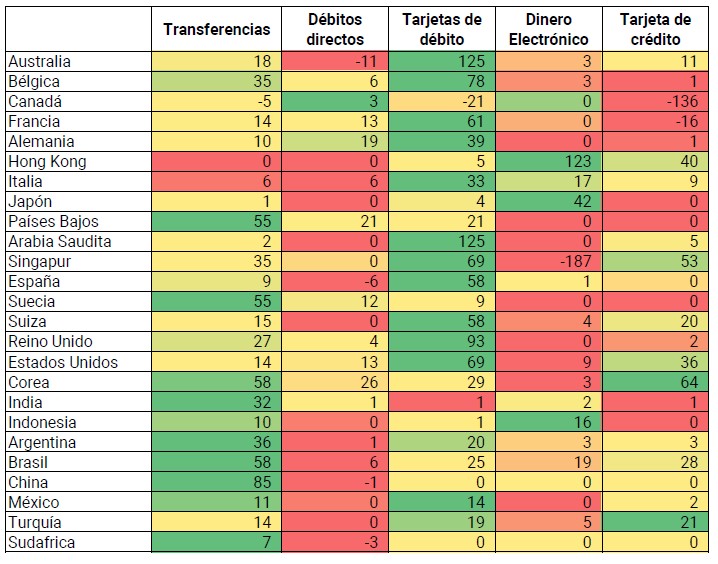

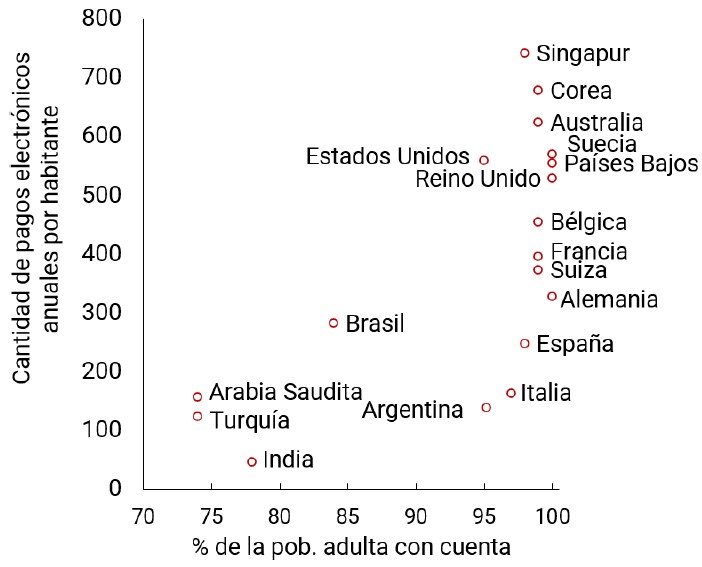

International comparison. At the international level, the global trend towards the digitization of payments, accelerated by the COVID-19 pandemic, is independent of the income level of countries, as both high- and middle-income economies increase their operations year after year in terms of population.

Figure 8 | International comparison of retail electronic payments

Var. of operations per inhabitant. (17 vs. 21)

Annual Payments and Account Holding (2021)

Note | The data for Argentina are sourced by the BCRA and correspond to the metric per adult. Data for the remaining countries are from BIS and Global Findex (graph left and right, respectively). Of the series published in BIS, the following are considered to make up the set of retail payments: transfers, direct debits, debit and credit cards, and electronic money payments (e-money payments). Table on the left: Colors are generated by each row based on the minimum and maximum value.

Source | BCRA, BIS (Committee on Payments and Market Infrastructures) and World Bank (Global Findex 2021).

Argentina, in terms of population coverage of accounts (bank and/or payment), registered a level of annual PEM operations per adult below that of countries with similar coverage. This fact indicates that MEPs have room to continue growing at the local level, although significant variability is observed between countries with a high percentage of their population with accounts. On the other hand, there is also an outstanding performance in the growth of the use of PEMs in Argentina between 2017 and 2021 from an international comparison41.

High-income countries (including Australia and Korea, in the table in Figure 8) tended to expand their use of debit cards between 2017 and 2021, while upper-middle-income and low-income countries expanded through the use of transfers. In the case of the former, the growth in their use would be associated with contactless payments, while the development of instant or fast payments contributed to the increase in transfers42. Contactless card payments do not require cardholders to sign a receipt or enter a personal identification code at point-of-sale (POS) terminals, as long as the transaction does not exceed a certain value. In this way, it tends to simplify the operation and speed up its use. Instant payment systems can be used at any time of the day, the funds are immediately available to the beneficiary43 and have lower costs than other means of payment.

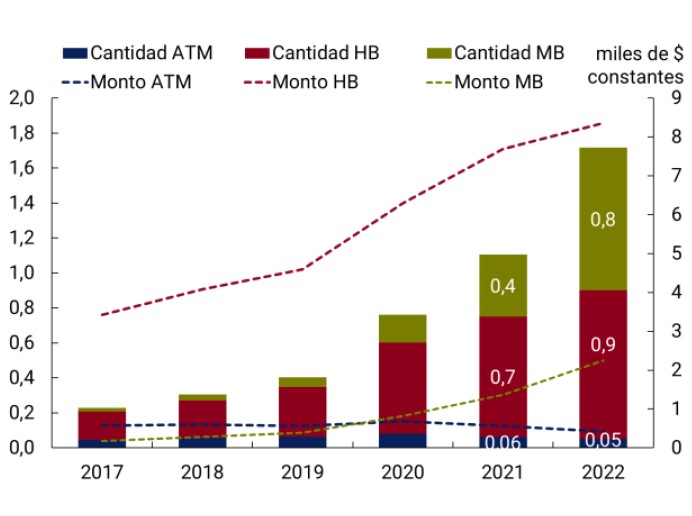

Physical payment infrastructure. The expansion of the POS44 and mPOS (mobile POS) terminal park continued during 2022. mPOS devices reached around 4.4 million devices, an all-time high in the series, with a year-on-year growth of 17%. For their part, POS terminals registered a monthly average of around 840,000 units during 2022, 5,000 more than last year. Although the total number of POS remains without significant changes since 2019, the active terminals indicator exhibited improvements, reaching an average of 60% in 2022, compared to values of 57%, 53%45 and 58% in 2019, 2020 and 2021, respectively. The significant expansion of mPOS units could be explained by their low acquisition and maintenance costs as well as their ease of transport and use.

Card purchases show improvements in the intensity of use of POS terminals (both in amount and quantities per device). On the other hand, in mPOS operations, there is a small increase on the side of the number of operations per device and a reduction in the average amount46. A structural aspect to highlight in the historical series of payments made by both terminals is that the average purchase in an mPOS terminal is systematically lower than the average value of a transaction per POS47.

The devices in terms of the population, the number and the amount of operations channeled in each of them, allow us to infer the profile of the businesses or entrepreneurs that use each tool. mPOS, which have a greater relative reach, would be used by small merchants, arguably, less frequently than the use of a POS terminal. These merchants, given their smaller structure, could charge a substantial part of their sales in cash and channel some operations through these cheaper devices, which would explain the low rate of transactions per unit. Regardless, mPOS would meet the demand for electronic payments from users who previously might have operated entirely in cash at those merchants. On the other hand, the X-ray of operations in POS assumes that they would be larger businesses, which would channel a significant part of their sales through these devices.

Table 3 | Stock, quantity and amount of operations in POS and mPOS devices

Note | Device operations: Monthly averages of operations per device for each year. Debit card payments at POS and payments with all cards at mPOS. Amount by device: Monthly averages of the amount in real terms per device for each year.

Source | BCRA and INDEC.

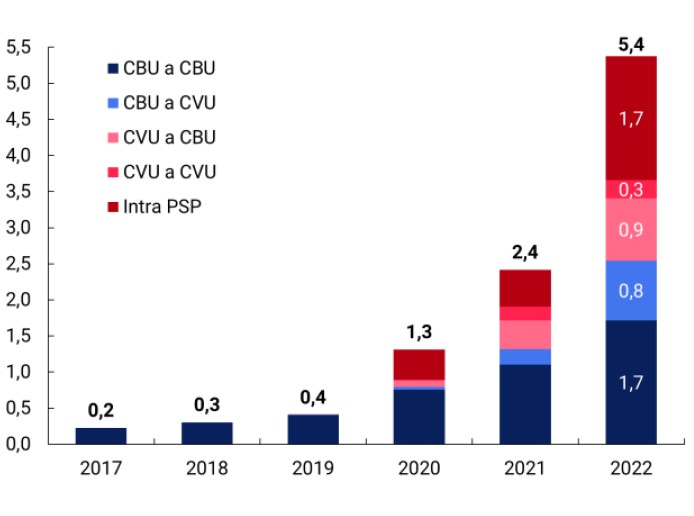

Wire transfers. In 2022, each adult made an average of 5.4 transfers per month, more than double those made in 202148. The contribution of transfers initiated on mobile devices (originating from a payment account and those made via mobile banking) to the year-on-year variation in total transfers was very significant49. Thus, 2 out of 3 total transfers per adult would have originated on mobile devices. This is reflected in the drop in transfers through ATMs in the last two years, a fact that suggests a replacement of this channel by the remaining50.

In all transfers between financial institutions (EEFF) (CBU to CBU), mobile banking continued for the sixth consecutive year to register the highest year-on-year rates (3 digits in the last 3 years51). There is an upward trend in the amounts channeled through mobile devices, although only 39% of the total transfer amounts per adult were processed through these means in the period. This phenomenon would reflect the growing habit of people to carry out more and more daily operations through a cell phone for relatively low amounts. This goes hand in hand with the more intensive use of cell phones (88.1%) by the population52 and the increase in mobile banking to carry out transactional operations (See Section 1).

Figure 9 | Transfers per adult

Total Quantities

CBU to CBU Transfers by Channel

Note | Monthly averages for each year.

Source | BCRA and INDEC.

Transfers from CBU to CBU via home banking continued with the highest concentration of amounts. In this way, when it comes to trading larger sums, individuals continue to prefer home banking. Unlike cell phones, personal computers are used by 42.3%53 of the population. On the flip side, the reduced use of computers by individuals could pose a challenge in the face of the need to transfer larger sums.

On the other hand, the importance of having interoperable systems was reflected once again in the evolution of transfers between bank accounts and payment accounts. During 2022, the amounts per adult of “cross-transfers” practically tripled, a situation that was also verified in the amounts per adult, although in a more attenuated way.

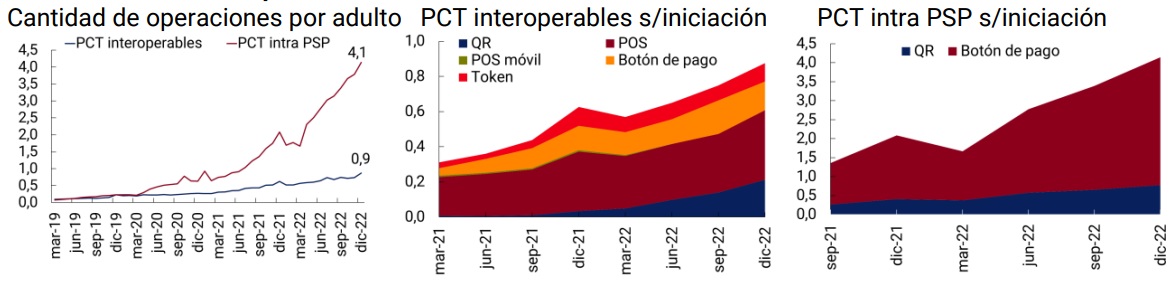

Payments with transfers (PCT)54. In 2022, each adult made an average of 3.5 monthly payments through PCT, registering an increase of 123% compared to the previous year, representing 2 out of 10 payments by electronic means per month. The amounts per adult grew by 63% at constant prices, while the greater intensity of use implied a reduction in the amount of the average operation at constant values (-27%). The evolution of these indicators suggests that the impetus for the increased use of PCT is explained by intra-PSP operations. These transactions are carried out between customers of the same payment service provider (PSP) with funds available in the payment accounts, initiated through the reading of a QR code or a payment button.

Table 4 | Transfer payments

Note | The contribution of Interoperable PCTs to the a.i. variation is defined as the change between 2021 and 2022 of Interoperable PCTs, divided by the total value of PCTs in 2021. In the same sense, the contribution to variation is defined. i.a. of the PCT Intra PSP.

Source | BCRA.

The “interoperable PCTs”55 had a year-on-year growth of 64% in quantities per adult, mainly driven by operations initiated through the reading of QR codes, which accounted for 24 p.p. of the aforementioned variation. Transactions initiated via this technology registered a remarkable dynamic, multiplying by 10 and representing 16% of the total of “interoperable PCTs”. The amounts per adult via “interoperable PCTs” had a modest variation (+15%) and a drop in the average value of each transaction, thus showing their most widespread use for everyday transactions.

Intra-PSP PCTs continued to grow at high rates (a.i. rate 143%), although there is a slight slowdown. In this case, payments initiated through a payment button, associated with non-face-to-face e-commerce, accounted for 80% of the total. The amounts of PCTs within PSPs also registered a significant increase.

Figure 10 | Interoperable PCTs and intra PSPs

Note | “S/”: According to. Source | BCRA and INDEC.

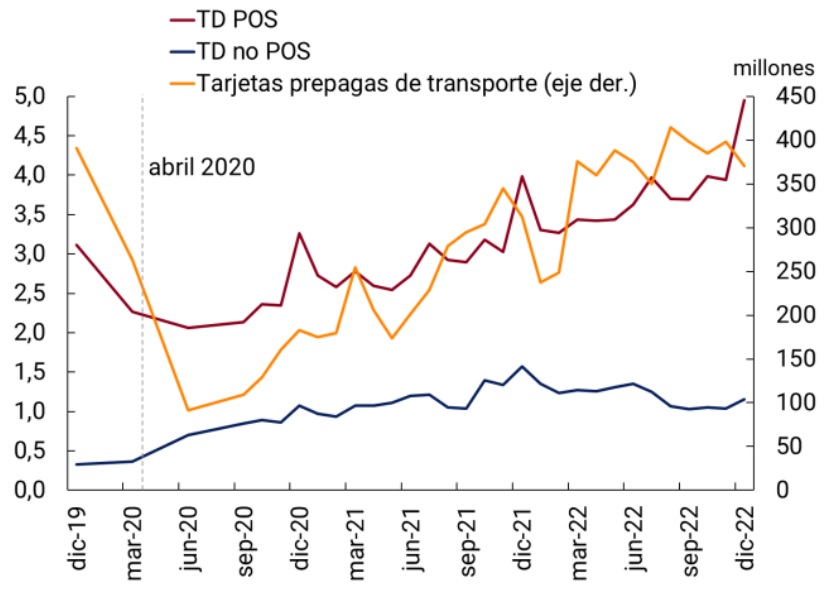

Debit card. In 2022, debit card payments continued their uninterrupted growth in terms of amounts per adult (+21%). Of the total monthly electronic payments, on average each individual made 1 out of 4 debit card transactions. The variations in the amounts per adult were more modest (+8%) with the consequent further fall in the average value of each operation (-10%). This reduction is registered in most MPEs and, as noted in the last IIF, this would show a greater penetration of the debit card in the daily payments of the population. In this sense, the participation of debit cards in supermarket sales increased 2 p.p. in 2022 compared to 2021. While in sales in wholesale self-service stores it grew by 1 p.p. in the average of the year 202256.

The growth in debit card payments was driven by transactions made through POS. The year 2022 closed with an increase in these payments (27.5%) higher than those channeled through the rest of the channels (mPOS, QR codes and remotes; 3%). In the case of amounts per adult, this behavior was even more pronounced given that there was a reduction in the amount per adult via mPOS, QR codes, and remote operations.

Figure 11 | Number of debit card transactions per adult

Note | TD: debit card. POS: Point of sale terminals. Non-POS: includes debit card transactions channeled by mPOS devices (mobile POS), QR code reading and remotely.

Source | BCRA and INDEC.

This breakdown, after two years of lower relative growth in payments made through POS compared to the remaining modalities, could be associated with the normalization of face-to-face activities. In particular, in general terms, there is a positive relationship between the evolution of operations with prepaid transport cards (proxy for the level of face-to-face activity) and payments with debit cards via POS devices. Thus, 76% of debit card payments were made in these units in 2022, 4 p.p. more than a year earlier. This behavior was not associated with a significant increase in the stock of POS devices since the variation in the average of the units that registered at least one operation in the month was equal to 4% during 2022 (see Physical payment infrastructure).

3.2. Savings and investment modalities

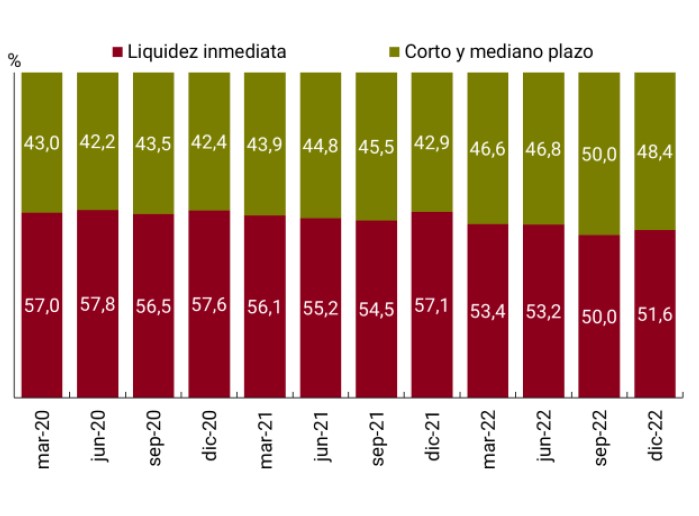

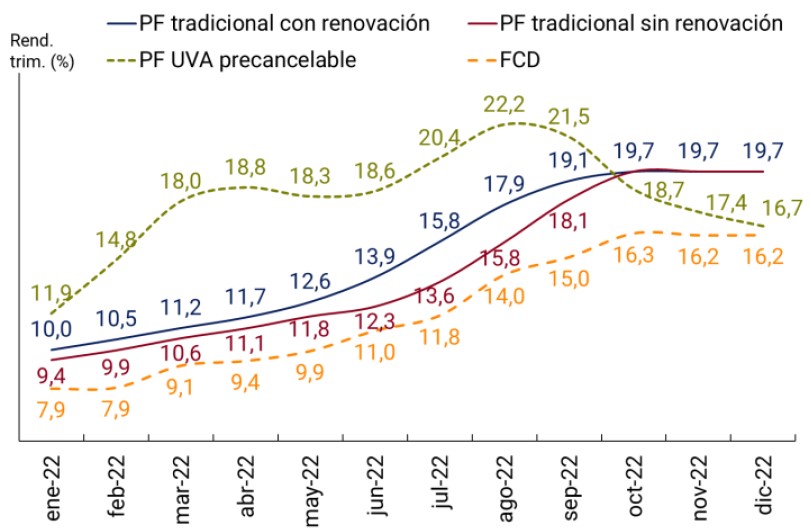

Individuals (PH) have the possibility of allocating their money among various savings and investment products, depending on their liquidity objectives, term and risk-return ratio57. As of December 2022, considering the products offered by financial institutions (EEFF) and Payment Service Providers (PSPs), the savings and investment balance of PHs represented 8.7% of the Gross Domestic Product (GDP) in 2022. Over the last three years, immediate liquidity products (account balances and in Mutual Funds (DCFs)) maintained a relevant (but decreasing) share of total savings and investment balances. For its part, in December 2022, short- and medium-term products registered a 48.4% share of total savings and investment balances. This share is the second highest value since the beginning of the COVID-19 pandemic, which could be related to the will to maintain the purchasing power of the capital saved and invested.

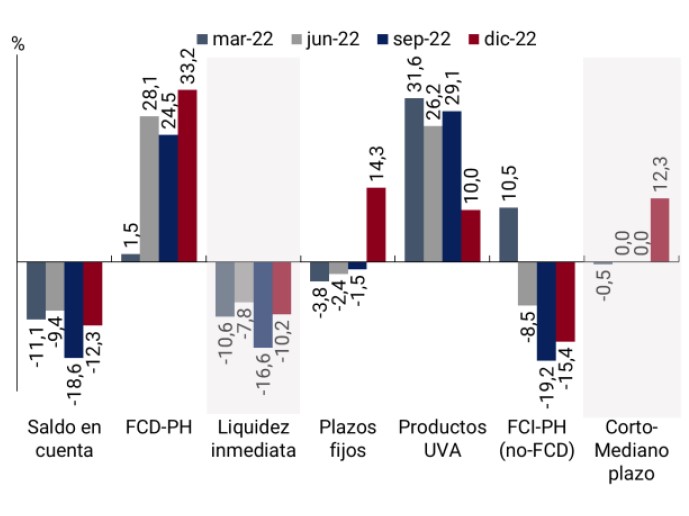

In the last year (Dec-21 vs. Dec-22), a 0.6% reduction was observed in the real savings and investment balances of PHs, partly explained by a 10.2% drop in immediate liquidity balances. This drop was partially offset by a 12.3% year-on-year increase in short- and medium-term products. The variations recorded in each instrument operated in different directions. Balances in traditional fixed terms and in Purchasing Value Units (UVA) increased by 14.3% and 10% respectively, while balances in Mutual Funds (non-CDF FCIs) registered falls of 15.4%.

Figure 12 | PH savings and investment product balances

Participation

Year-on-year rates of change

Note | The balances of the savings and investment products of the PHs in local currency and foreign currency are considered. Balances at constant prices in January 2019 (CPI January 2019 = 100).

Source | BCRA and CAFCI.

In terms of financial inclusion, it is relevant to investigate whether the increase in real balances in UVA, CDF, and traditional fixed-term products was accompanied by an increase in PHs’ use of savings and investment products. For this analysis, based on the statistical information available, traditional fixed terms and UVA without pre-cancellation option (hereinafter, “fixed terms”), and DCFs subscribed through payment accounts, are considered as a single set.

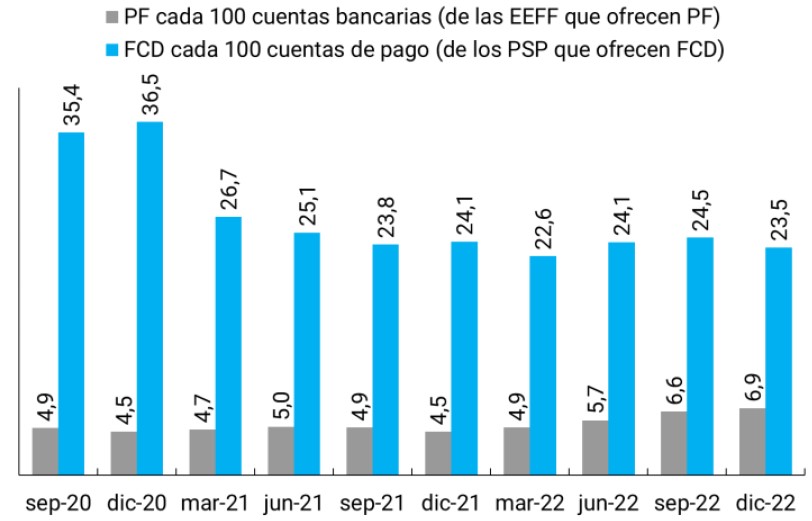

In December 2022, the number of PH fixed terms in force stood at 6.9 units per 100 bank accounts58, reaching the highest point in the last 4 years. During 2022, the metric in question grew 53% due to a significant increase in the number of fixed terms close to 70%. The increase in the real monthly interest rate on fixed-term deposits towards positive values during the last four months of 2022 could be associated with the increase in their amount. As can be seen in Graph 13, the evolution of the metric shows a greater use of this savings product in terms of bank accounts, which could indicate a greater participation of PH in this product.

For its part, PH accounts in PSP with balances in FCD went from 3.7 million in December 2021 to 5.6 million in December 2022 (+36%). This growing adherence is reflected in the fact that 23.5% of payment accounts registered balances in DCF in December 2022. It should be noted that as of December 2022, the number of PHs with payment accounts reached a figure of 19 million PH, registering a net increase of 3.4 million, compared to the same month of the previous year.

Figure 13 | Human persons. Evolution of the number of fixed terms and CDFs in PSPs with respect to the account park

Note | The number of fixed-term certificates includes fixed terms in ARS and UVA without the option of pre-cancellation. Bank accounts and payment accounts include those nominated in ARS belonging to PH and located in the EEFF and PSP that offer fixed terms and FCDs respectively.

Source | COELSA and BCRA.

Short and medium-term products. In 2022, the balances in DCFs and UVA products grew steadily at year-on-year rates close to 35% and 10%, respectively, although the balance of each of these products still represents a small portion of the volume of traditional fixed-term loans (DCFs by 8% and UVA products by 9% in December 2022). For its part, the balance in traditional fixed terms began to grow again in the fourth quarter of 2022.

The increases in the minimum interest rate for fixed-term deposits in pesos for PH during 2022 had a positive impact on retail savers, as they caused certain savings and investment alternatives to offer a more attractive return59. In particular, the growth in the balances of traditional fixed terms, FCDs in pesos and fixed terms in UVA with a pre-cancellation option could be due to the increase in the returns of these investment instruments.

Under the assumption that the saver places or subscribes an amount of money on the first day of each month and withdraws or redeems it after 90 calendar days, the quarterly return of 4 savings alternatives to investment was calculated:

- (i) Traditional fixed terms in pesos with automatic renewal every 30 days, until the 90 days are completed;

- (ii) Traditional fixed terms in pesos for 90 days, without renewal;

- (iii) Fixed terms in UVA for 90 days, with pre-cancellation option,

- (iv) Mutual Funds (CDF).

Figure 14 | Quarterly returns on savings and investment products

Note | For the calculation of the yields of fixed terms in pesos, months of 30 days and years of 365 days60 were used. For more details on the calculation, see Methodological Note.

Source | BCRA, CAFCI and CNV.

Pre-cancelable UVA fixed terms were the most profitable products throughout the first three quarters of 2022, which is reflected in an increase in UVA product balances. In this way, the lower flexibility and liquidity of UVA fixed terms would be more than compensated for by their higher profitability, making this savings instrument more attractive. In second place, there are traditional fixed terms (with renewal): successive increases in the minimum interest rate made the prize for renewing this product every 30 days higher than depositing money for an equivalent period of time, without renewal.

However, as of October 2022, traditional fixed-term loans in pesos will become the most profitable products. Since there were no increases in interest rates in the last quarter of 2022, the rollover option does not affect the yield on these instruments. In addition, there was an increase in the profitability of DCFs, although their high liquidity61 implies that the yield is lower than that of fixed terms (both in pesos and UVA). This discourages the balances subscribed in DCFs from having a significant share within the portfolio of savings and investment products of individuals. Likewise, in the last quarter of 2022, a substitution of product balances in UVA was observed for traditional fixed-term balances (see chart 12 on the right).

4. Credit

4.1 Credit to individuals

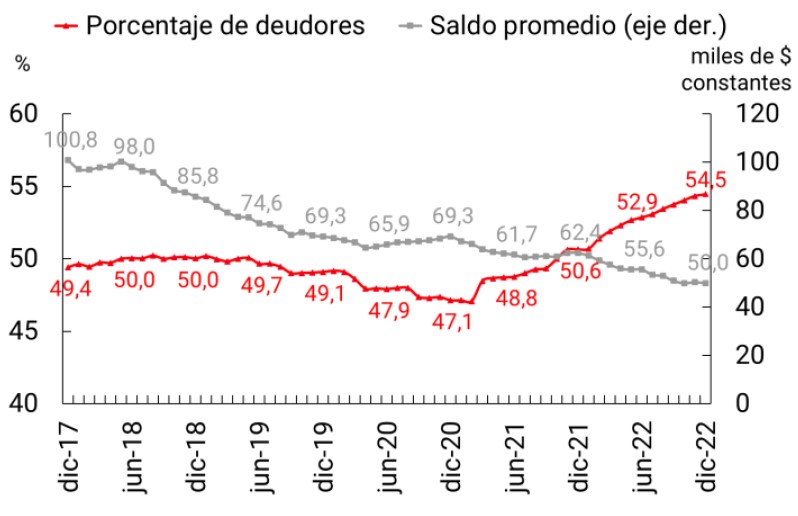

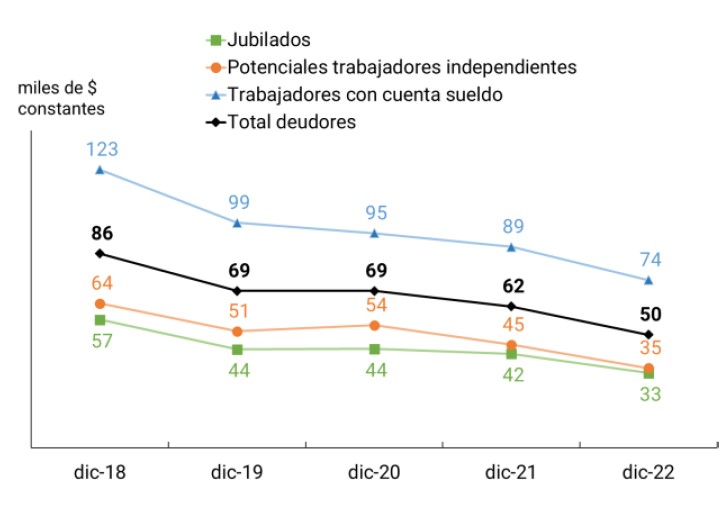

The number of individuals (PH) with financing in the expanded financial system (SFA) reached 19.3 million in December 2022, which implies that 54.5% of the adult population had at least one financing. In this way, this group registered a net increase of 1.6 million people compared to December 2021 (3.8 p.p.), consolidating two years of sustained growth. However, the total PH financing balance in the SFA decreased by 13% in real terms between December 2021 and December 202262. As a result, the average balance per debtor in real terms continues on a downward path.

Figure 15 | SFA Financing to Individuals

Note | Balances in thousands of constant pesos (base CPI 100 = Jan-19).

Source | BCRA and INDEC.

The holding of a growing number of PHs with financing in the SFA is influenced by new actors that take advantage of technology to offer credit63. Likewise, the number of PHs who receive income, whether a salary, a pension or payments for independent work, experienced an increase in the period under analysis. Having a registered income is a determining factor in the holding of credit products, which affects both the demand and supply of credit. Credit providers analyze a series of variables including income level, employment status, expense profile, and credit history to determine the granting of the loan, its amount, and interest rate. Holding a stable income allows users to meet the repayment of their debt and reduces the risk for financing providers.

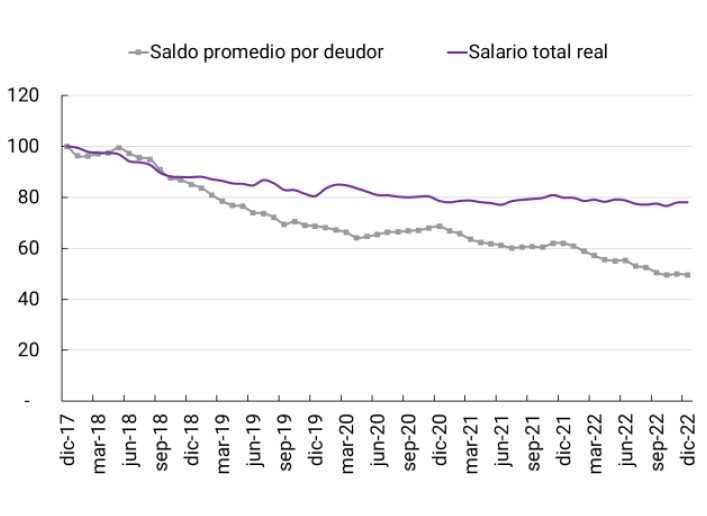

The reduction in the average financing balance, although slightly interrupted during the COVID-19 pandemic due to countercyclical policies, is pronounced and accompanies the movement of the economy’s average remuneration and the increase in the cost of financing during the second half of 2022. Likewise, the incorporation of new users who were previously excluded, whose income is relatively lower, has an impact on the average amount financed.

Figure 16 | Evolution of SFA financing to PH and macroeconomic variables

Quantity variables

Balance and price variables

Note | Base 100 in December 2017. Amounts in constant pesos (base CPI 100 = Jan-19).

Source | BCRA, INDEC and Ministry of Labor.

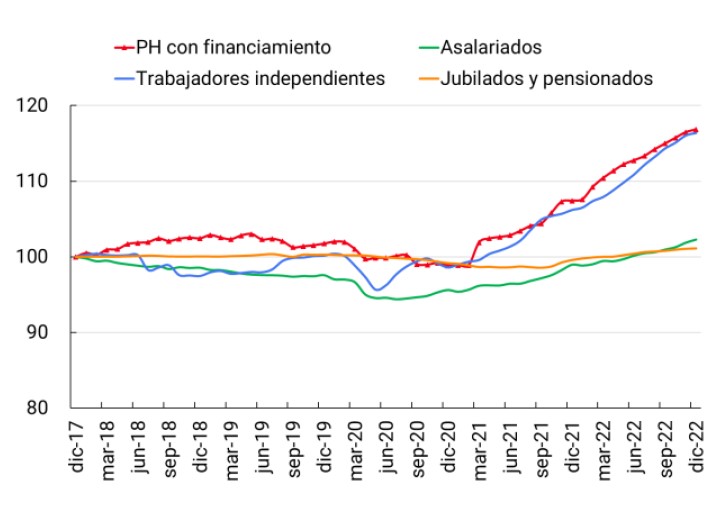

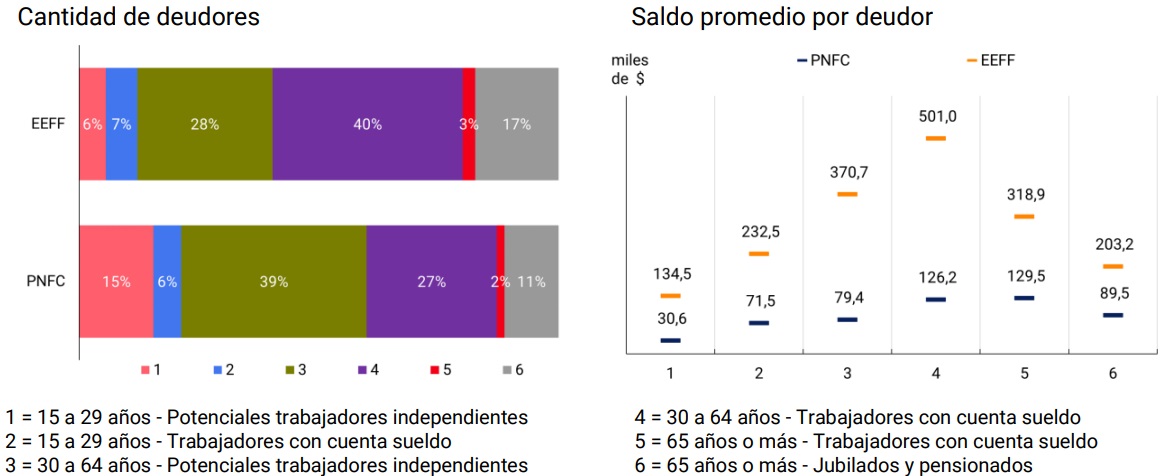

According to the information available, more than half of the PHs that registered credit products have a formal salary for their work in a relationship of dependency or with a retirement for having reached the corresponding age64. The remaining set of PHs with financing, which are mostly of working age, would have some type of income from independent work (for example, from commercial activities) to meet the repayment of their debt.

Figure 17 | Percentage of the adult population with financing and average balance per debtor

Percentage of adults with funding

Average balance per customer

Note | Workers with a salary account includes all debtors who collect their salaries in a salary account. Potential independent workers correspond to debtors between 15 and 64 years of age who do not register a salary account. Retirees corresponds to debtors 65 years of age and older who do not have a salary account.

Source | BCRA and INDEC.

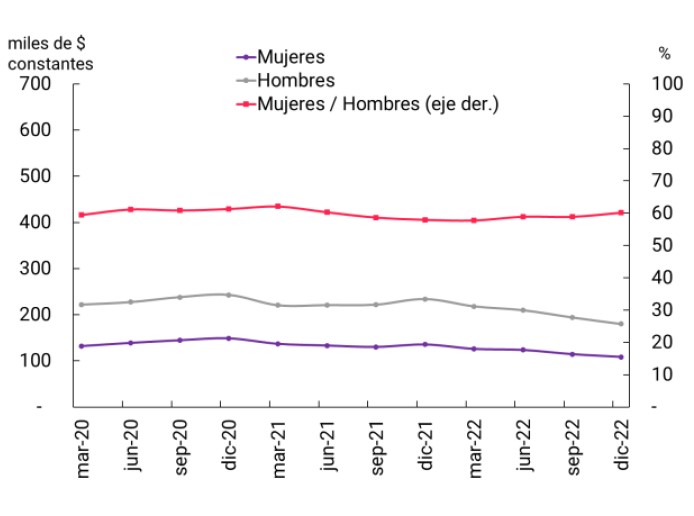

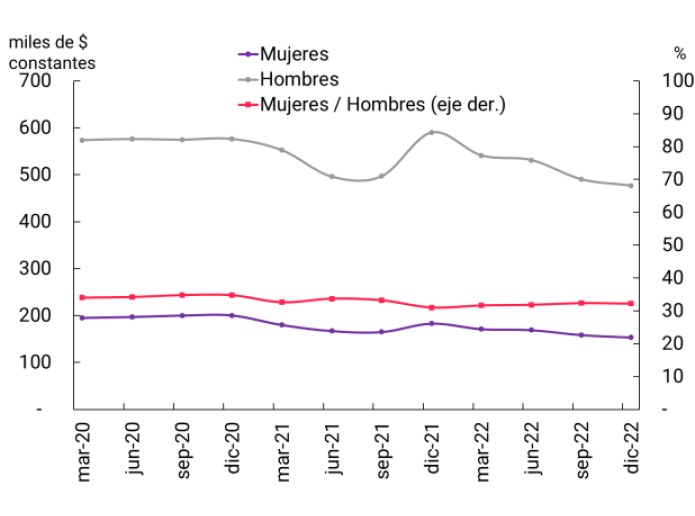

When looking at the financing balances, it can be seen that the type of income (and therefore its amount) significantly influences the level of the average debt balance. PHs that have a salary (salary account) register an average balance per debtor that is double that of those debtors who have an independent job (i.e., they do not register a salary account). In this way, although PHs that do not have registered work have access to financing, they do so for considerably lower amounts. Likewise, the evolution of the number of people with financing from the 3 groups shows that the reduction in the financing balance is explained by the contraction of the debt of all types of people who receive income and not by a particular type of person.

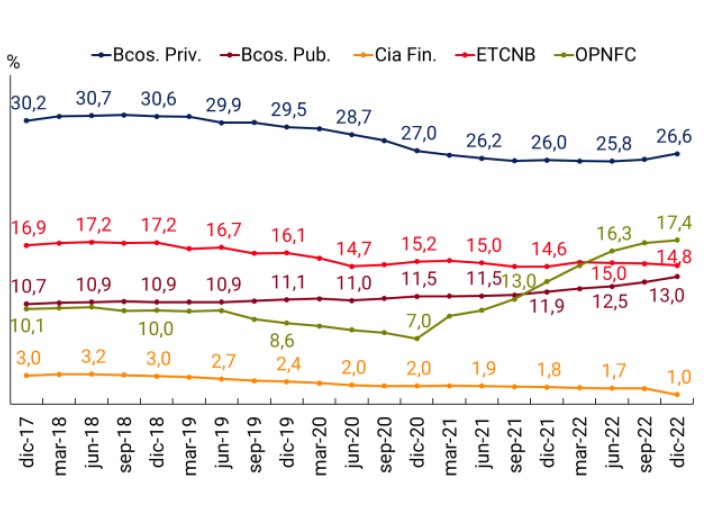

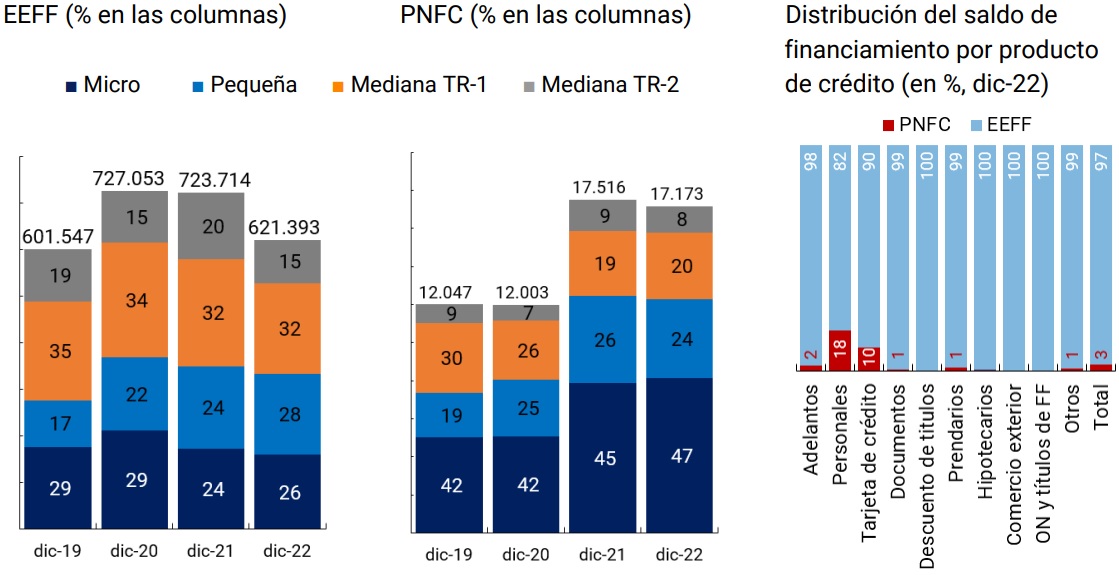

Credit providers. As of December 2022, 37 out of every 100 adults were financed with EEFF and 28 out of every 100 with non-financial credit providers (NFCPs). These values imply growth of 1.9% and 3.6%, respectively, compared to December 2021 and 1.6% and 8.1% compared to December 2020. Although both types of providers are under the orbit of the BCRA, the regulations applied to each of them have different implications for users. Documentation requirements, types of products, cost and amount of financing, ways of managing credit (face-to-face, mobile, or computer) and business models are among the variables that distinguish the EEFF from the PNFCs.

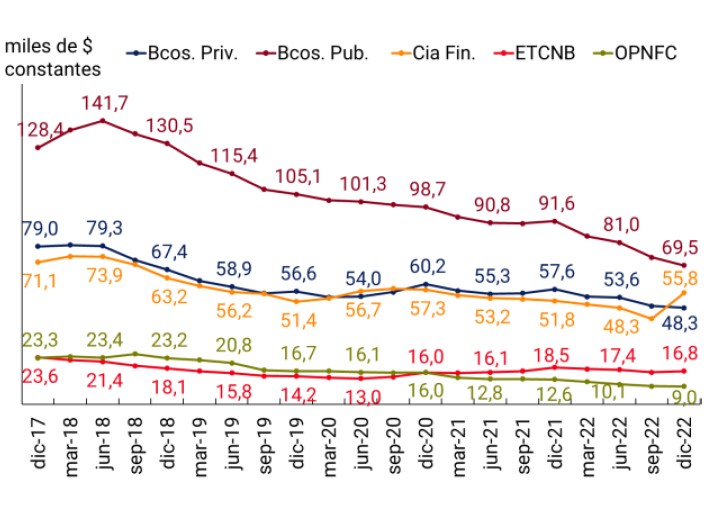

The average balance of the EEFF debtor is equivalent to 4.3 times the average balance of the PNFC debtor, indicating clear differences in the amounts financed by each group. In part, the balance gap between the two groups is explained by the type of financing offered. PNFCs offer their customers personal loans and credit card assistance, while the EEFF have a wider range of products that also includes current account advances and title and mortgage loans, among others. In particular, title and mortgage loans are characterized by their high amounts, which impacts the average balance per debtor. Likewise, characteristics of the people who receive the financing, such as age and the possession of a registered job in a relationship of dependency, affect the amount financed.

Within the EEFFs as a whole, private banks are the institutional group that finances the most people with 9.4 million debtors. During 2022, this group of banks registered an increase in the number of people they provide assistance to and ended with three consecutive years of decrease in the number of debtors. However, the total balance financed by this group fell by 13%, resulting in a 16% drop in the average amount per debtor (vs. 4% the previous year). Public banks, for their part, accelerated their incorporation of debtors, tripling the growth of the previous year and reaching a total of 4.8 million adults with financing. In terms of balances, the total financed by this group fell by 13% and the average balance per debtor fell by 24% (vs. 7% in 2021).

For their part, non-bank credit card issuers (ETCNBs) slightly increased the number of people with financing, which represents a change in the trend of reducing debtors of the last three years. However, during 2022 they reduced the total financed balance by 8% and the average balance per debtor by 10%. The other non-financial credit providers (NPPOs) continue to incorporate new debtors and reached 6.2 million adults financed, surpassing the ETCNBs (5.2 million). Driven mainly by providers that grant personal loans digitally and for small amounts, OPNFCs consolidate a clear trend towards the incorporation of people with financing. However, during 2022, this group registered a decrease in the total financed balance of 3%, which, together with the growth of the people assisted, generated a drop in the average balance per debtor of 28%.

Figure 18 | Percentage of the adult population with financing and average balance per debtor

Percentage of adults with funding

Average balance per customer

Source | BCRA and INDEC.

Throughout 2022, all institutional groups (except financial companies) recorded an increase in the number of PHs with financing, but reduced the average balance financed to each debtor. On the other hand, public banks and OPNFCs are the two institutional groups that sustain a PH portfolio with financing that exceeds that of the pre-COVID-19 pandemic periods.

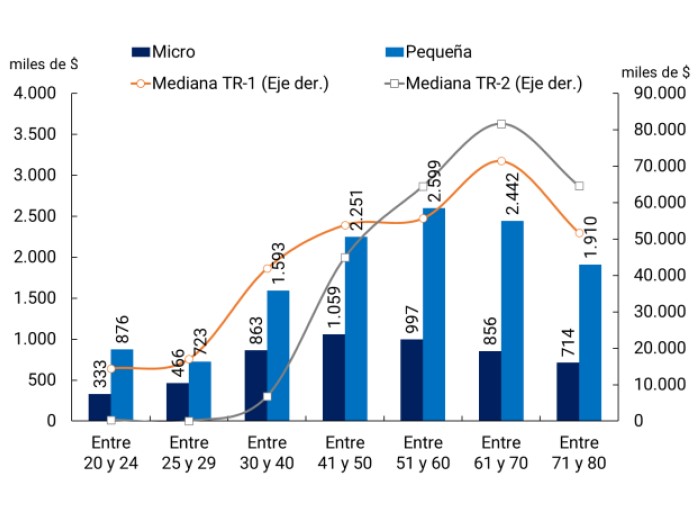

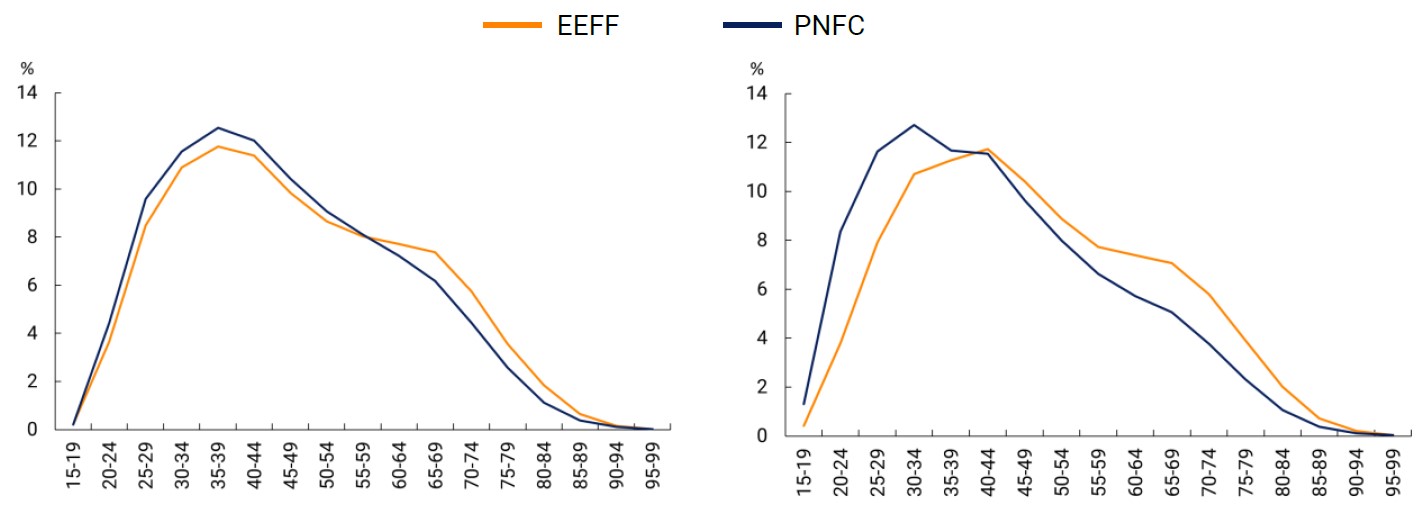

Characteristics of debtors by group. Within the PNFC group, young adults (15 to 29 years old) represent 21% of the total number of people with financing, while for the EEFF the same group reaches 12% of the total. The emergence of NFPPs that operate exclusively digitally may explain, at least partially, the higher proportion of young debtors in this group, by virtue of their greater propensity to operate in digital environments.

On the other hand, continuing with the distinction of the type of income of people with financing, it emerges that potential self-employed workers represent 54% of the total debtors for the PNFCs and 34% for the EEFFs. OPNFCs that combine the offer of credit together with activities such as payment services or e-commerce use alternative information to generate a profile of their users and a credit score. This makes it easier for people who do not have a job in a dependent relationship (but do have other income) to access formal financing, although for significantly lower amounts than those of people with a salary account and at higher interest rates.

In terms of age, the average balance per debtor replicates the inverted “U” behavior of the evolution of income, with lower average balances for young adults and older adults65. Likewise, the possession of a salary account (which indicates a registered job in a relationship of dependency) has a positive impact on the balance financed by both EEFF and PNFC. Combining both attributes, it emerges that people between 30 and 64 years of age who have a dependent salary receive the highest amounts of financing.

Figure 19 | PH with financing by institutional group

Note | Data as of December 2022. Graph on the right: balance in thousands of current pesos.

Source | BCRA.

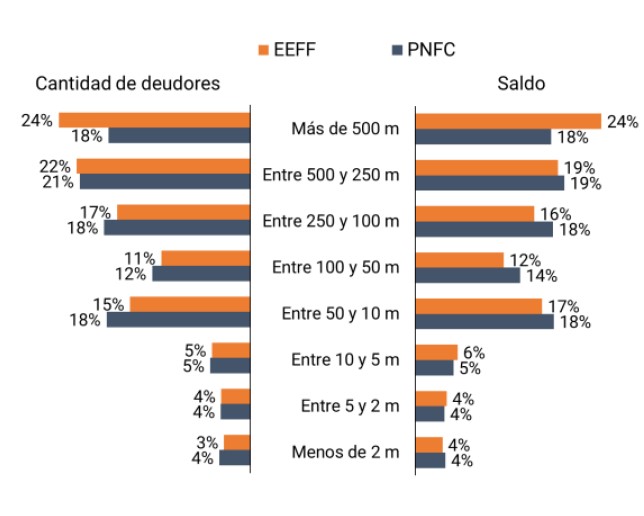

On the other hand, in relation to the PNFCs, the EEFF show a higher proportion of their debtors in localities with a greater number of inhabitants. This phenomenon is also replicated for the balance of financing, indicating a greater allocation of resources by the EEFF in larger localities66. These localities have a greater presence of physical infrastructure, with which users can contract credit products not only digitally but also in person. The PNFCs, on the other hand, register a higher proportion of people with financing and debt balance in intermediate-sized localities, especially in the range of between 10 thousand and 50 thousand adult inhabitants. For both types of providers, this behavior deepens over time, both in the number of people with financing and in their corresponding balance.

Figure 20 | Debtors by age range and salary account holdings

By age ranges

By possession of a salary account

Note | The Communes of the Autonomous City of Buenos Aires (CABA) are grouped into a single unit that totals more than 500 thousand adults.

Source | BCRA.

4.2. Credit to productive units

Micro, small and medium-sized enterprises (MSMEs) are a fundamental asset of a country’s productive scheme. Their relevance lies both in the number of companies in the economy and in their contribution to employment67 and, consequently, they are key actors in economic development. The availability of funds for these companies is, therefore, a transcendental factor in the purpose of financing production processes and investment in equipment68,69. In this sense, this section contributes to visualizing two external sources of the financing structure of MSMEs, the financing of financial institutions (EEFF) and non-financial credit providers (PNFC)70. The section inquires about the most used credit products and the age of MSMEs.

In recent years, the BCRA has implemented different regulatory initiatives aimed at improving MSMEs’ access to EEFF financing, both to respond to the transitory impact caused by the COVID-19 pandemic and also of a more permanent nature to help reduce barriers to access to financing71. These include:

a. Incentives for reducing the cost of financing MSMEs through minimum cash reduction:

i. Based on the share of financing to MSMEs with respect to total financing to the non-financial private sector (NFPS).

ii. For credit to MSMEs without EEFF financing.

b. Financing Line for Productive Investment of MSMEs (LFIP). As of 2020, the EEFF must maintain a balance of financing included that is at least equivalent to 7.5% of their NFPS deposits in pesos subject to fractional reserves, whose interest rate is subject to a maximum ceiling.

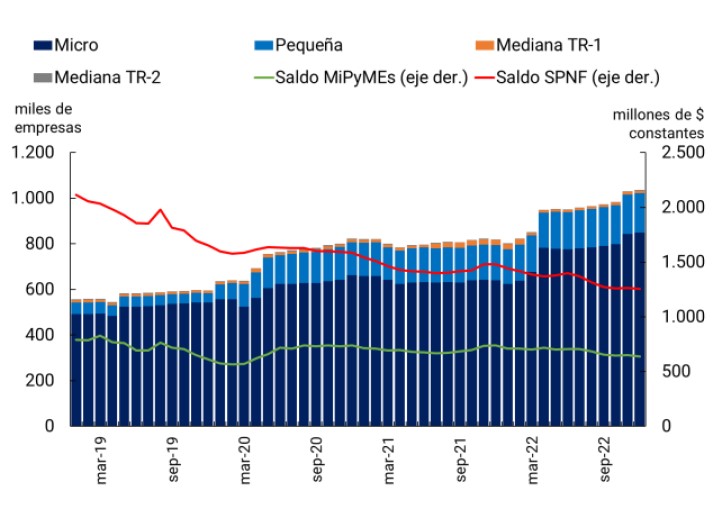

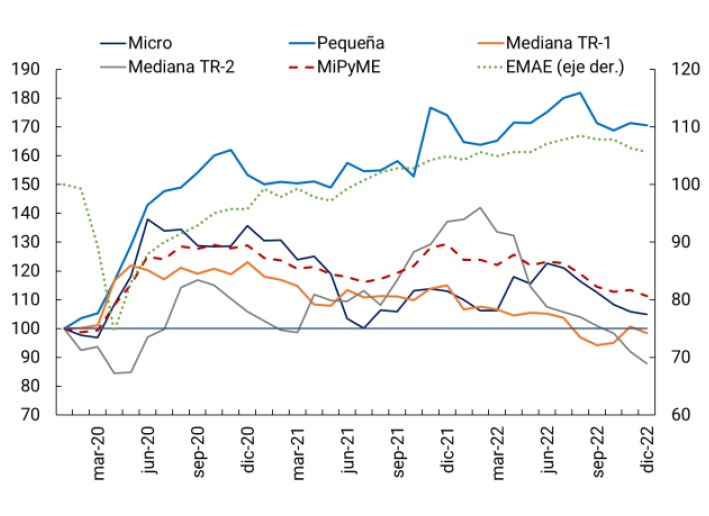

In this framework, the number of MSME companies with financing in the expanded financial system (SFA) reached a number of 1.04 million as of December 2022, close to 63% of companies with MSME72 certificate. In this way, this group of firms registered a net increase of 215,542 units compared to December 2021. Micro companies contributed almost all of the 26% year-on-year increase. On the other hand, the financing balance of MSMEs in the SFA amounted in current values to $3.8 trillion in December 2022. At constant values, this balance fell by 14% in year-on-year terms73, experiencing the same dynamics as credit to NFPS, which fell by 15% in that period74.

Figure 21 | MSMEs with financing and economic activity

Note | Includes financing in domestic currency and foreign currency. Graph on the right: base 100= January 2020.

Source | BCRA.

As previously indicated, the Financing Line for Productive Investment of MSMEs (LFIP) and the minimum cash reduction incentives for credit to MSMEs collaborate in directing financing to this group of companies at a cost lower than the market average75. From its implementation in October 2020 to December 2022, the LFIP disbursed $4.2 billion, benefiting more than 371,280 companies76.

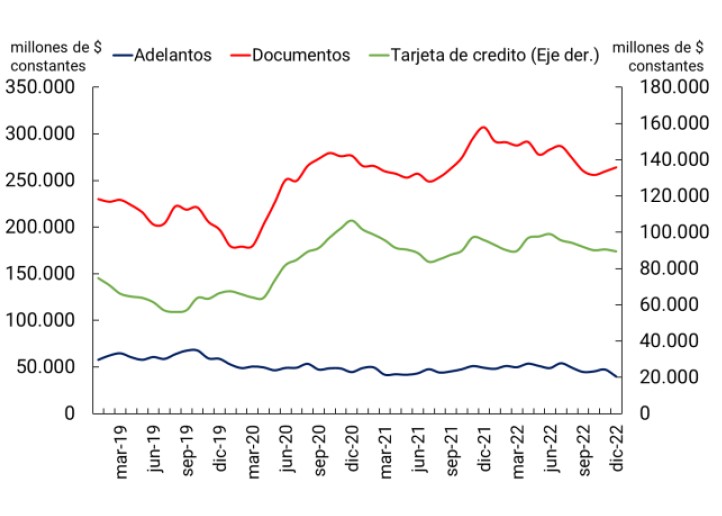

On the other hand, with respect to the types of assistance most used by MSMEs since the COVID-19 pandemic, documents stand out, which includes both single-signature documents and discounted and purchased documents (hereinafter “documents”). Credit card assistance and title loans appear in second place. On the other hand, assistance associated with foreign trade and advances had contractions.

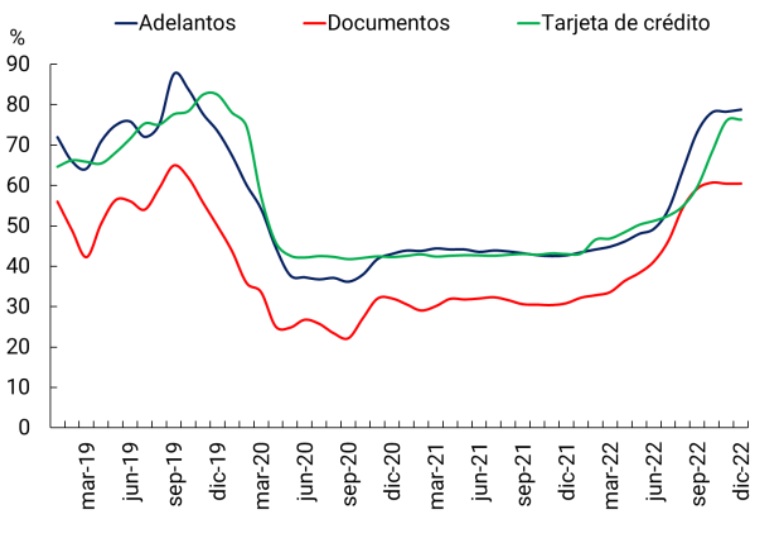

Figure 22 | Balance and interest rates per financing line

Financing balance

Interest rates

Note | Graph on the right: the interest rate on documents corresponds to the average of the interest rates on single-signature documents, discounted documents and purchased documents weighted by the amounts traded monthly in each type of assistance. These are interest rates and amounts operated by PJ PyMEs. The credit card rate applies for PH.

Source | BCRA.

Different factors are associated with the behaviour of different types of assistance. On the one hand, the LFIP created favorable conditions for the existence of supply of certain lines of credit, such as, for example, document discounts. Likewise, the lower interest rate associated with the assistance of documents with respect to current account advances may have induced a greater use of the former77. In the case of credit card financing, the abrupt reduction in the compensatory interest rate towards the first quarter of 2020, as well as the maximum limits to said rate based on a fixed rate78 and the characteristic of being revolving loans could be associated with its outstanding performance. In 2022, some reduction was observed towards the last months of the year, while the rate for financing through this instrument showed an increasing trend in the second half of the year.

On the other hand, despite the consolidation of the recovery in economic activity, the financing levels of MSMEs registered in 2022, although they remained above pre-pandemic levels, are on a downward path. When disaggregated by company size, it can be seen that only small companies experienced a positive dynamic, more linked to the development of economic activity, while micro and medium-sized companies showed a reduction in the financing balance.

What SFA credit products do MSMEs use? The relevance of credit products, measured both in terms of balance and number of companies, varies depending on the size of MSME companies. The choice of the type of financing depends on a variety of factors, from the destination of the financing and the document requirements for the application to the interest rate, the amount of the financing and the repayment term. In terms of financial inclusion, the availability of a range of credit products that adapt to the diverse needs of MSMEs improves the growth possibilities of companies and facilitates the cycle of production of goods and/or provision of services.

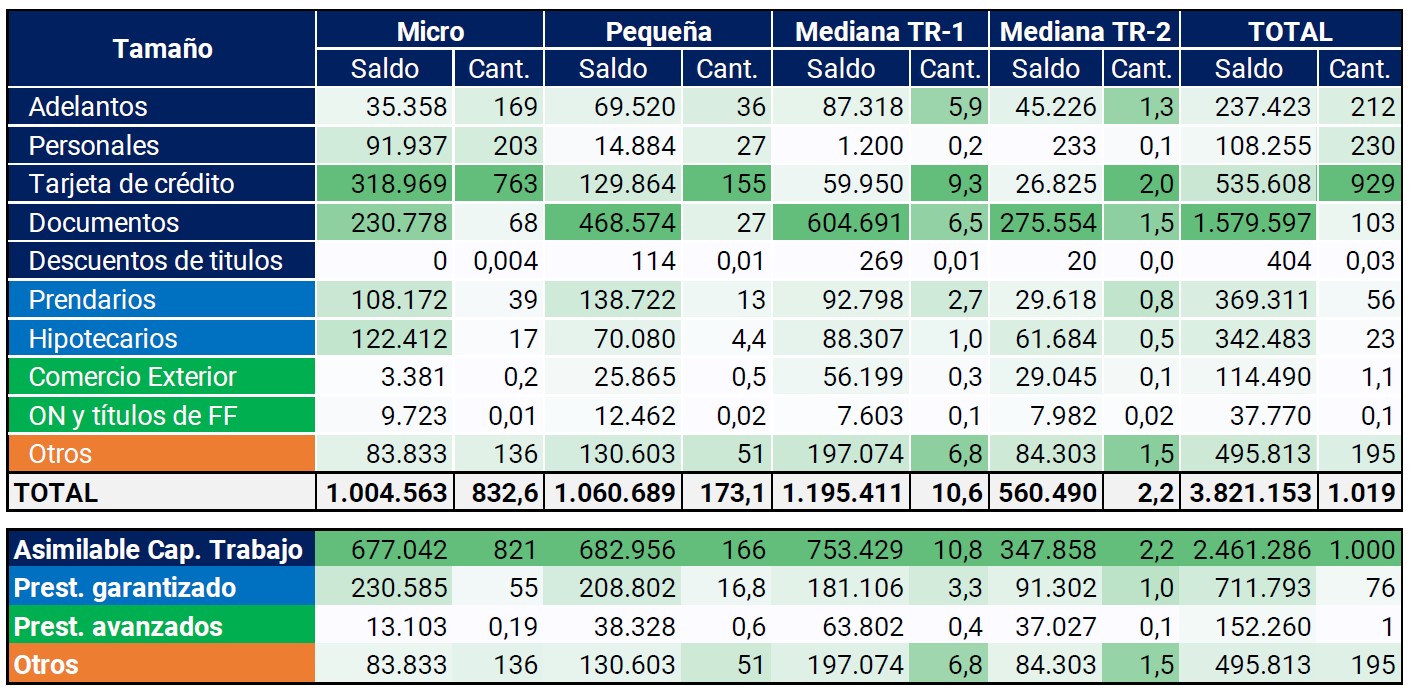

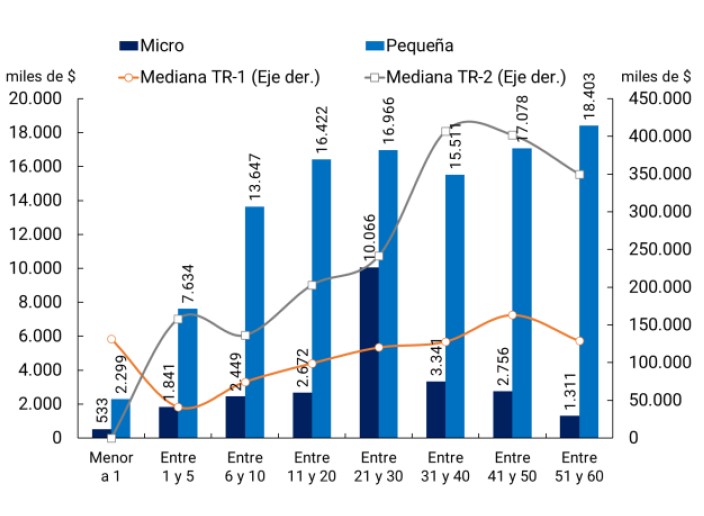

In terms of balance, micro and small enterprises are financed mostly by credit cards and documents, while medium-sized enterprises are financed mainly by documents and advances79. Therefore, the use of documents is the main financing mechanism for MSMEs, which consists of the delivery of their own documents or those of third parties as consideration for the loan granted by the EEFF. In the last 24 months, this credit product concentrated between 37% and 41% of the financing balance of MSMEs and represented a significant portion of the funds obtained that can be assimilated to working capital of small and medium-sized enterprises (68% to 78%). It should be noted that, among the destinations provided for by the LFIP, the application of funds to working capital is included, whose financing is instrumented, among other alternatives, through the mechanism of documents with a single signature80.

In terms of the number of participating companies, credit cards maintain their relative share within each size, although their importance decreases as their size grows and, therefore, the participation of legal entities (PJs) increases. In addition, credit products such as advances, documents, and secured loans increase the share of firms as firms grow in size (i.e., PH share falls).

Table 5 | MSME Financing by Attendance Group and Size

Data as of December 2022

Note | “Balance” in millions of current pesos. Number of companies in the thousands. The green color of the cells is calculated based on the minimum and maximum value of each metric (balance and quantity) for each of the sizes.

Source | BCRA.

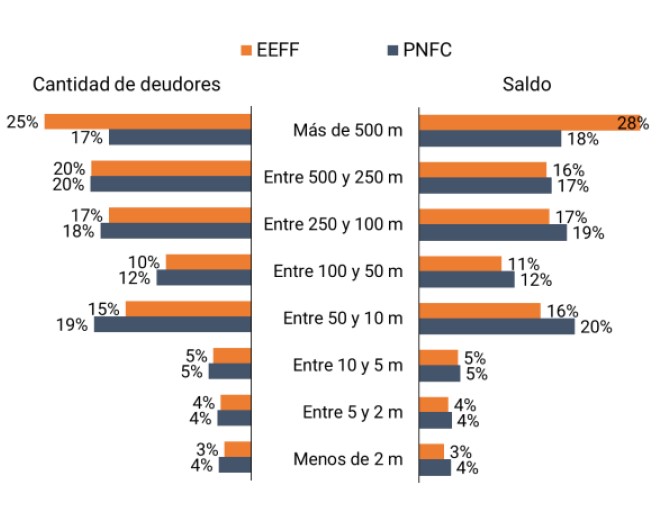

Regarding financing by type of supplier, i.e. EEFF and PNFC81, MSMEs are mainly financed by the former, regardless of the size of the company82. On the other hand, it is observed that these companies are increasing their exposure to PNFC financing, although at levels much lower than those recorded by the EEFF83. The emergence of new credit providers, leveraged on the use of technology for credit evaluation and management and on the use of equity and/or capital market financing, expanded the supply of credit for MSMEs.

In December 2019, the ratio of EEFF to PNFC financing was 50 to 1 (i.e., for every $1 of financing in PNFC, MSMEs had $50 in EEFF), while in December 2022, the ratio rose to 37 to 1. In this period, the balance of financing of MSME companies in PNFC increased by 50%84. Likewise, during the period in question, the financing granted by the PNFCs was concentrated in smaller companies, while in the case of the LFES it was distributed more equitably, with a certain predominance of small and medium-sized TR-1 companies.

Figure 23 | MSME Financing Balance by Vendor Group and Size

Note | Balance in millions of constant pesos (base CPI Jan-19=100).

Source | BCRA.

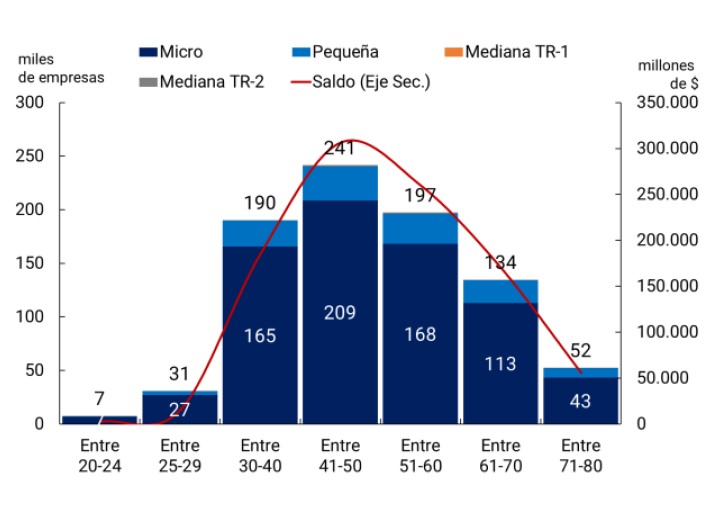

How long do MSMEs with financing have?85 The distribution of financing according to the life span of the productive unit is a relevant element for the financial inclusion of young MSMEs. On the one hand, young companies require an injection of resources in the early stages of development86, but, on the other hand, they have less economic history of their company, which makes it difficult to evaluate their credit. At the same time, smaller firms, to the extent that they generate positive results (profits), tend to finance themselves through the reinvestment of profits, implying that they could substitute external sources of financing for internal ones87.

In the case of PJ MSMEs, three-quarters of the productive units are up to 20 years old, with a predominance of micro and small sizes, and they account for less than 50% of the financing balance. Although young companies have a significant portion of the financing balance, the average balance is very low, which could be an indication that small companies use other sources of financing. Likewise, the passage of time seemed to have an impact on the level of financing of companies of all sizes, although the effect tends to be partially reversed for the group of companies with the longest life.

Figure 24 | Amount and balance of financing by type of person and length of life

Data as of December 2022

Individuals

Legal persons

Note | Balance in current pesos. The X-axis shows strata of years.

Source | BCRA.

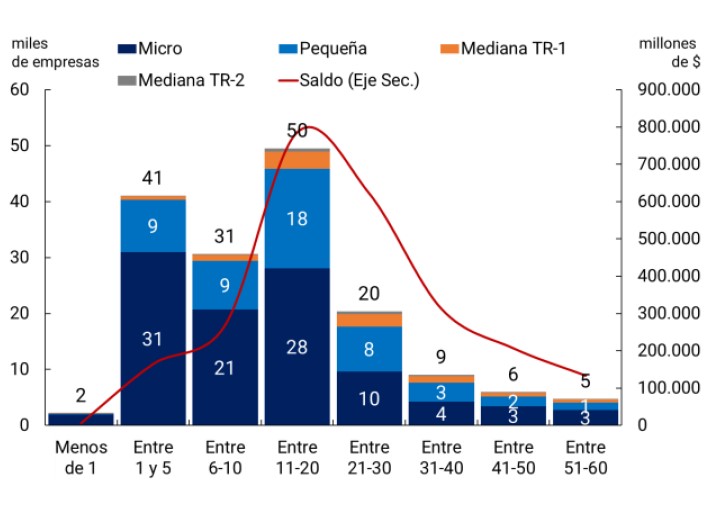

In the case of PH MSMEs, micro-sized companies predominate in all age groups. Also, as the age of the person increases, the participation of small companies grows, which could be linked to a certain trajectory of commercial activities. This can be seen in the fact that people over 50 years of age account for 50% of the financing balance and maintain average financing balances similar to or close to younger age groups.

Likewise, similar to what happens with PJ MSMEs, the growth in the age of people seems to affect the level of financing regardless of the size of the MSME. It should be noted that the number of medium-sized PH MSMEs is a very small portion of the total PH MSMEs (less than 1%), taking into account that the amount of turnover required for these sizes is very high for a commercial activity organized around a human person.

Figure 25 | Average current financing balance per lifetime

Data as of December 2022

Individuals

Legal persons

Note | Balance in current pesos. The X-axis shows strata of years.

Source | BCRA.

Section 1 / An approach to the use of electronic channels by financial institutions

In view of the significant progress made in digitalization, measuring the use of electronic channels is a crucial aspect of assessing the degree of (digital) financial inclusion. While aggregate variables such as electronic payments (see Section 3.1) show the growth of electronic channels, information is scarce on user behavior across electronic channels.

As a first approach to the subject, a survey was carried out on the use of electronic channels by individuals to carry out transactions that involve movements of funds. This survey consisted of a voluntary survey of all financial institutions (EEFF), which focused on collecting historical information on users and their activity in home banking (HB) and mobile banking or electronic banking wallet (MB or mobile banking)88. The analysis proposed in this section considers a sample of 10 FBSEs, which accounted for 49% of bank account holdings in December 202189.

Figure A.1.1 | Using HB and MB to perform a transactional operation

Note | “Usage” means the percentage of account holders with at least one transactional transaction in the quarter. In the same period, the number of times a person is counted is determined by the number of the 10 EEFF in the sample where he or she has an account registered. This applies both to the number of account holders and to those who register a transactional transaction.

Source | BCRA

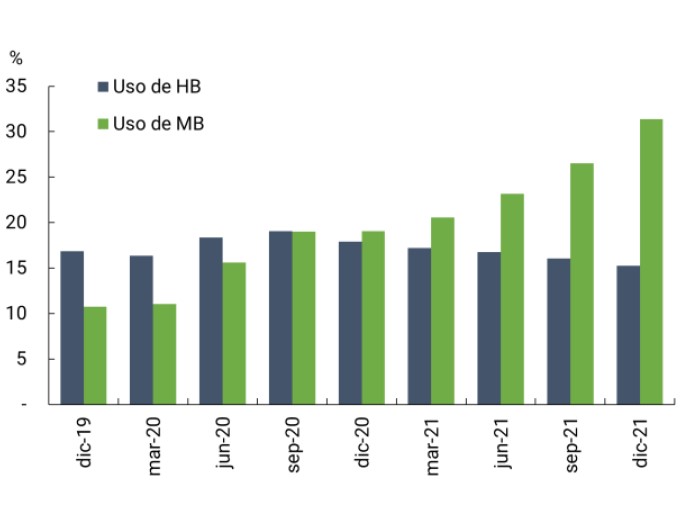

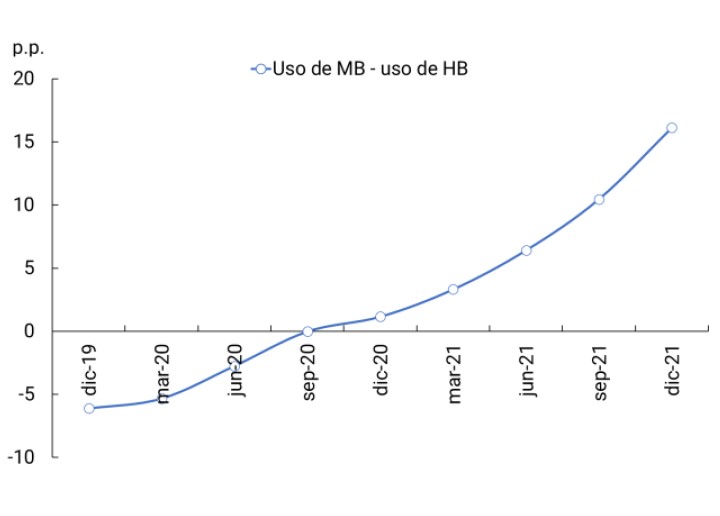

In general terms, the use of mobile banking or electronic banking wallet to carry out transactional operations grew significantly. After the COVID-19 pandemic, a change in behavior is observed in the electronic channel chosen for transactions, losing home-banking relevance with respect to mobile banking.

The progressive inclination of account holders towards mobile banking is supported, among other factors, by a more intense use of mobile devices and the greater offer of banking applications with services and products that meet the different needs of individuals. Likewise, the cell phone has the potential to include new people in electronic channels, in particular population groups with a certain degree of vulnerability90.

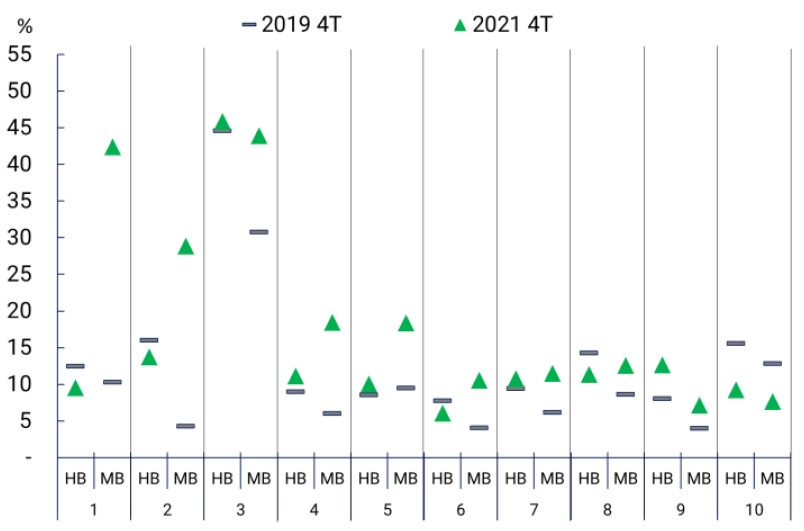

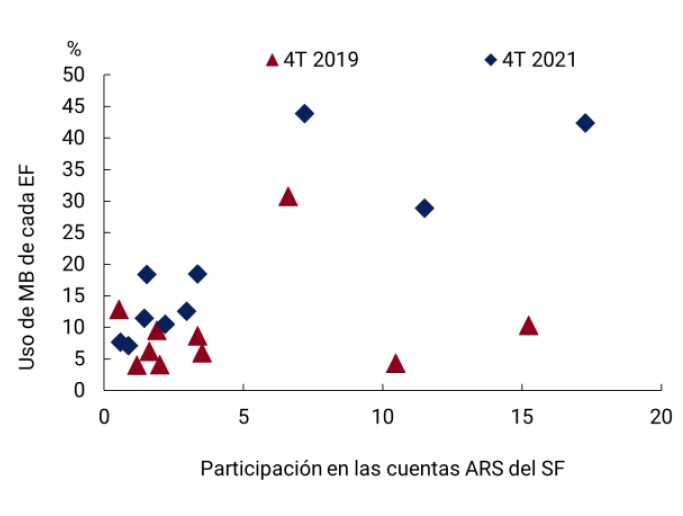

Results at the level of financial institution. Practically all the EEFF in the sample (9 out of 10) registered an increase in account holders who used mobile banking to carry out at least one transactional transaction between the last quarter of 2019 and the same period in 2021. These 9 EEFF accounted for 48% of the accounts in pesos in the financial system as of the last quarter of 2021.

Figure A.1.2 | Use of electronic channels to perform a transactional operation

Note | “Usage” means the percentage of account holders with at least one transactional transaction in the quarter. The numbering of the “x” axis corresponds to the 10 EEFF that are part of the final sample. They are ordered in descending order based on the variation in MB channel usage between Q4 2019 and Q4 2021.

Source | BCRA.

Likewise, mobile banking became the main channel for a large part of the SEEs (7 out of 10 vs. 1 out of 10, in the last quarters of 2021 vs. 2019). On the user side, new digital behaviors are in line with a greater use of mobile banking: each person spent on average more than 3 hours per day on the cell phone during 2021 and it is estimated that downloads of mobile-banking applications and digital wallets and payments went from 5 million to 9.9 million in the period under analysis91.

For its part, the HB channel also recorded increases in its usage levels, but in a smaller amount of EEFF (5 out of 10) and with increases well below MB. In addition to what was previously mentioned about the increased use of mobile devices, the HB channel has certain characteristics that would limit the expansion of its use: (i) low ownership and use of computers, and (ii) the characteristics of the device that do not allow it to be used for certain operations (such as QR payments or other face-to-face electronic payments). On the other hand, certain behaviors of account holders would also limit the expansion of their use. The available information allows us to infer that account holders prefer to use the HB to make transfers of funds for higher amounts, which are made less frequently (See Section 3. Electronic means of payment).

Thus, the LFSE showed two behaviors: on the one hand, increases in MB use and simultaneously decreases in HB use (4 out of 10), and on the other hand, increases in the use of both channels (5 out of 10). This implies the incorporation of a significant number of new users to mobile banking, without this increase implying a significant loss of users in the HB.

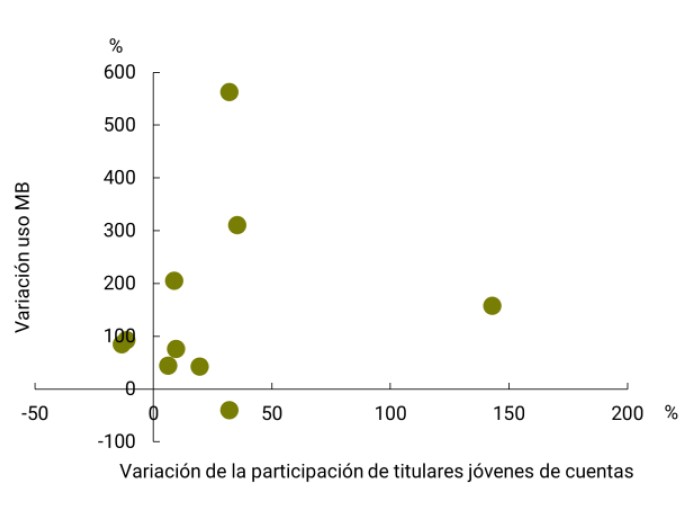

Characteristics of the EEFF. As part of this process, certain attributes of the EFFS, such as the size of the EFFS and the age composition of account holders, could have boosted the adoption of mobile banking:

Figure A.1.3 | Account holding, MB use, and age structure

Note | Q4: 4th trimester. SF: Financial system. Variation in the use of the MB and Variation in the participation of young account holders: variation between the last quarters of 2019 and 2021. Youth: 15 to 29 years old.

Source | BCRA.