I. Financial intermediation activity

In August, the aggregate financial system increased its intermediation activity with the private sector. Considering the most relevant variations in the balance sheet of the financial institutions as a whole for items in pesos —expressed in homogeneous currency—,1 in the month the balance of private sector deposits increased and, to a lesser extent, financing to the public sector was reduced. These changes were mainly offset by increases in real terms in liquidity in the broad sense and in the real balance of credit to the private sector. On the other hand, the main movements in the segment of items denominated in foreign currency – expressed in the currency of origin – were an increase in private sector deposits and an increase in liquidity in this denomination.

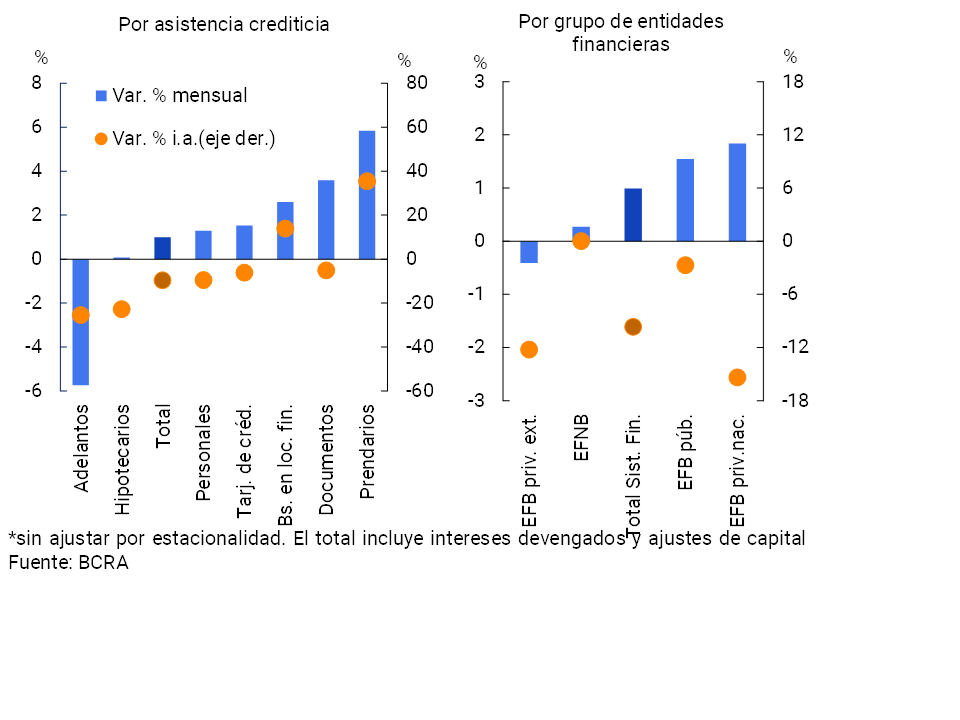

In August, the balance of credit to the private sector in pesos increased by 1% in real terms compared to the previous month (+3.5% in nominal terms)2. With the exception of advances, all loan lines showed increases in real terms during the period (see Graph 1). National and public private financial institutions mainly drove this growth. In a year-on-year comparison, the balance of financing in national currency to the private sector decreased by 9.7% in real terms (+36.8% nominal) in August, with a greater relative fall in domestic and foreign private financial institutions3.

Graph 1 | Credit balance to the private sector in pesos

In real terms*

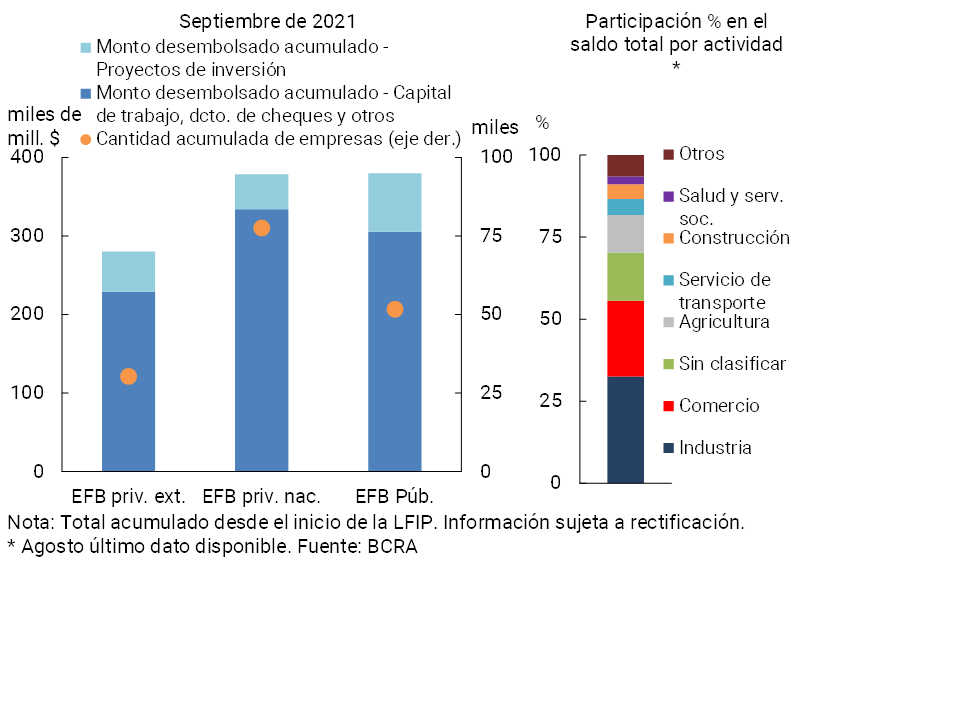

The monthly increase in credit in pesos was driven in part by the Financing Line for Productive Investment (LFIP) for MSMEs4. The loans channeled through this tool totaled disbursements of almost $1.04 trillion from October 2020 to September 2021, benefiting approximately 160,000 companies. National public and private financial institutions accounted for 36.6% and 36.4% of the total amount disbursed, respectively, while foreign private entities accounted for 27% (See Graph 2). It is estimated that almost 33% of these resources were channeled to industry, followed by commerce (with 23.1%) and agriculture (with 11.4%).

Graph 2 | Financing Line for Productive Investment (LFIP) of MSMEs

It is worth mentioning that, with the aim of promoting a balanced and sustained economic recovery throughout the country, the BCRA recently approved a set of measures focused mainly on the productive sectors most affected by the context of the pandemic5. In particular, at the beginning of October, the Productive Investment Line for MSMEs was relaunched, mainly aimed at the industrial and services sector for the period 2021-2022. From October 2021 until the end of March 2022, financial institutions covered must maintain a balance of financing comprised that is at least equivalent to 7.5% of their non-financial private sector deposits in pesos corresponding to September 20216. In line with the terms and conditions of the financing provided for the two previous quotas, the maximum APR for loans for investment in capital goods (with a minimum average term of 2 years – weighted by maturities) is maintained at 30% and at 35% maximum APR for those financings for working capital. In this new tranche (quota) of the LFIP, the benefits for the productive sectors are further expanded. Specifically: i) MSMEs producing meat and/or milk are incorporated, which will be able to access the two types of lines; ii) MSMEs and non-MSMEs producing chicken and/or pork remain within the eligible financing, which will have access to credits for investment in capital goods; iii) additional benefits are provided to companies in the gastronomy, hospitality, cultural and leisure services sectors, which will be able to access the Working Capital Line and will have a grace period of 6 months before paying the first installment of the loan.

For its part, through the line of financing at subsidized interest rates for companies registered in the “Emergency Assistance Program for Work and Production” (ATP)7, $14,265 million have been granted through more than 20,900 loans.

Among the lines of financing under favorable conditions, in August the BCRA implemented the “Zero Rate Credit 2021” Program for workers adhered to the Simplified Regime for Small Taxpayers (RS). From its implementation until mid-October, almost 135,000 loans were granted for a total amount of $15,866 million8. It should be noted that through the “2020 Zero-Rate Credits“9 , about $66,500 million were channeled (more than $300 million additional contemplating the line of “Zero-Rate Credits Culture”)10.

As a result, it is estimated that as of July of this year, approximately 19% of the total credit balance in pesos to the private sector had some stimulus designed by the BCRA in terms of lower minimum cash requirements for the offering financial institutions.

In this scenario, it should be considered that the recent results of the Credit ConditionsSurvey 11 corresponding to the third quarter of the year would indicate a moderate easing of the supply (credit standards) of loans to companies with respect to the previous quarter (in all sizes of companies and financing terms). According to the responses received, this performance would be mainly explained by an improvement in both the situation of the sector to which the company belongs and in the current economic situation (and/or future prospects), and by the decision to increase market share. On the side of perceived credit demand, in the period the entities consulted indicated that they observed a moderate drop originating in large companies and neutrality in the case of SMEs, although they expect growth for the following period.

Considering the segment in foreign currency, in August the balance of credit to the private sector increased 0.2% —in currency of origin—, explained by the performance of domestic private entities. Thus, the balance of total financing (in domestic and foreign currency) to the private sector increased by 0.7% in real terms in the month (+3.2% in nominal terms), thus accumulating a fall of 11.5% in real terms compared to the level of a year ago.

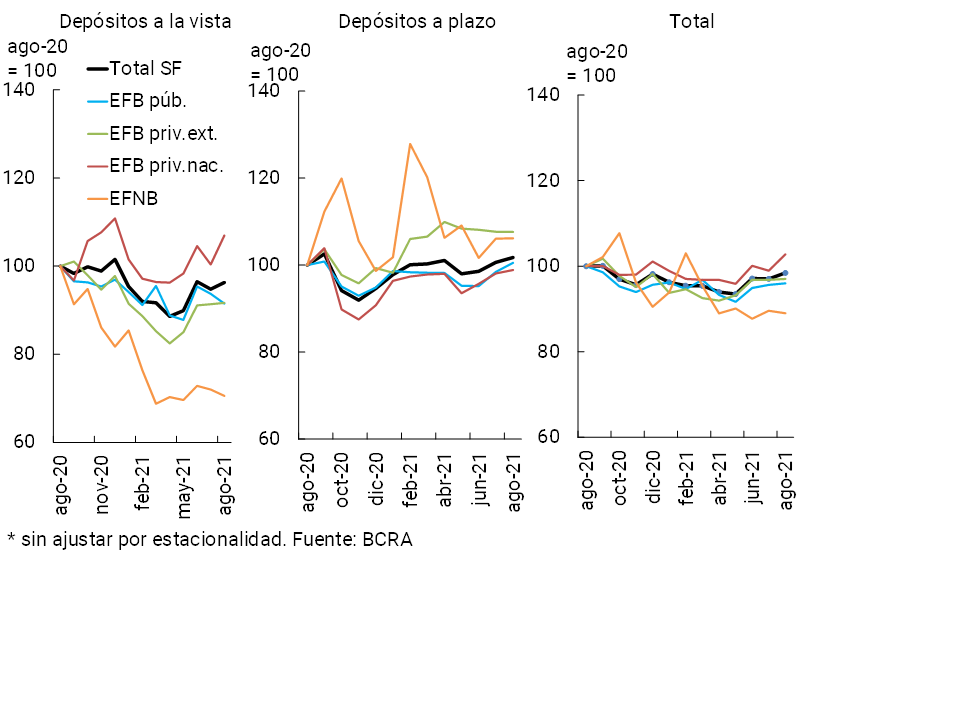

On the funding side of the financial institutions as a whole, in August the balance of deposits in pesos of the private sector increased by 1.4% in real terms (+4% nominal), with greater relative dynamism in national private financial institutions (see Graph 3). Demand accounts grew 1.6% in real terms compared to July (+4.1% nominal), with heterogeneous performances among groups of financial institutions. For its part, the balance of time deposits increased by 1.1% in real terms (+3.6% nominal), mainly explained by the performance of public financial institutions. In particular, in August the traditional segment of deposits (not the one denominated in UVA) verified an increase of 2.2% in real terms, while fixed-term deposits in UVA fell 6.7% in real terms compared to July.

Graph 3 | Balance of private sector deposits in pesos

In real terms*

In August, the balance of deposits in foreign currency of the private sector increased 0.6% – in foreign currency – compared to the previous month. Thus, the balance of total deposits of the private sector (including domestic and foreign currency) accumulated an increase of 1% in real terms in the period. (+3.5% nominal).

In year-on-year terms, the balance of deposits in pesos of the private sector accumulated a fall of 1.6% in real terms (+49.1% nominal). Demand accounts fell by 3.7% YoY in real terms (+45.8% YoY in nominal terms), while time deposits increased by 1.7% YoY in real terms (+54.1% YoY in nominal terms). On the other hand, the balance of public sector deposits in national currency increased by 2.5% YoY in real terms (+55.3% YoY in nominal terms). Thus, total deposits in pesos (considering both the private and public sectors) decreased by 0.5% YoY in real terms (+50.7% YoY in nominal terms), while total deposits (covering both sectors and considering all currencies) fell by 3.5% YoY (+46.2% YoY in nominal terms).

II. Aggregate evolution and composition of the balance sheet

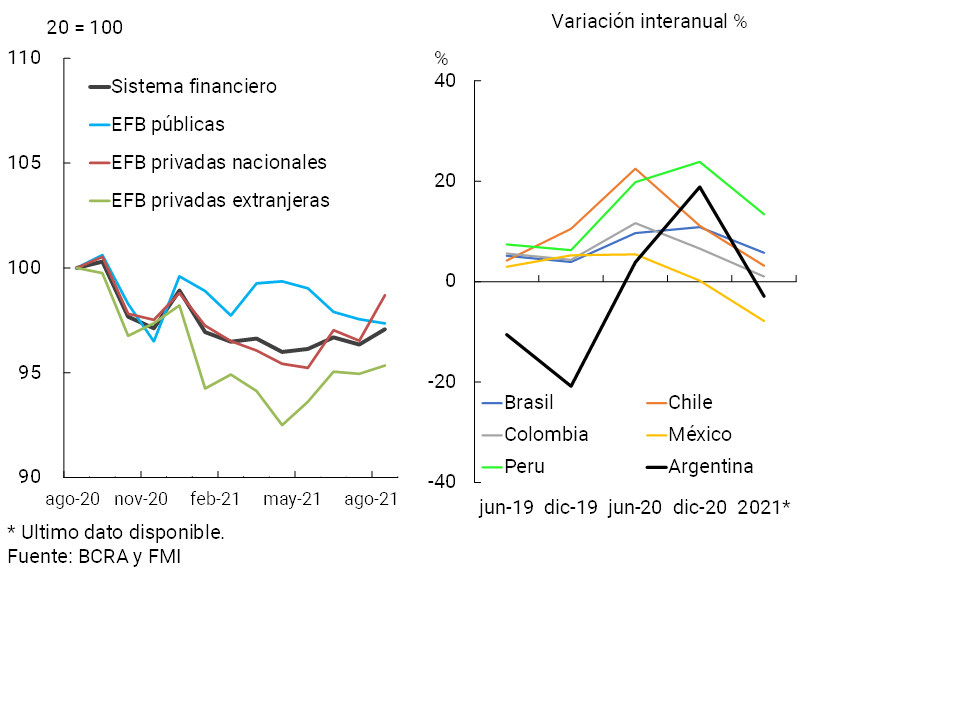

In August, the balance of total assets of the financial system increased by 0.8% in real terms compared to July, with greater dynamism in national private entities (see Chart 4). In year-on-year terms, the sector’s assets fell by 2.9% in real terms, with a greater relative fall in foreign private financial institutions. This year-on-year performance occurred after the significant increase evidenced in 2020, which was mainly due to the growth of credit in pesos and the increase in LELIQ and passes (as a counterpart to the monetary sterilization carried out by the BCRA, after the issuance of pesos destined in part to the PEN to finance extraordinary programs to counteract the effects of the pandemic). In general, in other financial systems in the region, total assets moderated their year-on-year growth rate in 2021 (according to the latest available information, see Chart 4) compared to what was recorded in 2020 (in some cases, such as Mexico’s, it even showed a year-on-year reduction in 2021).

Figure 4 | Total assets of the financial system

In real terms

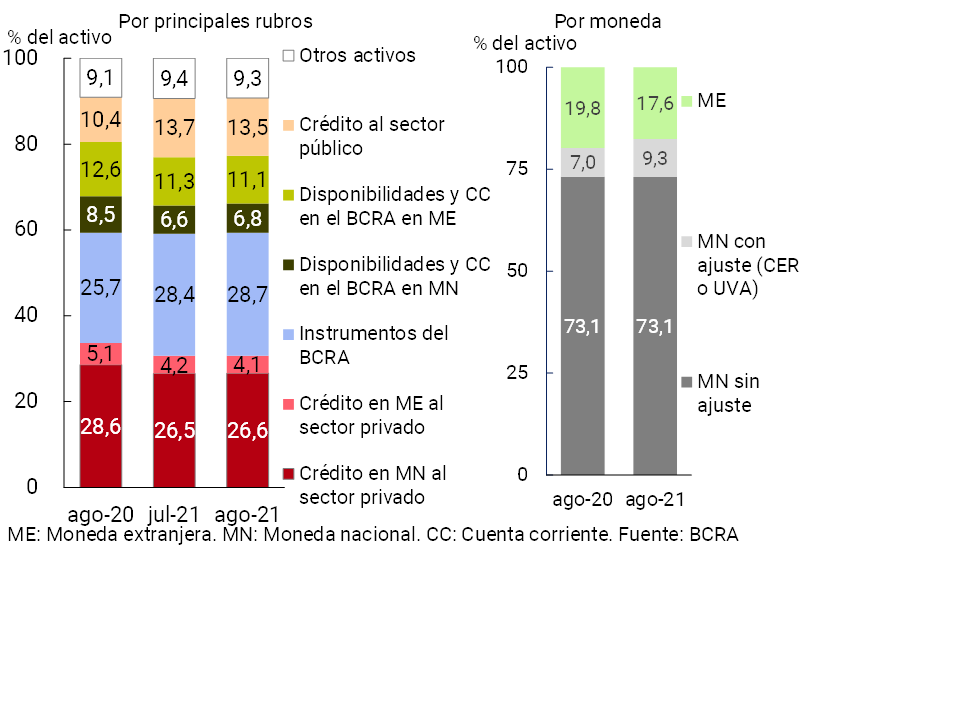

In relation to the composition of the total assets of all financial institutions by items, in August the relevance of liquid assets in national currency (BCRA instruments, current accounts at the BCRA and other availabilities) increased slightly. On the other hand, the relative weight of credit to the public sector in total assets was reduced, while the other items remained unchanged in magnitude in the month. Taking into account the composition of the total assets of the financial system by currency, from low levels the items adjustable by CER (including those denominated in UVA) increased their participation in the last twelve months, to weighted 9.3% in August (see Chart 5). In contrast, foreign currency items decreased in importance in the total in the last year. On the other hand, assets in pesos (unadjusted) maintained their relative weight compared to August 2020 and account for most of the total (73.1%).

Graph 5 | Composition of total assets

Financial system – Share %

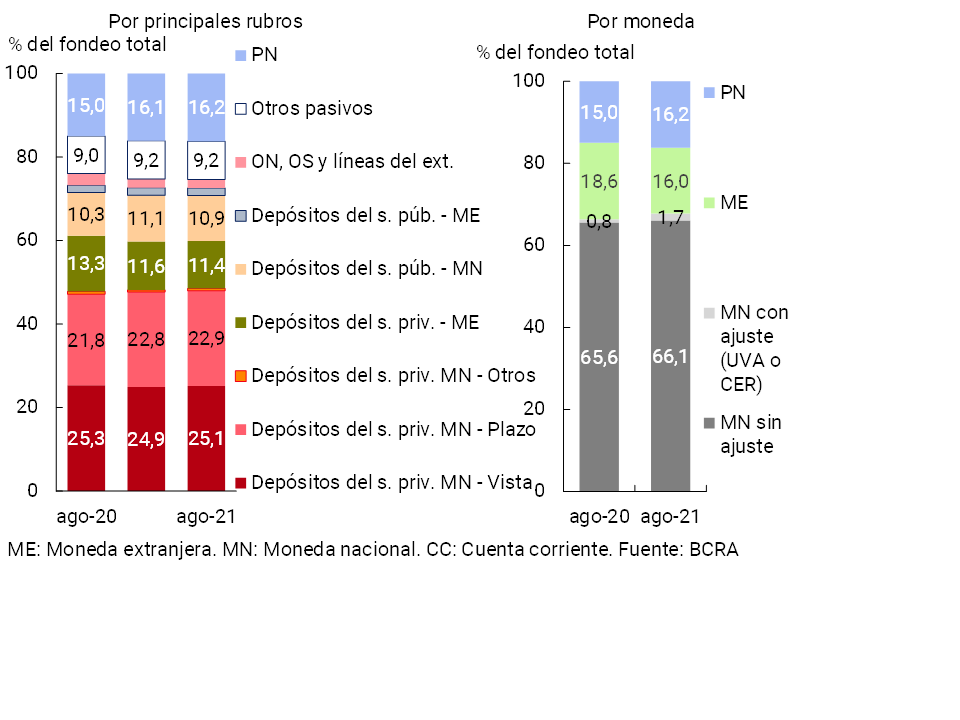

With respect to the items that make up the funding of the financial system, in August the balance of private sector deposits in national currency increased and the weighting of public sector deposits in that denomination and of private sector placements in foreign currency was reduced. When considering the funding of the financial system by currency, in year-on-year terms, items in pesos with an adjustment clause for CER or UVA and, to a lesser extent, those without adjustments increased their relative importance in the total, while those denominated in foreign currency decreased their weighting (see Chart 6).

Graph 6 | Total system funding composition

In % of total funding (liabilities + equity)

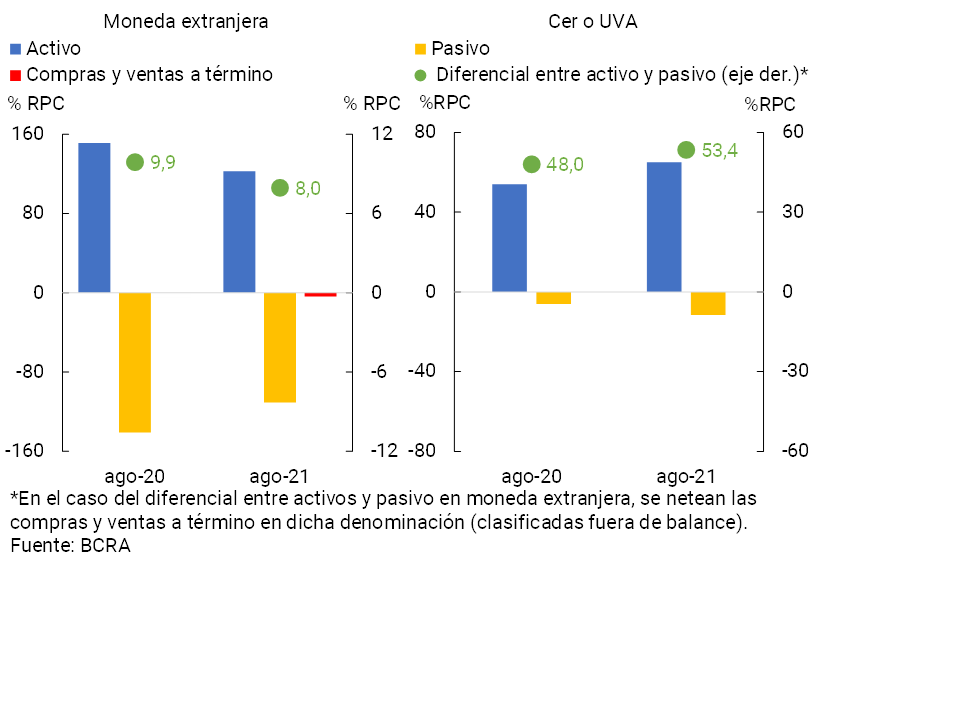

Considering the assets and funding of the financial system by currency and their spreads, the sector shows limited levels of exposure to items in pesos with adjustment clauses and to those denominated in foreign currency (see Chart 7), the latter within the framework of current prudential regulations. As part of their operations, the group of entities can verify currency spreads (between assets and liabilities that can be positive or negative). In this case, the sector is exposed to variations in the exchange rate and/or in the adjustment coefficients (CER) having an effect on the results. In terms of spreads (assets – liabilities), it is estimated that in August the financial institutions as a whole registered a positive level of 53.4% of regulatory capital for items with capital adjustment for CER/UVA (+5.4 p.p. y.o.y.) and 8% of regulatory capital when considering assets and liabilities in foreign currency12 (-1.9 p.p. y.a.).

Figure 7 | Estimating Spreads Between Assets and Liabilities by Currency – Financial System

III. Portfolio quality

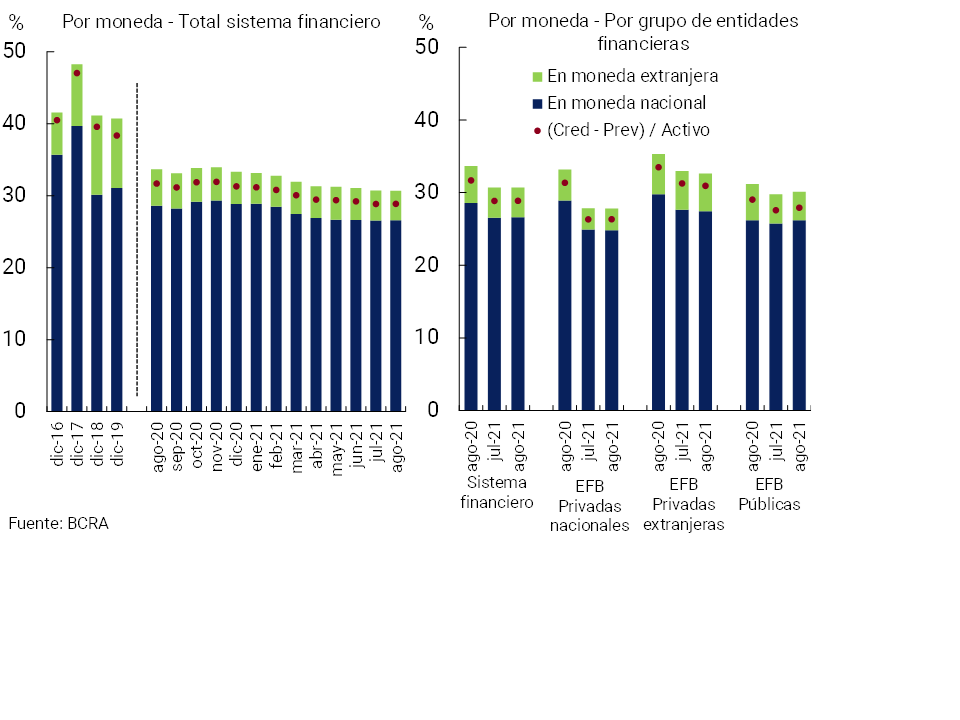

In August, the gross exposure of the financial system to the private sector (including domestic and foreign currency) stood at 30.7% of total assets13, in line with the previous month’s record (-3 p.p. y.o.y.). As in previous months, in August this ratio increased in public financial institutions, while it fell in private ones. When considering only financing in pesos, the indicator stood at 26.6%, slightly above July and without significant changes in a year-on-year comparison (-0.1 p.p. y.o.y.) (see Graph 8). In the month, the weighting of credit to the private sector in foreign currency in total assets fell slightly to 4.1% (-1.4 p.p. y.o.y.).

Figure 8 | Credit balance to the Private Sector / Assets

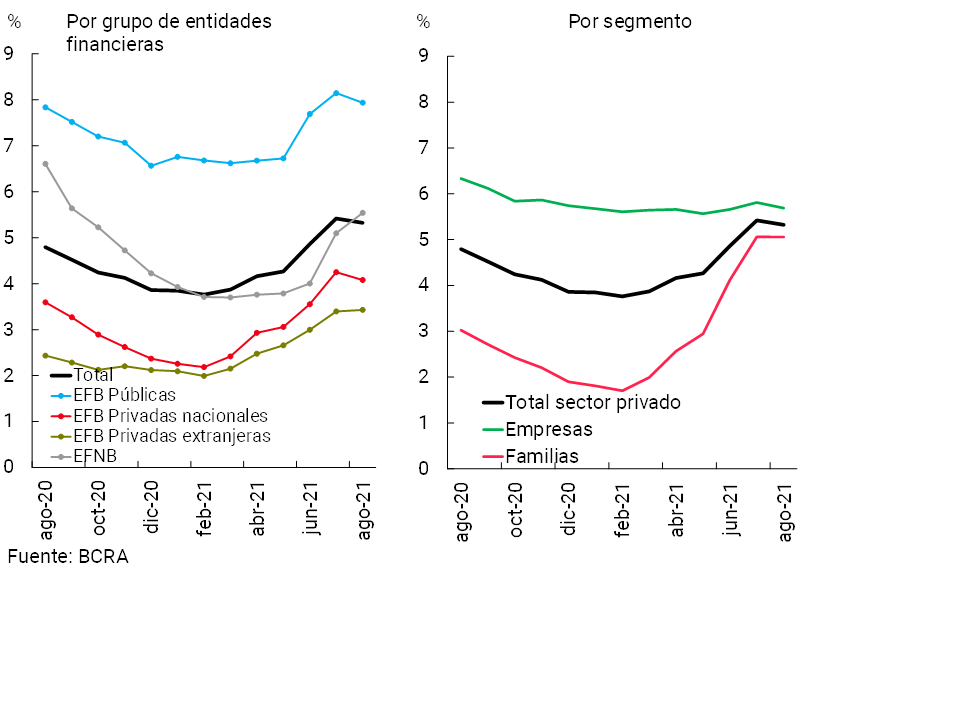

After 5 months of growth, in August the irregularity ratio of credit to the private sector fell slightly (-0.1 p.p. compared to July) to 5.3%, reflecting the combined effect of the increase in real terms in the total credit balance and the fall in real terms in the balance in an irregular situation. This monthly decline was mainly caused by public and private national financial institutions (see Graph 9). It should be considered that the evolution of this indicator since last April was partly explained by the gradual reduction and targeting of the BCRA’s financial relief measures. To date, in terms of transfer to the end of the life of the credit of unpaid contributions for debtors, the measure corresponding to the assistance granted to those who are employers covered by REPRO II14 is still in force

Figure 9 | Irregularity of credit to the private sector

Irregular financing / Total financing (%)

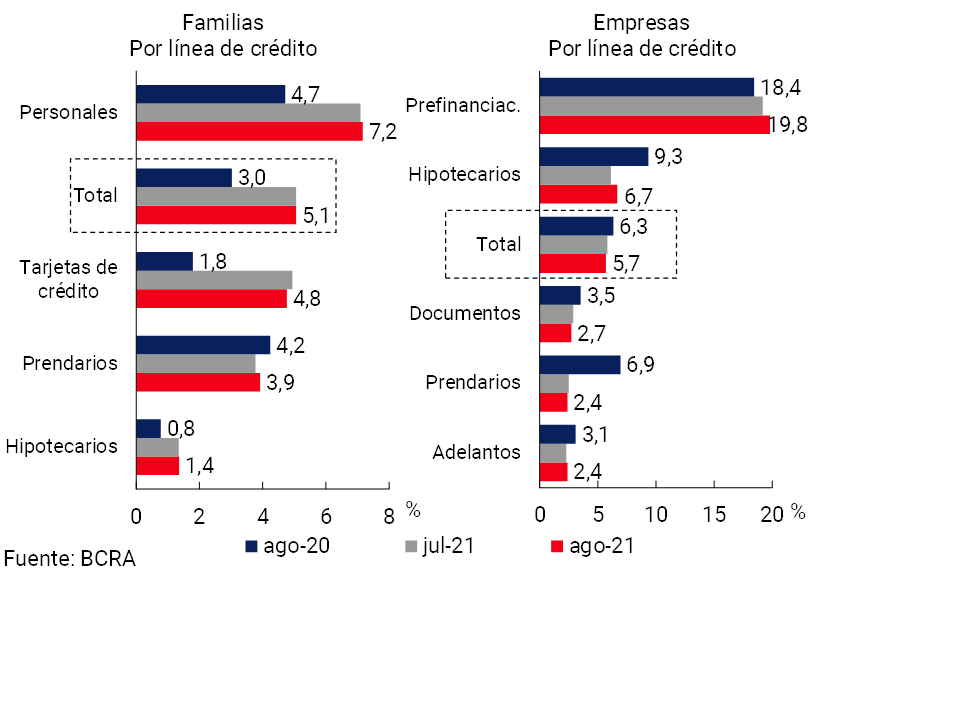

In August, the irregularity of financing to families stood at 5.1% (see Graph 10), in line with the previous month’s record (+2 p.p. y.o.y.), with no major changes among the different credit assistance. For its part, the non-performing loan ratio for companies stood at 5.7% in the period, slightly (-0.1 p.p.) below the July figure (-0.6 p.p. y.o.y.).

Figure 10 | Irregularity of credit to the private sector

Irregular financing / Total financing (%)

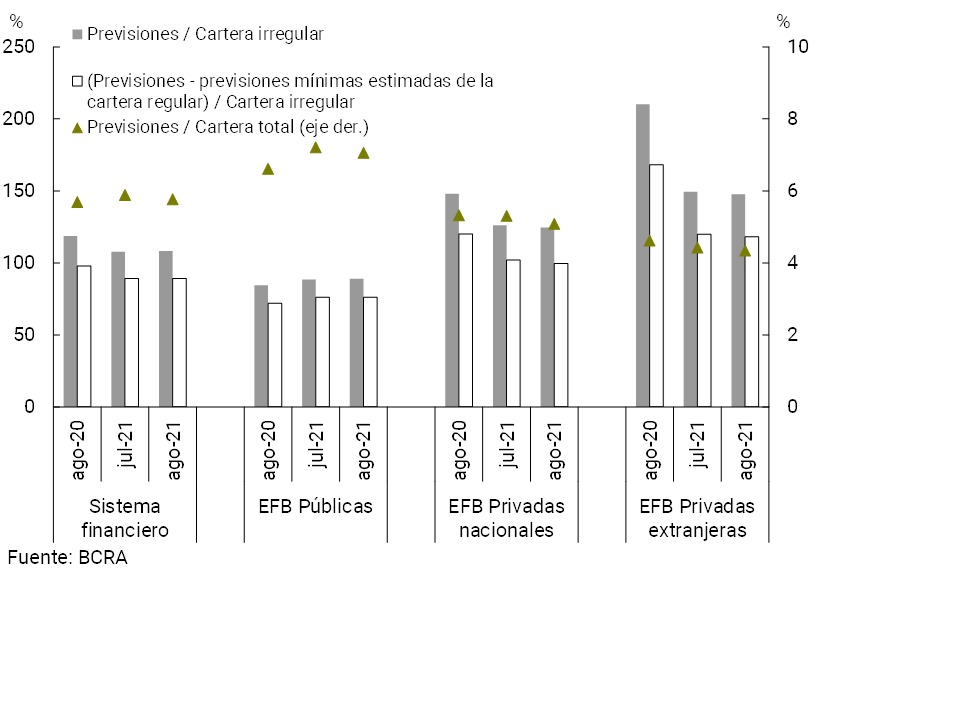

The aggregate financial system’s total forecasts accounted for 5.8% of total lending to the private sector in August, unchanged from July (-0.1 p.p.) and year-on-year (+0.1 p.p. y.o.y.) (see Graph 11). The total forecasts in terms of the non-performing portfolio stood at 108.4% in the month at the systemic level, 0.6 p.p. more than in July (-10.4 p.p. y.o.y.). For its part, in August the balance of regulatory forecasts attributable to the non-performing portfolio (following the criteria of the minimum regulatory forecasts for uncollectibility risk) represented 89.3% of said portfolio for the aggregate of entities.

Figure 11 | Credit to the private sector and forecasts

By Entity Group

IV. Liquidity and solvency

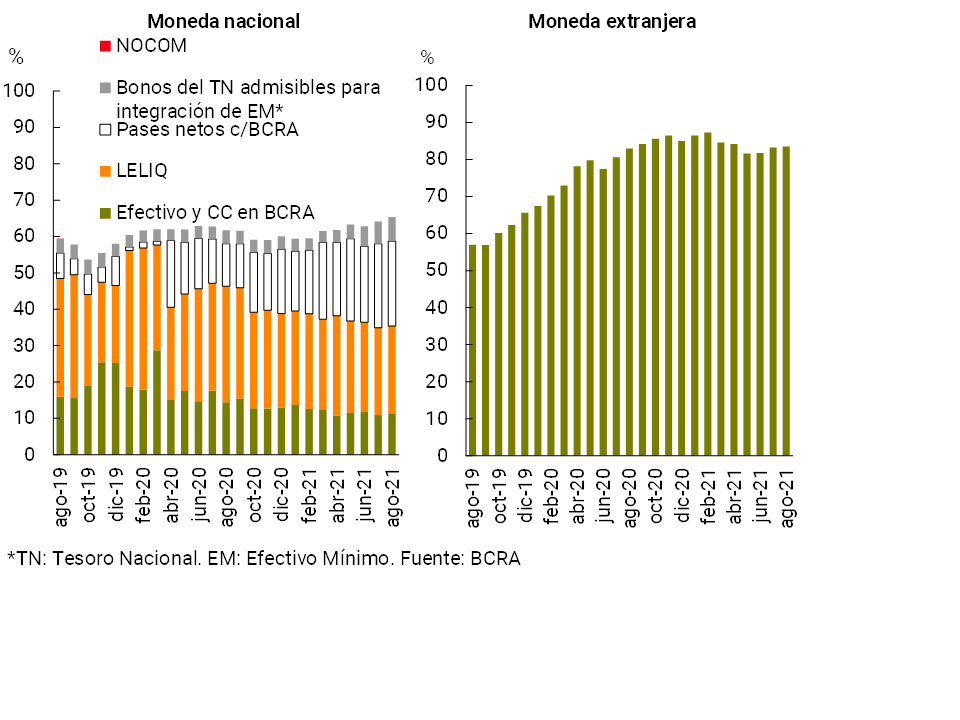

In August, the broad liquidity indicator15 of the group of entities represented 68.6% of total deposits (65.4% considering the segment in pesos and 83.5% for items in foreign currency, see Chart 12), 1 p.p. more than the level recorded in July (+1.2 p.p. for the segment in pesos and +0.2 p.p. for items in foreign currency). All components of ample liquidity in pesos increased their share in terms of total deposits between peak of the month. In the last 12 months, the broad liquidity ratio increased by 2.6 p.p. at the aggregate level, a variation driven mainly by the performance of the segment in pesos and reflected to a greater extent in national private banking entities.

Figure 12 | In % of deposits

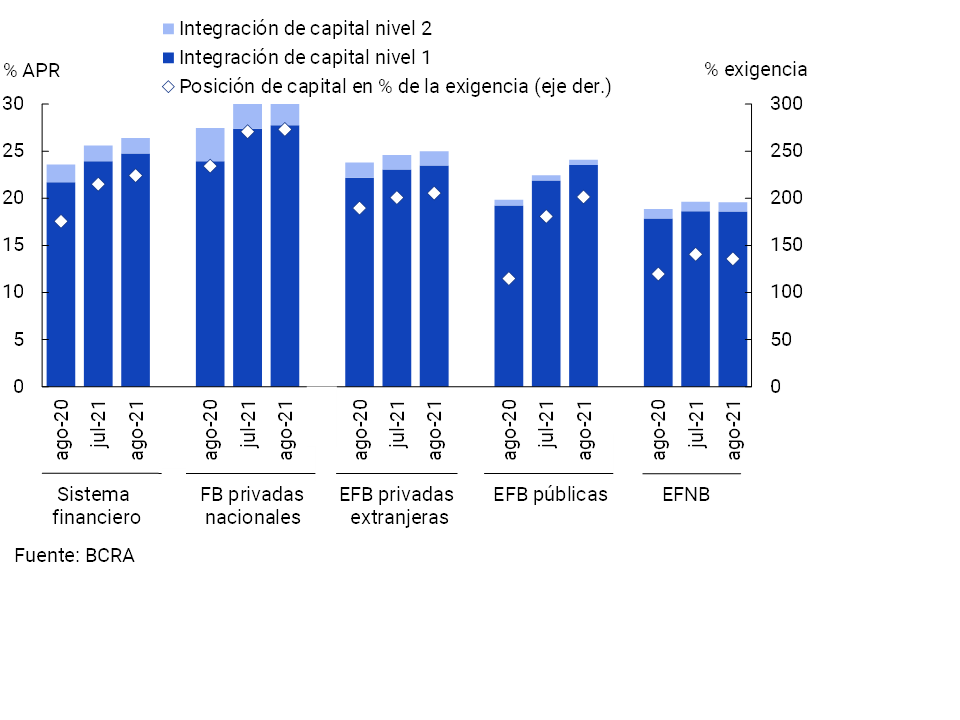

In relation to the sector’s solvency indicators, in August the integration of regulatory capital (RPC) of the financial system increased by 0.8 p.p. of risk-weighted assets (RWA), to 26.4% (+2.8 p.p. y.o.y.) (see Graph 13), generalized dynamics among the different groups of banking financial institutions. The monthly increase in this ratio was explained by a growth in the PRC of 3.3% in real terms, while RWAs increased by 0.2% in real terms in the period. Tier 1 capital integration – with a greater capacity to face eventual losses – continued to represent more than 90% of the total capital integration of the entire set of entities. The surplus capital position (CPR net of the minimum regulatory capital requirement in terms of the regulatory requirement) for the sector aggregate totaled 224% in the month, 9.2 p.p. more than in July (in a context of greater relative growth of regulatory capital above that recorded in the capital requirement) and 48.6 p.p. more than in the same period of 2020.

Figure 13 | Integration of regulatory capital

By financial institution group

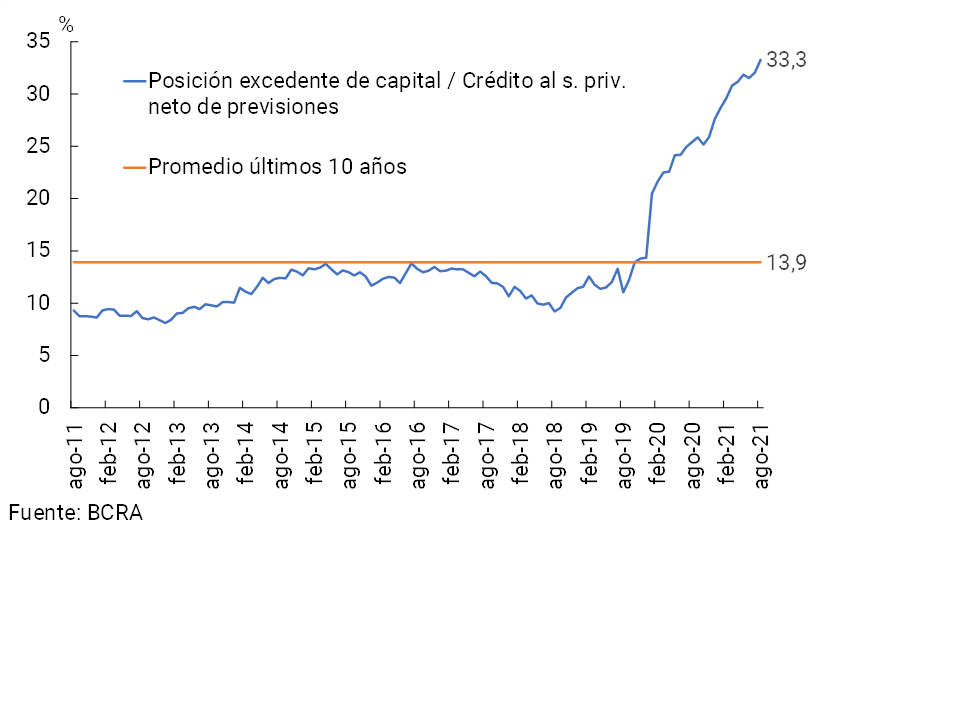

The ratio of surplus capital to credit to the private sector net of forecasts stood at 33.3% for the financial system as a whole in August, up 7.9 p.p. year-on-year and well above the average of the last 10 years (13.9%) (see Chart 14). The year-on-year evolution of this indicator reflects the combined effect of an increase in the surplus capital position (15.7% y.o.y. in real terms) and a fall in the credit net of forecasts (-11.6% y.o.y. in real terms).

Figure 14 | Surplus capital position in terms of credit to the private sector net of forecasts

Financial system

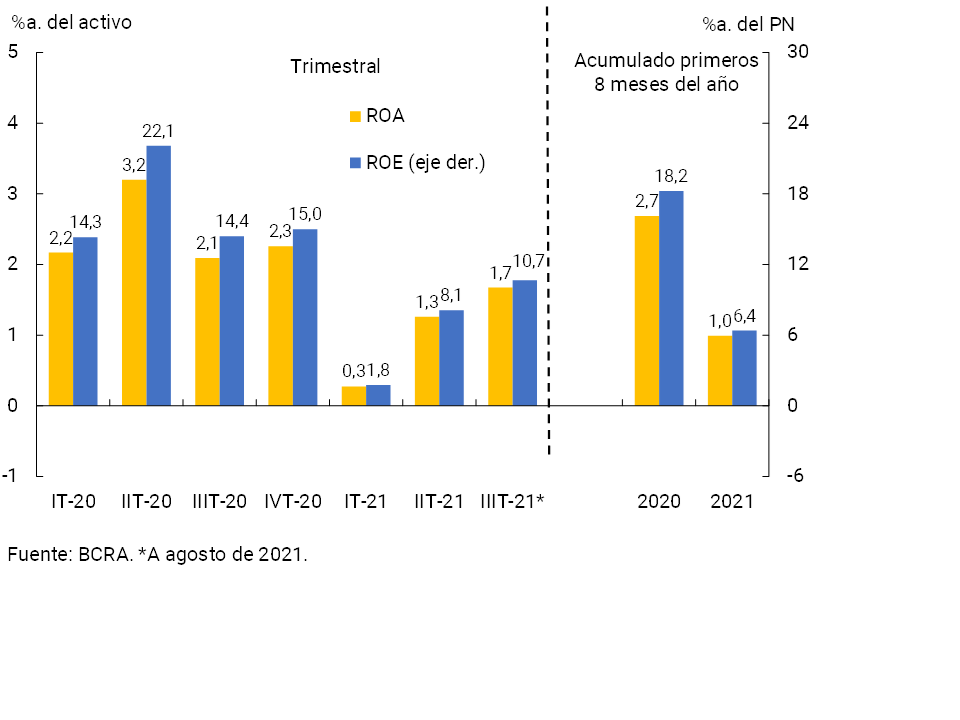

With regard to the sector’s profitability indicators, in recent months there has been a moderate increase in those monthly, although the cumulative figure for 2021 remains at levels below those observed in 2020 (see Chart 15). In the first 8 months of 2021, the total comprehensive results in homogeneous currency were equivalent to 1%y. of assets (ROA) and 6.4%y. of equity (ROE). These levels were lower than those recorded a year ago: -1.7 p.p. for ROA and -11.9 p.p. for ROE

Figure 15 | Comprehensive total profit in homogeneous currency of the financial system

V. Payment system

Electronic means of payment continued to grow at a remarkable rate in the first 9 months of the year, reflecting both the greater demand from people and the growing supply of available channels and instruments: These dynamics are in line with the incentives promoted by the BCRA in this area.

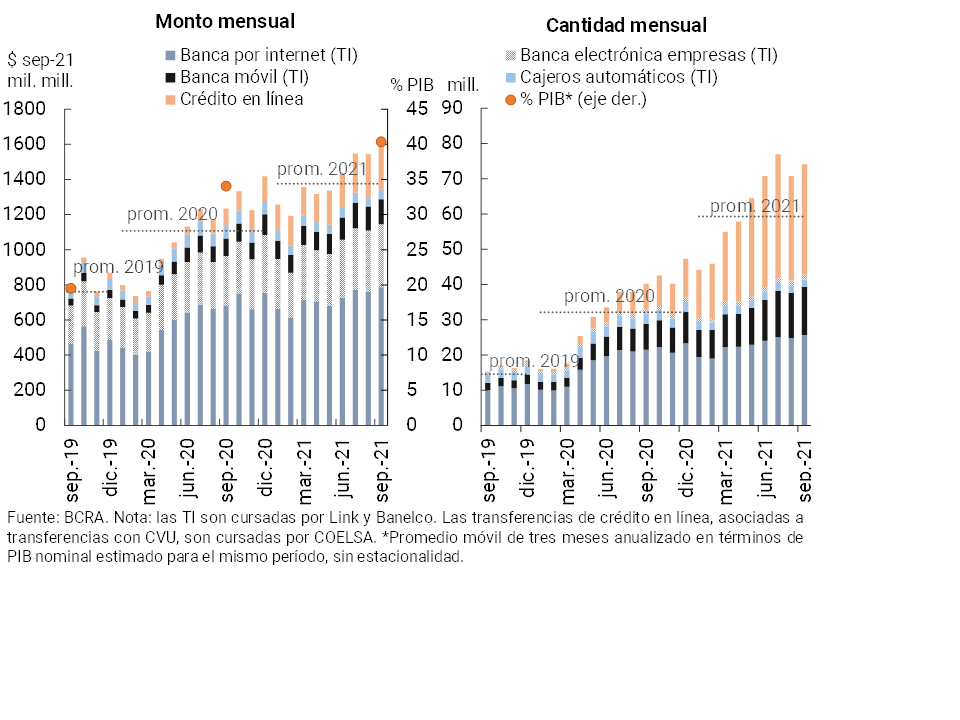

In September, online transfers (sum of immediate transfers and online credit) increased compared to the previous month, both in amounts (+4.6%) and in real amounts (+3.2%). This behavior was observed both in online credit operations and in instant transfers (TI)16. In year-on-year terms, the number of online transfers expanded by 84%, while the values did so by 28% in real terms. Thus, it is estimated that online transfers came to represent 40.4% of GDP when considering annualized amounts of the last three months (2.7 p.p. more than the same month of the previous year, see Graph 16). Within the IT segment, the year-on-year performance of Mobile Banking stood out (with increases of 85% in quantities and 44% in real amounts). Thus, these operations continue to gain share within IT, accounting for 32% of the number of operations carried out in September (9.5 p.p. more than the same month of the previous year) and 11% with respect to amounts (+2 p.p. compared to the same month of the previous year)17.

Figure 16 | Online Transfers: Immediate (TI) and Online Credit

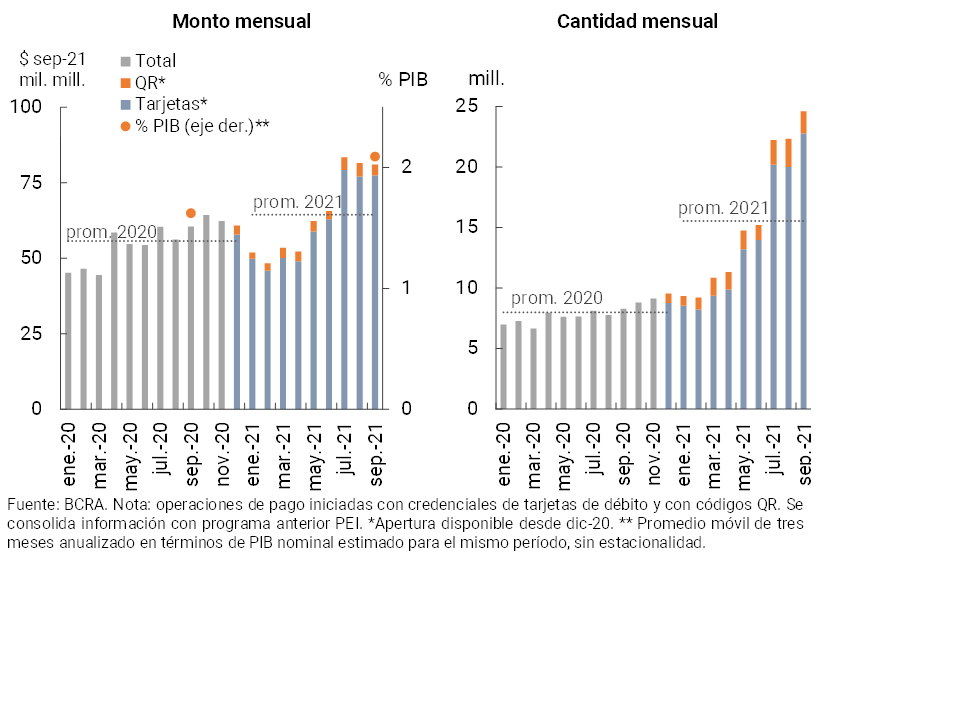

In September, the number of transfer payments increased in amounts (+10.2%) and decreased slightly in real amounts (-0.6%)18. In the month, payments initiated through cards showed a relatively greater dynamism than those made with QR. Compared to the same month of the previous year, transfers (total) increased in amounts (197.2%) and in real amounts (33.9%, see Graph 17).

Figure 17 | Transfer payments

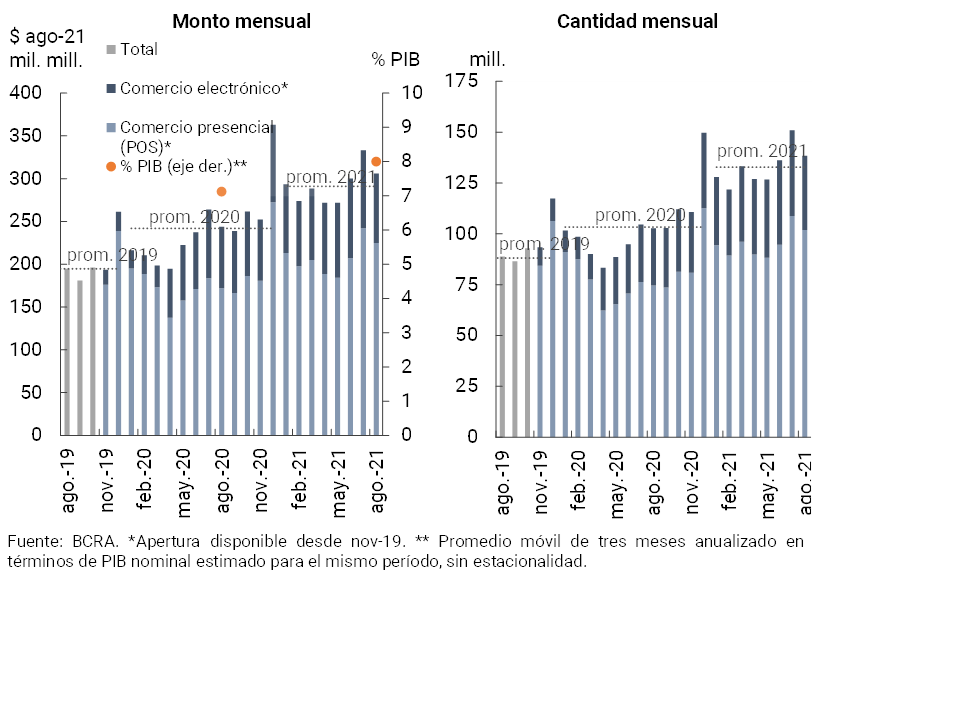

After the peaks that are usually observed in July, during August (latest available information) debit card operations decreased. In year-on-year terms, debit card transactions grew in amounts (34.7%, see Chart 18) and in real amounts (21.2%). This performance was fueled by both the dynamism of face-to-face and electronic operations. Thus, it is estimated that debit card transactions accounted for 8% of GDP (1 p.p. more than in the same month of the previous year).

Figure 18 | Debit card transactions

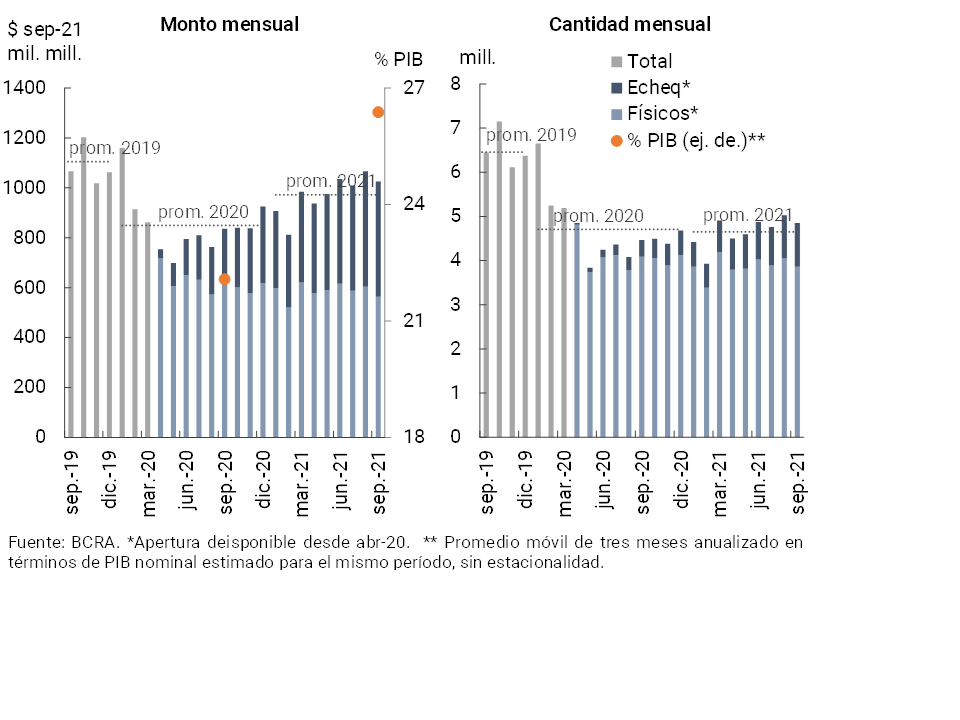

In September, the number and amount of checks cleared decreased compared to the previous month, although they are at levels higher than the average for 2021 (see Chart 19). The monthly decrease in check clearing was explained by the physical format. Compared to the same month of the previous year, the total clearing of checks increased in amounts (8.7%) and in real amounts (22.6%), a dynamism explained entirely by the ECHEQs (162% y.o.y. in quantities and 110% in real amounts). Thus, in September the ECHEQs format came to represent 20.4% of the total number of cleared checks (+12 p.p. compared to the same month of the previous year) and 45% of the total cleared amounts (+18.8 p.p. compared to the same month of the previous year). In this sense, as a result of the performance of the ECHEQs, it is estimated that in recent months the clearing of cheques increased in terms of GDP (up to 26.4%, + 4.3 p.p. y.o.y.).

Figure 19 | Check clearing

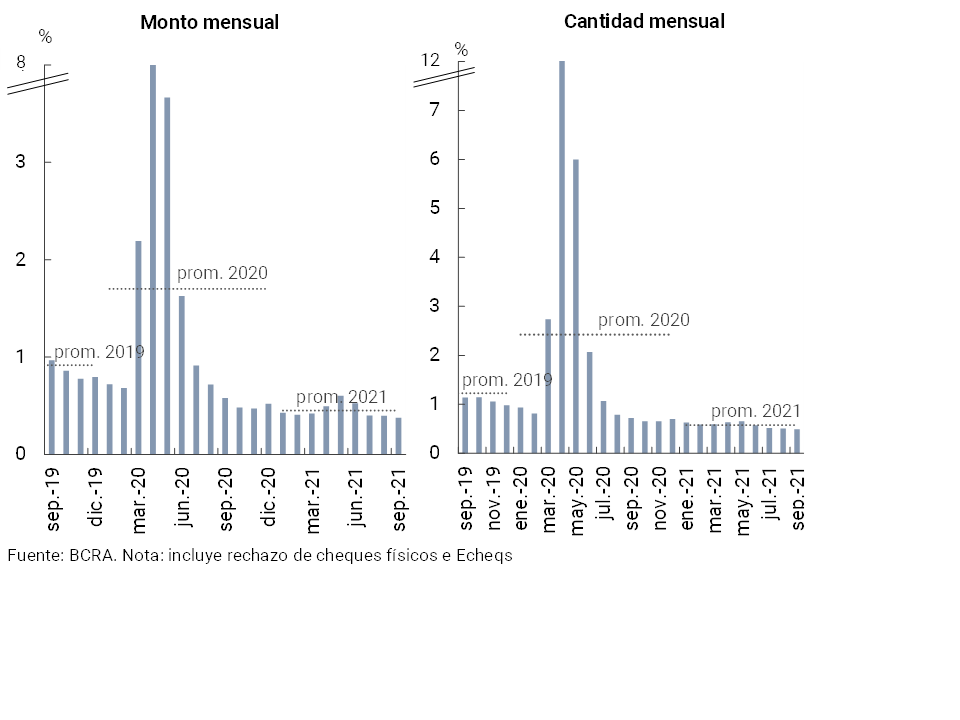

In September, the ratio of rejection of checks due to lack of funds in terms of the total compensated continued at limited levels19. This indicator decreased slightly compared to the previous month (-0.01 p.p. to 0.49% in quantities and -0.02 p.p. to 0.38% in amounts, see Graph 20), thus placing it at levels below the average for 2021. Compared to the same month of the previous year, the check rejection ratio decreased both in amounts (-0.23 p.p.) and in amounts (-0.2 p.p.).

Figure 20 | Bounce checks due to insufficient funds

Back to top

References

1 Differences in balance sheet balances expressed in homogeneous currency. Information extracted from the Monthly Accounting Information Regime (August 2021last information available at the time of publication of this Report).

2 Includes principal adjustments and accrued interest.

3 Throughout the Report, when reference is made to groups of private (national and/or foreign) and public financial institutions, it corresponds to banking entities. Non-bank entities will be referred to as “EFNBs”.

4 For more details, see Ordered text “Financing line for productive investment in MSMEs”.

5 See “Communication “A” 7369″. “Press release of 30/09/21” and “Press release of 02/10/21”.

6 For financial institutions covered that are not included in group A, the minimum percentage to be applied will be 25% of the foreseen.

7 See Communication “A” “7082” and Communication “A” “7102”.

8 See Communication “A” “7342”. According to the aforementioned communication and Communication “B” “12,209”, almost $51 million corresponds to the refinanced amount of “Zero Rate Loans 2020”.

9 See Communication “A” “6993”.

10 See Communication “A” “7082”.

11 See “Credit Conditions Survey” for the third quarter of 2021.

12 including forward purchase and sale transactions of foreign currency classified off-balance sheet.

13 This ratio reached 28.9% if the accounting balance of forecasts is subtracted.

14 See Communication “A” “6938”, Communication “A” “7107”, Communication “A” “7181”, Communication “A” “7245” and Point 2.1.1. of the Ordered Text “Financial Services in the Framework of the Health Emergency Provided for by Decree No. 260/2020 CORONAVIRUS (COVID-19)”.

15 Considers availability, integration of minimum cash and BCRA instruments, in national and foreign currency.

16 “Online credit” includes transfer transactions with instant credit associated with uniform virtual keys (CVU) that are carried out through the Electronic Clearing House for Means of Payment (COELSA). Instant transfers (TI) are operations with instant accreditation whose administration corresponds to the Link and Banelco networks.

17 MB’s operations include transfers through electronic wallets. During the month of September, the wallets corresponding to public banks continued to increase their relative participation.

18 Transfer payments represent a separate set of transactions from online transfers. They correspond to payments initiated with debit card credentials and with open QR codes, while consolidating information previously presented as Immediate Electronic Payment (PEI).

19 Considers physical checks as electronic.

Share on